UNITED

STATES

SECURITIES

AND EXCHANGE COMMISSION

WASHINGTON,

D.C. 20549

FORM

6-K

REPORT

OF FOREIGN PRIVATE ISSUER

PURSUANT

TO RULE 13a-16 OR 15d-16 UNDER

THE

SECURITIES EXCHANGE ACT OF 1934

For

the month of December 2023

Commission

File Number 001-36896

MERCURITY

FINTECH HOLDING INC.

(Registrant’s

name)

1330

Avenue of the Americas, Fl 33,

New

York, NY 10019

(Address

of principal executive office)

Indicate

by check mark whether the registrant files or will file annual reports under cover of Form 20-F or Form 40-F.

SIGNATURES

Pursuant

to the requirements of the Securities Exchange Act of 1934, the registrant has duly caused this report to be signed on its behalf by

the undersigned, thereunto duly authorized.

| |

Mercurity

Fintech Holding Inc. |

| |

|

|

| |

By: |

/s/

Shi Qiu |

| |

Name: |

Shi

Qiu |

| |

Title: |

Chief

Executive Officer |

Date:

December 28, 2023

EXHIBIT

INDEX

Exhibit

99.1— Press Release

Exhibit

99.1

New

York, NY— Mercurity Fintech Holding Inc. (the “Company,” “we,” “us,” “our company,”

or “MFH”) (Nasdaq: MFH), a digital fintech group powered by blockchain technology, today announced its unaudited financial

results for the six months ended June 30, 2023.

First

Half 2023 Financial and Operating Highlights

| ● |

GAAP

revenue - First half 2023 GAAP revenues of USD$246,242, compared to revenues of USD$783,089 in first half 2022, reflecting a decrease

of 68.56% in GAAP revenue and demonstrating the Company’s enhanced profitability and diversified revenue stream in the six

months ended June 30, 2023. |

| ● |

GAAP

gross loss - First half 2023 GAAP gross loss of USD$447,178, compared to gross loss of USD$508,695 in first half 2022, reflecting

a decrease of 12.09% in GAAP gross loss. |

| ● |

GAAP

net loss - First half 2023 GAAP net loss of USD$2,578,541, compared to net loss of USD$4,646,205 in first half 2022, reflecting a

decrease of 44.5% in GAAP net loss and demonstrating the Company’s cost management improvement. |

CONTACTS

Hoi

Yi Xian

Mercurity

Fintech Holding Inc.

ir@mercurityfintech.com

Tel:

+ 1 646 283 7120

International

Elite Capital Inc.

Vicky Chueng

Tel:

+1(646) 866-7989

Email: mfhfintech@iecapitalusa.com

Cautionary

Statement Regarding Forward Looking Statements

We

have made statements in this report that constitute forward-looking statements. Forward-looking statements involve risks and uncertainties,

such as statements about our plans, objectives, expectations, assumptions or future events. In some cases, you can identify forward-looking

statements by terminology such as “anticipate,” “estimate,” “plan,” “project,” “continuing,”

“ongoing,” “expect,” “we believe,” “we intend,” “may,” “should,”

“could” and similar expressions. These statements involve estimates, assumptions, known and unknown risks, uncertainties

and other factors that could cause actual results to differ materially from any future results, performances or achievements expressed

or implied by the forward-looking statements.

These

forward-looking statements include statements about: our business and operating strategies and plans for the development of existing

and new businesses, ability to implement such strategies and plans and expected time; developments in, or changes to, laws, regulations,

governmental policies, incentives, taxation and regulatory and policy environment affecting our operations and the cryptocurrency and

blockchain industry; our future business development, financial condition and results of operations; expected changes in our revenues,

costs or expenditures; general business, political, social and economic conditions in mainland China and the international markets we

have operations.

The

ultimate correctness of these forward-looking statements depends upon a number of known and unknown risks and events. Many factors could

cause our actual results to differ materially from those expressed or implied in our forward-looking statements. Consequently, you should

not place undue reliance on these forward-looking statements. The forward-looking statements speak only as of the date on which they

are made, and, except as required by law; we undertake no obligation to update any forward-looking statement to reflect events or circumstances

after the date on which the statement is made or to reflect the occurrence of unanticipated events.

In

addition, we cannot assess the impact of each factor on our business or the extent to which any factor, or combination of factors, may

cause actual results to differ materially from those contained in any forward-looking statements. Readers are cautioned not to place

undue reliance on these forward-looking statements, which speak only as of the date hereof. We undertake no obligation to update this

forward-looking information. Nonetheless, we reserve the right to make such updates from time to time by press release, periodic report

or other method of public disclosure without the need for specific reference to this interim report. No such update shall be deemed to

indicate that other statements not addressed by such update remain correct or create an obligation to provide any other updates.

MANAGEMENT’S

DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS

This

management’s discussion and analysis is designed to provide you with a narrative explanation of our financial condition and results

of operations for the six months ended June 30, 2022 and 2023. This section should be read in conjunction with our unaudited interim

condensed consolidated financial statements and the related notes included elsewhere in this interim report. See “Unaudited Interim

Condensed Consolidated Financial Statements of Mercurity Fintech Holding Inc as of December 31, 2022 and June 30, 2023 and for the six

months ended June 30, 2022 and 2023.” We also recommend that you read our management’s discussion and analysis and our audited

consolidated financial statements for fiscal year 2022, and the notes thereto, which appear in our annual report on Form 20-F for the

year ended December 31, 2022, or the Annual Report, filed with the U.S. Securities and Exchange Commission, or the SEC, on April 25,

2023.

Unless

otherwise indicated or the context otherwise requires, all references to “our company,” “we,” “our,”

“ours,” “us” or similar terms refer to Mercurity Fintech Holding Inc, its predecessor entities, its subsidiaries

and consolidated affiliated subsidiaries. “VIE” refers to variable interest entity.

All

such financial statements were prepared in accordance with accounting principles generally accepted in the United States, or U.S. GAAP.

We have made rounding adjustments to some of the figures included in this management’s discussion and analysis. Accordingly, numerical

figures shown as totals in some tables may not be an arithmetic aggregation of the figures that precede them. This discussion contains

forward-looking statements that involve risks, uncertainties and assumptions. Our actual results may differ materially from those anticipated

in these forward-looking statements as a result of various factors.

RECENT

DEVELOPMENTS

On

November 30, 2023, the Company priced a private investment in public equity (“PIPE”) offering, through which it sold an aggregate

of 14,251,781 units of its securities, each consisting of one (1) ordinary share and three (3) warrants, to one non-U.S. institutional

investor at an offering price of $0.421 per unit, for the gross proceeds of $6 million (the “Gross Proceeds”), prior to the

deduction of fees and offering expenses payable by the Company. The warrants are exercisable to purchase up to a total of 42,755,344

ordinary shares, for a period of three years commencing from November 30, 2023, at an exercise price of US$1.00 per ordinary share. The

Company received the PIPE financing proceeds on December 4, 2023.

Overview

Prior

to July 2019, we provided integrated B2B services to food service suppliers and customers in China. In May 2019, we acquired Mercurity

Limited and its subsidiaries and variable interest entity (“VIE”) to start blockchain technical services including developing

digital asset transaction platforms and other solutions based on blockchain technologies. On July 22, 2019, we divested our B2B services

to food service suppliers and customers by selling all the issued and outstanding shares of New Admiral Limited, or New Admiral, our

former wholly-owned subsidiary operating the B2B business, to Marvel Billion Development Limited, or Marvel Billion. After this divestment,

we are no longer engaged in B2B services and our current principal business is focused on providing blockchain technical services. We

designed and developed digital asset transaction platforms based on blockchain technologies for customers to facilitate crypto asset

trading and asset digitalization and provide supplemental services for such platforms, such as customized software development services,

maintenance services and compliance support services. In March 2020, we acquired NBpay Investment Limited and its subsidiaries and VIE,

a developer of asset transaction platform products based on blockchain technologies, to advance the blockchain technical services business.

Due

to the extremely adverse regulatory measures taken by the Chinese government in 2021 in the field of digital currency production and

transaction, our Board of Directors (“Board”) decided on December 10, 2021 to divest the VIEs, which were the Chinese operating

companies of the related business controlled through VIE agreements, and the divestiture of such VIEs was completed on January 15, 2022.

In

August 2021, we added cryptocurrency mining as one of our main businesses going forward. We entered into cryptocurrency mining pools

by executing a business contract with a collective mining service provider on October 22, 2021 to provide computing power to the mining

pool and derived USD$664,307 related revenue in 2021 and USD$783,089 related revenue in the first half of 2022.

