UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

SCHEDULE 14A

(RULE 14a-101)

INFORMATION REQUIRED IN PROXY STATEMENT

SCHEDULE 14A INFORMATION

Proxy Statement Pursuant to Section 14(a) of

the

Securities Exchange Act of 1934

(Amendment No.

)

Filed by the Registrant x

Filed by a party other than the Registrant ¨

Check the appropriate box:

| ¨ | Preliminary Proxy Statement |

| ¨ | Confidential, for Use of the Commission Only (as permitted

by Rule 14a-6(e)(2)) |

| ¨ | Definitive Proxy Statement |

| x | Definitive Additional Materials |

| ¨ | Soliciting Material Pursuant to §240.14a-12 |

Cracker Barrel

Old Country Store, Inc.

(Name of Registrant as Specified In Its Charter)

(Name of Person(s) Filing Proxy Statement,

if Other Than The Registrant)

Payment of Filing Fee (Check the appropriate box):

| ¨ | Fee paid previously with preliminary materials. |

| ¨ | Fee computed on table in exhibit required by Item 25(b) per

Exchange Act Rules 14a-6(i)(1) and 0-11 |

On

October 29, 2024, the following presentation was posted by Cracker Barrel Old Country Store, Inc. (the “Company”)

to its proxy solicitation campaign website at www.crackerbarrelshareholders.com (the “Campaign Website”).

| OCTOBER 2024

REINVIGORATING A CHERISHED

BRAND TO CARVE NEW PATHS OF

GROWTH & USHER IN THE NEXT

ERA OF VALUE CREATION |

| FORWARD LOOKING STATEMENTS

Forward-Looking Statements

Except for specific historical information, certain of the matters discussed in this presentation may express or imply projections of items such

as revenues or expenditures, statements of plans and objectives or future operations or statements of future economic performance. These

and similar statements regarding events or results that Cracker Barrel Old Country Store, Inc. (“Cracker Barrel” or the “Company”) expects

will or may occur in the future are forward-looking statements concerning matters that involve risks, uncertainties and other factors which

may cause the actual results and performance of the Company to differ materially from those expressed or implied by such forward-looking

statements. All forward-looking information is provided pursuant to the safe harbor established under the Private Securities Litigation Reform

Act of 1995 and should be evaluated in the context of these risks, uncertainties and other factors. Forward-looking statements generally can

be identified by the use of forward-looking terminology such as "trends," "assumptions," "target," "guidance," "outlook," "opportunity," "future,"

"plans," "goals," "objectives," "expectations," "near-term," "long-term," "projection," "may," "will," "would," "could," "expect," "intend," "estimate,"

"anticipate," "believe," "potential," "regular," "should," "projects," "forecasts," or "continue" (or the negative or other derivatives of each of

these terms) or similar terminology.

The Company believes that the assumptions underlying any forward-looking statements are reasonable; however, any of the assumptions

could be inaccurate, and therefore, actual results may differ materially from those projected in or implied by the forward-looking statements.

In addition to the risks of ordinary business operations, factors and risks that may result in actual results differing from this forward-looking

information include, but are not limited to risks and uncertainties associated with inflationary conditions with respect to the price of

commodities, ingredients, transportation, distribution and labor; disruptions to the Company’s restaurant or retail supply chain; the

Company’s ability to manage retail inventory and merchandise mix; the Company’s ability to sustain or the effects of plans intended to

improve operational or marketing execution and performance, including the Company’s strategic transformation plan; the effects of

increased competition at the Company’s locations on sales and on labor recruiting, cost, and retention; consumer behavior based on

negative publicity or changes in consumer health or dietary trends or safety aspects of the Company’s food or products or those of the

restaurant industry in general, including concerns about outbreaks of infectious disease; the effects of the Company’s indebtedness and

associated restrictions on the Company’s financial and operating flexibility and ability to execute or pursue its operating plans and

objectives; changes in interest rates, increases in borrowed capital or capital market conditions affecting the Company’s financing costs and

ability to refinance its indebtedness, in whole or in part; the Company’s reliance on a single distribution facility and certain significant

vendors, particularly for foreign-sourced retail products; information technology disruptions and data privacy and information security

breaches, whether as a result of infrastructure failures, employee or vendor errors or actions of third parties; the Company’s compliance with

privacy and data protection laws; changes in or implementation of additional governmental or regulatory rules, regulations and

interpretations affecting tax, health and safety, animal welfare, pensions, insurance or other undeterminable areas; the actual results of

pending, future or threatened litigation or governmental investigations; the Company’s ability to manage the impact of negative social media

attention and the costs and effects of negative publicity; the impact of activist shareholders; the Company’s ability to achieve aspirations,

goals and projections related to its environmental, social and governance initiatives; the Company’s ability to enter successfully into new

geographic markets that may be less familiar to it; changes in land, building materials and construction costs; the availability and cost of

suitable sites for restaurant development and the Company’s ability to identify those sites; the Company’s ability to retain key personnel; the

ability of and cost to the Company to recruit, train, and retain qualified hourly and management employees; uncertain performance of

acquired businesses, strategic investments and other initiatives that the Company may pursue from time to time; the effects of business

trends on the outlook for individual restaurant locations and the effect on the carrying value of those locations; general or regional economic

weakness, business and societal conditions and the weather impact on sales and customer travel; discretionary income or personal

expenditure activity of the Company’s customers; implementation of new or changes in interpretation of existing accounting principles

generally accepted in the United States of America ("GAAP"); and other factors described from time to time in the Company’s filings with the

Securities and Exchange Commission (the “SEC”), press releases, and other communications. Any forward-looking statement made by the

Company herein, or elsewhere, speaks only as of the date on which made. The Company expressly disclaims any intent, obligation or

undertaking to update or revise any forward-looking statements made herein to reflect any change in the Company’s expectations with

regard thereto or any change in events, conditions or circumstances on which any such statements are based.

Important Additional Information and Where to Find It

On October 9, 2024, Cracker Barrel filed a definitive proxy statement on Schedule 14A (the “Proxy Statement”) and an accompanying WHITE

proxy card in connection with the solicitation of proxies for the 2024 Annual Meeting of Cracker Barrel shareholders (the “Annual Meeting”).

INVESTORS AND SHAREHOLDERS ARE STRONGLY ENCOURAGED TO READ THE PROXY STATEMENT (INCLUDING ANY AMENDMENTS OR

SUPPLEMENTS THERETO) AND OTHER RELEVANT DOCUMENTS FILED WITH THE SEC CAREFULLY AND IN THEIR ENTIRETY AS THEY CONTAIN

OR WILL CONTAIN IMPORTANT INFORMATION. Shareholders may obtain copies of these documents and other documents filed with the SEC

by Cracker Barrel for no charge at the SEC’s website at www.sec.gov. Copies will also be available at no charge in the Investors section of

Cracker Barrel’s corporate website at www.crackerbarrel.com.

Participants

Cracker Barrel, its directors and its executive officers will be participants in the solicitation of proxies from Cracker Barrel shareholders in

connection with the matters to be considered at the Annual Meeting. Information regarding the names of Cracker Barrel’s directors and

executive officers and certain other individuals and their respective interests in Cracker Barrel by security holdings or otherwise is set forth in

the Proxy Statement. To the extent holdings of such participants in Cracker Barrel's securities have changed since the amounts described in

the Proxy Statement, such changes have been reflected on Initial Statements of Beneficial Ownership on Form 3, Statements of Change in

Ownership on Forms 4 or Annual Statement of Changes in Beneficial Ownership of Securities on Forms 5 filed with the SEC. Copies of these

documents are or will be available at no charge and may be obtained as described in the preceding paragraph.

Third Party Information

Certain information contained in this presentation includes data or information that has been obtained from or is based upon information

from third party sources or publicly available filings made by third parties with the SEC. Although the information is believed to be reliable,

neither Cracker Barrel nor its agents have independently verified the accuracy, currency, or completeness of any of the information from

third party sources referred to in this presentation or ascertained from the underlying economic assumptions relied upon by such third party

sources. Cracker Barrel and its agents disclaim any responsibility or liability whatsoever in respect of any such information derived from such

third party sources.

Non-GAAP Financial Measures

This presentation contains certain non-GAAP financial measures, such as adjusted EBITDA. Such non-GAAP financial measures are not

prepared in accordance with GAAP and have important limitations as analytical tools. Non-GAAP financial measures are supplemental,

should only be used in conjunction with results presented in accordance with GAAP and should not be considered in isolation or as a

substitute for such GAAP results. In addition, such non-GAAP financial measures may not be calculated in the same manner as similarly titled

non-GAAP financial measures presented by other companies. For a reconciliation of these non-GAAP financial measures to the most directly

comparable GAAP financial measure, see the Non-GAAP Reconciliations section of this presentation.

2 |

| After fairly evaluating all of his nominees, we decided

to recommend that one of Biglari’s own nominees,

Michael Goodwin, join the Board – after

appointing Jody Bilney to the Board in 2022 as part of

a settlement agreement with Biglari.

The Board recommends the election of its 10

recommended nominees who we believe have the

best qualifications to grow the value of your Cracker

Barrel investment. By contrast, we believe Mr. Biglari

and Ms. Alberti-Perez would be value destructive.

Afte

to r

Mic

app

a se

The

reco

bes

Bar

and

The Cracker Barrel Board has taken and continues to

take deliberate and thoughtful actions to drive growth

and value creation to address post-pandemic

performance.

Our new CEO, Julie Masino, and bolstered leadership

team are executing a strategic transformation plan

informed by months of data-driven analysis and customer

insights. This plan has the unanimous support of the

Board, including Biglari's own director nominee

appointed by Cracker Barrel in 2022.

We are in the early innings of this transformation – with

positive signs that we are on the right path.

WE ARE HERE

Source: Public filings and company website as of October 2024.

The

tak

and

per

Ou

tea

info

ins

Boa

app

We

pos

This is the 7th time Biglari has pursued a proxy

contest in the past 13 years. Each time his prior

contests came to a vote, shareholders rejected

Biglari’s nominees and positions by significant and

widening margins.

Biglari’s insistence on another proxy contest appears

to be about self-interest – NOT the best interests of

all shareholders.

Nevertheless, the Board interviewed all of Biglari’s

nominees and made multiple settlement offers that

included appointing two of his nominees to the Board.

Biglari rejected all offers and made clear that his

overriding goal was to personally join the Board.

s and company website as of October 2024.

We are asking for your support of CRACKER BARREL’S 10 RECOMMENDED NOMINEES to ensure

we can continue to execute our plan without interruption for the benefit of all shareholders.

3 |

| EXECUTIVE SUMMARY

• We recognized our post-pandemic challenges and underperformance and appointed Julie Masino as CEO in FY 2024 to lead a new chapter of growth

and innovation.

• Julie and the Board, with the assistance of top-tier external advisors, worked for months to conduct a thorough review of strategy and brand position,

which informed the design and implementation of a strategic transformation plan.

• We are now in the early innings of execution of the plan, which is unanimously supported by the full Board, including Biglari’s nominee from 2022,

Jody Bilney.

• This strategic transformation plan is about reinvigorating a beloved brand and making operational changes to adjust our business model to today’s

reality – it is not a financial “turnaround.”

The Board has taken

aggressive steps to

enhance performance

• The strategic transformation plan is focused on key brand and operational changes that will restore growth and profitability by driving relevance and

delivering an experience guests love. It honors what guests cherish about Cracker Barrel while also opening the door to a new community of guests.

• It includes five pillars and specific initiatives aimed at: refining the brand; enhancing the menu; evolving the store and guest experience; winning in

digital and off-premise; and elevating the employee experience.

• We are seeing the plan take hold, as discussed on our last earnings call.

Our strategic

transformation plan is

the right plan

Our plan is working —

don’t jeopardize the

momentum

• The Board and leadership team are working with urgency to deliver on Cracker Barrel’s promise, carve new paths for growth, and usher in the next

era of value creation for Cracker Barrel shareholders.

• We believe the election of Sardar Biglari and Milena Alberti-Perez would endanger the progress we are seeing and jeopardize value creation.

• We are asking for your support to ensure this critical work can continue uninterrupted.

4 |

| EXECUTIVE SUMMARY

• We agreed to put Jody Bilney on our Board in 2022 as part of a settlement with Biglari.

• The Board interviewed all four of Biglari’s original independent nominees, and made multiple settlement offers that included

offering to appoint two of his original nominees to the Board. Biglari owns less than 10% of our stock – we offered nominees that would represent

30% of the Board.

