false

0001843162

0001843162

2024-02-20

2024-02-20

iso4217:USD

xbrli:shares

iso4217:USD

xbrli:shares

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM 8-K

CURRENT REPORT

Pursuant to Section 13 or 15(d) of the Securities

Exchange Act of 1934

Date of Report (Date of earliest event reported):

February 20, 2024

Silver Spike Investment Corp.

(Exact name of Registrant as Specified in Its Charter)

| Maryland |

001-40564 |

86-2872887 |

(State or Other Jurisdiction

of Incorporation) |

(Commission File Number) |

(IRS Employer

Identification No.) |

600 Madison Avenue, Suite 1800

New York, New York |

10022 |

| (Address of Principal Executive Offices) |

(Zip Code) |

Registrant’s Telephone Number, Including

Area Code: (212) 905-4923

Not Applicable

(Former Name or Former Address, if Changed Since

Last Report)

Check the appropriate box below if the Form 8-K filing is intended

to simultaneously satisfy the filing obligation of the registrant under any of the following provisions (see General Instructions A.2.

below):

| ☒ |

Written communications pursuant to Rule 425 under the Securities Act (17 CFR 230.425) |

| ☐ |

Soliciting material pursuant to Rule 14a-12 under the Exchange Act (17 CFR 240.14a-12) |

| ☐ |

Pre-commencement communications pursuant to Rule 14d-2(b) under the Exchange Act (17 CFR 240.14d-2(b)) |

| ☐ |

Pre-commencement communications pursuant to Rule 13e-4(c) under the Exchange Act (17 CFR 240.13e-4(c)) |

Securities registered pursuant to Section 12(b) of the Act:

| Title of each class |

Trading Symbol(s) |

Name of each exchange on which registered |

| Common Stock, $0.01 par value per share |

SSIC |

The Nasdaq Stock Market LLC |

Indicate by check mark whether the registrant is an emerging growth

company as defined in Rule 405 of the Securities Act of 1933 or Rule 12b-2 of the Securities Exchange Act of 1934. Emerging growth company

☒

If an emerging growth company, indicate by check mark if the registrant

has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant

to Section 13(a) of the Exchange Act.

Item 7.01. Regulation FD Disclosure

On

February 20, 2024, Silver Spike Investment Corp. (the “Company”) issued a press release announcing the broadening of the Company’s

investment strategy. A copy of the press release is furnished herewith as Exhibit 99.1.

On

February 20, 2024, the Company issued a press release announcing the Company’s entry into an agreement with Chicago Atlantic Loan

Portfolio, LLC (“CALP”) to acquire a loan portfolio from CALP (the “Loan Portfolio Acquisition”). A copy of the

press release is furnished herewith as Exhibit 99.2.

On

February 20, 2024, the Company provided an investor presentation in connection with the Loan Portfolio Acquisition. A copy of the investor

presentation is furnished herewith as Exhibit 99.3.

The

information in Item 7.01 of this Current Report on Form 8-K, including Exhibits 99.1, 99.2 and 99.3 furnished herewith, is being furnished

and shall not be deemed “filed” for any purpose of Section 18 of the Securities Exchange Act of 1934, as amended (the “Exchange

Act”), or otherwise subject to the liabilities of such section. The information in Item 7.01 of this Current Report on Form 8-K

shall not be deemed to be incorporated by reference into any filing under the Securities Act of 1933, as amended (the “Securities

Act”) or the Exchange Act, except as shall be expressly set forth by specific reference in such filing.

Forward-Looking Statements

Some

of the statements in this Current Report on Form 8-K constitute forward-looking statements because they relate to future events, future

performance or financial condition of the Company or the Loan Portfolio Acquisition. The forward-looking statements may include statements

as to: future operating results of the Company and distribution projections; business prospects of the Company and the prospects of its

portfolio companies; and the impact of the investments that the Company expects to make. In addition, words such as “may,”

“might,” “will,” “intend,” “should,” “could,” “can,” “would,”

“expect,” “believe,” “estimate,” “anticipate,” “predict,” “potential,”

“plan” or similar words indicate forward-looking statements, although not all forward-looking statements include these words.

The forward-looking statements contained in this Current Report on Form 8-K involve risks and uncertainties. Certain factors could cause

actual results and conditions to differ materially from those projected, including the uncertainties associated with (i) the timing or

likelihood of the Loan Portfolio Acquisition closing; (ii) the ability to realize the anticipated benefits of the Loan Portfolio Acquisition;

(iii) the percentage of Company stockholders voting in favor of the proposals submitted for their approval; (iv) the possibility that

competing offers or acquisition proposals will be made; (v) the possibility that any or all of the various conditions to the consummation

of the Loan Portfolio Acquisition may not be satisfied or waived; (vi) risks related to diverting management’s attention from ongoing

business operations; (vii) the risk that stockholder litigation in connection with the Loan Portfolio Acquisition may result in significant

costs of defense and liability; (viii) changes in the economy, financial markets and political environment, including the impacts of inflation

and rising interest rates; (ix) risks associated with possible disruption in the operations of the Company or the economy generally due

to terrorism, war or other geopolitical conflict (including the current conflict between Russia and Ukraine), natural disasters or global

health pandemics, such as the COVID-19 pandemic; (x) future changes in laws or regulations (including the interpretation of these laws

and regulations by regulatory authorities); (xi) changes in political, economic or industry conditions, the interest rate environment

or conditions affecting the financial and capital markets that could result in changes to the value of the Company’s assets; (xii)

elevating levels of inflation, and its impact on the Company, on its portfolio companies and on the industries in which it invests; (xiii)

the Company’s plans, expectations, objectives and intentions, as a result of the Loan Portfolio Acquisition; (xiv) the future operating

results and net investment income projections of the Company; (xv) the ability of Silver Spike Capital, LLC (the “Adviser”)

to locate suitable investments for the Company and to monitor and administer its investments; (xvi) the ability of the Adviser or its

affiliates to attract and retain highly talented professionals; (xvii) the business prospects of the Company and the prospects of its

portfolio companies; (xviii) the impact of the investments that the Company expects to make; (xix) the expected financings and investments

and additional leverage that the Company may seek to incur in the future; (xx) conditions in the Company’s operating areas, particularly

with respect to business development companies or regulated investment companies; (xxi) the ability of CALP to obtain the necessary consents

for, or otherwise identify and obtain additional loans for including in the CALP Loan Portfolio; (xxii) the regulatory requirements applicable

to the transaction and any changes to the transaction necessary to comply with

such requirements; (xxiii)

the satisfaction or waiver of the conditions to the consummation of the transaction, and the possibility in that in connection that the

closing will not occur or that it will be significantly delayed; (xxiv) the realization generally of the anticipated benefits of the Loan

Portfolio Acquisition and the possibility that the Company will not realize those benefits, in part or at all; (xxv) the performance of

the loans included in the CALP Loan Portfolio, and the possibility of defects or deficiencies in such loans notwithstanding the diligence

performed by the Company and its advisors; (xxvi) the ability of the Company to realize cost savings and other management efficiencies

in connection with the transaction as anticipated; (xxvii) the reaction of the trading markets to the transaction and the possibility

that a more liquid market or more extensive analyst coverage will not develop for the Company as anticipated; (xxviii) the reaction of

the financial markets to the transaction and the possibility that the Company will not be able to raise capital as anticipated; (xxix)

the diversion of management’s attention from the Company’s ongoing business operations; (xxx) the risk of stockholder litigation

in connection with the transaction; (xxxi) the strategic, business, economic, financial, political and governmental risks and other risk

factors affecting the business of the Company and the companies in which it is invested as described in the Company’s public filings

with the SEC; and (xxxii) other considerations that may be disclosed from time to time in the Company’s publicly disseminated documents

and filings. The Company has based the forward-looking statements included in this Current Report on Form 8-K on information available

to it on the date of this Current Report on Form 8-K, and it assumes no obligation to update any such forward-looking statements. Although

the Company undertakes no obligation to revise or update any forward-looking statements, whether as a result of new information, future

events or otherwise, you are advised to consult any additional disclosures that the Company may make directly to you or through reports

that the Company in the future may file with the Securities and Exchange Commission (the “SEC”), including the Proxy Statement/Prospectus

(as defined below), annual reports on Form 10-K, quarterly reports on Form 10-Q and current reports on Form 8-K.

Additional Information and Where to

Find It

This

Current Report on Form 8-K relates to a proposed business combination involving the Company and CALP, along with the related proposals

for which stockholder approval will be sought. In connection with the proposals, the Company intends to file relevant materials with the

SEC, including a registration statement on Form N-14, which will include a proxy statement and a prospectus of the Company (the “Proxy

Statement/Prospectus”). This Current Report on Form 8-K does not constitute an offer to sell or the solicitation of an offer to

buy any securities or a solicitation of any vote or approval. No offer of securities shall be made except by means of a prospectus meeting

the requirements of Section 10 of the Securities Act of 1933, as amended. STOCKHOLDERS OF THE COMPANY ARE URGED TO READ THE PROXY STATEMENT/PROSPECTUS,

AND OTHER DOCUMENTS THAT ARE FILED OR WILL BE FILED WITH THE SEC, AS WELL AS ANY AMENDMENTS OR SUPPLEMENTS TO THESE DOCUMENTS, CAREFULLY

AND IN THEIR ENTIRETY WHEN THEY BECOME AVAILABLE BECAUSE THEY WILL CONTAIN IMPORTANT INFORMATION ABOUT THE COMPANY, THE LOAN PORTFOLIO

ACQUISITION AND THE PROPOSALS. Investors and security holders will be able to obtain the documents filed with the SEC free of charge

at the SEC’s website, www.sec.gov, or from the Company’s website at ssic.silverspikecap.com.

Participants in the Solicitation

The

Company and its directors, executive officers and certain other members of management and employees of the Adviser and its affiliates

may be deemed to be participants in the solicitation of proxies from the stockholders of the Company in connection with the Loan Portfolio

Acquisition. Information regarding the persons who may, under the rules of the SEC, be considered participants in the solicitation of

the Company stockholders in connection with the Loan Portfolio Acquisition will be contained in the Proxy Statement/Prospectus when such

document becomes available. This document may be obtained free of charge from the sources indicated above.

No Offer or Solicitation

This

Current Report on Form 8-K is not, and under no circumstances is it to be construed as, a prospectus or an advertisement and the communication

of this Current Report on Form 8-K is not, and under no circumstances is it to be construed as, an offer to sell or a solicitation of

an offer to purchase any securities in the Company or in any fund or other investment vehicle managed by the Adviser or any of its affiliates.

Item 9.01. Financial Statements and Exhibits

(d) Exhibits

SIGNATURES

Pursuant to the requirements of the Securities Exchange Act of 1934,

the registrant has duly caused this report to be signed on its behalf by the undersigned thereunto duly authorized.

| |

Silver Spike Investment Corp. |

| |

|

| February 20, 2024 |

By: |

/s/ Umesh Mahajan |

| |

|

Name: |

Umesh Mahajan |

| |

|

Title: |

Chief Financial Officer |

Exhibit 99.1

SILVER SPIKE

INVESTMENT CORP. ANNOUNCES A BROADENING OF ITS INVESTMENT STRATEGY

NEW YORK, February

20, 2024 (GLOBE NEWSWIRE) — Silver Spike Investment Corp. (“Silver Spike” or the “Company”) (Nasdaq: SSIC),

a specialty finance company that has elected to be treated as a business development company, today announced that the board of directors

of Silver Spike has unanimously approved an expansion of Silver Spike’s investment strategy to permit investments in companies

outside of the cannabis and health and wellness sectors that otherwise meet the Company’s current investment criteria.