In

late February 2022, Wei Zhu, our former acting Chief Financial Officer, former Co-Chief Executive Officer, and a former member and Co-Chairperson

of the Board, and Minghao Li, a former member of the Board, were suspected of certain criminal offenses unrelated to our company’s

operations and were detained by the Economic Crime Investigation Detachment of Sheyang County Public Security Bureau, Yancheng City,

Jiangsu Province, People’s Republic of China. At the same time, the Sheyang Public Security Bureau wrongfully seized the digital

assets hardware cold wallet which belonged to the Company, along with the cryptocurrencies stored therein.

Due

to the dismantling of the VIEs and the cessation of all business related to the digital asset transaction platforms, the temporary difficulties

we faced by the abovementioned incident where most of our cryptocurrencies were seized and impounded, the departure of our original Chinese

technical team in the first half of 2022, and because we failed to rebuild the technical service team in the second half of 2022, our

blockchain technical services business did not generate any revenue in 2022.

In

July 2022, we added digital consultation services as one of our main businesses going forward, providing business consulting services

and digital payment solutions to global corporate clients, especially those in the blockchain industry, and continued our planned expansion

into online and traditional brokerage services.

In

July 2022, we incorporated Mercurity Fintech Technology Holding Inc. (“MFH Tech”) in New York to develop distributed computing

and storage services (including cryptocurrency mining and providing cloud storage services for decentralized platform operators) and

digital consultation services.

On

December 15, 2022, we entered into an asset purchase agreement with Huangtong International Co., Ltd., providing for the acquisition

and purchase of Web3 decentralized storage infrastructure, including cryptocurrency mining servers, cables, and other electronic devices,

for an aggregate consideration of USD$5,980,000, payable in our ordinary shares. The investment was made with the aim to own mining machines

capable of gathering, processing, and storing vast amounts of data, to advance the cryptocurrency mining business, and to advance the

Web3 framework. On December 20, 2022, the assets began to be used for Filecoin (“FIL”) mining operations. In January 2023,

we transferred all of the Web3 decentralized storage infrastructure to our US subsidiary MFH Tech, which serves as the operating entity

for our business of Filecoin mining and cloud storage services for decentralized platform operators.

On

January 10, 2023, we entered into an asset purchase agreement with Jinhe Capital Limited, providing for the purchase of 5,000 Antminer

S19 PRO Bitcoin mining machines, for an aggregate consideration of USD$9,000,000.

On

January 28, 2023, we decided to write off NBpay Investment Limited and its subsidiaries, which had no meaningful assets, business or

employees.

On

April 12, 2023, we completed the incorporation of another U.S. subsidiary, Chaince Securities,Inc. (“Chaince Securities”),

which plans to develop financial advisory services, online and traditional brokerage services independently in the future. On May 3,

2023, Chaince Securities entered into a Purchase and Sale Agreement for the acquisition of all assets and liabilities of J.V. Delaney

& Associates, an investment advisory firm and FINRA licensed broker dealer.

From

April to June 2023, our management reassessed the potential adverse effects of changes in the Company’s business environment and

readjusted the Company’s business structure and the future development plan.

Considering

the increasing difficulty of mining in the crypto mining industry and the general losses by top crypto mining enterprises, we decided

to reduce the scale of procurement of Bitcoin miners and reduce the Company’s investment in the crypto mining field. As such, the

Company and Jinhe Capital Limited entered into an amendment (the “Amendment”) to the S19 Pro Purchase Agreement, pursuant

to which the parties agreed to reduce the purchase order to no more than 2,000 Bitcoin miners for a total amount of no more than $3.6

million.

Also

considering the enormous uncertainty brought by the cryptocurrency market turmoil in the past two years to the blockchain industry, as

well as the regulatory uncertainties, although we have the ability to quickly reorganize the blockchain technical service team, we have

still decided not to continue conducting blockchain technology service business related to the asset trading platform, asset digitalization

platform and decentralized finance (DeFi) platform.

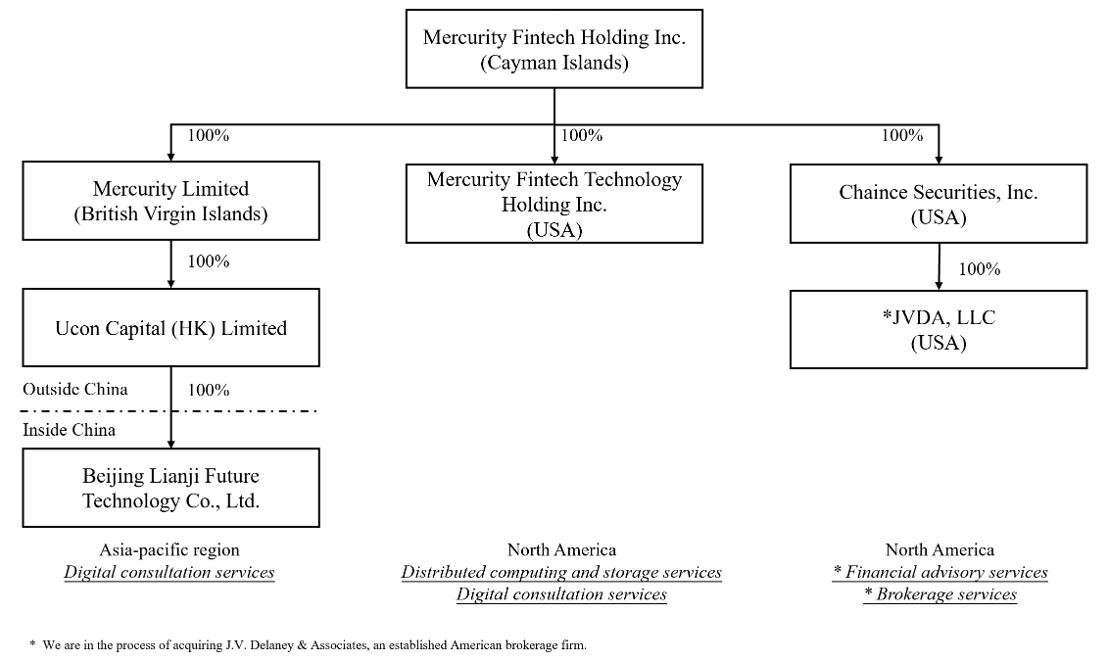

After

the adjustment of our business focuses, we have the following corporate structure and lines of business: (i) our US subsidiary MFH Tech

functions as the operating entity of distributed computing and storage services and digital consultation services business in North America,

(ii) after completing the acquisition of all assets and liabilities of J.V. Delaney & Associates, our US subsidiary Chaince Securities

(as well as its future subsidiary) will function as the operating entity of our future financial advisory services, online and traditional

brokerage services business in North America, and (iii) our Hong Kong subsidiary Ucon Capital (HK) Limited and its China subsidiary Beijing

Lianji Future Technology Co., Ltd. will function as the operating entity of our digital consultation services business in the Asia-Pacific

region.

Our

current business structure is as follows:

Note:

JVDA, LLC and Chaince Securities, Inc. were each incorporated in Delaware. JVDA, LLC will assume the business of J.V. Delaney & Associates.

Mercurity Fintech Technology Holding Inc. was incorporated in New York.

Description

of Key Statement of Operations Items

Revenue

The

table below sets forth our revenue by service types for the six months ended June 30, 2022 and 2023:

| | |

June 30, | | |

June 30, | |

| | |

2023 | | |

2022 | |

| | |

US$ | | |

US$ | |

| Revenue: | |

| | | |

| | |

| Distributed computing and storage services (i) | |

| 166,242 | | |

| 783,089 | |

| Digital consultation services (ii) | |

| 80,000 | | |

| | |

| Total revenue | |

| 246,242 | | |

| 783,089 | |

(i)

Revenue from distributed computing and storage services

The

Company’s distributed storage and computing services business includes cryptocurrency mining and cloud storage services for other

decentralized platform operators.

In

the first half of 2022, the Company’s revenue came entirely from the Bitcoin shared mining business, which began in October 2021

and ended in April 2022. During the same period, the Wei Zhu incident caused the Company to temporarily lose control of most of its cryptocurrencies,

and the Company’s daily operations also faced temporary difficulties, resulting in the Company’s original expansion plan

for cryptocurrency mining business not being implemented. It is worth mentioning that during this period, the Bitcoin market price experienced

a significant decline, and all of the Company’s Bitcoins were unable to be sold in a timely manner for cash due to loss of control.