• Biglari rejected these offers outright – and has made it clear his overriding goal is to personally join the Board.

Biglari already has a

director on the Board

and we made multiple

settlement attempts to

avoid another proxy

contest

X Biglari offers no substantive solutions to Cracker Barrel's challenges. He has demonstrated a shallow and outdated understanding of our

guests, our operations, our industry, and the work we are doing.

X Biglari’s track record in restaurants is terrible. Under his leadership, Steak ’n Shake’s traffic and same store sales (“SSS”) significantly declined

and revenue has fallen by a 20.6%1 CAGR since 2018. Western Sizzlin’ system sales fell by ~50% and only 33 units remain as of June 2024.

X Biglari’s focus at Cracker Barrel and other companies where he has been involved appears to be on gains for himself and his fund at the expense

of other shareholders. We believe that his goal is to extract capital from the business, not invest in its growth.

Biglari’s ideas

risk destroying

shareholder value

Cracker Barrel’s

recommended

nominees are the right

ones to advance our

transformation

• Our recommended nominees bring the necessary experience to oversee the Company’s transformation, return the business to growth, and

deliver enhanced value for all shareholders.

• If all 10 recommended nominees are elected to the Board, none will have joined before 2017, and eight will have joined since the beginning of

2020.

• Importantly, two of the Board’s recommended nominees were originally put forward by Biglari – clear evidence of our Board’s openness to

shareholder feedback and outside perspective, no matter the source.

5 1. Decrease in revenues due to reduced traffic, franchising and reduced units. |

| We are executing a long-term strategic

transformation plan that will return

Cracker Barrel to growth and profitability |

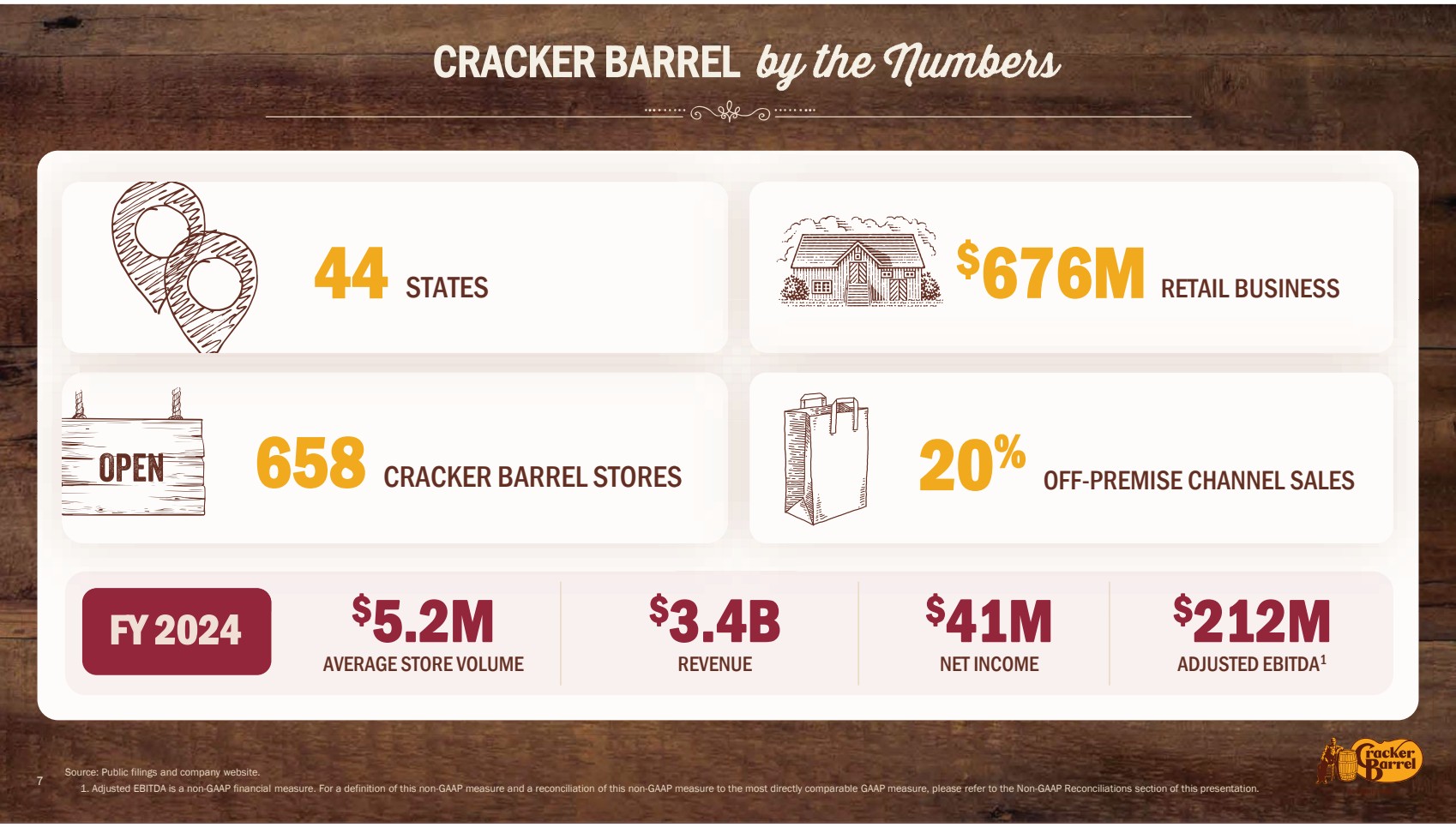

| 7

CRACKER BARREL

44 STATES

658 CRACKER BARREL STORES

$676M RETAIL BUSINESS

20% OFF-PREMISE CHANNEL SALES

FY 2024 $5.2M

AVERAGE STORE VOLUME

$3.4B

REVENUE

$41M

NET INCOME

$212M

ADJUSTED EBITDA1

Source: Public filings and company website.

1. 1. Adjusted EBITDA is a non-GAAP financial measure. For a definition of this non-GAAP measure and a reconciliation of this non-GAAP measure to the most directly comparable GAAP measure, please refer to the Non-GAAP Reconciliations section of this presentation. |

| CRACKER BARREL IS A SPECIAL AND DIFFERENTIATED BRAND WITH UNIQUE

ATTRIBUTES THAT DRIVE OUR DIRECTORS’ SKILL NEEDS

8 1. Source: Black Box Intelligence, as of the week ending October 6, 2024

EVERYDAY VALUE

leveraged to drive traffic, not discounting

LOW AVERAGE CHECK SIZE WITH HIGH VOLUMES

Cracker Barrel average check size $14.58 vs. Casual Dining at $25.981

A BELOVED BRAND

with 55 years of history

LOYAL CUSTOMER BASE

with over 200 million guest

visits per year

AMERICAN STAPLE

that is well-known and

recognized nationwide

OVER 6 MILLION

registered loyalty program members

HIGHLY EXPERIENTIAL BRAND

with significant, profitable, and

complex retail component comprising

~20% of sales

MANY LOCATIONS ALONG

INTERSTATE TRAVEL

CORRIDORS

100%

COMPANY-OWNED

units; no franchisees |

| THE BOARD RECOGNIZED THE NEED FOR CHANGE AND

Casual dining trends, cost

structures, and consumer

behaviors have changed,

particularly post-pandemic

Cracker Barrel needs to refresh

our brand and experience to

delight existing guests and

attract new ones

Brand and business model

investments are needed to adapt

to new generation of guests

9 |

| THE BOARD RECRUITED CEO JULIE MASINO TO CHART A

10

25+ years of experience driving innovation and growth

for globally loved and recognized restaurant and retail brands

As President of International of Taco Bell, she led the

expansion of the division to over 1,000 restaurants in 32 countries

Previously, as North America President of Taco Bell, she

delivered eight consecutive quarters of positive comp growth

while launching culinary, technology, and business model innovations

Previously served in various leadership roles at Starbucks,

Mattel, and as CEO of Sprinkles Cupcakes |

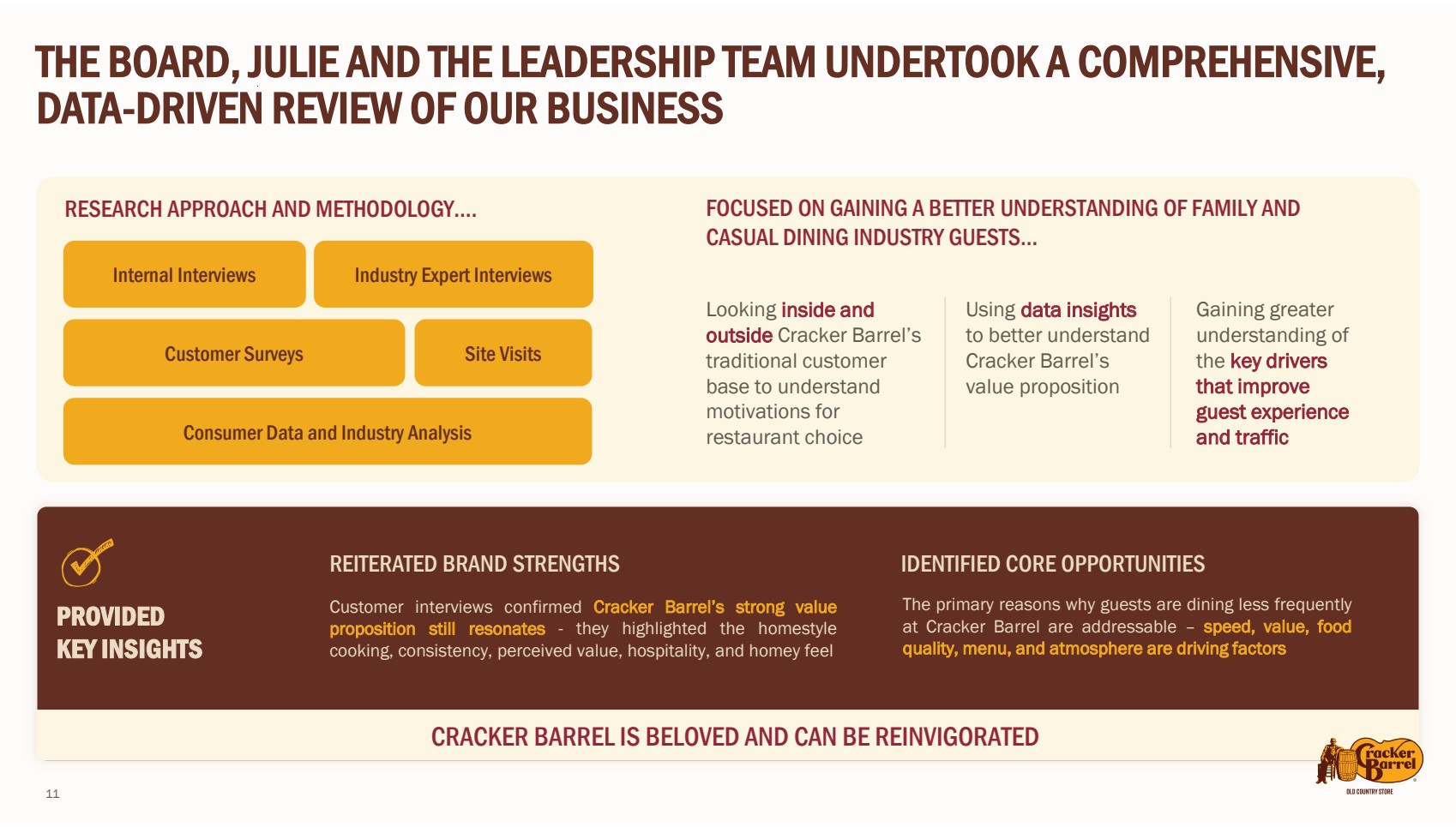

| 11

THE BOARD, JULIE AND THE LEADERSHIP TEAM UNDERTOOK A COMPREHENSIVE,

DATA-DRIVEN REVIEW OF OUR BUSINESS

The primary reasons why guests are dining less frequently

at Cracker Barrel are addressable – speed, value, food

quality, menu, and atmosphere are driving factors

RESEARCH APPROACH AND METHODOLOGY….