While the cannabis

sector will continue to be a focus of Silver Spike’s investment efforts, Silver Spike believes that the broadened investment strategy

will benefit Silver Spike and its stockholders by enabling Silver Spike to take advantage of investment opportunities outside of the

cannabis and health and wellness sectors that offer attractive risk-adjusted returns.

The investment strategy

change is expected to become effective on or about April 22, 2024.

About Silver

Spike Investment Corp.

Silver Spike is

a specialty finance company that has elected to be regulated as a business development company under the Investment Company Act of 1940,

as amended. Silver Spike’s investment objective is to maximize risk-adjusted returns on equity for its shareholders by investing

primarily in direct loans to privately held middle-market companies, with a focus on cannabis companies and other companies in the health

and wellness sector. Silver Spike is managed by Silver Spike Capital, LLC, an investment manager focused on the cannabis and alternative

health and wellness industries. For more information, please visit ssic.silverspikecap.com.

Forward-Looking

Statements

Certain

information contained herein may constitute “forward-looking statements” that involve substantial risks and uncertainties.

Such statements involve known and unknown risks, uncertainties and other factors and undue reliance should not be placed thereon. These

forward-looking statements are not historical facts, but rather are based on current expectations, estimates and projections about the

Company, its current and prospective portfolio investments, its industry, its beliefs and opinions, and its assumptions. Words such as

“anticipates,” “expects,” “intends,” “plans,” “will,” “may,”

“continue,” “believes,” “seeks,” “estimates,” “would,” “could,”

“should,” “targets,” “projects,” “outlook,” “potential,” “predicts”

and variations of these words and similar expressions are intended to identify forward-looking statements. These statements are not guarantees

of future performance and are subject to risks, uncertainties and other factors, some of which are beyond the Company’s control

and difficult to predict and could cause actual results to differ materially from those expressed or forecasted in the forward-looking

statements including, without limitation, the risks, uncertainties and other factors identified in the Company’s filings with the

SEC. Investors should not place undue reliance on these forward-looking statements, which apply only as of the date on which the Company

makes them. The Company does not undertake any obligation to update or revise any forward-looking statements or any other information

contained herein, except as required by applicable law.

Contacts

Investors:

Bill Healy

Bill@silverspikecap.com

212-905-4933

Exhibit 99.2

SILVER SPIKE

INVESTMENT CORP. ANNOUNCES AGREEMENT TO ACQUIRE LOAN PORTFOLIO FROM CHICAGO ATLANTIC

NEW YORK, February

20, 2024 (GLOBE NEWSWIRE) — Silver Spike Investment Corp. (the “Company”) (Nasdaq: SSIC), a specialty finance company

that has elected to be treated as a business development company, today announced that it entered into a definitive agreement with Chicago

Atlantic Loan Portfolio, LLC (“CALP”) for the purchase (the “Loan Portfolio Acquisition”) from CALP of a sizeable

portfolio of loans (the “CALP Loan Portfolio”). The Company will acquire the CALP Loan Portfolio in exchange for newly issued

shares of the Company’s common stock with a net asset value equal to the value of the CALP Loan Portfolio, each determined shortly

before closing. The Loan Portfolio Acquisition is consistent with the Company’s new, broadened investment strategy, separately

announced today.

The closing of the

Loan Portfolio Acquisition is subject to certain customary closing conditions. Assuming satisfaction of the conditions to the transaction,

the Loan Portfolio Acquisition is expected to close in mid-2024.

As of January 1,

2024, the CALP Loan Portfolio comprised 24 loans with an aggregate value of approximately $130 million. CALP has agreed to use reasonable

best efforts to add 4 loans with an aggregate value of approximately $43 million to the CALP Loan Portfolio prior to the closing of the

Loan Portfolio Acquisition. The Company and CALP may also agree to the addition of other loans to the CALP Loan Portfolio prior to the

closing of the Loan Portfolio Acquisition. The addition of certain loans to the CALP Loan Portfolio requires third-party consents, and/or

such loans may need to be acquired by CALP, and there can be no assurance that any additional loans will be added to the CALP Loan Portfolio

prior to the closing of the Loan Portfolio Acquisition. Certain loans may also be removed from the CALP Loan Portfolio upon the agreement

of the Company and CALP, or upon the repayment of the loans. The pro-forma information presented herein is based on data of the Company

data as of September 30, 2023 and CALP Loan Portfolio data as of January 1, 2024.

Based on CALP Loan

Portfolio data as of January 1, 2024, following the closing of the Loan Portfolio Acquisition, the Company is expected to have approximately

$213 million in net assets, and investments in approximately 27 portfolio companies. As of the closing of the Loan Portfolio Acquisition,

CALP is expected to own the majority of the Company’s common stock.

The Loan Portfolio

Acquisition was unanimously approved by the board of directors of the Company (the “Board”), upon the recommendation of its

special committee consisting solely of independent directors, which separately approved the transaction.

The Company’s

present officers will continue to be a part of the Company’s management team following the Loan Portfolio Acquisition.

Scott Gordon, Chairman

and Chief Executive Officer of the Company, said “We are very excited to announce the agreement for the Loan Portfolio Acquisition.

We believe that the Loan Portfolio Acquisition is a compelling transaction that will enhance value for our stockholders, and we view

the Loan Portfolio Acquisition as an important step on our path to achieving greater scale, trading liquidity and access to capital markets

for the Company.”

Key Transactional

Highlights

The Company believes

that the Loan Portfolio Acquisition is compelling for stockholders for several reasons:

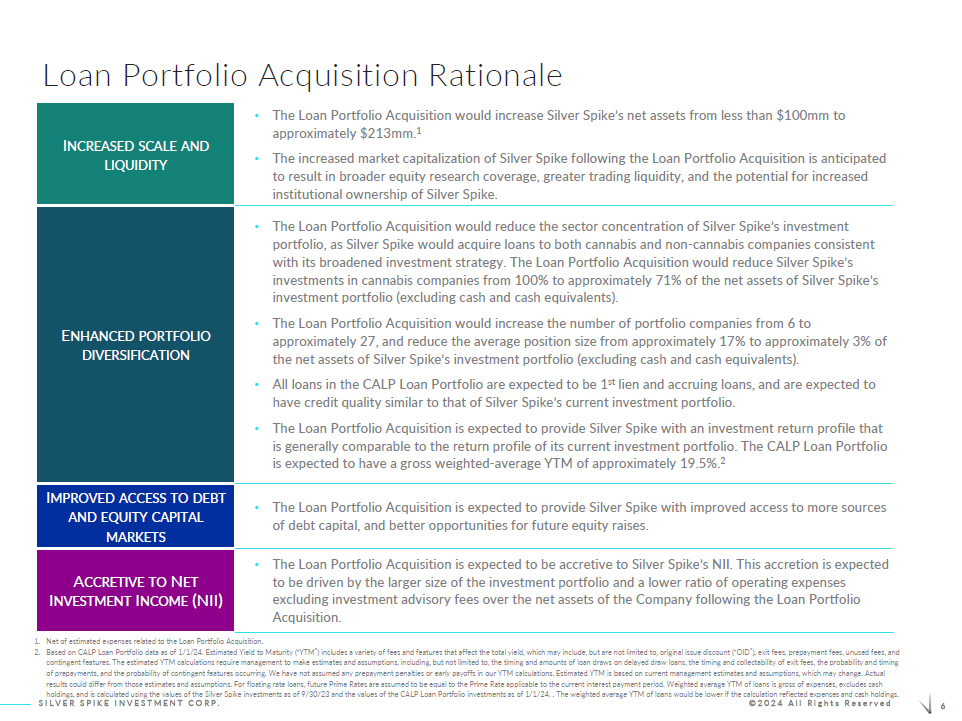

| · | Increased

scale and liquidity. The Loan Portfolio Acquisition would increase the Company’s

scale meaningfully, with its net assets expected to increase from less than $100 million

to approximately $213 million. The increased market capitalization of the Company following

the Loan Portfolio Acquisition is anticipated to result in broader equity research coverage,

greater trading liquidity, and the potential for increased institutional ownership of the

Company. |

| · | Enhanced

portfolio diversification. The Loan Portfolio Acquisition would reduce the sector

concentration of the Company’s investment portfolio, as the Company would acquire loans

to both cannabis and non-cannabis companies consistent with its broadened investment strategy.

The Loan Portfolio Acquisition would reduce the Company’s investments in cannabis companies

from 100% to approximately 71% of the net assets of the Company’s investment portfolio

(excluding cash and cash equivalents). The Loan Portfolio Acquisition would also diversify

the Company’s investment portfolio by increasing the number of portfolio companies

from 6 to approximately 27, and reducing the average position size from approximately 17%

to approximately 3% of the net assets of the Company’s investment portfolio (excluding

cash and cash equivalents). |

| · | Improved

access to debt and equity capital markets. The Loan Portfolio Acquisition is expected

to provide the Company with improved access to more sources of debt capital, and better opportunities

for future equity raises. |

| · | Accretive

to Net Investment Income (NII). The Loan Portfolio Acquisition is expected to be

accretive to the Company’s NII. This accretion is expected to be driven by the Company’s

anticipated lower ratio of operating expenses, excluding investment advisory fees, over the

net assets of the Company following the closing of the Loan Portfolio Acquisition. |

Keefe, Bruyette

& Woods, A Stifel Company, served as financial advisor and Kramer Levin Naftalis & Frankel LLP served as legal counsel

to the special committee of the Board. Davis Polk & Wardwell LLP serves as legal counsel to the Company. Eversheds Sutherland (US)

LLP serves as legal counsel to CALP.

Separately, Silver

Spike Capital, LLC (“SSC” or the “Adviser”), the investment adviser of the Company, today announced that it separately

entered into a definitive agreement with Chicago Atlantic BDC Holdings, LLC (together with its affiliates, “Chicago Atlantic”),

the investment adviser of CALP, pursuant to which a joint venture between Chicago Atlantic and SSC would be created to combine and jointly

operate SSC’s, and a portion of Chicago Atlantic’s, investment management businesses, subject to certain Company stockholder

approvals and customary closing conditions (the “Joint Venture”). The Joint Venture would cause the automatic termination

of the existing advisory agreement with SSC. As a result, the Board unanimously approved, upon the recommendation of its special committee,

a new investment advisory agreement with SSC to take effect upon closing of the Joint Venture, subject to company stockholder approval.

The new advisory agreement is identical, in all material respects, to the current agreement. Upon closing of the Joint Venture, the Company

would be renamed Chicago Atlantic BDC, Inc. and SSC would be renamed Chicago Atlantic BDC Advisers, LLC.

Conference Call

The Company will

host a conference call at 8:00 a.m. Eastern Time on Tuesday, February 20, 2024 to discuss the Loan Portfolio Acquisition. Participants

may register for the call here. A live webcast

of the call will also be available on the Company’s website at ssic.silverspikecap.com.

A presentation containing

a discussion of the Loan Portfolio Acquisition will be referenced on the call and has been posted to the Company’s website at ssic.silverspikecap.com

and filed with the Securities and Exchange Commission (the “SEC”).