This also led to the Company having to make significant impairment losses on these Bitcoins in the first half of 2022.

In

December 2022, the Company acquired a batch of Web3 decentralized storage infrastructure, including cryptocurrency mining servers, cables,

and other electronic devices, for an aggregate consideration of USD$5.98 million, payable in the Company’s ordinary shares. Starting

on December 20, 2022, the Company uses some of the storage capacity of these devices for Filecoin mining business, and other storage

capacity will be used to provide cloud storage services to distributed application product operators. For the six months ended June 30,

2023, the Company earned $166,242 revenue from Filecoin physical mining operations, and did not receive any revenue from providing cloud

storage services to decentralized platform operators.

On

December 5, 2023, the Company signed an Origin Storage Filecoin Mining Service Contract with Origin Storage PTE. LTD. (“Origin

Storage”). The Company will use Origin Storage’s technology to repackage the Web3 decentralized storage infrastructure and

conduct Filecoin mining business through Origin Storage’s network platform. The Filecoin mining services provided by Origin Storage

include but are not limited to storage server services, computing encapsulation server services, and technical services. Through Origin

Storage’s new technology in the Filecoin mining field, the Company is expected to improve the output efficiency of the Filecoin

mining business.

(ii)

Revenue from digital consultation services

In

the second half of 2022, the new management of the Company fully considered the huge uncertainty caused by the volatility of the cryptocurrency

market, and decided to add digital consultation services as one of our main businesses, providing business consultation services and

digital payment solutions to global corporate clients, especially those in the blockchain industry.

On

August 23, 2022, the Company signed a Consulting Agreement with a Chinese media company, pursuant to which the Company will serve as

a business consultant in order to facilitate the client to establish its operating entity in the United States and related financing

strategy, and the agreed amount of the immutable consideration portion of the agreement is $160,000. As of December 31, 2022, approximately

50% of the agreed services had been completed as scheduled, and the Company recognized consultation services revenue of $80,000 for the

year ended December 31, 2022 based on the percentage-of-completion. As of June 30, 2023, all the agreed services under this agreement

have been completed, and the Company recognized consultation services revenue of $80,000 for the six months ended June 30, 2023 based

on the percentage-of-completion.

Cost

of Revenue

The

table below sets forth our revenues by service types for the six months ended June 30, 2022 and 2023:

| | |

June 30, | | |

June 30, | |

| | |

2023 | | |

2022 | |

| | |

US$ | | |

US$ | |

| Cost of Revenue: | |

| | | |

| | |

| Distributed computing and storage services (i) | |

| (641,920 | ) | |

| (1,291,784 | ) |

| Digital consultation services (ii) | |

| (51,500 | ) | |

| | |

| Total Cost of Revenue | |

| (693,420 | ) | |

| (1,291,784 | ) |

(i)

Cost of revenue of distributed computing and storage services

The

Company carried out Bitcoin mining from October 2021 to April 2022. The Company’s computing power during this period was 35,000TH/s,

the average daily output during this period was 0.17011136 BTC, and the revenue per unit of computing power was 0.000004860 BTC/TH/day.

For this Bitcoin mining business, the Company essentially leased the Bitcoin mining machines instead of owning them, while the cost of

renting the mining machines proved to be very high. The average daily operating cost (including the cost of renting the mining machines)

of the Company’s Bitcoin mining was $110,80.51, so the Company would not make a profit until the average price of Bitcoin exceeds

$65,137. The cost of Bitcoin shared mining operations was recognized in the six months ended June 30, 2022 in the amount of $1,291,784.

However, back in October 2021, the management did not anticipate the Bitcoin market crash that would begin in December 2021. In December

2021, the price of Bitcoin suddenly plummeted from the price range of $60,000 per coin and during the first six months of 2022 such price

lingered around the range of $17,000 to $49,000, causing our Bitcoin mining business to suffer a great loss. Due to the sharp fluctuations

in the price of Bitcoin over the past two years, from May 2022 to June 2023, we did not carry out any business related to Bitcoin mining.

The

Company carried out Filecoin mining business from December 2022. As of June 30, 2023, the Company has opened two nodes on the Filecoin

blockchain with a set storage capacity of 30.2Pib, one of which has not reached the maximum set storage capacity, so the current storage

capacity of the two nodes was 25.16PiB. The operating costs of Filecoin mining business currently include depreciation costs of equipment,

site fees, electricity fees, network fees and software deployment costs. Due to the fact that the number of nodes in the Company’s

Filecoin mining business and the storage capacity of each node have not yet reached the set maximum level, the Company still receives

relatively few Filecoin rewards, and the corresponding revenue recognized by the Company is also relatively low. However, the Web3 decentralized

storage infrastructure used by the Company for Filecoin mining are depreciated based on the expected useful life using the straight-line

method, which resulted in depreciation costs far exceeding Filecoin mining revenue in the first half of 2023. The Company plans to open

another two nodes in the second half of 2023 to enable its hardware devices to release more storage capacity in exchange for revenue,

and the Company expect our storage capacity for Filecoin mining operations to reach 60.4PiB in June 2024. The cost of Filecoin mining

operations was recognized in the six months ended June 30, 2023 in the amount of $641,920.

In

December 2023, the Company began adopting new technologies to carry out filecoin mining business, and it is expected that the mining

output efficiency of filecoin will be significantly improved in 2024, and the Company’s Filecoin mining business is expected to

be profitable commencing in 2024.

(ii)

Cost of revenue of digital consultation services

In

the first half of 2023, the Company only implemented one business consultation project in its digital consulting service business. The

direct costs of the Company’s business consultation services included office space expenses, team salaries, travel expenses, printing

fees, and the fees required to acquire clients. The cost of digital consulting services operations was recognized in the six months ended

June 30, 2023 in the amount of $51,500.

Operating

Expenses

The

table below sets forth our operating expenses for the six months ended June 30, 2022 and 2023:

| |

|

June

30, |

|

|

June

30, |

|

| |

|

2023 |

|

|

2022 |

|

| |

|

US$ |

|

|

US$ |

|

| Operating Expenses: |

|

|

|

|

|

|

|

|

| Sales and marketing (i) |

|

|

(152,400) |

|

|

|

— |

|

| General and administrative

(ii) |

|

|

(1,251,559 |

) |

|

|

(1,247,161) |

|

| Provision for doubtful

accounts (iii) |

|

|

— |

|

|

|

(4,648) |

|

| Loss on disposal of intangible

assets (iv) |

|

|

— |

|

|

|

(29,968) |

|

| Impairment loss of intangible

assets (v) |

|

|

(79,821) |

|

|

|

(2,850,422) |

|

| Total Operating Expenses |

|

|

(1,483,780) |

|

|

|

(4,132,199) |

|

(i)

Sales and marketing expenses

On

January 13, 2023, the Company’s US subsidiary MFH Tech signed a Consulting Agreement with Dato Ai Technology Corporation (“Dato”),

pursuant to which Dato will provide sales and marketing services as an independent contractor in order to search for and identify potential

clients of the Company’s business consultation services. According to the Consulting Agreement, MFH Tech should pay Dato an annual

fee of $300,000. As of June 30, 2023, MFH Tech has paid Dato $150,000 and recognized the sales and marketing expenses of $150,000 for

the six months ended June 30, 2023. In addition, other marketing fees of $2,400 were recognized for MFH Tech’s business promotion

for the six months ended June 30, 2023. The Company did not generate any sales and marketing expenses directly for its main business

in the six months ended June 30, 2022.

The

definition of our main business has undergone some restructuring in recent years, and as it becomes more well-defined, and as current

structural business investments mature and begin to yield revenue, we have plans to steadily increase our marketing and promotional investment

and efforts.

(ii)

General and administrative

The

Company’s general and administrative expenses consist primarily of (i) salaries and benefits for employees, which are the salaries

and benefits for our management, merchant service representatives and general administrative staff, (ii) office expenses, which consist

primarily of office rental, maintenance and utilities expenses, depreciation of office equipment and other office expenses, and (iii)

professional expenses, which consist primarily of legal expense and audit fees.

The

Company’s general and administrative expenses were $1,251,559 for the first half of 2023, compared to $1,247,161 in the same period

of 2022. General and administrative expenses for the first half of 2023 consisted primarily of $251,747 in employment costs, $642,579

in professional fees, and $357,233 in other office expenses. General and administrative expenses for the first half of 2022 consisted

primarily of $356,173 in stock-based compensation costs, $500,196 in employment costs, $365,613 in professional fees, and $25,179 in

other office expenses.