Internal Interviews Industry Expert Interviews

Customer Surveys Site Visits

Consumer Data and Industry Analysis

Looking inside and

outside Cracker Barrel’s

traditional customer

base to understand

motivations for

restaurant choice

FOCUSED ON GAINING A BETTER UNDERSTANDING OF FAMILY AND

CASUAL DINING INDUSTRY GUESTS…

Using data insights

to better understand

Cracker Barrel’s

value proposition

Gaining greater

understanding of

the key drivers

that improve

guest experience

and traffic

PROVIDED

KEY INSIGHTS

REITERATED BRAND STRENGTHS IDENTIFIED CORE OPPORTUNITIES

Customer interviews confirmed Cracker Barrel’s strong value

proposition still resonates - they highlighted the homestyle

cooking, consistency, perceived value, hospitality, and homey feel

CRACKER BARREL IS BELOVED AND CAN BE REINVIGORATED |

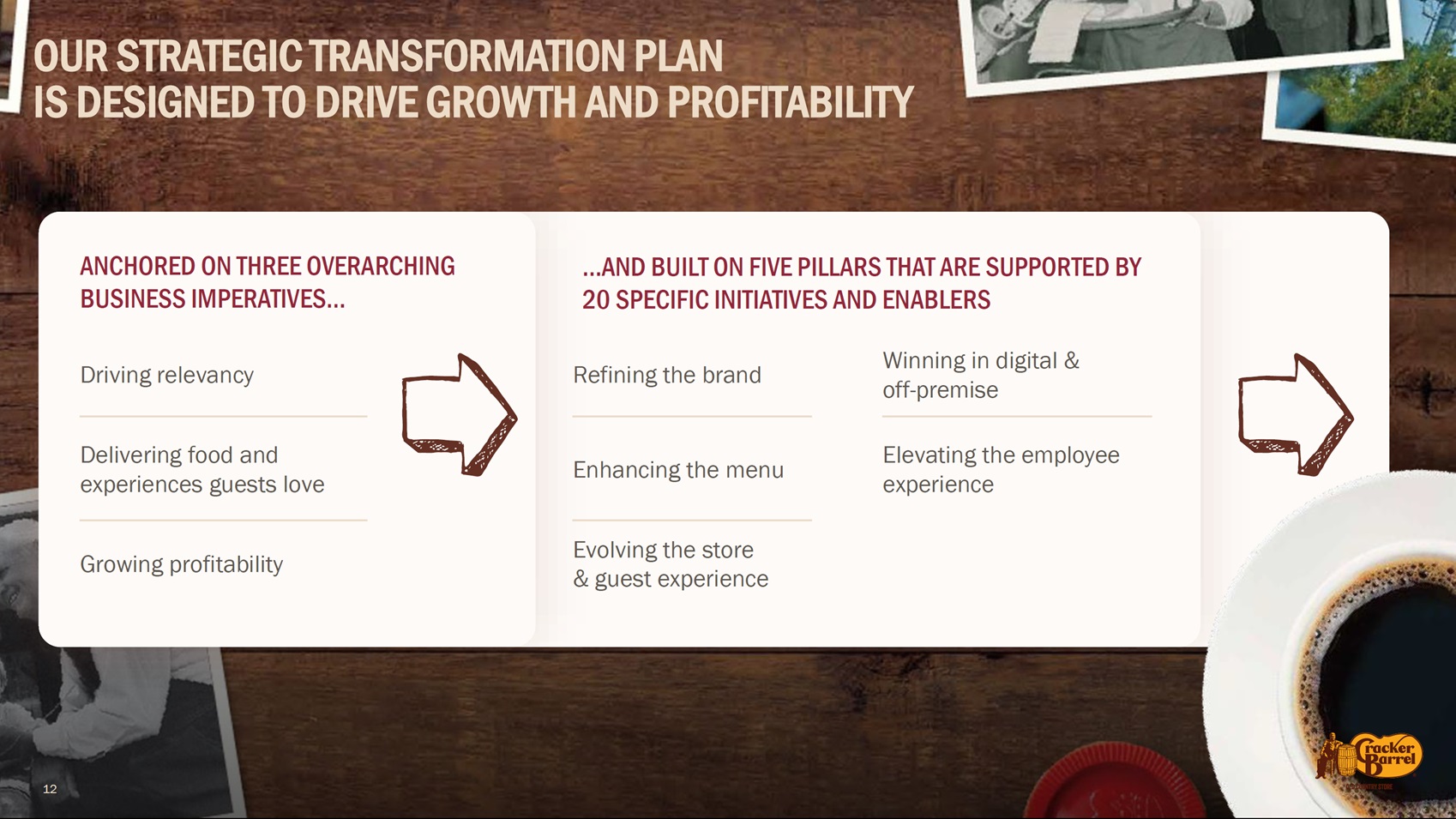

| OUR STRATEGIC TRANSFORMATION PLAN

IS DESIGNED TO DRIVE GROWTH AND PROFITABILITY

ANCHORED ON THREE OVERARCHING

BUSINESS IMPERATIVES…

Driving relevancy

Delivering food and

experiences guests love

Growing profitability

12

…AND BUILT ON FIVE PILLARS THAT ARE SUPPORTED BY

20 SPECIFIC INITIATIVES AND ENABLERS

Refining the brand

Enhancing the menu

Evolving the store

& guest experience

Winning in digital &

off-premise

Elevating the employee

experience |

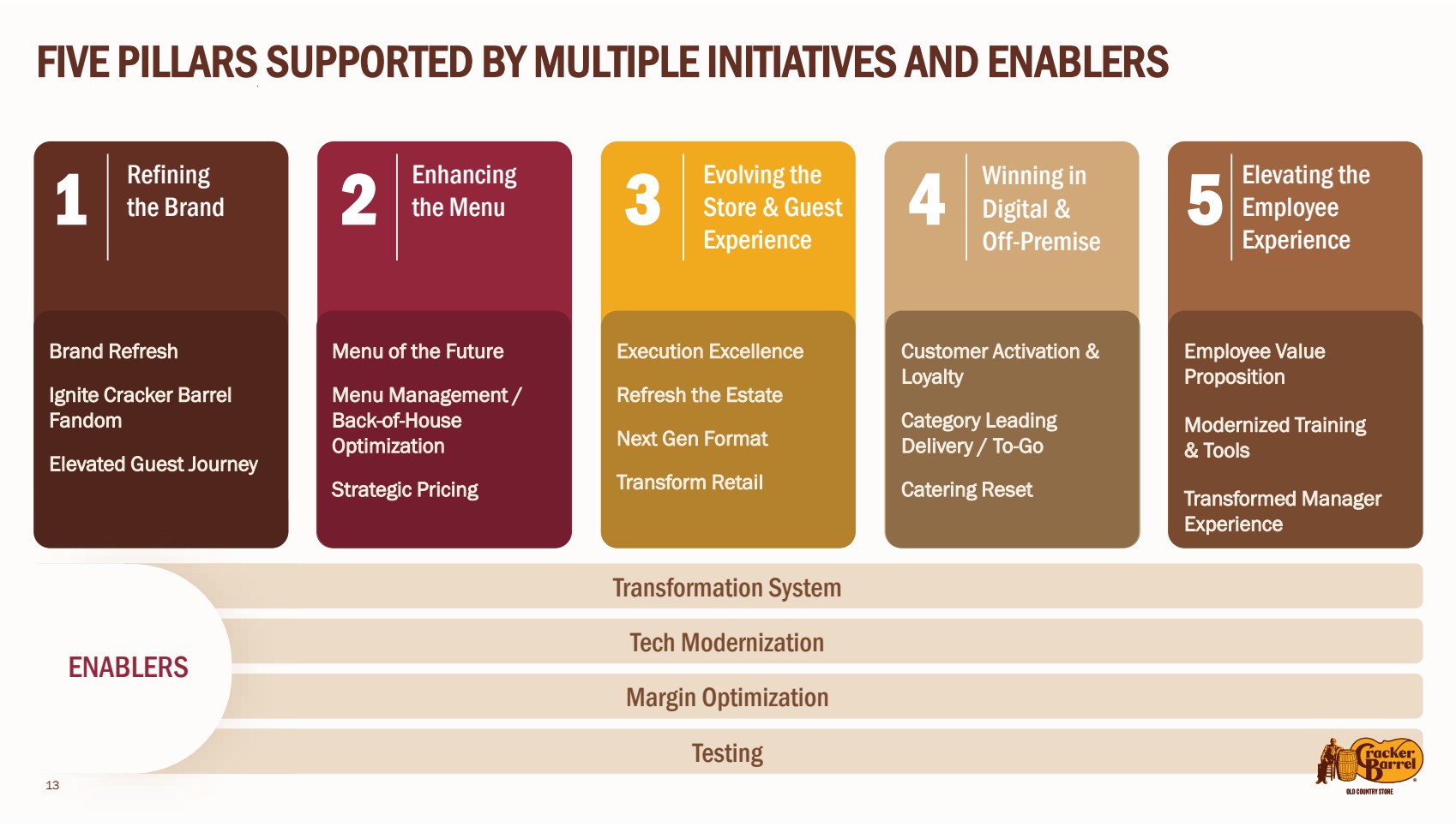

| Enhancing 2 the Menu

13

FIVE PILLARS SUPPORTED BY MULTIPLE INITIATIVES AND ENABLERS

Evolving the

Store & Guest

Experience

Winning in

Digital &

Off-Premise

3 4 Refining 1 the Brand

Brand Refresh

Ignite Cracker Barrel

Fandom

Elevated Guest Journey

Elevating the

Employee

Experience

5

Menu of the Future

Menu Management /

Back-of-House

Optimization

Strategic Pricing

Execution Excellence

Refresh the Estate

Next Gen Format

Transform Retail

Customer Activation &

Loyalty

Category Leading

Delivery / To-Go

Catering Reset

Employee Value

Proposition

Modernized Training

& Tools

Transformed Manager

Experience

Transformation System

Tech Modernization

Margin Optimization

Testing

13

ENABLERS |

| OUR STRATEGIC TRANSFORMATION PLAN TOUCHES EVERY PART OF

OUR BUSINESS

14 Source: Public filings as of October 2024.

We are modernizing and refreshing the Cracker Barrel brand

REFINING THE BRAND

Updating brand platform

and positioning

• Research revealed strong

foundation of customer

love and brand affinity

Completed new customer segmentation

strategy for enhanced targeting

Improving allocation of marketing and

advertising spend across channels |

| Enhanced culinary innovation

and new menu item introduction

process

• Largest proprietary guest

research in brand history

resulted in 60+ items added

to innovation pipeline

• New menu items for lunch

and dinner, leading to 4%

increase in year-over-year day

part traffic

Introduced new menu architecture and

design, improving value scores despite

taking additional price

Optimizing back of house strategy to drive

efficiency, enhance product quality and taste,

and simplify execution in restaurants

OUR STRATEGIC TRANSFORMATION PLAN TOUCHES EVERY PART OF

OUR BUSINESS

15 Source: Public filings as of October 2024.

We are reimagining our menu to highlight signature dishes, while adding

craveable and ownable new items that drive repeat traffic. Additionally, we

are improving our scratch-made processes and strategic pricing

capabilities.