A replay of the call will be available at ssic.silverspikecap.com by the end of the day on February 20, 2024.

About Silver

Spike Investment Corp.

The Company is a

specialty finance company that has elected to be regulated as a business development company under the Investment Company Act of 1940,

as amended. The Company’s investment objective is to maximize risk-adjusted returns on equity for its shareholders by investing

primarily in direct loans to privately held middle-market companies, with a focus on cannabis companies and other companies in the health

and wellness sector. The Company is managed by SSC, an investment manager focused on the cannabis and alternative health and wellness

industries. For more information, please visit ssic.silverspikecap.com.

Forward-Looking

Statements

Some of the statements

in this communication constitute forward-looking statements because they relate to future events, future performance or financial condition

of the Company or the Loan Portfolio Acquisition. The forward-looking statements may include statements as to: future operating results

of the Company and distribution projections; business prospects of the Company and the prospects of its portfolio companies; and the

impact of the investments that the Company expects to make. In addition, words such as “may,” “might,” “will,”

“intend,” “should,” “could,” “can,” “would,” “expect,” “believe,”

“estimate,” “anticipate,” “predict,” “potential,” “plan” or similar words

indicate forward-looking statements, although not all forward-looking statements include these words. The forward-looking statements

contained in this communication involve risks and uncertainties. Certain factors could cause actual results and conditions to differ

materially from those projected, including the uncertainties associated with (i) the timing or likelihood of the Loan Portfolio Acquisition

closing; (ii) the ability to realize the anticipated benefits of the Loan Portfolio Acquisition; (iii) the percentage of Company stockholders

voting in favor of the proposals submitted for their approval; (iv) the possibility that competing offers or acquisition proposals will

be made; (v) the possibility that any or all of the various conditions to the consummation of the Loan Portfolio Acquisition may not

be satisfied or waived; (vi) risks related to diverting management’s attention from ongoing business operations; (vii) the risk

that stockholder litigation in connection with the Loan Portfolio Acquisition may result in significant costs of defense and liability;

(viii) changes in the economy, financial markets and political environment, including the impacts of inflation and rising interest rates;

(ix) risks associated with possible disruption in the operations of the Company or the economy generally due to terrorism, war or other

geopolitical conflict (including the current conflict between Russia and Ukraine), natural disasters or global health pandemics, such

as the COVID-19 pandemic; (x) future changes in laws or regulations (including the interpretation of these laws and regulations by regulatory

authorities); (xi) changes in political, economic or industry conditions, the interest rate environment or conditions affecting the financial

and capital markets that could result in changes to the value of the Company’s assets; (xii) elevating levels of inflation, and

its impact on the Company, on its portfolio companies and on the industries in which it invests; (xiii) the Company’s plans,

expectations, objectives

and intentions, as a result of the Loan Portfolio Acquisition; (xiv) the future operating results and net investment income projections

of the Company; (xv) the ability of the Adviser to locate suitable investments for the Company and to monitor and administer its investments;

(xvi) the ability of the Adviser or its affiliates to attract and retain highly talented professionals; (xvii) the business prospects

of the Company and the prospects of its portfolio companies; (xviii) the impact of the investments that the Company expects to make;

(xix) the expected financings and investments and additional leverage that the Company may seek to incur in the future; (xx) conditions

in the Company’s operating areas, particularly with respect to business development companies or regulated investment companies;

(xxi) the ability of CALP to obtain the necessary consents for, or otherwise identify and obtain additional loans for including in the

CALP Loan Portfolio; (xxii) the regulatory requirements applicable to the transaction and any changes to the transaction necessary to

comply with such requirements; (xxiii) the satisfaction or waiver of the conditions to the consummation of the transaction, and the possibility

in that in connection that the closing will not occur or that it will be significantly delayed; (xxiv) the realization generally of the

anticipated benefits of the Loan Portfolio Acquisition and the possibility that the Company will not realize those benefits, in part

or at all; (xxv) the performance of the loans included in the CALP Loan Portfolio, and the possibility of defects or deficiencies in

such loans notwithstanding the diligence performed by the Company and its advisors; (xxvi) the ability of the Company to realize cost

savings and other management efficiencies in connection with the transaction as anticipated; (xxvii) the reaction of the trading markets

to the transaction and the possibility that a more liquid market or more extensive analyst coverage will not develop for the Company

as anticipated; (xxviii) the reaction of the financial markets to the transaction and the possibility that the Company will not be able

to raise capital as anticipated; (xxix) the diversion of management’s attention from the Company’s ongoing business operations;

(xxx) the risk of stockholder litigation in connection with the transaction; (xxxi) the strategic, business, economic, financial, political

and governmental risks and other risk factors affecting the business of the Company and the companies in which it is invested as described

in the Company’s public filings with the SEC and (xxxii) other considerations that may be disclosed from time to time in the Company’s

publicly disseminated documents and filings. The Company has based the forward-looking statements included in this communication on information

available to it on the date of this communication, and it assumes no obligation to update any such forward-looking statements. Although

the Company undertakes no obligation to revise or update any forward-looking statements, whether as a result of new information, future

events or otherwise, you are advised to consult any additional disclosures that the Company may make directly to you or through reports

that the Company in the future may file with the SEC, including the Proxy Statement/Prospectus, annual reports on Form 10-K, quarterly

reports on Form 10-Q and current reports on Form 8-K.

Additional Information

and Where to Find It

This communication

relates to a proposed business combination involving the Company and CALP, along with the related proposals for which stockholder approval

will be sought. In connection with the proposals, the Company intends to file relevant materials with the SEC, including a registration

statement on Form N-14, which will include a proxy statement and a prospectus of the Company (the “Proxy Statement/Prospectus”).

This communication does not constitute an offer to sell or the solicitation of an offer to buy any securities or a solicitation of any

vote or approval. No offer of securities shall be made except by means of a prospectus meeting the requirements of Section 10 of the

Securities Act of 1933, as amended. STOCKHOLDERS OF THE COMPANY ARE URGED TO READ THE PROXY STATEMENT/PROSPECTUS, AND OTHER DOCUMENTS

THAT ARE FILED OR WILL BE FILED WITH THE SEC, AS WELL AS ANY AMENDMENTS OR SUPPLEMENTS TO THESE DOCUMENTS, CAREFULLY AND IN THEIR ENTIRETY

WHEN THEY BECOME AVAILABLE BECAUSE THEY WILL CONTAIN IMPORTANT INFORMATION ABOUT THE COMPANY, THE LOAN PORTFOLIO ACQUISITION AND THE

PROPOSALS. Investors and security holders will be able to obtain the documents filed with the SEC free of charge at the SEC’s

website, www.sec.gov, or from the Company’s website at ssic.silverspikecap.com.

Participants

in the Solicitation

The Company and

its directors, executive officers and certain other members of management and employees of the Adviser and its affiliates may be deemed

to be participants in the solicitation of proxies from the stockholders of the Company in connection with the Loan Portfolio Acquisition.

Information regarding the persons who may, under the rules of the SEC, be considered participants in the solicitation of the Company

stockholders in connection with the Loan Portfolio Acquisition will be contained in the Proxy Statement/Prospectus when such document

becomes available. This document may be obtained free of charge from the sources indicated above.

No Offer or Solicitation

This communication

is not, and under no circumstances is it to be construed as, a prospectus or an advertisement and the communication is not, and under

no circumstances is it to be construed as, an offer to sell or a solicitation of an offer to purchase any securities in the Company or

in any fund or other investment vehicle managed by the Adviser or any of its affiliates.

Contacts

Investors:

Bill Healy

Bill@silverspikecap.com

212-905-4933

Exhibit 99.3

Silver Spike Investment Corp. Acquisition of Loan Portfolio from Chicago Atlantic February 20, 2024