(iii)

Provision for doubtful accounts

The

Company’s losses from provision for doubtful accounts for the six months ended June 30, 2022 were all due to other receivables

that could not be collected.

(iv)

Loss on disposal of intangible assets

In

January 2022, the Company sold 1,000,000 USD Coins to finance our daily operations and generated a loss of $29,968. No related gains

or losses occurred in the six months ended June 30, 2023.

(v)

Impairment loss of intangible assets

Due

to the price crash of Bitcoin in 2022, the Company, out of caution, decided to change the impairment test method of Bitcoin and other

cryptocurrencies from testing once or twice a year by calculating the fair value based on the average daily closing price of the past

12 months to testing every day by calculating the fair value based on the intraday low price.

The

Company evaluated the materiality of the changes from qualitative and quantitative perspectives, and concluded that the changes were

material to the unaudited interim Consolidated Statements of Operations and Cash Flows for the six months ended June 30, 2022. We restated

the impacted unaudited interim consolidated financial statements for the six months ended June 30, 2022 to correct these changes.

We

estimated the fair values of the cryptocurrencies based on the intraday low price every day and recognized $79,821 impairment loss for

the six months ended June 30, 2022, all of which was impairment loss of Filecoins.

We

estimated the fair values of the cryptocurrencies based on the intraday low price every day and recognized $2,850,422 impairment loss

for the six months ended June 30, 2022, including $2,844,558 impairment loss of Bitcoins and $5,864 impairment loss of Tether USDs.

Interest

income/(expenses), net

The

table below sets forth our interest income/(expenses) for the six months ended June 30, 2022 and 2023:

| | |

June 30, | | |

June 30, | |

| | |

2023 | | |

2022 | |

| | |

US$ | | |

US$ | |

| Interest income/(expenses), net: | |

| | | |

| | |

| Bond interest expenses (i) | |

| (186,250 | ) | |

| — | |

| Interest income from cash and short-term deposits | |

| 68,161 | | |

| 84 | |

| Interest income/(expenses), net | |

| (118,089 | ) | |

| 84 | |

(i)

Amortization of discount on bonds payable and Bond interest expenses

The

Company entered into a Securities Purchase Agreement (“SPA”) with a non-U.S. investor (the “Purchaser”). Pursuant

to the SPA dated January 31, 2023, the Company issued the Purchaser an Unsecured Convertible Promissory Note (the “Note”)

with a face value of $9 million (the “Proceeds”) upon receiving the Proceeds from the Purchaser on February 2, 2023. The

Note shall bear non-compounding interest at a rate per annum equal to 5% from the date of issuance until repayment of the Note unless

the Purchaser elects to convert the Note into ordinary shares. If the Purchaser does not elect to convert the Note, then the outstanding

principal amount and all accrued but unpaid interest on the Note shall be due and payable upon the one-year anniversary of the Issuance

Date of the Note (the “Maturity Date”). For the six months ended June 30, 2023, the Company recognized $186,250 interest

expenses for the Note.

The

Purchaser has the right to convert the outstanding balance (excluding any and all accrued but unpaid interest on the Note as of the date

of such notice) under the Note into the Company’s ordinary shares (the “Conversion Shares”) at a per share price equal

to $0.00172, (70% of the average closing price of the American Depositary Receipts divided by 360 during the 30-consecutive trading day

period immediately preceding the date of the Securities Purchase Agreement, equivalent to $0.688 per ordinary share after the share consolidation

effected on February 28, 2023) according to the terms and conditions of the Note. Prior to repayment of the Note, the Holder may, in

its sole discretion, elect to convert this Note during two select periods before the Maturity Date, including the fifteen days period

preceding the calendar date six months after the date of issuance of the Note (the “First Election Period”), as well as the

fifteen days period preceding the Maturity Date (the “Second Election Period”).

Pursuant

to the Accounting Standards Update 2020-06, for convertible instruments, the instruments primarily affected are those issued with beneficial

conversion features or cash conversion features because the accounting models for those specific features are removed. However, all entities

that issue convertible instruments are affected by the amendments to the disclosure requirements in this Update. Under the amendments

in Accounting Standards Update 2020-06, the embedded conversion features no longer are separated from the host contract for convertible

instruments with conversion features that are not required to be accounted for as derivatives under Topic 815, Derivatives and Hedging,

or that do not result in substantial premiums accounted for as paid-in capital. Consequently, a convertible debt instrument will be accounted

for as a single liability measured at its amortized cost and a convertible preferred stock will be accounted for as a single equity instrument

measured at its historical cost, as long as no other features require bifurcation and recognition as derivatives. Therefore, when the

Company received the convertible bond financing of $9 million, we recognized the debt (bonds payable) of $9 million based on the principal

and calculated interest according to the coupon interest agreed upon in the contract.

No

related income or expenses occurred in the six months ended June 30, 2022.

Financing

costs

The

table below sets forth our financing costs recognized in current expenses for the six months ended 2022 and 2023:

| | |

June 30, | | |

June 30, | |

| | |

2023 | | |

2022 | |

| | |

US$ | | |

US$ | |

| Financing costs: | |

| | | |

| | |

| Financial advisory fees for Unsecured Convertible Promissory Note | |

| (450,000 | ) | |

| — | |

| Total financing costs | |

| (450,000 | ) | |

| — | |

In

February 2023, according to the agreement with the financial advisor for the Company’s Unsecured Convertible Promissory Note with

a financing amount of $9 million, the Company paid a financial advisor fee of 5% of the financing amount to the financial advisor. No

related costs occurred in the six months ended June 30, 2022.

Other

Income

Other

income consists primarily of the gain generated from the government subsidies.

Loss

on market price of short-term investment

The

loss on market price of short-term investment for the six months ended June 30, 2023 consists primarily of the loss on the market price

changes of the ETFs held by the Company as of June 30, 2023. No related gains or losses occurred in the six months ended June 30, 2022.

Loss

from selling short-term investments

The

loss from selling short-term investments for the six months ended June 30, 2023 consists primarily of the loss from selling common stocks

held by the Company during the same period. No related gains or losses occurred in the six months ended June 30, 2022.

Loss

from disposal of subsidiaries

Due

to the extremely adverse regulatory measures taken by the Chinese government in 2021 in the field of digital currency production and

transaction, the Company’s board of Directors decided on December 10, 2021 to divest the Chinese companies of the related business

controlled through VIE agreements, and the divestiture was completed on January 15, 2022. The financial statements of the Company for

the six months ended June 30, 2022 recognized the loss from disposal of VIEs as $4,664.

Results

of Operations

The

following summary of the unaudited consolidated financial data for the periods and as of the dates indicated is qualified by reference

to, and should be read in conjunction with, our unaudited consolidated financial statements and related notes.

Our

historical results do not necessarily indicate our results to be expected for any future period.