ENHANCING THE MENU

Supply chain innovations to deliver

significant cost savings |

| OUR STRATEGIC TRANSFORMATION PLAN TOUCHES EVERY PART OF

OUR BUSINESS

16 Source: Public filings as of October 2024.

We are focusing on operations, returning our stores to brand standards, and

undertaking a targeted, efficient approach to store refreshes and remodeling

Focusing on metrics that matter

• Improved Google Star rating to

4.2; highest correlation with

SSS growth

• Internal net sentiment scores hit

highest levels

• Seat-to-eat times improved 7%,

one of the biggest pain points for

our guests

Making needed investments in

maintenance and facilities

25+ remodels planned for FY 2025

that enable the team to test different

configurations and spend/investment

levels to optimize the ROIC for

shareholders and speed to market

for the future

EVOLVING THE STORE AND GUEST EXPERIENCE |

| OUR STRATEGIC TRANSFORMATION PLAN TOUCHES EVERY PART OF

OUR BUSINESS

17 Source: Public filings as of October 2024.

WINNING IN DIGITAL AND OFF-PREMISE

We have launched a rewards program to delight guests while providing robust

data and insights to drive the business as we continue to invest in other

technology systems

Over 6 million registered members

in just one year, more members

than initial projections

Rewards delivering incremental

traffic, gross sales, net sales,

restaurant and retail transactions

• 50% more visits and 10% higher

check size from members versus

non-members

• Members also spend 40% more in

the retail department than non-members

• Rewards members showing greater

frequency and overall basket spend

Investing in technology systems

to enhance guest experience and

streamline operations

Unique program where guests have

ability to earn and redeem on both

restaurant and retail purchases |

| OUR STRATEGIC TRANSFORMATION PLAN TOUCHES EVERY PART OF

OUR BUSINESS

18 Source: Public filings as of October 2024.

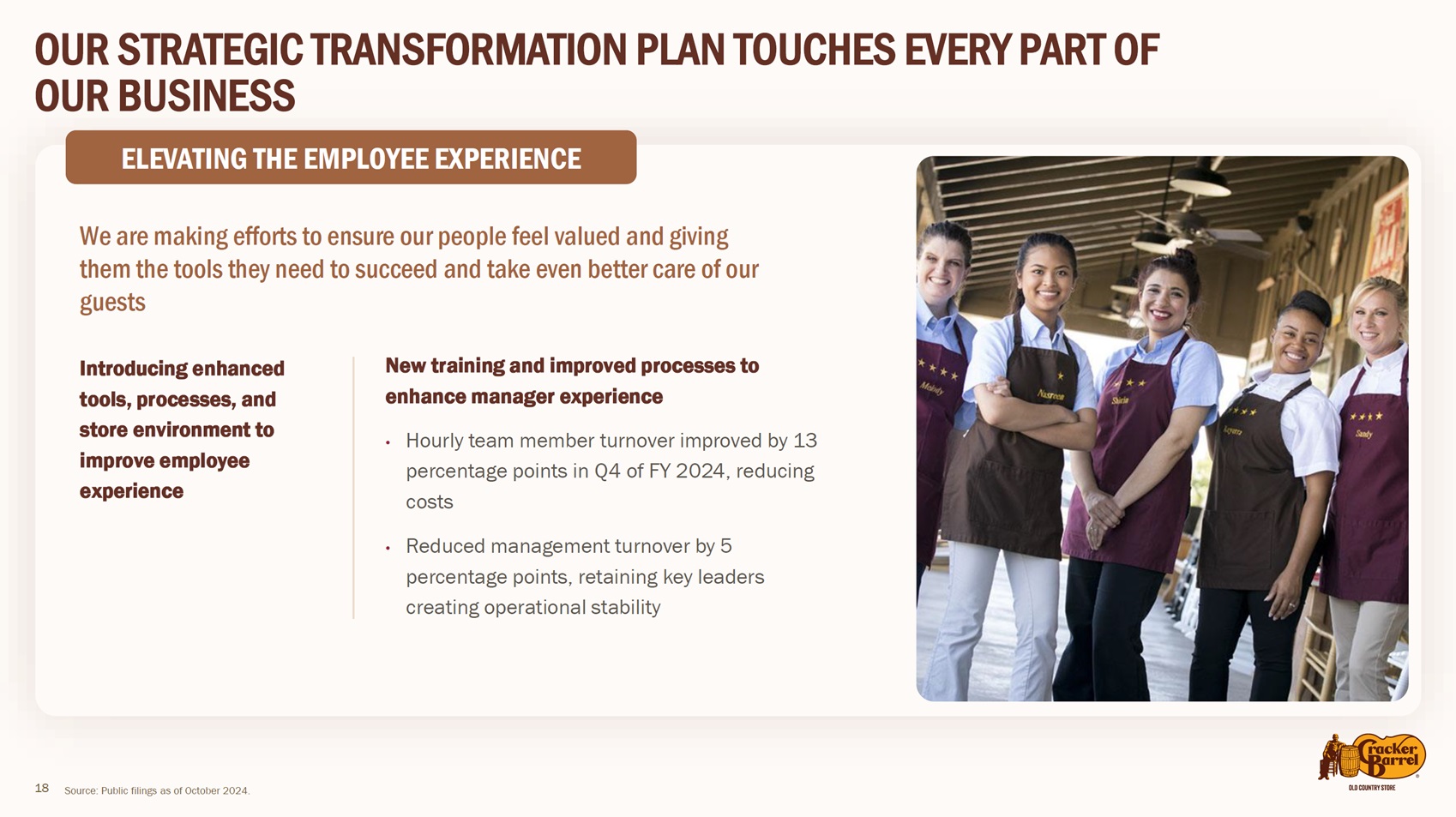

ELEVATING THE EMPLOYEE EXPERIENCE

We are making efforts to ensure our people feel valued and giving

them the tools they need to succeed and take even better care of our

guests

Introducing enhanced

tools, processes, and

store environment to

improve employee

experience

New training and improved processes to

enhance manager experience

• Hourly team member turnover improved by 13

percentage points in Q4 of FY 2024, reducing

costs

• Reduced management turnover by 5

percentage points, retaining key leaders

creating operational stability |

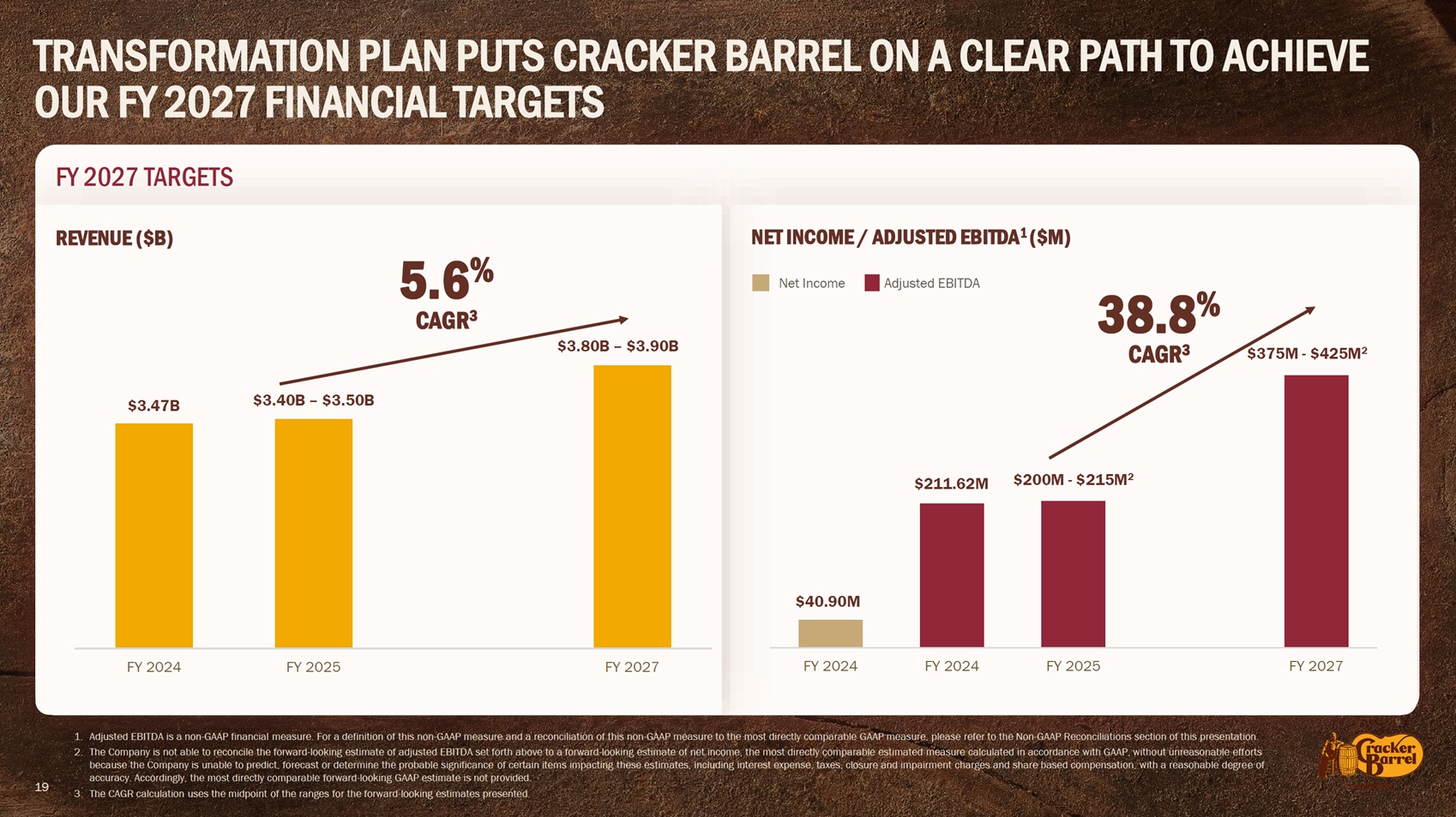

| TRANSFORMATION PLAN PUTS CRACKER BARREL ON A CLEAR PATH TO ACHIEVE

OUR FY 2027 FINANCIAL TARGETS

19

FY 2024 FY 2025 FY 2027

$3.47B

$3.80B – $3.90B

$3.40B – $3.50B

FY 2024 FY 2024 FY 2025 FY 2027

$211.62M

$375M - $425M2

$200M - $215M2

$40.90M

FY 2027 TARGETS

REVENUE ($B) NET INCOME / ADJUSTED EBITDA1 ($M)

1. Adjusted EBITDA is a non-GAAP financial measure. For a definition of this non-GAAP measure and a reconciliation of this non-GAAP measure to the most directly comparable GAAP measure, please refer to the Non-GAAP Reconciliations section of this presentation.

2. The Company is not able to reconcile the forward-looking estimate of adjusted EBITDA set forth above to a forward-looking estimate of net income, the most directly comparable estimated measure calculated in accordance with GAAP, without unreasonable efforts

because the Company is unable to predict, forecast or determine the probable significance of certain items impacting these estimates, including interest expense, taxes, closure and impairment charges and share based compensation, with a reasonable degree of

accuracy. Accordingly, the most directly comparable forward-looking GAAP estimate is not provided.