2 SILVER SPIKE INVESTMENT CORP. ©2024 All Rights Reserved DISCLAIMERS AND FORWARD - LOOKING STATEMENTS The information contained in this presentation should be viewed in conjunction with the conference call of Silver Spike Investment Corp . (“Silver Spike” or the “Company”) (NASDAQ : SSIC) held on February 20 , 2024 regarding Silver Spike’s definitive agreement with Chicago Atlantic Loan Portfolio, LLC (“CALP”) to purchase from CALP a portfolio of loans in exchange for newly issued shares of Silver Spike, subject to certain stockholder approvals and customary closing conditions (the “Loan Portfolio Acquisition”) . The information contained herein may not be used, reproduced or distributed to others, in whole or in part, for any other purpose without the prior written consent of the Company . Nothing in these materials should be construed as a recommendation to invest in any securities that may be issued by Silver Spike or as legal, accounting or tax advice . An investment in securities of the type described herein presents certain risks . Nothing contained herein shall be relied upon as a promise or representation whether as to the past or future performance . Certain information contained herein has been derived from sources prepared by third parties . While such information is believed to be reliable for the purposes used herein, we make no representation or warranty with respect to the accuracy of such information . The information contained in this presentation is summary information that is intended to be considered in the context of other public announcements that we may make, by press release or otherwise, from time to time . We undertake no duty or obligation to publicly update or revise the information contained in this presentation, except as required by law . These materials contain information about Silver Spike, certain of its personnel and affiliates and its historical performance . You should not view information related to the past performance of Silver Spike as indicative of Silver Spike’s future results, the achievement of which cannot be assured . Past performance does not guarantee future results, which may vary. The value of investments and the income derived from inve stm ents will fluctuate and can go down as well as up. A loss of principal may occur. Forward - Looking Statements Some of the statements in this communication constitute forward - looking statements because they relate to future events, future performance or financial condition of the Company or the Loan Portfolio Acquisition . The forward - looking statements may include statements as to : future operating results of the Company and distribution projections ; business prospects of the Company and the prospects of its portfolio companies ; and the impact of the investments that the Company expects to make . In addition, words such as “may,” “might,” “will,” “intend,” “should,” “could,” “can,” “would,” “expect,” “believe,” “estimate,” “anticipate,” “predict,” “potential,” “plan” or similar words indicate forward - looking statements, although not all forward - looking statements include these words . The forward - looking statements contained in this communication involve risks and uncertainties . Certain factors could cause actual results and conditions to differ materially from those projected, including the uncertainties associated with (i) the timing or likelihood of the Loan Portfolio Acquisition closing ; (ii) the ability to realize the anticipated benefits of the Loan Portfolio Acquisition ; (iii) the percentage of Company stockholders voting in favor of the proposals submitted for their approval ; (iv) the possibility that competing offers or acquisition proposals will be made ; (v) the possibility that any or all of the various conditions to the consummation of the Loan Portfolio Acquisition may not be satisfied or waived ; (vi) risks related to diverting management’s attention from ongoing business operations ; (vii) the risk that stockholder litigation in connection with the Loan Portfolio Acquisition may result in significant costs of defense and liability ; (viii) changes in the economy, financial markets and political environment, including the impacts of inflation and rising interest rates ; (ix) risks associated with possible disruption in the operations of the Company or the economy generally due to terrorism, war or other geopolitical conflict (including the current conflict between Russia and Ukraine), natural disasters or global health pandemics, such as the COVID - 19 pandemic ; (x) future changes in laws or regulations (including the interpretation of these laws and regulations by regulatory authorities) ; (xi) changes in political, economic or industry conditions, the interest rate environment or conditions affecting the financial and capital markets that could result in changes to the value of the Company’s assets ; (xii) elevating levels of inflation, and its impact on the Company, on its portfolio companies and on the industries in which it invests ; (xiii) the Company’s plans, expectations, objectives and intentions, as a result of the Loan Portfolio Acquisition ; (xiv) the future operating results and net investment income projections of the Company ; (xv) the ability of the Adviser to locate suitable investments for the Company and to monitor and administer its investments ; (xvi) the ability of the Adviser or its affiliates to attract and retain highly talented professionals ; (xvii) the business prospects of the Company and the prospects of its portfolio companies ; (xviii) the impact of the investments that the Company expects to make ; (xix) the expected financings and investments and additional leverage that the Company may seek to incur in the future ; (xx) conditions in the Company’s operating areas, particularly with respect to business development companies or regulated investment companies ; (xxi) the ability of CALP to obtain the necessary consents for, or otherwise identify and obtain additional loans for including in the CALP Loan Portfolio ; (xxii) the regulatory requirements applicable to the transaction and any changes to the transaction necessary to comply with such requirements ; (xxiii) the satisfaction or waiver of the conditions to the consummation of the transaction, and the possibility in that in connection that the closing will not occur or that it will be significantly delayed ; (xxiv) the realization generally of the anticipated benefits of the Loan Portfolio Acquisition and the possibility that the Company will not realize those benefits, in part or at all ; (xxv) the performance of the loans included in the CALP Loan Portfolio, and the possibility of defects or deficiencies in such loans notwithstanding the diligence performed by the Company and its advisors ; (xxvi) the ability of the Company to realize cost savings and other management efficiencies in connection with the transaction as anticipated ; (xxvii) the reaction of the trading markets to the transaction and the possibility that a more liquid market or more extensive analyst coverage will not develop for the Company as anticipated ; (xxviii) the reaction of the financial markets to the transaction and the possibility that the Company will not be able to raise capital as anticipated ; (xxix) the diversion of management’s attention from the Company’s ongoing business operations ; (xxx) the risk of stockholder litigation in connection with the transaction ; (xxxi) the strategic, business, economic, financial, political and governmental risks and other risk factors affecting the business of the Company and the companies in which it is invested as described in the Company’s public filings with the SEC ; and (xxxii) other considerations that may be disclosed from time to time in the Company’s publicly disseminated documents and filings . The Company has based the forward - looking statements included in this communication on information available to it on the date of this communication, and it assumes no obligation to update any such forward - looking statements . Although the Company undertakes no obligation to revise or update any forward - looking statements, whether as a result of new information, future events or otherwise, you are advised to consult any additional disclosures that the Company may make directly to you or through reports that the Company in the future may file with the SEC, including the Joint Proxy Statement/Prospectus (as defined below), annual reports on Form 10 - K, quarterly reports on Form 10 - Q and current reports on Form 8 - K . Additional Information and Where to Find It This communication relates to a proposed business combination involving the Company and CALP, along with the related proposals for which stockholder approval will be sought . In connection with the proposals, the Company intends to file relevant materials with the SEC, including a registration statement on Form N - 14 , which will include a proxy statement and a prospectus of the Company (the “Joint Proxy Statement/Prospectus”) . This communication does not constitute an offer to sell or the solicitation of an offer to buy any securities or a solicitation of any vote or approval . No offer of securities shall be made except by means of a prospectus meeting the requirements of Section 10 of the Securities Act of 1933 , as amended . STOCKHOLDERS OF THE COMPANY ARE URGED TO READ THE JOINT PROXY STATEMENT/PROSPECTUS, AND OTHER DOCUMENTS THAT ARE FILED OR WILL BE FILED WITH THE SEC, AS WELL AS ANY AMENDMENTS OR SUPPLEMENTS TO THESE DOCUMENTS, CAREFULLY AND IN THEIR ENTIRETY WHEN THEY BECOME AVAILABLE BECAUSE THEY WILL CONTAIN IMPORTANT INFORMATION ABOUT THE COMPANY, THE LOAN PORTFOLIO ACQUISITION AND THE PROPOSALS . Investors and security holders will be able to obtain the documents filed with the SEC free of charge at the SEC’s website, www . sec . gov, or from the Company’s website at ssic . silverspikecap . com . Participants in the Solicitation The Company and its directors, executive officers and certain other members of management and employees of the Adviser and its affiliates may be deemed to be participants in the solicitation of proxies from the stockholders of the Company in connection with the Loan Portfolio Acquisition . Information regarding the persons who may, under the rules of the SEC, be considered participants in the solicitation of the Company stockholders in connection with the Loan Portfolio Acquisition will be contained in the Joint Proxy Statement/Prospectus when such document becomes available . This document may be obtained free of charge from the sources indicated above . No Offer or Solicitation This communication is not, and under no circumstances is it to be construed as, a prospectus or an advertisement and the communication is not, and under no circumstances is it to be construed as, an offer to sell or a solicitation of an offer to purchase any securities in the Company or in any fund or other investment vehicle managed by the Adviser or any of its affiliates .

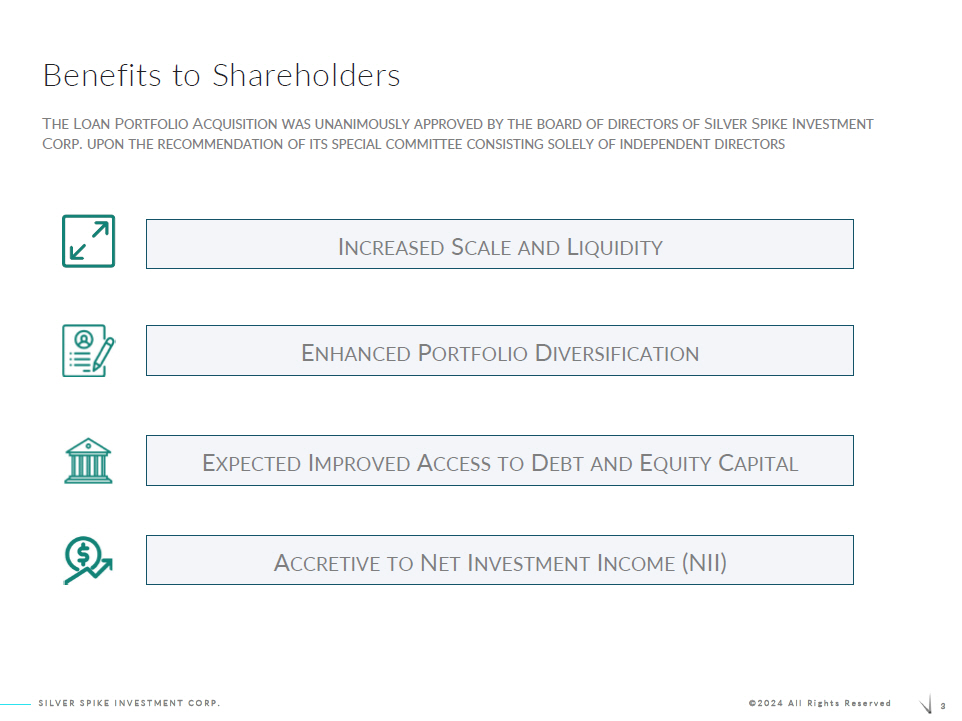

3 SILVER SPIKE INVESTMENT CORP. ©2024 All Rights Reserved Benefits to Shareholders T HE L OAN P ORTFOLIO A CQUISITION WAS UNANIMOUSLY APPROVED BY THE BOARD OF DIRECTORS OF S ILVER S PIKE I NVESTMENT C ORP . UPON THE RECOMMENDATION OF ITS SPECIAL COMMITTEE CONSISTING SOLELY OF INDEPENDENT DIRECTORS I NCREASED S CALE AND L IQUIDITY E NHANCED P ORTFOLIO D IVERSIFICATION E XPECTED I MPROVED A CCESS TO D EBT AND E QUITY C APITAL A CCRETIVE TO N ET I NVESTMENT I NCOME (NII)