| | |

For the six months ended June 30 | |

| | |

2023 | | |

2022 | |

| | |

(unaudited) | | |

(restated) | |

| Revenue: | |

| | | |

| | |

| Consultation services | |

| 80,000 | | |

| — | |

| Cryptocurrency mining | |

| 166,242 | | |

| 783,089 | |

| Total Revenue | |

$ | 246,242 | | |

$ | 783,089 | |

| | |

| | | |

| | |

| Cost of Revenue: | |

| | | |

| | |

| Consultation services | |

| (51,500 | ) | |

| — | |

| Cryptocurrency mining | |

| (641,920 | ) | |

| (1,291,784 | ) |

| Total Cost of Revenue | |

$ | (693,420 | ) | |

$ | (1,291,784 | ) |

| | |

| | | |

| | |

| Gross profit | |

$ | (447,178 | ) | |

$ | (508,695 | ) |

| | |

| | | |

| | |

| Operating expenses: | |

| | | |

| | |

| Sales and marketing | |

| (152,400 | ) | |

| — | |

| General and administrative | |

| (1,251,559 | ) | |

| (1,247,161 | ) |

| Provision for doubtful accounts | |

| — | | |

| (4,648 | ) |

| (Loss)/income on disposal of intangible assets | |

| — | | |

| (29,968 | ) |

| Impairment loss of intangible assets | |

| (79,821 | ) | |

| (2,850,422 | ) |

| Impairment loss of goodwill | |

| — | | |

| — | |

| Total operating expenses | |

$ | (1,483,780 | ) | |

$ | (4,132,199 | ) |

| Operating loss from continuing operations | |

$ | (1,930,958 | ) | |

$ | (4,640,894 | ) |

| | |

| | | |

| | |

| Interest income/(expenses), net | |

| (118,089 | ) | |

| 84 | |

| Financing costs | |

| (450,000 | ) | |

| — | |

| Other income/(expenses), net | |

| 70 | | |

| (731 | ) |

| Loss on market price of short-term investment | |

| (7 | ) | |

| — | |

| Loss from selling short-term investments | |

| (79,742 | ) | |

| — | |

| Loss from disposal of subsidiaries | |

| — | | |

| (4,664 | ) |

| Loss before provision for income taxes | |

$ | (2,578,726 | ) | |

$ | (4,646,205 | ) |

| Income tax benefits | |

| 185 | | |

| | |

| Loss from continuing operations | |

$ | (2,578,541 | ) | |

$ | (4,646,205 | ) |

| | |

| | | |

| | |

| Discontinued operations: | |

| | | |

| | |

| Loss from discontinued operations | |

| | | |

| | |

| Net loss | |

$ | (2,578,541 | ) | |

$ | (4,646,205 | ) |

About

Non-GAAP Financial Measures

As

a supplement to net loss, we use the non-GAAP financial measure of adjusted net loss which is U.S. GAAP net loss as adjusted to exclude

the impact of share-based compensation expenses, impairment of property and equipment, changes in fair value of contingent considerations,

and changes in fair value of derivative instruments. All adjustments are non-cash and we believe they are not reflective of our general

business performance. This non-GAAP financial measure is provided as additional information to help our investors compare business trends

among different reporting periods on a consistent basis and to enhance investors’ overall understanding of our current financial

performance and prospects for the future. This non-GAAP financial measure should not be considered in addition to or as a substitute

for or superior to U.S. GAAP net loss. In addition, our definition of adjusted net loss may be different from the definition of such

term used by other companies, and therefore comparability may be limited.

Reconciliations

of non-GAAP financial measures to U.S. GAAP financial measures are set forth in the following table:

| | |

For the six months ended June 30 | |

| | |

2023 | | |

2022 | |

| | |

| | |

(restated) | |

| Operating loss from continuing operations | |

$ | (1,930,958 | ) | |

$ | (4,640,894 | ) |

| Adjustment for share-based compensation expenses | |

| — | | |

| 356,173 | |

| Adjustment for impairment of property and equipment | |

| 79,821 | | |

| 2,850,422 | |

| Adjusted net loss (non-GAAP) | |

| (1,851,137 | ) | |

| (1,434,299 | ) |

| | |

| | | |

| | |

| Net loss attributable to Mercurity Fintech Holding Inc. | |

| (2,578,541 | ) | |

| (4,646,205 | ) |

| Adjustment for share-based compensation expenses | |

| — | | |

| 356,173 | |

| Adjustment for impairment of property and equipment | |

| 79,821 | | |

| 2,850,422 | |

| Adjustment for changes in fair value of short-term investment | |

| 7 | | |

| — | |

| Adjusted net loss attributable to Mercurity Fintech Holding Inc. (non-GAAP) | |

| (2,498,713 | ) | |

| (1,439,610 | ) |

| | |

| | | |

| | |

| Weighted average number of ordinary shares outstanding: | |

| | | |

| | |

| Basic | |

| 42,750,237 | | |

| 12,859,291 | |

| Diluted | |

| 42,750,237 | | |

| 12,859,291 | |

| | |

| | | |

| | |

| Losses per share attributable to Mercurity Fintech Holding Inc. (non-GAAP)-Basic | |

| | | |

| | |

| Net loss (non-GAAP) | |

| (0.06 | ) | |

| (0.11 | ) |

| Losses per share attributable to Mercurity Fintech Holding Inc. (non-GAAP)-Diluted | |

| | | |

| | |

| Net loss (non-GAAP) | |

| (0.06 | ) | |

| (0.11 | ) |

The

six months ended June 30, 2023 compared with the six months ended June 30, 2022

Revenues

For

the six months ended June 30, 2023, revenues were mainly comprised of revenues from the digital consultation services business of US$80,000

and the distributed computing and storage services business of US$166,242. For the six months ended June 30, 2022, revenues were mainly

comprised of revenues from the distributed computing and storage services business of US$783,089.

The

revenues from the digital consultation services business for the six months ended June 30, 2023 were all from one client of the Company’s

business consultation services. The revenues from the distributed computing and storage services business for the six months ended June

30, 2023 were all from Filecoin mining operations, while the revenues from the distributed computing and storage services business for

the six months ended June 30, 2022 were all from Bitcoin mining operations.

Cost

of revenues

For

the six months ended June 30, 2023, the cost of revenues was mainly comprised of revenues from the digital consultation services business

of US$51,500 and the distributed computing and storage services business of US$641,920. For the six months ended June 30, 2022, the cost

of revenues was mainly comprised of revenues from the distributed computing and storage services business of US$1,291,784.

The

revenues from the distributed computing and storage services business for the six months ended June 30, 2022 and 2023 were all from cryptocurrencies

mining operations, which had incurred significant losses. Please refer to “Description of Key Statement of Operations Items –

Cost of Revenues” for specific analysis.

Operating

expenses

The

Company’s operating expenses consist of sales and marketing expenses, general and administrative expenses, provision for doubtful

accounts, (loss)/income on disposal of intangible assets and impairment loss of intangible assets. The Company’s total operating

expenses were $4,132,199 and $1,483,780 for the six months ended June 30, 2022 and 2023.

The

Company paid $150,000 to a client’s referral agent for our digital consultation services business and we recognized it as sales

and marketing expenses in the unaudited interim consolidated statements of operations for the six months ended June 30, 2023. In addition,

other marketing fees of $2,400 were recognized for MFH Tech’s business promotion for the six months ended June 30, 2023. The Company

did not generate any sales and marketing expenses directly for our main business in the six months ended June 30, 2022.

The

Company’s general and administrative expenses consist primarily of (i) salaries and benefits for employees, which are the salaries

and benefits for our management, merchant service representatives and general administrative staff, (ii) office expenses, which consist

primarily of office rental, maintenance and utilities expenses, depreciation of office equipment and other office expenses, and (iii)

professional expenses, which consist primarily of legal expense and audit fees. The Company’s general and administrative expenses

were $1,251,559 for the first half of 2023, compared to $1,247,161 in the same period of 2022. General and administrative expenses for

the first half of 2023 consisted primarily of $251,747 in employment costs, $642,579 in professional fees, and $357,233 in other office

expenses. General and administrative expenses for the first half of 2022 consisted primarily of $356,173 in stock-based compensation

costs, $500,196 in employment costs, $365,613 in professional fees, and $25,179 in other office expenses.

The

Company’s losses from provision for doubtful accounts for the six months ended June 30, 2022 were all due to other receivables

that could not be collected. No losses from provision for doubtful accounts for the six months ended June 30, 2023 were recognized.

In

January 2022, the Company sold 1,000,000 USD Coins to finance our daily operations and generated a loss of $29,968. No related gains

or losses occurred in the six months ended June 30, 2023.

Due

to the price crash of Bitcoin in 2022, the Company, out of caution, decided to change the impairment test method of Bitcoin and other

cryptocurrencies from testing once or twice a year by calculating the fair value based on the average daily closing price of the past

12 months to testing every day by calculating the fair value based on the intraday low price. This is because the intraday low price

of cryptocurrencies to be utilized in calculating impairment of our cryptocurrencies is the most accurate indicator of whether it is

more likely than not that the asset is impaired. The Company evaluated the materiality of the changes from qualitative and quantitative

perspectives, and concluded that the changes were material to the unaudited interim Consolidated Statements of Operations and Cash Flows

for the six months ended June 30, 2022. We restated the impacted unaudited interim consolidated financial statements for the six months

ended June 30, 2022 to correct these changes. We estimated the fair values of the cryptocurrencies based on the intraday low price every

day and recognized $79,821 impairment loss for the six months ended June 30, 2022, all of which was impairment loss of Filecoins. We

estimated the fair values of the cryptocurrencies based on the intraday low price every day and recognized $2,850,422 impairment loss

for the six months ended June 30, 2022, including $2,844,558 impairment loss of Bitcoins and $5,864 impairment loss of Tether USDs.

While

our operating expenses currently remain relatively low, we expect, as our recent investments in future business lines capture increasing

revenues, to apply major reinvestments into the operations of all of our promising current investments and core business including R&D,

hiring expert staff, and efforts to support the further global expansion of our business.