3. The CAGR calculation uses the midpoint of the ranges for the forward-looking estimates presented.

5 Net Income Adjusted EBITDA .6%

CAGR3 38.8%

CAGR3 |

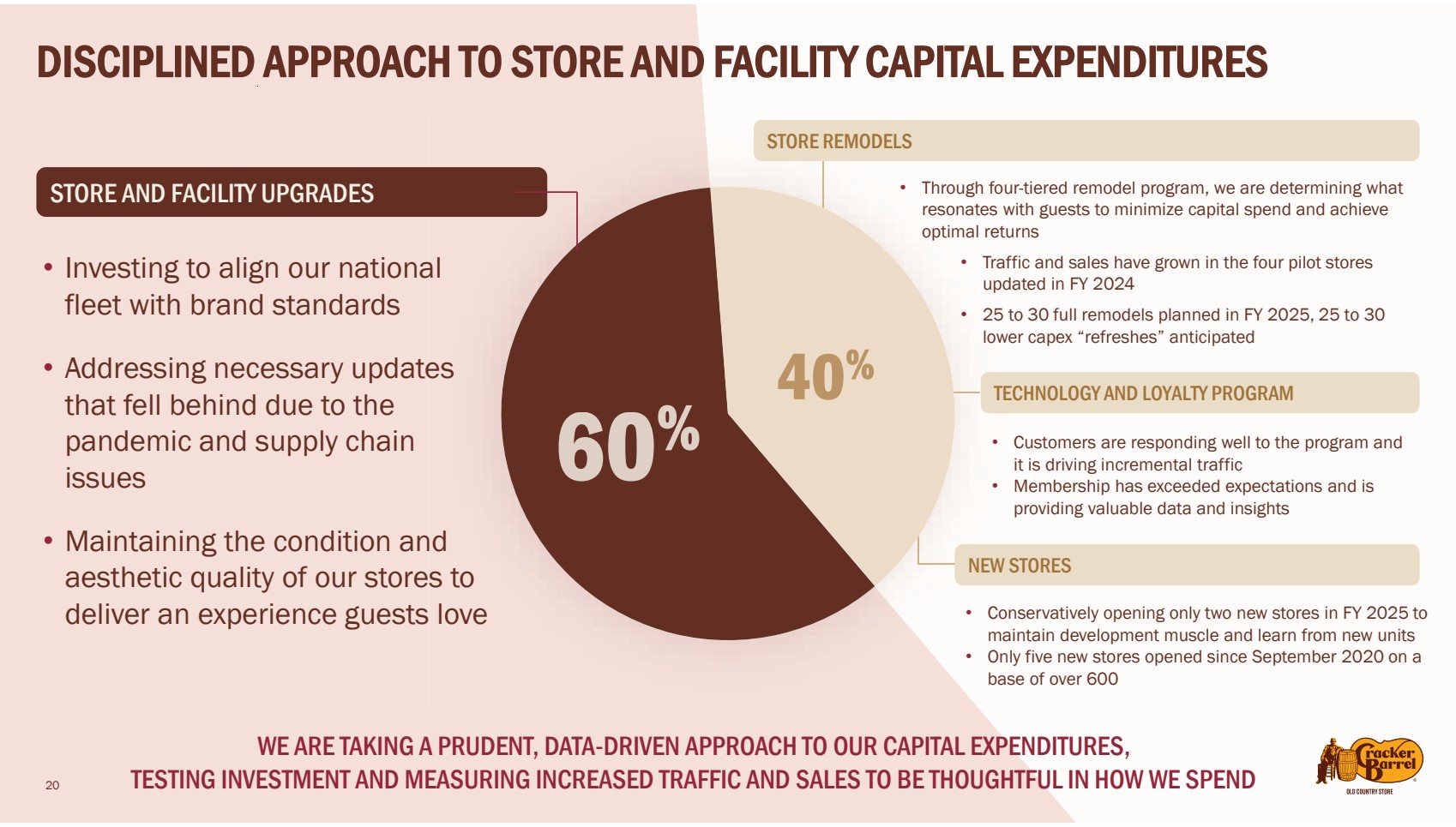

| DISCIPLINED APPROACH TO STORE AND FACILITY CAPITAL EXPENDITURES

WE ARE TAKING A PRUDENT, DATA-DRIVEN APPROACH TO OUR CAPITAL EXPENDITURES,

20 TESTING INVESTMENT AND MEASURING INCREASED TRAFFIC AND SALES TO BE THOUGHTFUL IN HOW WE SPEND

STORE REMODELS

• Through four-tiered remodel program, we are determining what

resonates with guests to minimize capital spend and achieve

optimal returns

• Traffic and sales have grown in the four pilot stores

updated in FY 2024

• 25 to 30 full remodels planned in FY 2025, 25 to 30

lower capex “refreshes” anticipated

TECHNOLOGY AND LOYALTY PROGRAM

• Customers are responding well to the program and

it is driving incremental traffic

• Membership has exceeded expectations and is

providing valuable data and insights

NEW STORES

• Conservatively opening only two new stores in FY 2025 to

maintain development muscle and learn from new units

• Only five new stores opened since September 2020 on a

base of over 600

STORE AND FACILITY UPGRADES

• Investing to align our national

fleet with brand standards

• Addressing necessary updates

that fell behind due to the

pandemic and supply chain

issues

• Maintaining the condition and

aesthetic quality of our stores to

deliver an experience guests love |

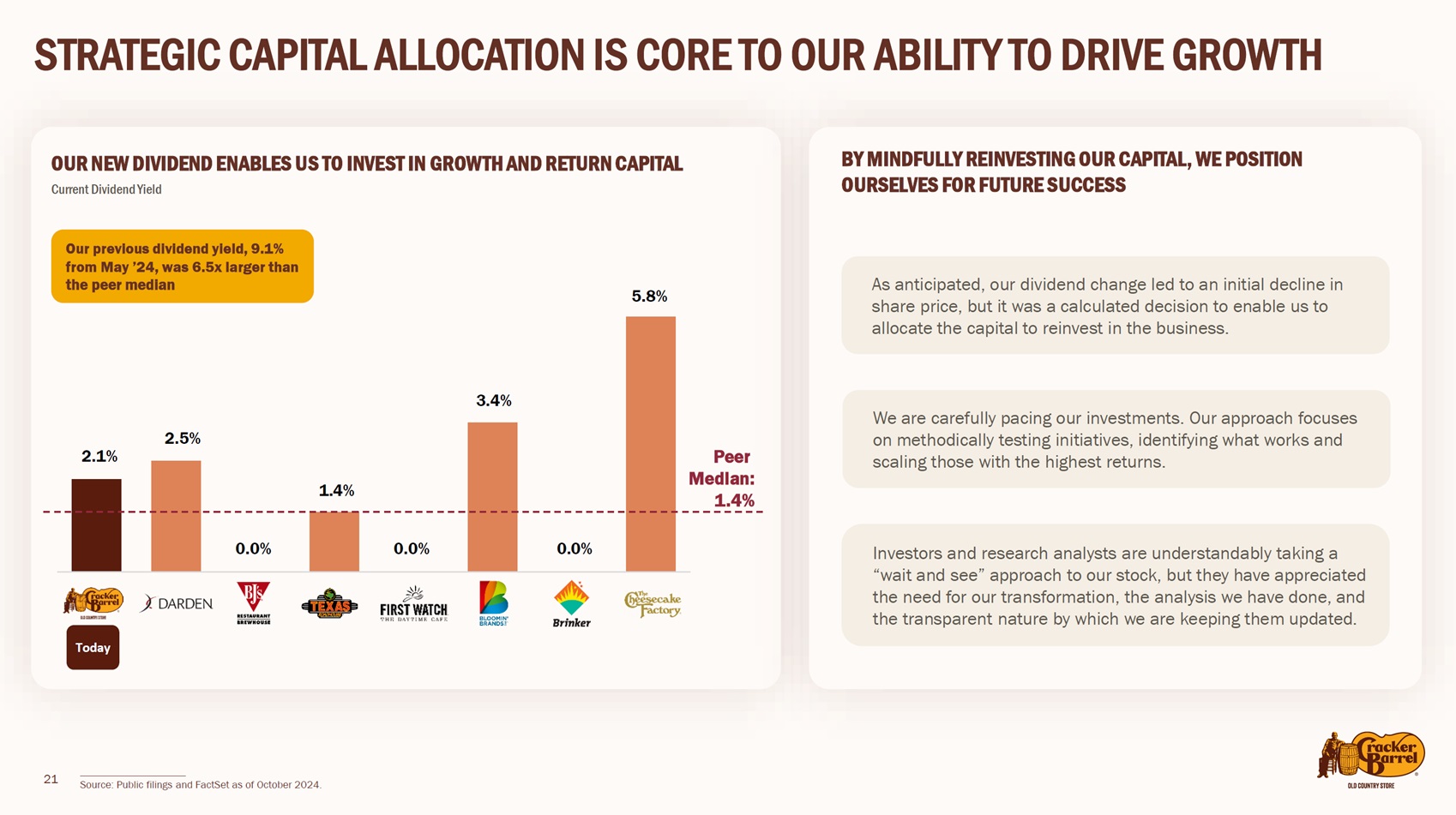

| 2.1%

2.5%

0.0%

1.4%

0.0%

3.4%

0.0%

5.8%

STRATEGIC CAPITAL ALLOCATION IS CORE TO OUR ABILITY TO DRIVE GROWTH

OUR NEW DIVIDEND ENABLES US TO INVEST IN GROWTH AND RETURN CAPITAL

Peer

Median:

1.4%

____________________

Source: Public filings and FactSet as of October 2024.

Current Dividend Yield

As anticipated, our dividend change led to an initial decline in

share price, but it was a calculated decision to enable us to

allocate the capital to reinvest in the business.

We are carefully pacing our investments. Our approach focuses

on methodically testing initiatives, identifying what works and

scaling those with the highest returns.

Investors and research analysts are understandably taking a

“wait and see” approach to our stock, but they have appreciated

the need for our transformation, the analysis we have done, and

the transparent nature by which we are keeping them updated.

BY MINDFULLY REINVESTING OUR CAPITAL, WE POSITION

OURSELVES FOR FUTURE SUCCESS

Today

Our previous dividend yield, 9.1%

from May ’24, was 6.5x larger than

the peer median

2.1%

2.5%

0.0% 0.0% 0.0%

1.4%

3.4%

5.8%

21 |

| HISTORY OF ENGAGING

WITH BIGLARI

We have made multiple attempts to

settle with Biglari and avoid another

unnecessary proxy contest

22 |

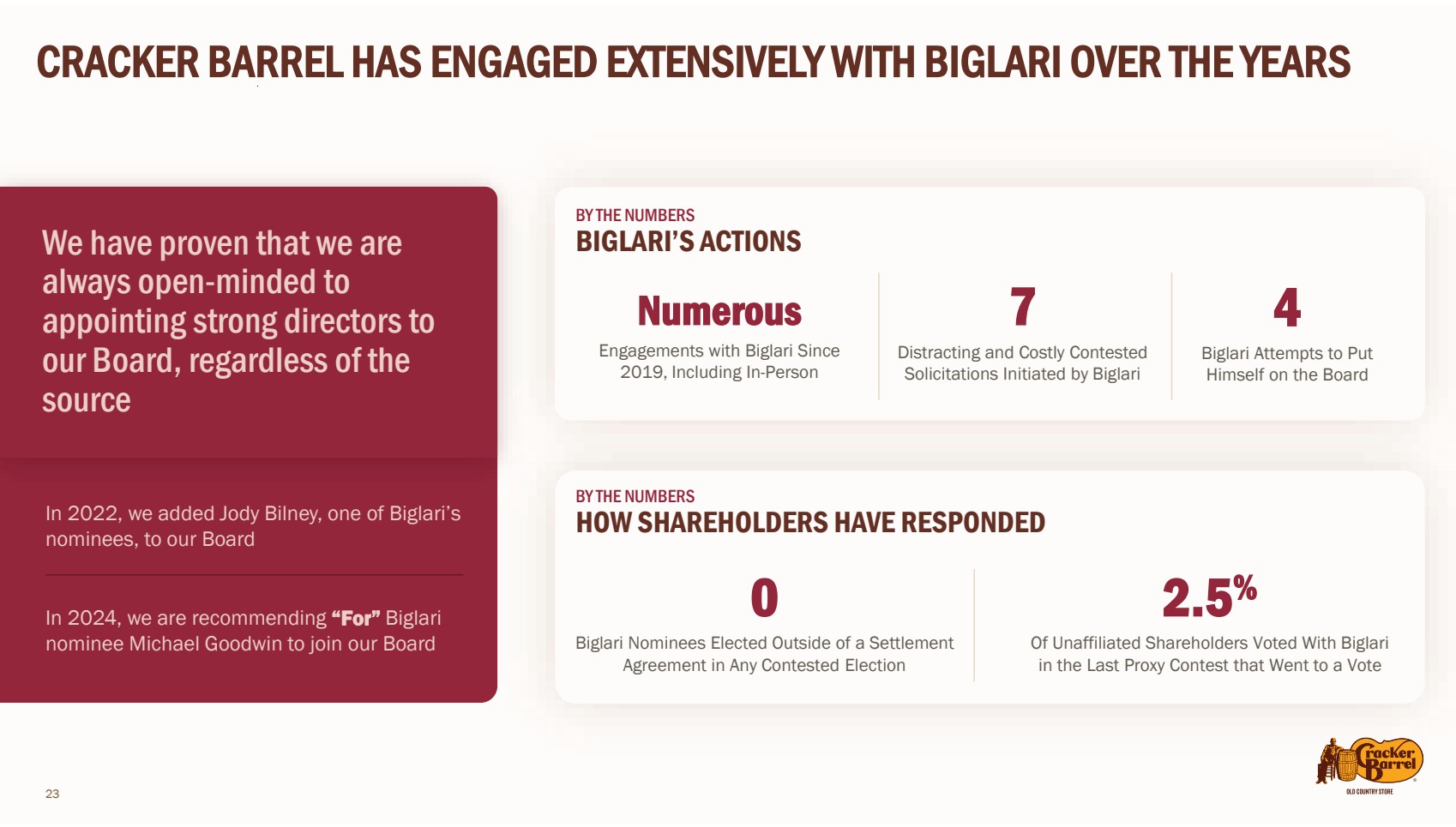

| 23

CRACKER BARREL HAS ENGAGED EXTENSIVELY WITH BIGLARI OVER THE YEARS

Numerous

Engagements with Biglari Since

2019, Including In-Person

2.5%

Of Unaffiliated Shareholders Voted With Biglari

in the Last Proxy Contest that Went to a Vote

4

Biglari Attempts to Put

Himself on the Board

7

Distracting and Costly Contested

Solicitations Initiated by Biglari

0

Biglari Nominees Elected Outside of a Settlement

Agreement in Any Contested Election

We have proven that we are

always open-minded to

appointing strong directors to

our Board, regardless of the

source

In 2022, we added Jody Bilney, one of Biglari’s

nominees, to our Board

In 2024, we are recommending “For” Biglari

nominee Michael Goodwin to join our Board

BY THE NUMBERS

BIGLARI’S ACTIONS

BY THE NUMBERS

HOW SHAREHOLDERS HAVE RESPONDED |

| CRACKER BARREL HAS LOOKED FOR SOLUTIONS BUT BIGLARI IS NOW FORCING

HIS SEVENTH PROXY FIGHT IN 13 YEARS

2011

DECEMBER 2011

Biglari’s proxy fight for one Board

seat was unsuccessful

Unaffiliated Support for Biglari:

26.2%

BIGLARI LOSS

NOVEMBER 2012

ISS and Glass Lewis

recommended rejecting

Biglari’s nominees – one of

which was Biglari himself

All management nominees

were elected

Unaffiliated Support for

Biglari: 9.9%

NOVEMBER –

DECEMBER 2013

Shareholders voted in

favor of all CBRL

nominees

Unaffiliated Support for

Biglari: 8.0%

APRIL 2014

ISS and Glass Lewis recommended

shareholders ignore Biglari’s push

for a sale of CBRL

Biglari’s proposals were voted down

Unaffiliated Support for Biglari:

6.8%

2012 2013–2014 2015–2016

OCTOBER –

NOVEMBER 2015

Biglari opposed CBRL’s

proposal to adopt a

poison pill

Shareholders approved

the poison pill

NOVEMBER 2016

Despite Biglari

withholding votes for

directors, all CBRL

directors were

re-elected

2020–2021

NOVEMBER 2020

Biglari nominated one director,

and after ISS and Glass Lewis

recommended against him –

shareholders re-elected CBRL

directors

Unaffiliated Support for Biglari:

2.5%

DECEMBER 2021

Biglari sent a letter to

shareholders, pushing

CBRL to target a near

100% dividend payout

ratio

2022

JUNE 2022

Biglari sent a follow up letter

nominating two directors

and pushing to replace CEO

Sandy Cochran

SEPTEMBER 2022

CBRL settled with

Biglari and agreed to

appoint one of

Biglari’s director

nominees, Jody

Bilney

Biglari’s previous campaigns that went to a vote were soundly rejected by shareholders by increasingly large margins

WE BELIEVE SARDAR BIGLARI’S FOCUS IS ALWAYS ON

SHORT-TERM GAINS AT THE EXPENSE OF LONG-TERM SUCCESS

BIGLARI LOSS BIGLARI LOSS

BIGLARI LOSS

BIGLARI LOSS

BIGLARI LOSS

24 |

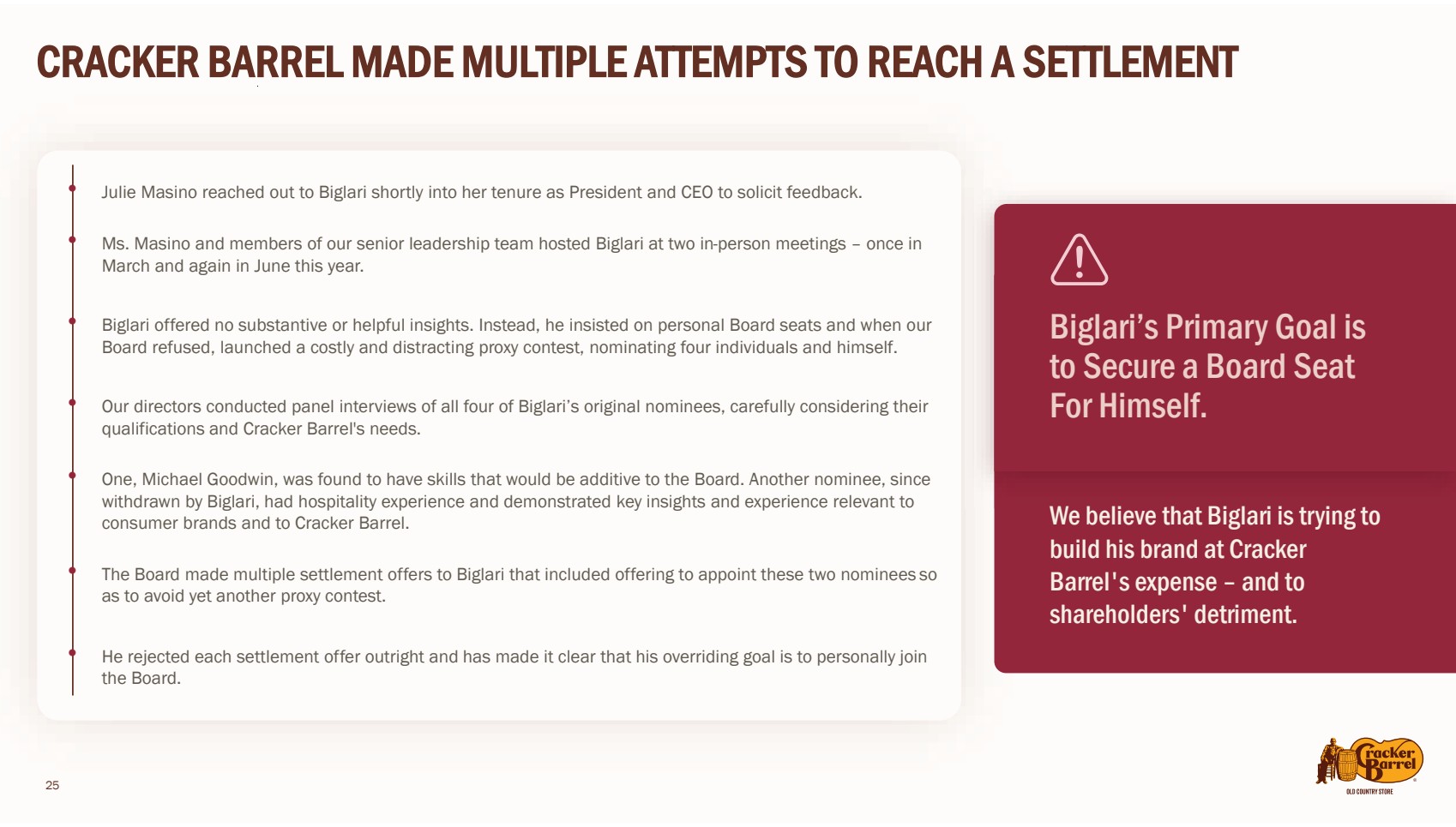

| CRACKER BARREL MADE MULTIPLE ATTEMPTS TO REACH A SETTLEMENT

Biglari’s Primary Goal is

to Secure a Board Seat

For Himself.

We believe that Biglari is trying to

build his brand at Cracker

Barrel's expense – and to

shareholders' detriment.

• Julie Masino reached out to Biglari shortly into her tenure as President and CEO to solicit feedback.

• Ms. Masino and members of our senior leadership team hosted Biglari at two in-person meetings – once in

March and again in June this year.

• Biglari offered no substantive or helpful insights. Instead, he insisted on personal Board seats and when our

Board refused, launched a costly and distracting proxy contest, nominating four individuals and himself.

• Our directors conducted panel interviews of all four of Biglari’s original nominees, carefully considering their

qualifications and Cracker Barrel's needs.

• One, Michael Goodwin, was found to have skills that would be additive to the Board. Another nominee, since

withdrawn by Biglari, had hospitality experience and demonstrated key insights and experience relevant to

consumer brands and to Cracker Barrel.

• The Board made multiple settlement offers to Biglari that included offering to appoint these two nominees so

as to avoid yet another proxy contest.

• He rejected each settlement offer outright and has made it clear that his overriding goal is to personally join

the Board.

25 |

| 26

BIGLARI WOULD HAVE TWO DIRECTORS ON THE BOARD WITH OUR SLATE OF

RECOMMENDED NOMINEES

1. Source: Biglari Capital Corp. Definitive Proxy Statement filed October 10, 2024

Jody Bilney has provided outstanding contributions since joining the Board in 2022.

Her deep understanding of marketing and consumer expertise helped shape the

strategic transformation plan, which she actively helped design and enthusiastically

supports.

JODY BILNEY

Independent Director

Originally nominated

by Biglari in 2022

MICHAEL GOODWIN1

Independent Director Nominee

Biglari nominee recommended

“For” by Cracker Barrel Board

Deep public company executive experience at

Humana, Inc., Bloomin’ Brands, Inc., Charles Schwab

Corporation, and Verizon Communications, Inc.

Restaurant Industry branding expertise having served

as Chief Brand Officer for Bloomin’ Brands, one of the

largest casual dining restaurant companies in the world

Extensive public company board experience, including

at Chuy’s Holdings, Inc., Masonite International

Corporation, and Alignment Healthcare, Inc.

Multi unit restaurant experience as both an executive

(Bloomin’ Brands) and Board member (Chuy’s)

RELEVANT EXPERIENCE TO CRACKER BARREL

30+ years of information technology and

cybersecurity experience at retail and

consumer brands, including as Chief

Information Technology Officer of PetSmart

Held several positions of increasing

responsibility at Hallmark Cards including

Chief Information Officer

Extensive experience serving in public and

private boards, including as current

director on the Burlington Stores board

RELEVANT EXPERIENCE TO CRACKER BARREL

The Board interviewed Michael Goodwin and believes he has the skills, experience,

and knowledge of retail and consumer brands to make him an outstanding Cracker

Barrel director.

We are taking the unusual step of recommending he replace Tom Barr, who is not

standing for reelection. |

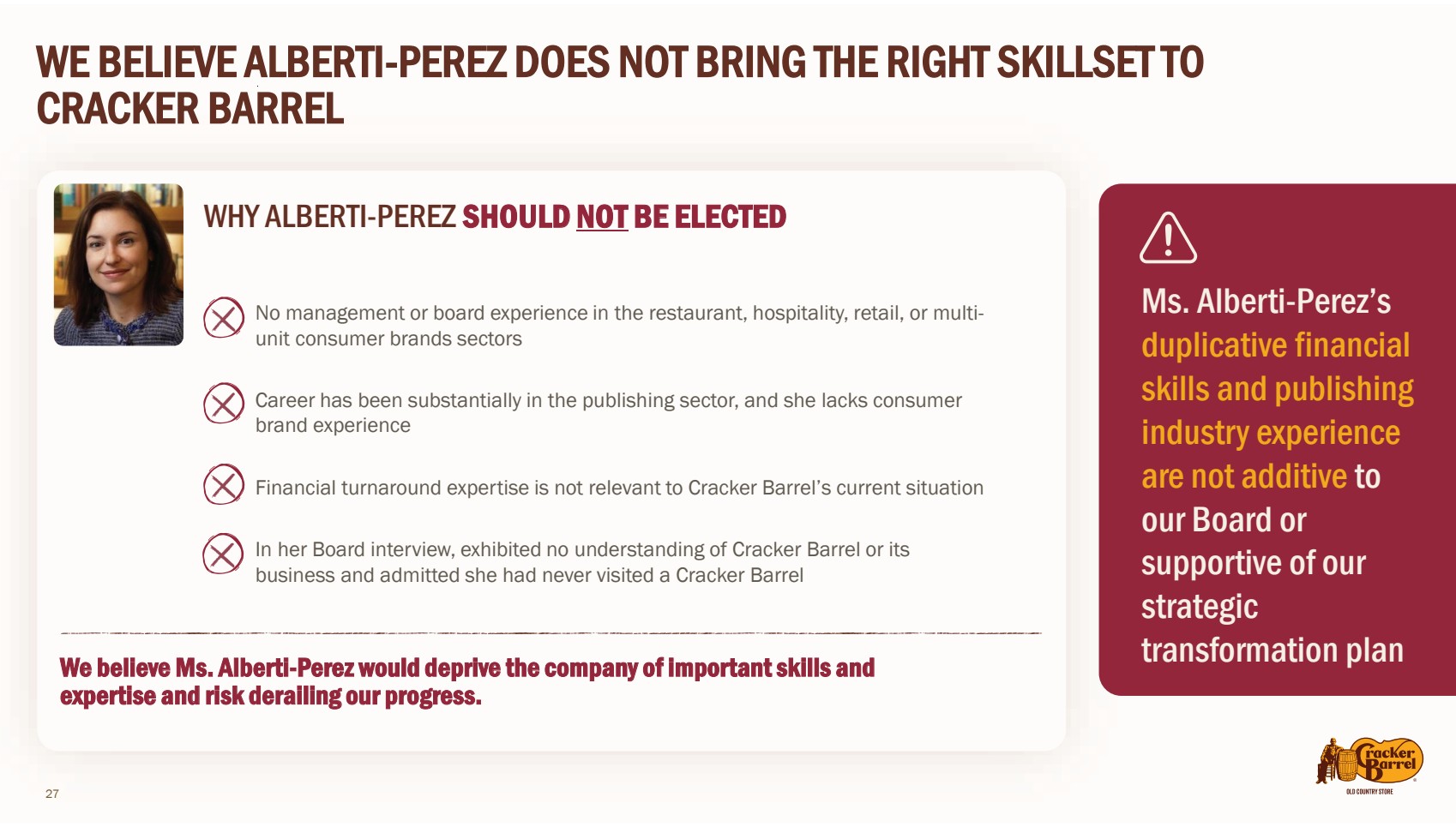

| 27

WE BELIEVE ALBERTI-PEREZ DOES NOT BRING THE RIGHT SKILLSET TO

CRACKER BARREL

WHY ALBERTI-PEREZ SHOULD NOT BE ELECTED

No management or board experience in the restaurant, hospitality, retail, or multi-unit consumer brands sectors

Career has been substantially in the publishing sector, and she lacks consumer

brand experience

Financial turnaround expertise is not relevant to Cracker Barrel’s current situation

In her Board interview, exhibited no understanding of Cracker Barrel or its

business and admitted she had never visited a Cracker Barrel

We believe Ms. Alberti-Perez would deprive the company of important skills and

expertise and risk derailing our progress.