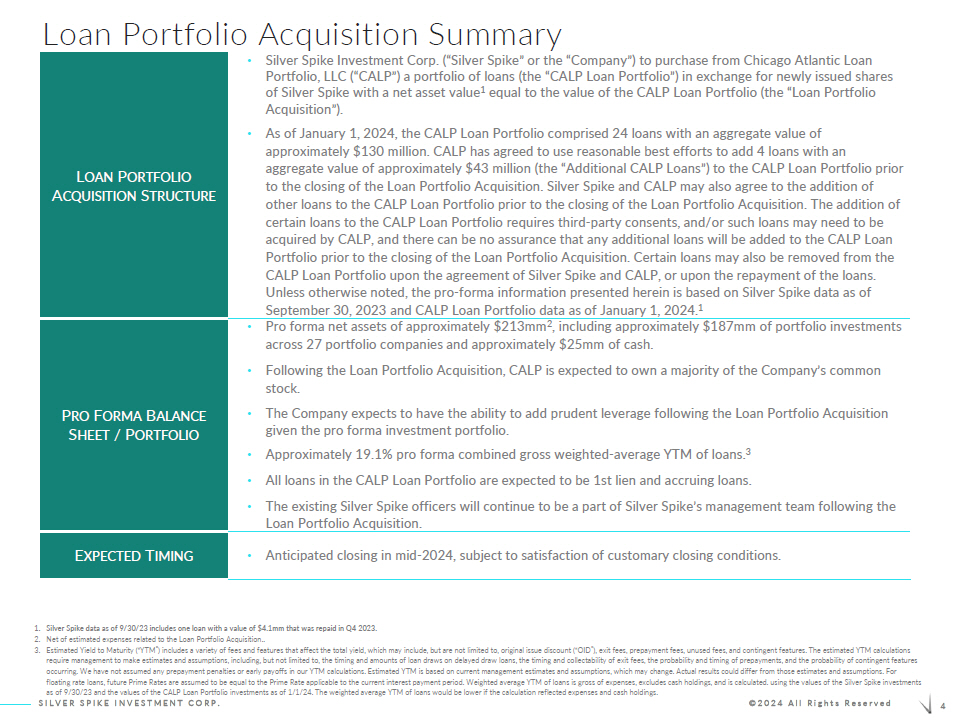

4 SILVER SPIKE INVESTMENT CORP. ©2024 All Rights Reserved Loan Portfolio Acquisition Summary L OAN P ORTFOLIO A CQUISITION S TRUCTURE • Silver Spike Investment Corp. (“Silver Spike” or the “Company”) to purchase from Chicago Atlantic Loan Portfolio, LLC (“CALP”) a portfolio of loans (the “CALP Loan Portfolio”) in exchange for newly issued shares of Silver Spike with a net asset value 1 equal to the value of the CALP Loan Portfolio (the “Loan Portfolio Acquisition”). • As of January 1, 2024, the CALP Loan Portfolio comprised 24 loans with an aggregate value of approximately $130 million. CALP has agreed to use reasonable best efforts to add 4 loans with an aggregate value of approximately $43 million (the “Additional CALP Loans”) to the CALP Loan Portfolio prior to the closing of the Loan Portfolio Acquisition. Silver Spike and CALP may also agree to the addition of other loans to the CALP Loan Portfolio prior to the closing of the Loan Portfolio Acquisition. The addition of certain loans to the CALP Loan Portfolio requires third - party consents, and/or such loans may need to be acquired by CALP, and there can be no assurance that any additional loans will be added to the CALP Loan Portfolio prior to the closing of the Loan Portfolio Acquisition. Certain loans may also be removed from the CALP Loan Portfolio upon the agreement of Silver Spike and CALP, or upon the repayment of the loans. Unless otherwise noted, the pro - forma information presented herein is based on Silver Spike data as of September 30, 2023 and CALP Loan Portfolio data as of January 1, 2024. 1 P RO F ORMA B ALANCE S HEET / P ORTFOLIO • Pro forma net assets of approximately $ 213mm 2 , including approximately $187mm of portfolio investments across 27 portfolio companies and approximately $25mm of cash. • Following the Loan Portfolio Acquisition, CALP is expected to own a majority of the Company’s common stock. • The Company expects to have the ability to add prudent leverage following the Loan Portfolio Acquisition given the pro forma investment portfolio. • Approximately 19.1% pro forma combined gross weighted - average YTM of loans. 3 • All loans in the CALP Loan Portfolio are expected to be 1st lien and accruing loans. • The existing Silver Spike officers will continue to be a part of Silver Spike’s management team following the Loan Portfolio Acquisition. E XPECTED T IMING • Anticipated closing in mid - 2024, subject to satisfaction of customary closing conditions. 1. Silver Spike data as of 9/30/23 includes one loan with a value of $ 4.1mm that was repaid in Q4 2023. 2. Net of estimated expenses related to the Loan Portfolio Acquisition.. 3. Estimated Yield to Maturity (“YTM”) includes a variety of fees and features that affect the total yield, which may include, b ut are not limited to, original issue discount (“OID”), exit fees, prepayment fees, unused fees, and contingent features. The es tim ated YTM calculations require management to make estimates and assumptions, including, but not limited to, the timing and amounts of loan draws on del ayed draw loans, the timing and collectability of exit fees, the probability and timing of prepayments, and the probability o f c ontingent features occurring. We have not assumed any prepayment penalties or early payoffs in our YTM calculations. Estimated YTM is based on c urr ent management estimates and assumptions, which may change. Actual results could differ from those estimates and assumptions. Fo r floating rate loans, future Prime Rates are assumed to be equal to the Prime Rate applicable to the current interest payment per iod. Weighted average YTM of loans is gross of expenses, excludes cash holdings, and is calculated. using the values of the Sil ver Spike investments as of 9/30/23 and the values of the CALP Loan Portfolio investments as of 1/1/24. The weighted average YTM of loans would be low er if the calculation reflected expenses and cash holdings.

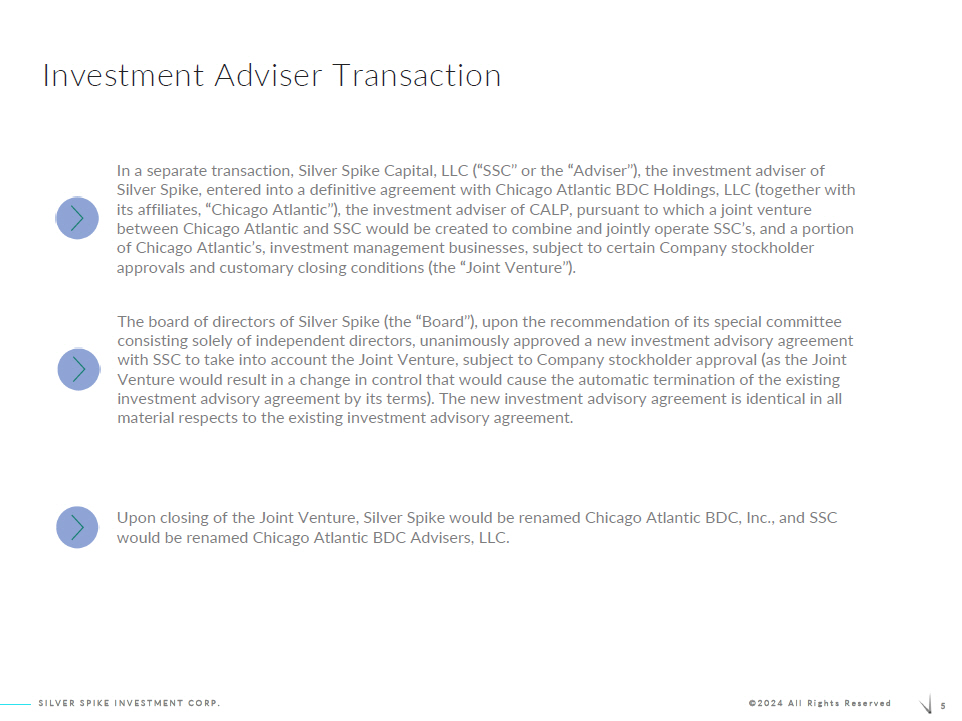

5 SILVER SPIKE INVESTMENT CORP. ©2024 All Rights Reserved Investment Adviser Transaction Upon closing of the Joint Venture, Silver Spike would be renamed Chicago Atlantic BDC, Inc., and SSC would be renamed Chicago Atlantic BDC Advisers, LLC. In a separate transaction, Silver Spike Capital, LLC (“SSC” or the “Adviser”), the investment adviser of Silver Spike, entered into a definitive agreement with Chicago Atlantic BDC Holdings, LLC (together with its affiliates, “Chicago Atlantic”), the investment adviser of CALP, pursuant to which a joint venture between Chicago Atlantic and SSC would be created to combine and jointly operate SSC’s, and a portion of Chicago Atlantic’s, investment management businesses, subject to certain Company stockholder approvals and customary closing conditions (the “Joint Venture”). The board of directors of Silver Spike (the “Board”), upon the recommendation of its special committee consisting solely of independent directors, unanimously approved a new investment advisory agreement with SSC to take into account the Joint Venture, subject to Company stockholder approval (as the Joint Venture would result in a change in control that would cause the automatic termination of the existing investment advisory agreement by its terms). The new investment advisory agreement is identical in all material respects to the existing investment advisory agreement.

6 SILVER SPIKE INVESTMENT CORP. ©2024 All Rights Reserved Loan Portfolio Acquisition Rationale I NCREASED SCALE AND LIQUIDITY • The Loan Portfolio Acquisition would increase Silver Spike’s net assets from less than $100mm to approximately $ 213 mm. 1 • The increased market capitalization of Silver Spike following the Loan Portfolio Acquisition is anticipated to result in broader equity research coverage, greater trading liquidity, and the potential for increased institutional ownership of Silver Spike. E NHANCED PORTFOLIO DIVERSIFICATION • The Loan Portfolio Acquisition would reduce the sector concentration of Silver Spike’s investment portfolio, as Silver Spike would acquire loans to both cannabis and non - cannabis companies consistent with its broadened investment strategy. The Loan Portfolio Acquisition would reduce Silver Spike’s investments in cannabis companies from 100% to approximately 71% of the net assets of Silver Spike’s investment portfolio (excluding cash and cash equivalents). • The Loan Portfolio Acquisition would increase the number of portfolio companies from 6 to approximately 27, and reduce the average position size from approximately 17% to approximately 3% of the net assets of Silver Spike’s investment portfolio (excluding cash and cash equivalents). • All loans in the CALP Loan Portfolio are expected to be 1 st lien and accruing loans, and are expected to have credit quality similar to that of Silver Spike’s current investment portfolio. • The Loan Portfolio Acquisition is expected to provide Silver Spike with an investment return profile that is generally comparable to the return profile of its current investment portfolio. The CALP Loan Portfolio is expected to have a gross weighted - average YTM of approximately 19.5%. 2 I MPROVED ACCESS TO DEBT AND EQUITY CAPITAL MARKETS • The Loan Portfolio Acquisition is expected to provide Silver Spike with improved access to more sources of debt capital, and better opportunities for future equity raises. A CCRETIVE TO N ET I NVESTMENT I NCOME ( NII ) • The Loan Portfolio Acquisition is expected to be accretive to Silver Spike’s NII. This accretion is expected to be driven by the larger size of the investment portfolio and a lower ratio of operating expenses excluding investment advisory fees over the net assets of the Company following the Loan Portfolio Acquisition. 1. Net of estimated expenses related to the Loan Portfolio Acquisition. 2. Based on CALP Loan Portfolio data as of 1/1/24. Estimated Yield to Maturity (“YTM”) includes a variety of fees and features t hat affect the total yield, which may include, but are not limited to, original issue discount (“OID”), exit fees, prepayment fee s, unused fees, and contingent features. The estimated YTM calculations require management to make estimates and assumptions, including, but not lim ited to, the timing and amounts of loan draws on delayed draw loans, the timing and collectability of exit fees, the probability and timing of prepayments, and the probability of contingent features occurring. We have not assumed any prepayment penalties or early p ayo ffs in our YTM calculations. Estimated YTM is based on current management estimates and assumptions, which may change. Actual results could differ from those estimates and assumptions. For floating rate loans, future Prime Rates are assumed to be equal t o the Prime Rate applicable to the current interest payment period. Weighted average YTM of loans is gross of expenses, exclude s cash holdings, and is calculated using the values of the Silver Spike investments as of 9/30/23 and the values of the CALP Loan Po rtf olio investments as of 1/1/24. . The weighted average YTM of loans would be lower if the calculation reflected expenses and c ash holdings.