Operating

loss

As

a result of the foregoing factors, we recorded operating loss of US$1,930,958 for six months ended June 30, 2023, compared with operating

loss of US$4,640,894 for the six months ended June 30, 2022.

Interest

income/(expenses), net

Our

interest income consists primarily of the amortization of discount on bonds payable, bond interest expenses and interest income from

our cash and short-term deposits. We generated $118,089 interest expenses, net in the six months ended 2023 and $84 interest income,

net in the six months ended 2022. Please refer to “Description of Key Statement of Operations Items – Interest income/(expenses),

net” for specific analysis.

Financing

costs

In

February 2023, according to the agreement with the financial advisor for the Company’s Unsecured Convertible Promissory Note with

a financing amount of $9 million, the Company paid a financial advisor fee of $450,000, 5% of the financing amount to the financial advisor.

No related costs occurred in the six months ended June 30, 2022.

Other

Income/(loss)

Other

income consists primarily of the gain generated from the government subsidies. We generated $70 other income in 2023 and $731 other expenses

in 2022.

Loss

on market price of short-term investment

The

loss on market price of short-term investment for the six months ended June 30, 2023 consists primarily of the loss on the market price

changes of the ETFs held by the Company as of June 30, 2023. No related gains or losses occurred in the six months ended June 30, 2022.

Loss

from selling short-term investments

The

loss from selling short-term investments for the six months ended June 30, 2023 consists primarily of the loss from selling common stocks

held by the Company during the same period. No related gains or losses occurred in the six months ended June 30, 2022.

Loss

from disposal of subsidiaries

Due

to the extremely adverse regulatory measures taken by the Chinese government in 2021 in the field of digital currency production and

transaction, the Company’s board of Directors decided on December 10, 2021 to divest the Chinese companies of the related business

controlled through VIE agreements, and the divestiture was completed on January 15, 2022. The financial statements of the Company.

Loss

before income taxes

Loss

before income taxes was US$2,578,726 for the six months ended June 30, 2023, compared with loss before income taxes of US$4,646,205 for

the six months ended June 30, 2022.

Income

tax expense/(benefits)

We

recorded income tax expense of nil and $185 for the six months ended June 30, 2022 and 2023.

The

reconciliation of tax computed by applying the statutory income tax rate of 21% applicable to the US operation, 16.5% applicable to the

Hong Kong operation, 25% applicable to the PRC operation and 17% applicable to the Singapore operation to income tax expense/(benefit)

from continuing operations for the six months ended June 30, 2023 is as follows:

| | |

For the six months ended June 30, 2023 | |

| | |

US$ | | |

US$ | | |

US$ | | |

US$ | | |

US$ | |

| | |

US | | |

Hong Kong | | |

PRC | | |

Singapore | | |

Consolidated | |

| Income/(Loss) before income taxes | |

| (869,183 | ) | |

| (4,678 | ) | |

| (70,436 | ) | |

| (507 | ) | |

| (944,804 | ) |

| Income tax computed at applicable tax rates | |

| (182,528 | ) | |

| (772 | ) | |

| (17,609 | ) | |

| (86 | ) | |

| (200,995 | ) |

| Effect of different tax rates in different jurisdictions | |

| | | |

| | | |

| | | |

| | | |

| | |

| Non-deductible expenses | |

| | | |

| | | |

| | | |

| | | |

| | |

| Current losses unrecognized deferred income tax | |

| 182,528 | | |

| | | |

| 17,609 | | |

| 86 | | |

| 200,224 | |

| Prior losses recognized deferred income tax in current period | |

| | | |

| | | |

| | | |

| | | |

| | |

| Prior income tax expense recognized in current period | |

| 587 | | |

| | | |

| | | |

| | | |

| 587 | |

| | |

| | | |

| | | |

| | | |

| | | |

| | |

| Income tax expenses/(benefits) | |

| 587 | | |

| (772 | ) | |

| — | | |

| — | | |

| (185 | ) |

Net

loss

As

a result of the foregoing factors, we recorded net loss of US$2,578,541 for the six months ended June 30, 2023, as compared to net loss

of US$4,646,205 for the six months ended June 30, 2022.

Net

loss attributable to Mercurity Fintech Holding Inc.

We

recorded net loss attributable to Mercurity Fintech Holding Inc. of US2,578,541 for the six months ended June 30, 2023, as compared to

net loss attributable to Mercurity Fintech Holding Inc. of US$4,646,205 for the six months ended June 30, 2022. We also recorded non-GAAP

net loss attributable to Mercurity Fintech Holding Inc. of US$2,498,713 for the six months ended June 30, 2023, as compared to non-GAAP

net loss attributable to Mercurity Fintech Holding Inc. of US$1,439,610 for the six months ended June 30, 2022.

Liquidity

and Capital Resources

As

a holding company with no material operations of our own, we conduct our operations primarily through our wholly- and majority-owned

subsidiaries outside mainland China.

We

had US$7,446,664 and US$13,577,030 in cash and cash equivalents as of December 31, 2022 and June 30, 2023, respectively.

Our

net losses were US$4,646,205 and US$2,578,541 for the six months ended June 30, 2022 and 2023, respectively, and our net cash used in

operating activities were US$53,391 and US$1,509,535 in the six months ended June 30, 2022 and 2023, respectively.

On

November 21, 2022, we issued 2,423,076,922 ordinary shares to three investors for the private investment in public equity (the “PIPE”)

of US$3.15 million, and issued 108,000,000 ordinary shares to pay the financing service fee of the PIPE.

On

December 20, 2022, we issued 3,676,470,589 ordinary shares to two investors for the private investment in public equity (the “PIPE”)

of US$5 million. On December 15, 2022, we entered into an asset purchase agreement with Huangtong International Co., Ltd., providing

for the acquisition and purchase of Web3 decentralized storage infrastructure, including cryptocurrency mining servers, cables, and other

electronic devices, for an aggregate consideration of USD$5,980,000, payable in our 2,718,181,818 ordinary shares. We issued the 2,718,181,818

ordinary shares on December 23, 2022.

On

December 23, 2022, we entered into a Securities Purchase Agreement in connection with a private investment in public equity (the “PIPE”)

financing with an accredited non-U.S. investor to offer and sell our units, each consisting of one ordinary share and three warrants

for total gross proceeds of USD$5 million. As of December 31, 2022, we had not yet issued the corresponding 4,545,454,546 ordinary shares

to the investor. Therefore, the Ordinary Shares in the financial statements for the year ended December 31, 2022 does not include such

unissued ordinary shares. We issued the 4,545,454,546 ordinary shares to the investor upon receiving the $5 million from the investor

on January 10, 2023.

We

entered into a Securities Purchase Agreement (“SPA”) with a non-U.S. investor (the “Purchaser”). Pursuant to

the SPA dated January 31, 2023, we issued the Purchaser an Unsecured Convertible Promissory Note (the “Note”) with a face

value of $9 million (the “Proceeds”) upon receiving the Proceeds from the Purchaser on February 2, 2023.

If

there is any change in business conditions or other future developments, including any investments we may decide to pursue, we may also

seek to sell additional equity securities or debt securities or borrow from lending institutions. Financing may be unavailable in the

amounts we need or on terms acceptable to us, if at all. The sale of additional equity securities, including convertible debt securities,

would dilute our earnings per share. The incurrence of debt would divert cash for working capital and capital expenditures to service

debt obligations and could result in operating and financial covenants that restrict our operations and our ability to pay dividends

to our shareholders. If we are unable to obtain additional equity or debt financing as required, our business operations and prospects

may suffer.

The

following table sets forth a summary of our cash flows for the periods indicated:

| | |

For the six months ended June 30 | |

| | |

2023 | | |

2022 | |

| | |

| | |

(restated) | |

| Net cash used in operating activities | |

| (1,509,535 | ) | |

| (53,391 | ) |

| Net cash used in investing activities | |

| (5,660,208 | ) | |

| — | |

| Net cash provided by/ (used in) financing activities | |

| 13,300,000 | | |

| (179,875 | ) |

| Effect of exchange rate changes | |

| (100 | ) | |

| (2,783 | ) |

| Increase/(decrease) in cash and cash equivalents | |

| 6,130,157 | | |

| (236,049 | ) |

| Cash at the beginning of the period | |

| 7,537,873 | | |

| 440,636 | |

| Cash at the end of the period | |

| 13,668,030 | | |

| 204,587 | |

Net

cash used in operating activities

Net

cash used in operating activities was US$1,509,535 for the six months ended June 30, 2023, all from continuing operations. The net cash

used in continuing operations was primarily due to: 1) Net loss from continuing operations of US$1,325,819 after excluding impairment

loss of intangible assets, depreciation of fixed assets and amortization of intangible assets, loss from selling short-term investments,

exchange gains and losses, loss on market price of short-term investment, and expenses included in financing activities; 2) Changes in

operating assets and liabilities, net of effect of acquisitions: digital assets generated from mining business of US$166,242, a decrease

in prepaid expenses and other current assets and right-of-use assets of US$167,965, a decrease in accounts payable, advance from customers

and accrued expenses and other current liabilities and lease liabilities of US$185,439.