Ms. Alberti-Perez’s

duplicative financial

skills and publishing

industry experience

are not additive to

our Board or

supportive of our

strategic

transformation plan |

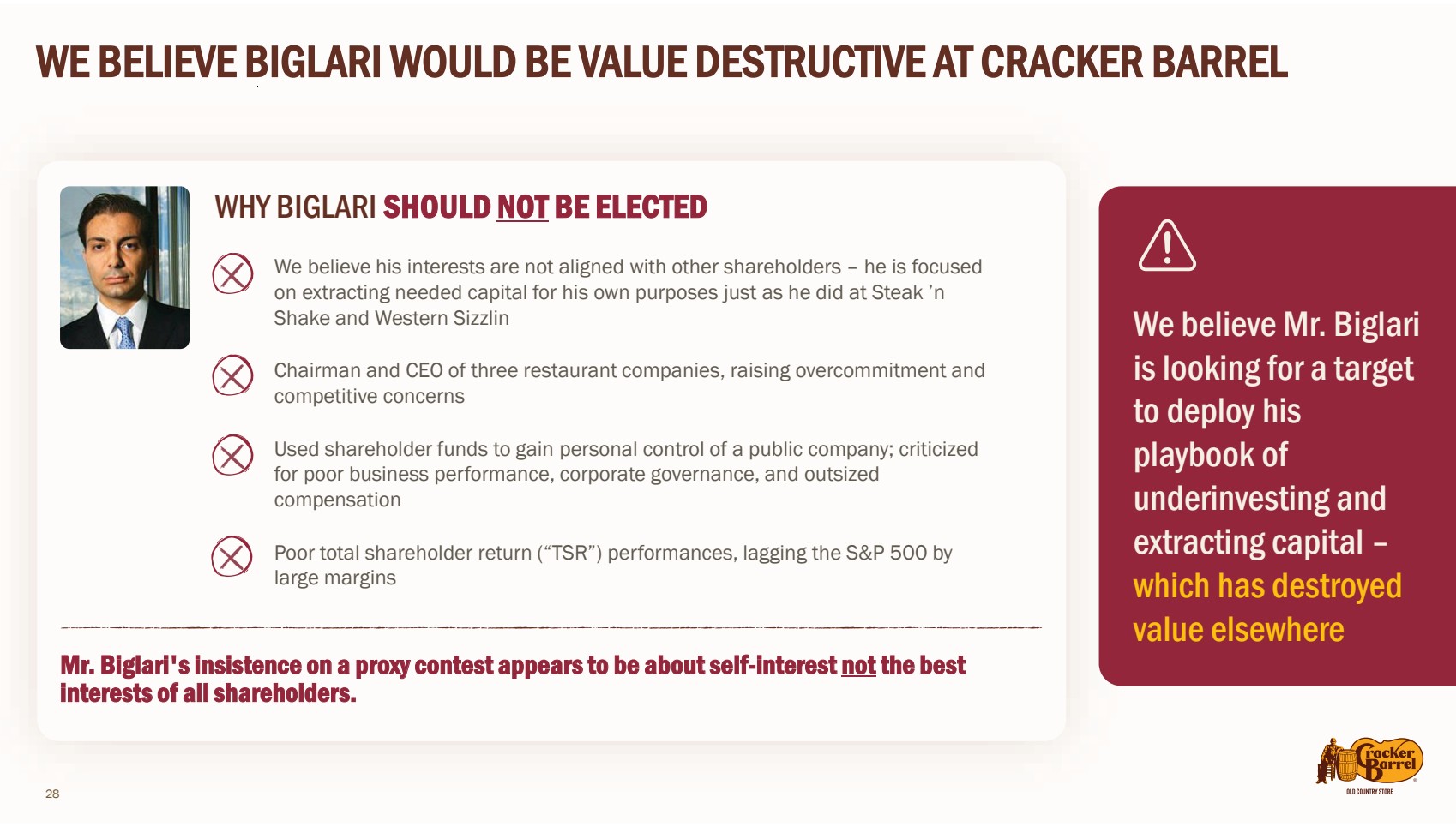

| 28

WE BELIEVE BIGLARI WOULD BE VALUE DESTRUCTIVE AT CRACKER BARREL

We believe Mr. Biglari

is looking for a target

to deploy his

playbook of

underinvesting and

extracting capital –

which has destroyed

value elsewhere

WHY BIGLARI SHOULD NOT BE ELECTED

We believe his interests are not aligned with other shareholders – he is focused

on extracting needed capital for his own purposes just as he did at Steak ’n

Shake and Western Sizzlin

Chairman and CEO of three restaurant companies, raising overcommitment and

competitive concerns

Used shareholder funds to gain personal control of a public company; criticized

for poor business performance, corporate governance, and outsized

compensation

Poor total shareholder return (“TSR”) performances, lagging the S&P 500 by

large margins

Mr. Biglari's insistence on a proxy contest appears to be about self-interest not the best

interests of all shareholders. |

| BIGLARI’S POOR

TRACK RECORD

29

Sardar Biglari’s history of shareholder

value destruction and bad governance |

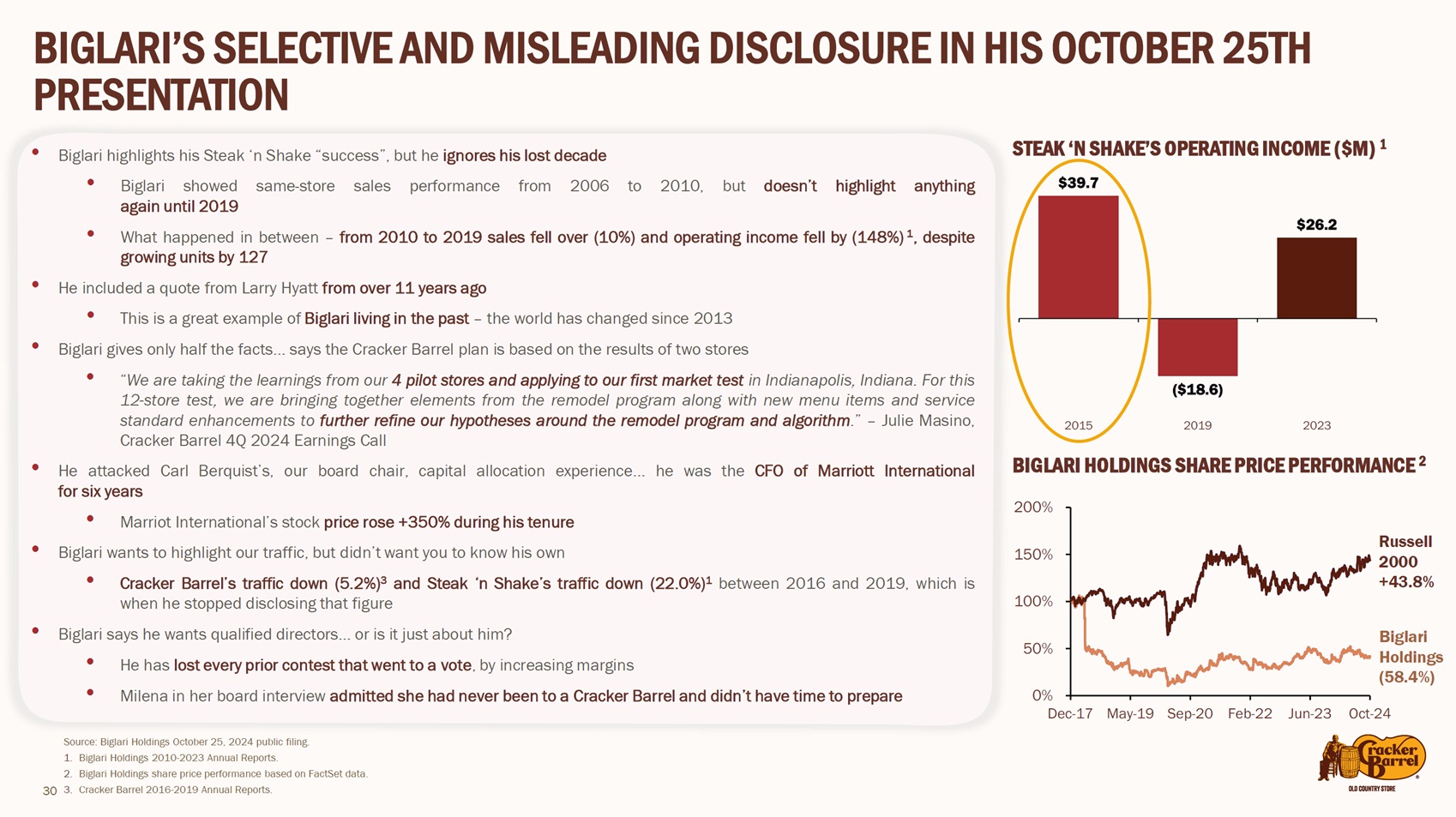

| 30

BIGLARI’S SELECTIVE AND MISLEADING DISCLOSURE IN HIS OCTOBER 25TH

PRESENTATION

• Biglari highlights his Steak ‘n Shake “success”, but he ignores his lost decade

• Biglari showed same-store sales performance from 2006 to 2010, but doesn’t highlight anything

again until 2019

• What happened in between – from 2010 to 2019 sales fell over (10%) and operating income fell by (148%) 1, despite

growing units by 127

• He included a quote from Larry Hyatt from over 11 years ago

• This is a great example of Biglari living in the past – the world has changed since 2013

• Biglari gives only half the facts… says the Cracker Barrel plan is based on the results of two stores

• “We are taking the learnings from our 4 pilot stores and applying to our first market test in Indianapolis, Indiana. For this

12-store test, we are bringing together elements from the remodel program along with new menu items and service

standard enhancements to further refine our hypotheses around the remodel program and algorithm.” – Julie Masino,

Cracker Barrel 4Q 2024 Earnings Call

• He attacked Carl Berquist’s, our board chair, capital allocation experience… he was the CFO of Marriott International

for six years

• Marriot International’s stock price rose +350% during his tenure

• Biglari wants to highlight our traffic, but didn’t want you to know his own

• Cracker Barrel’s traffic down (5.2%)3 and Steak ‘n Shake’s traffic down (22.0%)1 between 2016 and 2019, which is

when he stopped disclosing that figure

• Biglari says he wants qualified directors… or is it just about him?

• He has lost every prior contest that went to a vote, by increasing margins

• Milena in her board interview admitted she had never been to a Cracker Barrel and didn’t have time to prepare

$39.7

($18.6)

$26.2

2015 2019 2023

Source: Biglari Holdings October 25, 2024 public filing.