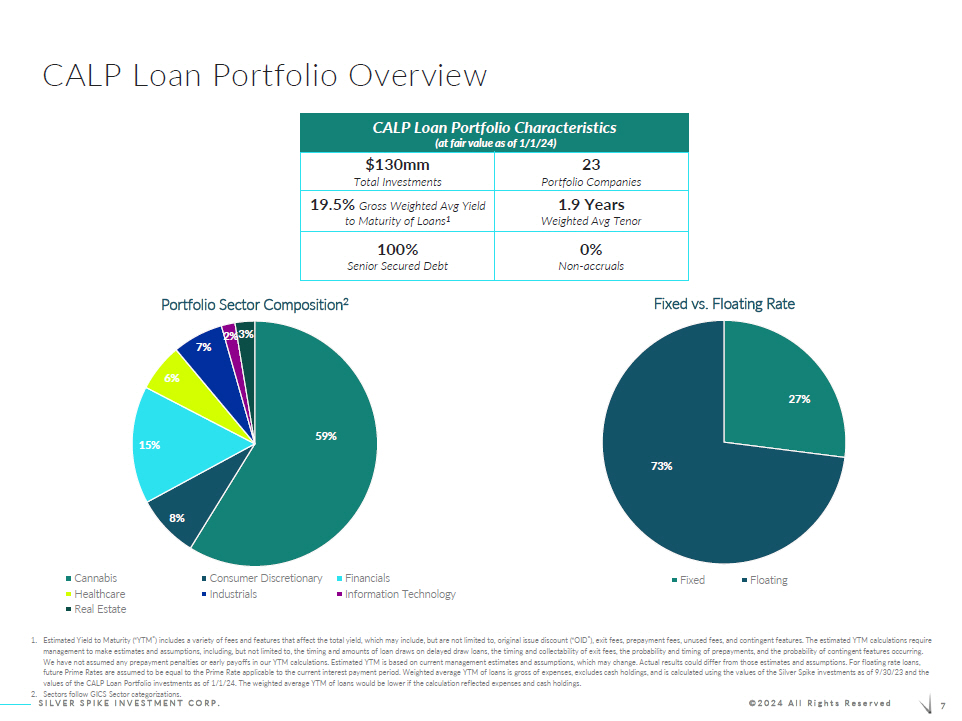

7 SILVER SPIKE INVESTMENT CORP. ©2024 All Rights Reserved CALP Loan Portfolio Overview CALP Loan Portfolio Characteristics (at fair value as of 1/1/24) $130mm Total Investments 23 Portfolio Companies 19.5% Gross Weighted Avg Yield to Maturity of Loans 1 1.9 Years Weighted Avg Tenor 100% Senior Secured Debt 0% Non - accruals 27% 73% Fixed vs. Floating Rate Fixed Floating 1. Estimated Yield to Maturity (“YTM”) includes a variety of fees and features that affect the total yield, which may include, b ut are not limited to, original issue discount (“OID”), exit fees, prepayment fees, unused fees, and contingent features. The es tim ated YTM calculations require management to make estimates and assumptions, including, but not limited to, the timing and amounts of loan draws on delayed dra w loans, the timing and collectability of exit fees, the probability and timing of prepayments, and the probability of contin gen t features occurring. We have not assumed any prepayment penalties or early payoffs in our YTM calculations. Estimated YTM is based on current mana gem ent estimates and assumptions, which may change. Actual results could differ from those estimates and assumptions. For floating rate loans, future Prime Rates are assumed to be equal to the Prime Rate applicable to the current interest payment period. Weighted averag e YTM of loans is gross of expenses, excludes cash holdings, and is calculated using the values of the Silver Spike investmen ts as of 9/30/23 and the values of the CALP Loan Portfolio investments as of 1/1/24. The weighted average YTM of loans would be lower if the calculati on reflected expenses and cash holdings. 2. Sectors follow GICS Sector categorizations. 59% 8% 15% 6% 7% 2% 3% Portfolio Sector Composition 2 Cannabis Consumer Discretionary Financials Healthcare Industrials Information Technology Real Estate

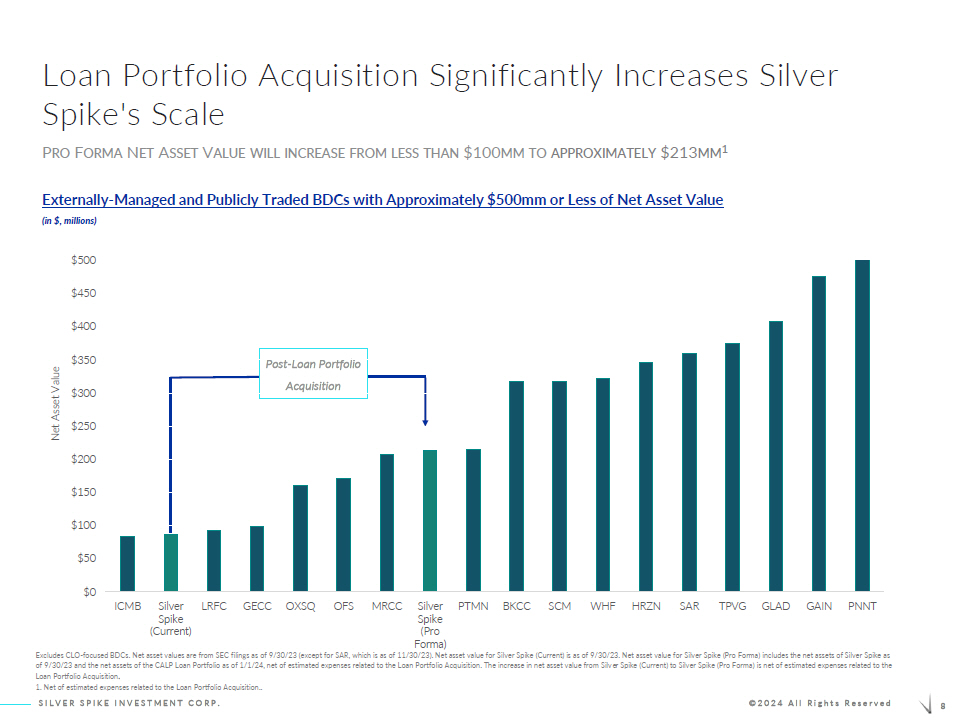

8 SILVER SPIKE INVESTMENT CORP. ©2024 All Rights Reserved Loan Portfolio Acquisition Significantly Increases Silver Spike's Scale P RO F ORMA N ET A SSET V ALUE WILL INCREASE FROM LESS THAN $100 MM TO APPROXIMATELY $ 213 MM 1 Externally - Managed and Publicly Traded BDCs with Approximately $500mm or Less of Net Asset Value (in $, millions) Post - Loan Portfolio Acquisition Excludes CLO - focused BDCs . Net asset values are from SEC filings as of 9/30/23 (except for SAR, which is as of 11/30/23). Net asset value for Silver S pik e (Current) is as of 9/30/23. Net asset value for Silver Spike (Pro Forma) includes the net assets of Silver Spike as of 9/30/23 and the net assets of the CALP Loan Portfolio as of 1/1/24, net of estimated expenses related to the Loan Portfoli o A cquisition. The increase in net asset value from Silver Spike (Current) to Silver Spike (Pro Forma) is net of estimated expen ses related to the Loan Portfolio Acquisition . 1. Net of estimated expenses related to the Loan Portfolio Acquisition.. $0 $50 $100 $150 $200 $250 $300 $350 $400 $450 $500 ICMB Silver Spike (Current) LRFC GECC OXSQ OFS MRCC Silver Spike (Pro Forma) PTMN BKCC SCM WHF HRZN SAR TPVG GLAD GAIN PNNT Net Asset Value

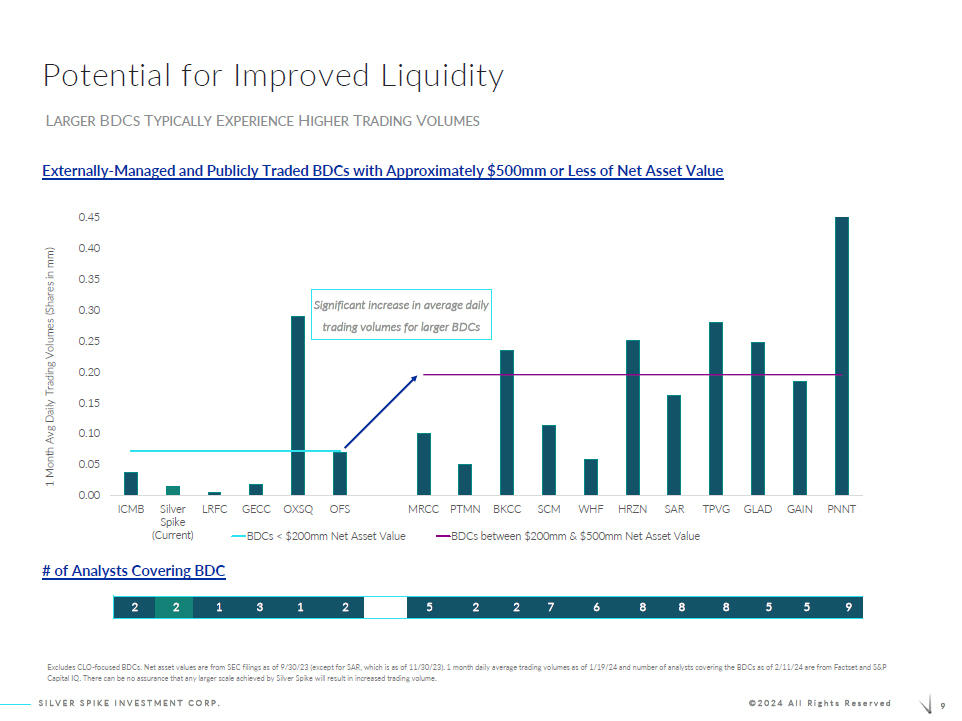

9 SILVER SPIKE INVESTMENT CORP. ©2024 All Rights Reserved 0.00 0.05 0.10 0.15 0.20 0.25 0.30 0.35 0.40 0.45 ICMB Silver Spike (Current) LRFC GECC OXSQ OFS MRCC PTMN BKCC SCM WHF HRZN SAR TPVG GLAD GAIN PNNT 1 Month Avg Daily Trading Volumes (Shares in mm) BDCs < $200mm Net Asset Value BDCs between $200mm & $500mm Net Asset Value Potential for Improved Liquidity Externally - Managed and Publicly Traded BDCs with Approximately $500mm or Less of Net Asset Value Significant increase in average daily trading volumes for larger BDCs # of Analysts Covering BDC 2 2 1 3 1 2 5 2 2 7 6 8 8 8 5 5 9 L ARGER BDC S T YPICALLY E XPERIENCE H IGHER T RADING V OLUMES Excludes CLO - focused BDCs . Net asset values are from SEC filings as of 9/30/23 (except for SAR, which is as of 11/30/23). 1 month daily average tradin g v olumes as of 1/19/24 and number of analysts covering the BDCs as of 2/11/24 are from Factset and S&P Capital IQ. There can be no assurance that any larger scale achieved by Silver Spike will result in increased trading volume.