Net

cash used in operating activities was US$53,391 for the six months ended June 30, 2022, all from continuing operations. The net cash

used in continuing operations was primarily due to:1) Net loss from continuing operations of US$1,382,523 after excluding provision for

doubtful accounts, impairment loss of intangible assets, stock-based compensation, loss from disposal of intangible assets, loss from

disposal of subsidiaries, exchange gains and losses and other income/(expenses) those non-cash items; 2) Changes in operating assets

and liabilities, net of effect of acquisitions: digital assets generated from mining business of US$783,089, a decrease in digital assets

of US$968,934, a decrease in prepaid expenses and other current assets of US$1,290,931, a decrease in accrued expenses and other current

liabilities of US$147,654.

Net

cash (used in)/provided by investing activities

Net

cash used in investing activities was US$5,660,208 for the six months ended June 30, 2023, which was primarily attributable to: Cash

from selling short-term investments of US$750,258, Received short-term investment interest of US$5,945, Cash paid for short-term investments

of US$3,136,411, Cash paid for long-term equity investments of US$160,000, Prepayments for purchasing fixed assets of US$3,000,000, and

Prepayments for acquisition of US$120,000.

Net

cash used in investing activities was nil for the six months ended June 30, 2022.

Net

cash provided by financing activities

Net

cash provided by financing activities was US$13,300,000 for the six months ended June 30, 2023, representing cash provided by private

placement of US$5 million, provided by convertible notes of US$ 9 million, and used in paying related financial advisory fees of US$700,000.

Net

cash used in financing activities was US$179,875 for the year ended December 31, 2022, representing cash provided by borrowings of US$400,000

and used in paying for debt of US$579,875.

Cash

and Cash Equivalents, and Restricted Cash

As

of June 30, 2023, the Company had cash and cash equivalents of US$13,577,030 and security deposit of US$91,000, compared with cash and

cash equivalents of US$7,446,664, security deposit of US$91,209 as of December 31, 2022.

Short-term

Investments

As

of June 30, 2023, the Company had short-term investments of US$2,306,404, which is the 6-month Certificate of Deposits of US$2,305,945

and the T-Bill ETF of US$459, compared with short-term investments of nil as of December 31, 2022.

Cryptocurrency

Assets

As

of June 30, 2023, the Company had cryptocurrency assets of US$4,319,649 in aggregate, which is the U.S. dollar equivalent of 125.8585

Bitcoins, 2,005,537.50 USD Coins, and 138,314.65 Filecoins. Among them, all of the Bitcoins and USD Coins, with a carrying amount of

US$3,944,808 as of June 30, 2023, were improperly seized by the Sheyang Public Security Bureau.

Capital

Expenditures

We

made capital expenditures, including for property and equipment, short-term investment stocks and business acquisition, of US$4,110,466

and nil for the six months ended June 30, 2023 and 2022, respectively.

Off-balance

Sheet Arrangements

As

of June 30, 2023, we did not enter into any financial guarantees or other commitments to guarantee the payment obligations of any third

parties. As of June 30, 2023, we did not enter into any derivative contracts that are indexed to our shares and classified as shareholder’s

equity or that are not reflected in our consolidated financial statements. Furthermore, as of June 30, 2023, we did not have any retained

or contingent interest in assets transferred to an unconsolidated entity that serves as credit, liquidity or market risk support to such

entity. As of June 30, 2023, we did not have any variable interest in any unconsolidated entity that provides financing, liquidity, market

risk or credit support to us or engages in leasing, hedging or product development services with us.

UNAUDITED

INTERIM CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

MERCURITY

FINTECH HOLDING INC.

INDEX

MERCURITY

FINTECH HOLDING INC.

UNAUDITED

INTERIM CONSOLIDATED STATEMENT OF FINANCIAL CONDITION

(In

U.S. dollars, except for number of shares and per share (or ADS) data)

| | |

| | |

June 30, | | |

December 31, | |

| | |

Note | | |

2023 | | |

2022 | |

| | |

| | |

| | |

| |

| ASSETS: | |

| | | |

| | | |

| | |

| Current assets: | |

| | | |

| | | |

| | |

| Cash and cash equivalents | |

| 5 | | |

| 13,577,030 | | |

| 7,446,664 | |

| Security deposit | |

| 6 | | |

| 33,700 | | |

| 33,909 | |

| Short-term investments | |

| 7 | | |

| 2,306,404 | | |

| — | |

| Prepaid expenses and other current assets,

net | |

| | | |

| — | | |

| 10,925 | |

| Amounts due from related parties | |

| 19 | | |

| 26,075 | | |

| 25,000 | |

| Assets relating to discontinued

operations | |

| | | |

| — | | |

| — | |

| Total current assets | |

| | | |

$ | 15,943,209 | | |

$ | 7,516,498 | |

| | |

| | | |

| | | |

| | |

| Non-current assets: | |

| | | |

| | | |

| | |

| Operating right-of-use assets, net | |

| 15 | | |

| 714,991 | | |

| 873,878 | |

| Property and equipment, net | |

| 8 | | |

| 5,511,769 | | |

| 5,961,173 | |

| Intangible assets, net

(including digital assets wrongfully seized and impounded by the Sheyang County Public Security Bureau of China, with a book value

of $3,944,808 as of June 30, 2023) | |

| 9 | | |

| 4,319,649 | | |

| 4,233,228 | |

| Security deposit | |

| 6 | | |

| 57,300 | | |

| 57,300 | |

| Prepayments for long-term asset | |

| 10 | | |

| 3,120,000 | | |

| — | |

| Long term equity investments | |

| 11 | | |

| 160,000 | | |

| — | |

| Deferred tax assets | |

| 16 | | |

| 251,777 | | |

| 251,005 | |

| Total non-current assets | |

| | | |

$ | 14,135,486 | | |

$ | 11,376,584 | |

| | |

| | | |

| | | |

| | |

| TOTAL

ASSETS | |

| | | |

$ | 30,078,695 | | |

$ | 18,893,082 | |

| | |

| | | |

| | | |

| | |

| LIABILITIES AND SHAREHOLDER’S

EQUITY: | |

| | | |

| | | |

| | |

| | |

| | | |

| | | |

| | |

| Current liabilities: | |

| | | |

| | | |

| | |

| Bonds payable | |

| 13 | | |

| 9,000,000 | | |

| | |

| Interest payable | |

| 14 | | |

| 186,250 | | |

| | |

| Accrued expenses and other current liabilities | |

| 12 | | |

| 151,657 | | |

| 236,490 | |

| Amounts due to related parties | |

| 19 | | |

| 914,814 | | |

| 923,596 | |

| Operating lease liabilities | |

| 15 | | |

| 338,368 | | |

| 269,675 | |

| Current liabilities

of discontinued operations | |

| | | |

| — | | |

| — | |

| Total current liabilities | |

| | | |

$ | 10,591,089 | | |

$ | 1,429,761 | |

The

accompanying notes are an integral part of these consolidated financial statements.

MERCURITY

FINTECH HOLDING INC.

UNAUDITED

INTERIM CONSOLIDATED STATEMENT OF FINANCIAL CONDITION (CONTINUED)

(In

U.S. dollars, except for number of shares and per share (or ADS) data)

| | |

| | |

June 30, | | |

December 31, | |

| | |

Note | | |

2023 | | |

2022 | |

| | |

| | |

| | |

| |

| LIABILITIES AND SHAREHOLDER’S

EQUITY (CONTINUED): | |

| | | |

| | | |

| | |

| | |

| | | |

| | | |

| | |

| Non-current liabilities: | |

| | | |

| | | |

| | |

| Operating lease liabilities | |

| 15 | | |

| 461,440 | | |

| 634,457 | |

| Total non-current liabilities | |

| | | |

$ | 461,440 | | |

$ | 634,457 | |

| | |

| | | |

| | | |

| | |

| TOTAL LIABILITIES | |

| | | |

$ | 11,052,529 | | |

$ | 2,064,218 | |

| | |

| | | |

| | | |

| | |

| Commitments and contingencies | |

| 20 | | |

| | | |

| | |

| | |

| | | |

| | | |

| | |

| Shareholders’ equity: | |

| | | |

| | | |

| | |

| Ordinary shares ($0.004 par value, 62,500,000

shares authorized as of December 31, 2022 and June 30, 2023, and 35,174,479 and 46,538,116 shares issued and outstanding as of December

31, 2022 and June 30, 2023, the above par value and number of shares as of December 31, 2022 have been restated based on the data

after the share consolidation on February 28, 2023) | |

| 17 | | |

| 186,171 | | |

| 140,716 | |

| Additional paid-in capital | |

| | | |

| 687,553,542 | | |

| 682,848,997 | |

| Accumulated deficit | |

| | | |

| (669,898,830 | ) | |

| (667,320,289 | ) |

| Accumulated other comprehensive (loss)/income | |

| | | |

| 1,185,283 | | |

| 1,159,440 | |

| Total shareholders’

equity | |

| | | |

$ | 19,026,166 | | |

$ | 16,828,864 | |

| | |

| | | |

| | | |

| | |

| TOTAL LIABILITIES AND SHAREHOLDERS’

EQUITY | |

| | | |

$ | 30,078,695 | | |

$ | 18,893,082 | |

The

accompanying notes are an integral part of these consolidated financial statements.

MERCURITY

FINTECH HOLDING INC.

UNAUDITED

INTERIM CONSOLIDATED STATEMENTS OF OPERATIONS

(In

U.S. dollars, except for number of shares and per share (or ADS) data)

| | |

| | |

For

the six months ended June 30 | |

| | |

Note | | |

2023 | | |

2022 | |

| | |

| | |

| | |

(restated) | |

| Revenue: | |

| | | |

| | | |

| | |

| Consultation services | |

| | | |

| 80,000 | | |

| — | |

| Cryptocurrency mining | |

| | | |

| 166,242 | | |

| 783,089 | |

| Total Revenue | |

| | | |

$ | 246,242 | | |

$ | 783,089 | |

| | |

| | | |

| | | |

| | |

| Cost of Revenue: | |

| | | |

| | | |

| | |

| Consultation services | |

| | | |

| (51,500 | ) | |

| — | |

| Cryptocurrency mining | |

| | | |

| (641,920 | ) | |

| (1,291,784 | ) |

| Total Cost of Revenue | |

| | | |

$ | (693,420 | ) | |

$ | (1,291,784 | ) |

| | |

| | | |

| | | |

| | |

| Gross profit | |

| | | |

$ | (447,178 | ) | |

$ | (508,695 | ) |

| | |

| | | |

| | | |

| | |

| Operating expenses: | |

| | | |

| | | |

| | |

| Sales and marketing | |

| | | |

| (152,400 | ) | |

| — | |

| General and administrative | |

| | | |

| (1,251,559 | ) | |

| (1,247,161 | ) |

| Provision for doubtful accounts | |

| | | |

| — | | |

| (4,648 | ) |

| (Loss)/income on disposal of intangible assets | |

| | | |

| — | | |

| (29,968 | ) |

| Impairment loss of intangible assets | |

| 2,

9 | | |

| (79,821 | ) | |

| (2,850,422 | ) |

| Impairment loss of goodwill | |

| | | |

| — | | |

| — | |

| Total

operating expenses | |

| | | |

$ | (1,483,780 | ) | |

$ | (4,132,199 | ) |

| Operating loss from continuing

operations | |

| | | |

$ | (1,930,958 | ) | |

$ | (4,640,894 | ) |

| | |

| | | |

| | | |

| | |

| Interest income/(expenses), net | |

| | | |

| (118,089 | ) | |

| 84 | |

| Financing costs | |

| | | |

| (450,000 | ) | |

| — | |

| Other income/(expenses), net | |

| | | |

| 70 | | |

| (731 | ) |

| Loss on market price of short-term investment | |

| | | |

| (7 | ) | |

| — | |

| Loss from selling short-term investments | |

| | | |

| (79,742 | ) | |

| — | |

| Loss from disposal of

subsidiaries | |

| | | |

| — | | |

| (4,664 | ) |

| Loss before provision for

income taxes | |

| | | |

$ | (2,578,726 | ) | |

$ | (4,646,205 | ) |

| Income tax benefits | |

| 16 | | |

| 185 | | |

| | |

| Loss from continuing operations | |

| | | |

$ | (2,578,541 | ) | |

$ | (4,646,205 | ) |

| | |

| | | |

| | | |

| | |

| Discontinued operations: | |

| | | |

| | | |

| | |

| Loss from discontinued

operations | |

| | | |

| | | |

| | |

| Net loss | |

| 2 | | |

$ | (2,578,541 | ) | |

$ | (4,646,205 | ) |

| | |

| | | |

| | | |

| | |

| Net loss attributable to

holders of ordinary shares of Mercurity Fintech Holding Inc. | |

| 2 | | |

$ | (2,578,541 | ) | |

$ | (4,646,205 | ) |

The

accompanying notes are an integral part of these consolidated financial statements.

MERCURITY

FINTECH HOLDING INC.

UNAUDITED

INTERIM CONSOLIDATED STATEMENTS OF OPERATIONS (CONTINUED)

(In

U.S. dollars, except for number of shares and per share (or ADS) data)

| | |

| | |

For

the six months ended June 30 | |

| | |

Note | | |

2023 | | |

2022 | |

| | |

| | |

| | |

| |

| Numerator | |

| | | |

| | | |

| | |

| Net loss attributable

to holders of ordinary shares of Mercurity Fintech Holding Inc. | |

| | | |

$ | (2,578,541 | ) | |

$ | (4,646,205 | ) |

| Continuing operations | |

| | | |

| (2,578,541 | ) | |

| (4,646,205 | ) |

| Discontinued operations | |

| | | |

| | | |

| | |

| | |

| | | |

| | | |

| | |

| Denominator | |

| | | |

| | | |

| | |

| Weighted average shares used in calculating

basic net loss per ordinary share | |

| 2 | | |

| 42,750,237 | | |

| 12,859,291 | |

| Weighted average shares used in calculating

diluted net loss per ordinary share | |

| 2 | | |

| 42,750,237 | | |

| 12,859,291 | |

| | |

| | | |

| | | |

| | |

| Net Loss per ordinary share | |

| | | |

| | | |

| | |

| Basic | |

| 2 | | |

| (0.06 | ) | |

| (0.36 | ) |

| Diluted | |

| 2 | | |

| (0.06 | ) | |

| (0.36 | ) |

| Net Loss per ordinary share

from continuing operation | |

| | | |

| | | |

| | |

| Basic | |

| 2 | | |

| (0.06 | ) | |

| (0.36 | ) |

| Diluted | |

| 2 | | |

| (0.06 | ) | |

| (0.36 | ) |

| Net Loss per ordinary share

from discontinued operation | |

| | | |

| | | |

| | |

| Basic | |

| 2 | | |

| — | | |

| — | |

| Diluted | |

| 2 | | |

| — | | |

| — | |

The

accompanying notes are an integral part of these consolidated financial statements

MERCURITY

FINTECH HOLDING INC.

UNAUDITED

INTERIM CONSOLIDATED STATEMENTS OF OPERATIONS (CONTINUED)

(In

U.S. dollars, except for number of shares and per share (or ADS) data)

| |

|

|

Note |

| |

For

the six months ended June 30 | |

| |

|

|

|

| |

2023 | | |

2022 | |

| |

|

|

|

| |

| | |

| |

| Net loss |

|

|

|

| |

$ | (2,578,541 | ) | |

$ | (4,646,205 | ) |

| Change in cumulative

foreign currency trans adjustment |

|

|

|

| |

| 25,843 | | |

| 19,683 | |

| Comprehensive loss |

|

|

|

| |

$ | (2,552,698 | ) | |

$ | (4,626,522 | ) |

The

accompanying notes are an integral part of these consolidated financial statements.

MERCURITY

FINTECH HOLDING INC.

UNAUDITED

INTERIM CONSOLIDATED STATEMENTS OF CHANGES IN SHAREHOLDERS’ EQUITY

(In

U.S. dollars, except for number of shares and per share (or ADS) data)

| | |