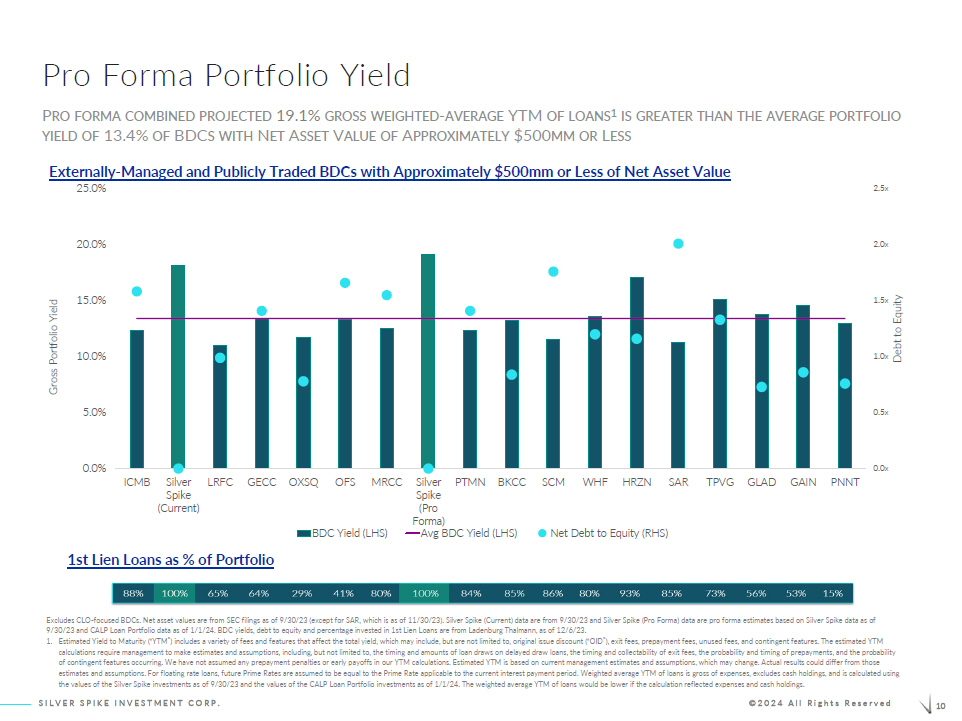

10 SILVER SPIKE INVESTMENT CORP. ©2024 All Rights Reserved Pro Forma Portfolio Yield P RO FORMA COMBINED PROJECTED 19.1% GROSS WEIGHTED - AVERAGE YTM OF LOANS 1 IS GREATER THAN THE AVERAGE PORTFOLIO YIELD OF 13.4% OF BDC S WITH N ET A SSET V ALUE OF A PPROXIMATELY $500 MM OR L ESS Externally - Managed and Publicly Traded BDCs with Approximately $500mm or Less of Net Asset Value 1st Lien Loans as % of Portfolio Excludes CLO - focused BDCs. Net asset values are from SEC filings as of 9/30/23 (except for SAR, which is as of 11/30/23). Silver Spike (Current) data are from 9/30/23 and Silver Spike (Pro Forma) data are pro forma estimates based on Silver Spike data as o f 9/30/23 and CALP Loan Portfolio data as of 1/1/24. BDC yields, debt to equity and percentage invested in 1st Lien Loans are f rom Ladenburg Thalmann , as of 12/6/23. 1. Estimated Yield to Maturity (“YTM”) includes a variety of fees and features that affect the total yield, which may include, b ut are not limited to, original issue discount (“OID”), exit fees, prepayment fees, unused fees, and contingent features. The es tim ated YTM calculations require management to make estimates and assumptions, including, but not limited to, the timing and amounts of loan draws on delayed draw loans, the timing and collectability of exit fees, the probability and timing of prepayments, and the p ro bability of contingent features occurring. We have not assumed any prepayment penalties or early payoffs in our YTM calculations. Esti mat ed YTM is based on current management estimates and assumptions, which may change. Actual results could differ from those estimates and assumptions. For floating rate loans, future Prime Rates are assumed to be equal to the Prime Rate applicable to t he current interest payment period. Weighted average YTM of loans is gross of expenses, excludes cash holdings, and is calculat ed using the values of the Silver Spike investments as of 9/30/23 and the values of the CALP Loan Portfolio investments as of 1/1/24. The weighted average YTM of loans would be lower if the calculation reflected expenses and cash holdings. 0.0x 0.5x 1.0x 1.5x 2.0x 2.5x 0.0% 5.0% 10.0% 15.0% 20.0% 25.0% ICMB Silver Spike (Current) LRFC GECC OXSQ OFS MRCC Silver Spike (Pro Forma) PTMN BKCC SCM WHF HRZN SAR TPVG GLAD GAIN PNNT Debt to Equity Gross Portfolio Yield BDC Yield (LHS) Avg BDC Yield (LHS) Net Debt to Equity (RHS)

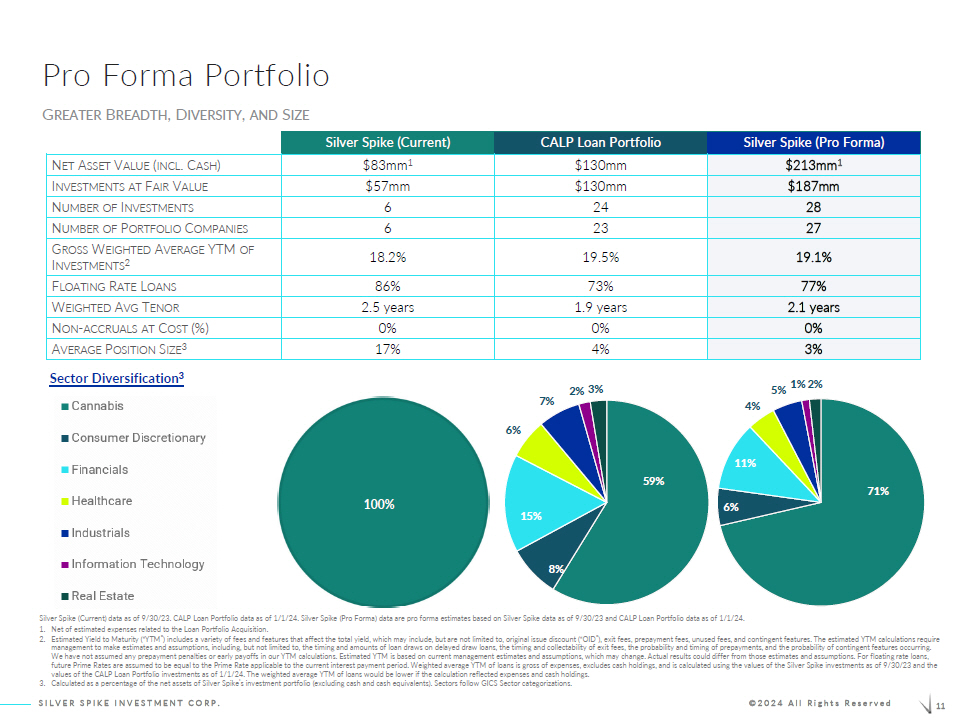

11 SILVER SPIKE INVESTMENT CORP. ©2024 All Rights Reserved Pro Forma Portfolio Silver Spike (Current) CALP Loan Portfolio Silver Spike (Pro Forma) N ET A SSET V ALUE ( INCL . C ASH ) $83mm 1 $130mm $213mm 1 I NVESTMENTS AT F AIR V ALUE $57mm $130mm $187mm N UMBER OF I NVESTMENTS 6 24 28 N UMBER OF P ORTFOLIO C OMPANIES 6 23 27 G ROSS W EIGHTED A VERAGE YTM OF I NVESTMENTS 2 18.2% 19.5% 19.1% F LOATING R ATE L OANS 86% 73% 77% W EIGHTED A VG T ENOR 2.5 years 1.9 years 2.1 years N ON - ACCRUALS AT C OST (%) 0% 0% 0% A VERAGE P OSITION S IZE 3 17% 4% 3% Sector Diversification 3 100% G REATER B READTH , D IVERSITY , AND S IZE Silver Spike (Current) data as of 9/30/23. CALP Loan Portfolio data as of 1/1/24. Silver Spike (Pro Forma) data are pro forma es timates based on Silver Spike data as of 9/30/23 and CALP Loan Portfolio data as of 1/1/24. 1. Net of estimated expenses related to the Loan Portfolio Acquisition. 2. Estimated Yield to Maturity (“YTM”) includes a variety of fees and features that affect the total yield, which may include, b ut are not limited to, original issue discount (“OID”), exit fees, prepayment fees, unused fees, and contingent features. The es tim ated YTM calculations require management to make estimates and assumptions, including, but not limited to, the timing and amounts of loan draws on delayed dra w loans, the timing and collectability of exit fees, the probability and timing of prepayments, and the probability of contin gen t features occurring. We have not assumed any prepayment penalties or early payoffs in our YTM calculations. Estimated YTM is based on current mana gem ent estimates and assumptions, which may change. Actual results could differ from those estimates and assumptions. For floating rate loans, future Prime Rates are assumed to be equal to the Prime Rate applicable to the current interest payment period. Weighted averag e YTM of loans is gross of expenses, excludes cash holdings, and is calculated using the values of the Silver Spike investmen ts as of 9/30/23 and the values of the CALP Loan Portfolio investments as of 1/1/24. The weighted average YTM of loans would be lower if the calculati on reflected expenses and cash holdings. 3. Calculated as a percentage of the net assets of Silver Spike’s investment portfolio (excluding cash and cash equivalents). Se cto rs follow GICS Sector categorizations. 59% 8% 15% 6% 7% 2% 3% 71% 6% 11% 4% 5% 1% 2%

12 SILVER SPIKE INVESTMENT CORP. ©2024 All Rights Reserved Anticipated Positive Impact to Net Investment Income T HE LOAN PORTFOLIO ACQUISITION IS EXPECTED TO BE ACCRETIVE TO S ILVER S PIKE ’ S NII Potential future accretion achievable with the implementation of leverage Additional scale anticipated to lower the ratio of operating expenses excluding management fees over the net assets of the Company Larger portfolio size D RIVERS OF E XPECTED NII A CCRETION

13 SILVER SPIKE CAPITAL ©2023 All Rights Reserved Appendix

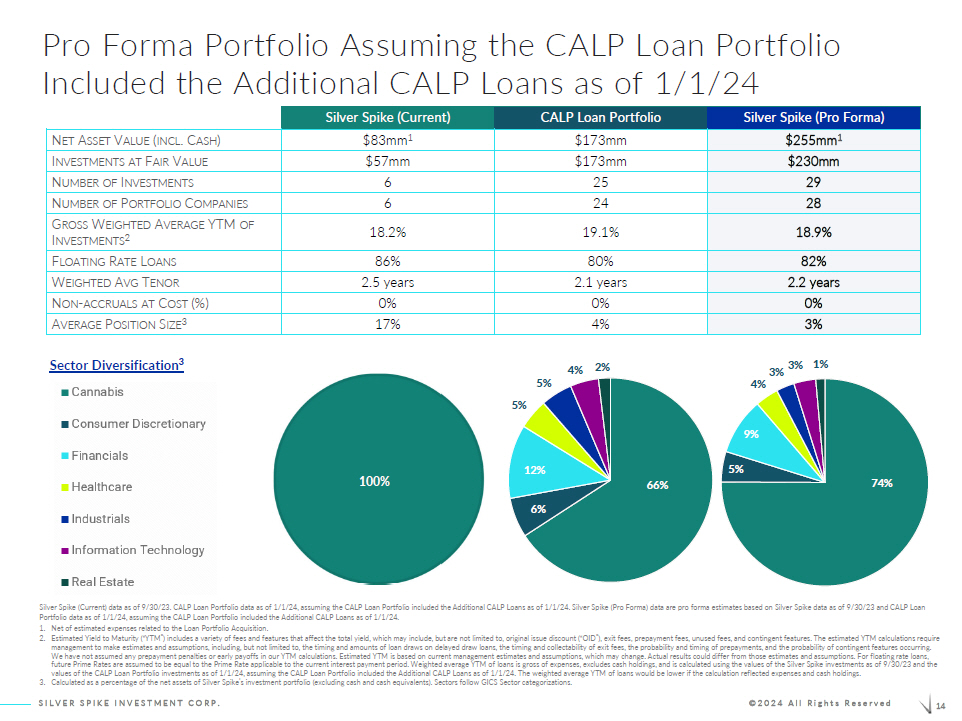

14 SILVER SPIKE INVESTMENT CORP. ©2024 All Rights Reserved Pro Forma Portfolio Assuming the CALP Loan Portfolio Included the Additional CALP Loans as of 1/1/24 Silver Spike (Current) CALP Loan Portfolio Silver Spike (Pro Forma) N ET A SSET V ALUE ( INCL . C ASH ) $83mm 1 $173mm $255mm 1 I NVESTMENTS AT F AIR V ALUE $57mm $173mm $230mm N UMBER OF I NVESTMENTS 6 25 29 N UMBER OF P ORTFOLIO C OMPANIES 6 24 28 G ROSS W EIGHTED A VERAGE YTM OF I NVESTMENTS 2 18.2% 19.1% 18.9% F LOATING R ATE L OANS 86% 80% 82% W EIGHTED A VG T ENOR 2.5 years 2.1 years 2.2 years N ON - ACCRUALS AT C OST (%) 0% 0% 0% A VERAGE P OSITION S IZE 3 17% 4% 3% Sector Diversification 3 100% Silver Spike (Current) data as of 9/30/23. CALP Loan Portfolio data as of 1/1/24, assuming the CALP Loan Portfolio included t he Additional CALP Loans as of 1/1/24. Silver Spike (Pro Forma) data are pro forma estimates based on Silver Spike data as of 9/ 30/ 23 and CALP Loan Portfolio data as of 1/1/24, assuming the CALP Loan Portfolio included the Additional CALP Loans as of 1/1/24. 1. Net of estimated expenses related to the Loan Portfolio Acquisition. 2. Estimated Yield to Maturity (“YTM”) includes a variety of fees and features that affect the total yield, which may include, b ut are not limited to, original issue discount (“OID”), exit fees, prepayment fees, unused fees, and contingent features. The es tim ated YTM calculations require management to make estimates and assumptions, including, but not limited to, the timing and amounts of loan draws on delayed dra w loans, the timing and collectability of exit fees, the probability and timing of prepayments, and the probability of contin gen t features occurring. We have not assumed any prepayment penalties or early payoffs in our YTM calculations. Estimated YTM is based on current mana gem ent estimates and assumptions, which may change. Actual results could differ from those estimates and assumptions. For floating rate loans, future Prime Rates are assumed to be equal to the Prime Rate applicable to the current interest payment period. Weighted averag e YTM of loans is gross of expenses, excludes cash holdings, and is calculated using the values of the Silver Spike investmen ts as of 9/30/23 and the values of the CALP Loan Portfolio investments as of 1/1/24, assuming the CALP Loan Portfolio included the Additional CALP Loa ns as of 1/1/24. The weighted average YTM of loans would be lower if the calculation reflected expenses and cash holdings. 3. Calculated as a percentage of the net assets of Silver Spike’s investment portfolio (excluding cash and cash equivalents). Se cto rs follow GICS Sector categorizations. 66% 6% 12% 5% 5% 4% 2% 74% 5% 9% 4% 3% 3% 1%

CONTACT: B ILL H EALY – P ARTNER BILL @ SILVERSPIKECAP . COM SSIC . SILVERSPIKECAP . COM

v3.24.0.1

| X |

- DefinitionBoolean flag that is true when the XBRL content amends previously-filed or accepted submission.

| Name: |

dei_AmendmentFlag |

| Namespace Prefix: |

dei_ |

| Data Type: |

xbrli:booleanItemType |

| Balance Type: |

na |

| Period Type: |

duration |

|

| X |

- DefinitionFor the EDGAR submission types of Form 8-K: the date of the report, the date of the earliest event reported; for the EDGAR submission types of Form N-1A: the filing date; for all other submission types: the end of the reporting or transition period. The format of the date is YYYY-MM-DD.

| Name: |

dei_DocumentPeriodEndDate |

| Namespace Prefix: |

dei_ |

| Data Type: |

xbrli:dateItemType |

| Balance Type: |

na |

| Period Type: |

duration |

|

| X |

- DefinitionThe type of document being provided (such as 10-K, 10-Q, 485BPOS, etc). The document type is limited to the same value as the supporting SEC submission type, or the word 'Other'.

| Name: |

dei_DocumentType |

| Namespace Prefix: |

dei_ |

| Data Type: |

dei:submissionTypeItemType |

| Balance Type: |

na |

| Period Type: |

duration |

|

| X |

- DefinitionAddress Line 1 such as Attn, Building Name, Street Name

| Name: |

dei_EntityAddressAddressLine1 |

| Namespace Prefix: |

dei_ |

| Data Type: |

xbrli:normalizedStringItemType |

| Balance Type: |

na |

| Period Type: |

duration |

|

| X |

- DefinitionAddress Line 2 such as Street or Suite number

| Name: |

dei_EntityAddressAddressLine2 |

| Namespace Prefix: |

dei_ |

| Data Type: |

xbrli:normalizedStringItemType |

| Balance Type: |

na |

| Period Type: |

duration |

|

| X |

- Definition

+ References

+ Details

| Name: |

dei_EntityAddressCityOrTown |

| Namespace Prefix: |

dei_ |

| Data Type: |

xbrli:normalizedStringItemType |

| Balance Type: |

na |

| Period Type: |

duration |

|

| X |

- DefinitionCode for the postal or zip code

| Name: |

dei_EntityAddressPostalZipCode |

| Namespace Prefix: |

dei_ |

| Data Type: |

xbrli:normalizedStringItemType |

| Balance Type: |

na |

| Period Type: |

duration |

|

| X |

- DefinitionName of the state or province.

| Name: |

dei_EntityAddressStateOrProvince |

| Namespace Prefix: |

dei_ |

| Data Type: |

dei:stateOrProvinceItemType |

| Balance Type: |

na |

| Period Type: |

duration |

|

| X |

- DefinitionA unique 10-digit SEC-issued value to identify entities that have filed disclosures with the SEC. It is commonly abbreviated as CIK. Reference 1: http://www.xbrl.org/2003/role/presentationRef

-Publisher SEC

-Name Exchange Act

-Number 240

-Section 12

-Subsection b-2

| Name: |

dei_EntityCentralIndexKey |

| Namespace Prefix: |

dei_ |

| Data Type: |

dei:centralIndexKeyItemType |

| Balance Type: |

na |

| Period Type: |

duration |

|

| X |

- DefinitionIndicate if registrant meets the emerging growth company criteria. Reference 1: http://www.xbrl.org/2003/role/presentationRef

-Publisher SEC

-Name Exchange Act

-Number 240

-Section 12

-Subsection b-2

| Name: |

dei_EntityEmergingGrowthCompany |

| Namespace Prefix: |

dei_ |

| Data Type: |

xbrli:booleanItemType |

| Balance Type: |

na |

| Period Type: |

duration |

|

| X |

- DefinitionCommission file number. The field allows up to 17 characters. The prefix may contain 1-3 digits, the sequence number may contain 1-8 digits, the optional suffix may contain 1-4 characters, and the fields are separated with a hyphen.

| Name: |

dei_EntityFileNumber |

| Namespace Prefix: |

dei_ |

| Data Type: |

dei:fileNumberItemType |

| Balance Type: |

na |

| Period Type: |

duration |

|

| X |

- DefinitionTwo-character EDGAR code representing the state or country of incorporation.

| Name: |

dei_EntityIncorporationStateCountryCode |

| Namespace Prefix: |

dei_ |

| Data Type: |

dei:edgarStateCountryItemType |

| Balance Type: |

na |

| Period Type: |

duration |

|

| X |

- DefinitionThe exact name of the entity filing the report as specified in its charter, which is required by forms filed with the SEC. Reference 1: http://www.xbrl.org/2003/role/presentationRef

-Publisher SEC

-Name Exchange Act

-Number 240

-Section 12

-Subsection b-2

| Name: |

dei_EntityRegistrantName |

| Namespace Prefix: |

dei_ |

| Data Type: |

xbrli:normalizedStringItemType |

| Balance Type: |

na |

| Period Type: |

duration |

|

| X |

- DefinitionThe Tax Identification Number (TIN), also known as an Employer Identification Number (EIN), is a unique 9-digit value assigned by the IRS. Reference 1: http://www.xbrl.org/2003/role/presentationRef

-Publisher SEC

-Name Exchange Act

-Number 240

-Section 12

-Subsection b-2

| Name: |

dei_EntityTaxIdentificationNumber |

| Namespace Prefix: |

dei_ |

| Data Type: |

dei:employerIdItemType |

| Balance Type: |

na |

| Period Type: |

duration |

|

| X |

- DefinitionLocal phone number for entity.

| Name: |

dei_LocalPhoneNumber |

| Namespace Prefix: |

dei_ |

| Data Type: |

xbrli:normalizedStringItemType |

| Balance Type: |

na |

| Period Type: |

duration |

|

| X |

- DefinitionBoolean flag that is true when the Form 8-K filing is intended to satisfy the filing obligation of the registrant as pre-commencement communications pursuant to Rule 13e-4(c) under the Exchange Act. Reference 1: http://www.xbrl.org/2003/role/presentationRef

-Publisher SEC

-Name Exchange Act

-Number 240

-Section 13e

-Subsection 4c

| Name: |

dei_PreCommencementIssuerTenderOffer |

| Namespace Prefix: |

dei_ |

| Data Type: |

xbrli:booleanItemType |

| Balance Type: |

na |

| Period Type: |

duration |

|

| X |

- DefinitionBoolean flag that is true when the Form 8-K filing is intended to satisfy the filing obligation of the registrant as pre-commencement communications pursuant to Rule 14d-2(b) under the Exchange Act. Reference 1: http://www.xbrl.org/2003/role/presentationRef

-Publisher SEC

-Name Exchange Act

-Number 240

-Section 14d

-Subsection 2b

| Name: |

dei_PreCommencementTenderOffer |

| Namespace Prefix: |

dei_ |

| Data Type: |

xbrli:booleanItemType |

| Balance Type: |

na |

| Period Type: |

duration |

|

| X |

- DefinitionTitle of a 12(b) registered security. Reference 1: http://www.xbrl.org/2003/role/presentationRef

-Publisher SEC

-Name Exchange Act

-Number 240

-Section 12

-Subsection b

| Name: |

dei_Security12bTitle |

| Namespace Prefix: |

dei_ |

| Data Type: |

dei:securityTitleItemType |

| Balance Type: |

na |

| Period Type: |

duration |

|

| X |

- DefinitionName of the Exchange on which a security is registered. Reference 1: http://www.xbrl.org/2003/role/presentationRef

-Publisher SEC

-Name Exchange Act

-Number 240

-Section 12

-Subsection d1-1

| Name: |

dei_SecurityExchangeName |

| Namespace Prefix: |

dei_ |

| Data Type: |

dei:edgarExchangeCodeItemType |

| Balance Type: |

na |

| Period Type: |

duration |

|

| X |

- DefinitionBoolean flag that is true when the Form 8-K filing is intended to satisfy the filing obligation of the registrant as soliciting material pursuant to Rule 14a-12 under the Exchange Act. Reference 1: http://www.xbrl.org/2003/role/presentationRef

-Publisher SEC

-Name Exchange Act

-Section 14a

-Number 240

-Subsection 12

| Name: |

dei_SolicitingMaterial |

| Namespace Prefix: |

dei_ |

| Data Type: |

xbrli:booleanItemType |

| Balance Type: |

na |

| Period Type: |

duration |

|

| X |

- DefinitionTrading symbol of an instrument as listed on an exchange.

| Name: |

dei_TradingSymbol |

| Namespace Prefix: |

dei_ |

| Data Type: |

dei:tradingSymbolItemType |

| Balance Type: |

na |

| Period Type: |

duration |

|

| X |

- DefinitionBoolean flag that is true when the Form 8-K filing is intended to satisfy the filing obligation of the registrant as written communications pursuant to Rule 425 under the Securities Act. Reference 1: http://www.xbrl.org/2003/role/presentationRef

-Publisher SEC

-Name Securities Act

-Number 230

-Section 425

| Name: |

dei_WrittenCommunications |

| Namespace Prefix: |

dei_ |

| Data Type: |

xbrli:booleanItemType |

| Balance Type: |

na |

| Period Type: |

duration |

|

Grafico Azioni Silver Spike Investment (NASDAQ:SSIC)

Storico

Da Mar 2025 a Apr 2025

Grafico Azioni Silver Spike Investment (NASDAQ:SSIC)

Storico

Da Apr 2024 a Apr 2025