1. Biglari Holdings 2010-2023 Annual Reports.

2. Biglari Holdings share price performance based on FactSet data.

3. Cracker Barrel 2016-2019 Annual Reports.

STEAK ‘N SHAKE’S OPERATING INCOME ($M) 1

BIGLARI HOLDINGS SHARE PRICE PERFORMANCE 2

0%

50%

100%

150%

200%

Dec-17 May-19 Sep-20 Feb-22 Jun-23 Oct-24

Russell

2000

+43.8%

Biglari

Holdings

(58.4%) |

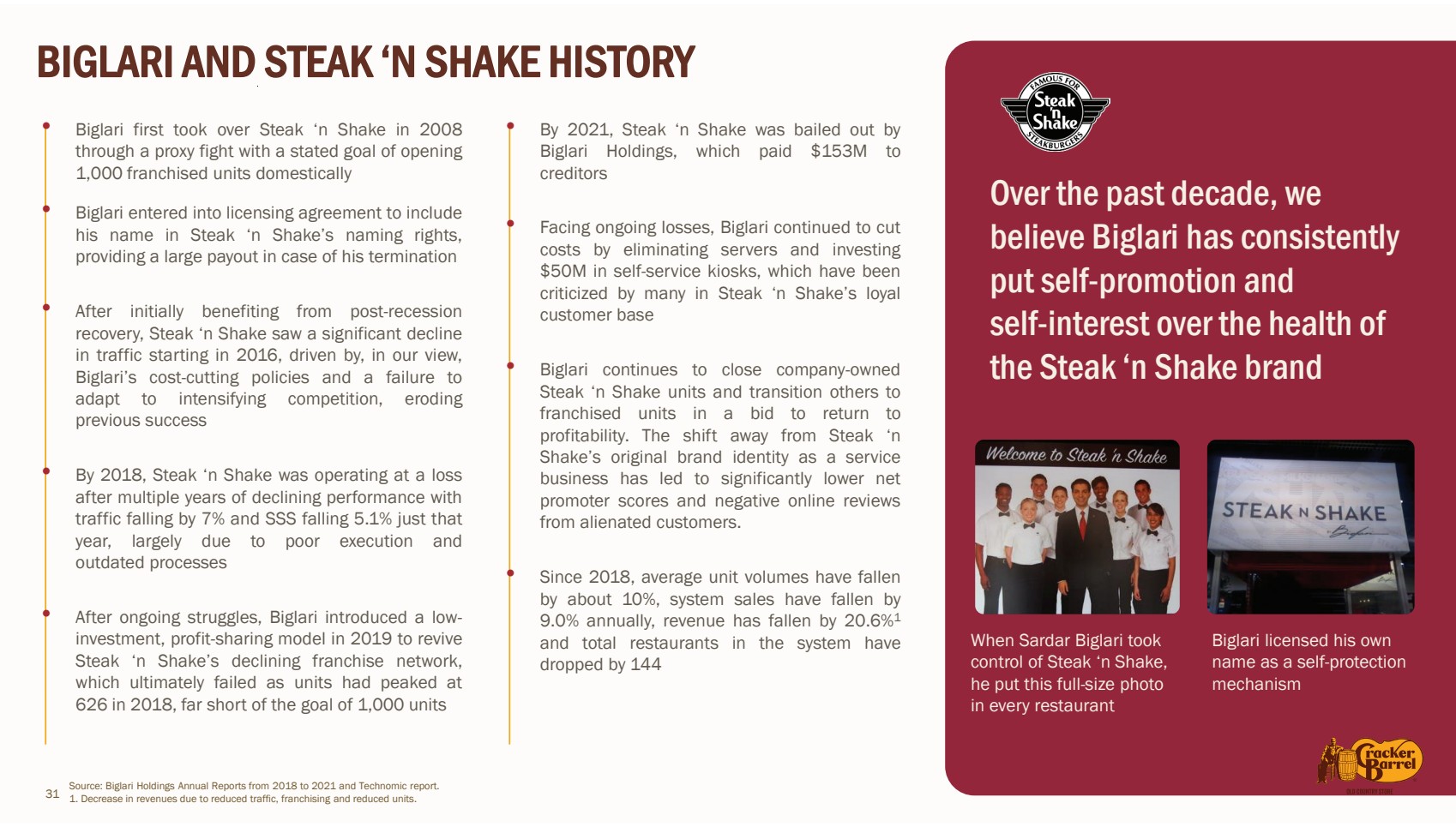

| 31

BIGLARI AND STEAK ‘N SHAKE HISTORY

Over the past decade, we

believe Biglari has consistently

put self-promotion and

self-interest over the health of

the Steak ‘n Shake brand

• Biglari first took over Steak ‘n Shake in 2008

through a proxy fight with a stated goal of opening

1,000 franchised units domestically

• Biglari entered into licensing agreement to include

his name in Steak ‘n Shake’s naming rights,

providing a large payout in case of his termination

• After initially benefiting from post-recession

recovery, Steak ‘n Shake saw a significant decline

in traffic starting in 2016, driven by, in our view,

Biglari’s cost-cutting policies and a failure to

adapt to intensifying competition, eroding

previous success

• By 2018, Steak ‘n Shake was operating at a loss

after multiple years of declining performance with

traffic falling by 7% and SSS falling 5.1% just that

year, largely due to poor execution and

outdated processes

• After ongoing struggles, Biglari introduced a low-investment, profit-sharing model in 2019 to revive

Steak ‘n Shake’s declining franchise network,

which ultimately failed as units had peaked at

626 in 2018, far short of the goal of 1,000 units

• By 2021, Steak ‘n Shake was bailed out by

Biglari Holdings, which paid $153M to

creditors

• Facing ongoing losses, Biglari continued to cut

costs by eliminating servers and investing

$50M in self-service kiosks, which have been

criticized by many in Steak ‘n Shake’s loyal

customer base

• Biglari continues to close company-owned

Steak ‘n Shake units and transition others to

franchised units in a bid to return to

profitability. The shift away from Steak ‘n

Shake’s original brand identity as a service

business has led to significantly lower net

promoter scores and negative online reviews

from alienated customers.

• Since 2018, average unit volumes have fallen

by about 10%, system sales have fallen by

9.0% annually, revenue has fallen by 20.6%1

and total restaurants in the system have

dropped by 144

When Sardar Biglari took

control of Steak ‘n Shake,

he put this full-size photo

in every restaurant

Source: Biglari Holdings Annual Reports from 2018 to 2021 and Technomic report.

1. Decrease in revenues due to reduced traffic, franchising and reduced units.

Biglari licensed his own

name as a self-protection

mechanism |

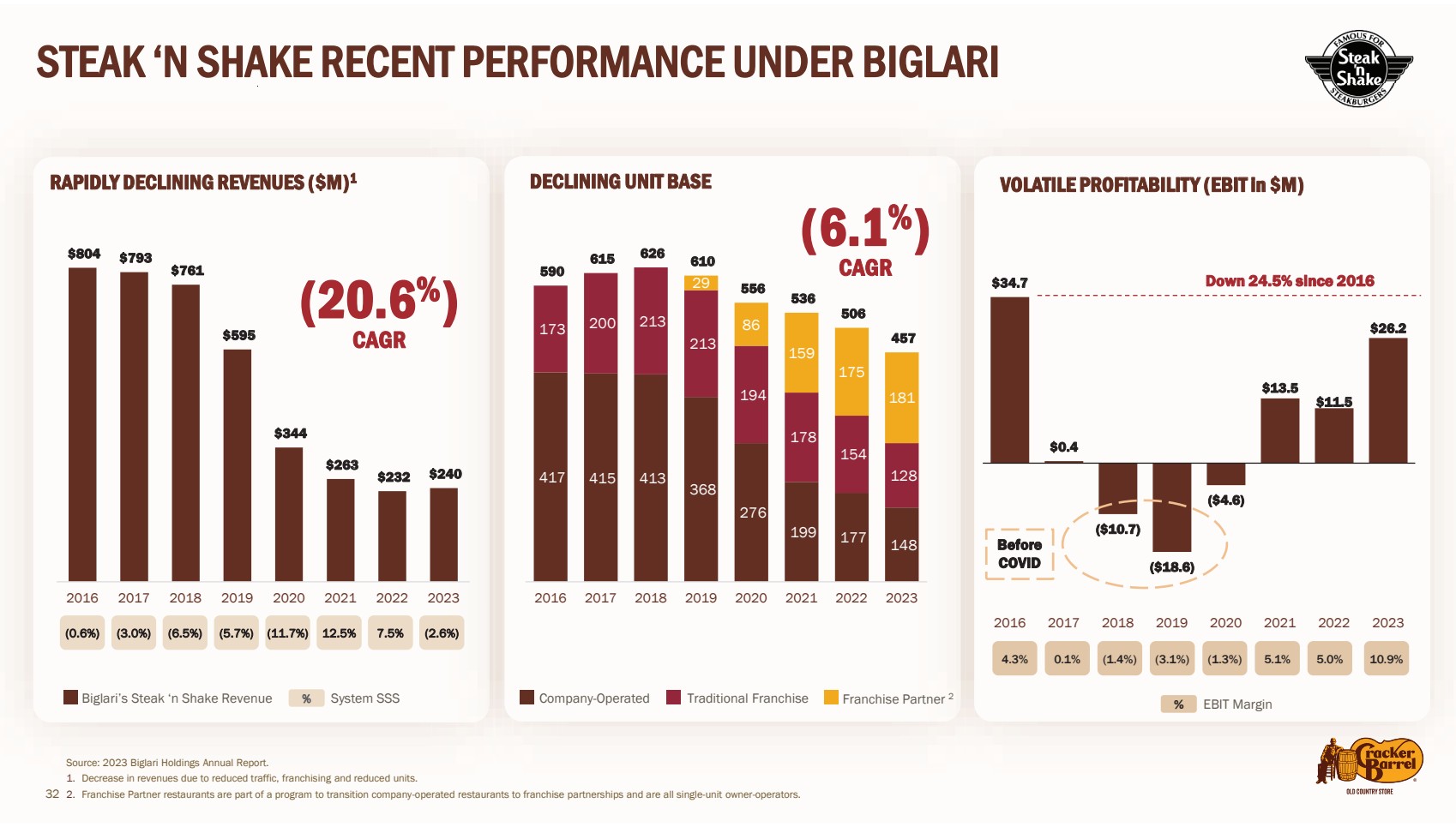

| $804 $793

$761

$595

$344

$263

$232 $240

2016 2017 2018 2019 2020 2021 2022 2023

32

STEAK ‘N SHAKE RECENT PERFORMANCE UNDER BIGLARI

Biglari’s Steak ‘n Shake Revenue % System SSS

(0.6%) (3.0%) (6.5%) (5.7%) (11.7%) 12.5% 7.5% (2.6%)

Traditional Franchise Franchise Partner Company-Operated 2

RAPIDLY DECLINING REVENUES ($M)1 DECLINING UNIT BASE VOLATILE PROFITABILITY (EBIT in $M)

(20.6%)

CAGR

Source: 2023 Biglari Holdings Annual Report.

1. Decrease in revenues due to reduced traffic, franchising and reduced units.

2. Franchise Partner restaurants are part of a program to transition company-operated restaurants to franchise partnerships and are all single-unit owner-operators.

417 415 413

368

276

199 177 148

173 200 213

213

194

178

154

128

29

86

159

175

181

590

615 626 610

556

536

506

457

2016 2017 2018 2019 2020 2021 2022 2023

(6.1%)

CAGR

% EBIT Margin

Down 24.5% since 2016

4.3% 0.1% (1.4%) (3.1%) (1.3%) 5.1% 5.0% 10.9%

$34.7

$0.4

($10.7)

($18.6)

($4.6)

$13.5

$11.5

$26.2

2016 2017 2018 2019 2020 2021 2022 2023

Before

COVID |

| 33

BIGLARI’S STRATEGY COMPROMISED STEAK ‘N SHAKE’S

STANDARDS IN CUSTOMERS’ EYES

“Weakening sales at the burger chain has ushered in an era of massive changes at the company, along with closed restaurants.

The brand operated 612 restaurants five years ago but has closed 129 of them since then... Steak ‘n Shake had come days from

filing for bankruptcy protection in 2021 until Biglari Holdings paid off its debt at the last minute.”

RESTAURANT BUSINESS ONLINE, 2023

34 19 8 (7) (14) (12)

Steak ‘n Shake is the only major burger chain that has declined since 2019 in system

sales and has by far the worst net promoter score

YoY Same-Store Traffic

Due to Biglari’s ineffective strategy, cumulative same-store traffic had fallen by 20%+ in

just four years, even before there was a global pandemic

Source: Biglari Holdings Annual Reports from 2016 to 2019 and Comparably.

TRAFFIC FELL RAPIDLY WELL BEFORE COVID… …AND CLEARLY THE BRAND HAS NOT IMPROVED SINCE

(1.2%)

(4.4%)

(7.0%)

(11.2%)

2016 2017 2018 2019

NET PROMOTER SCORE

(29.6%)

119.5%

38.3% 37.9%

32.7%

26.0%

11.0%

(33)

System Sales Since 2019

(20%+) |

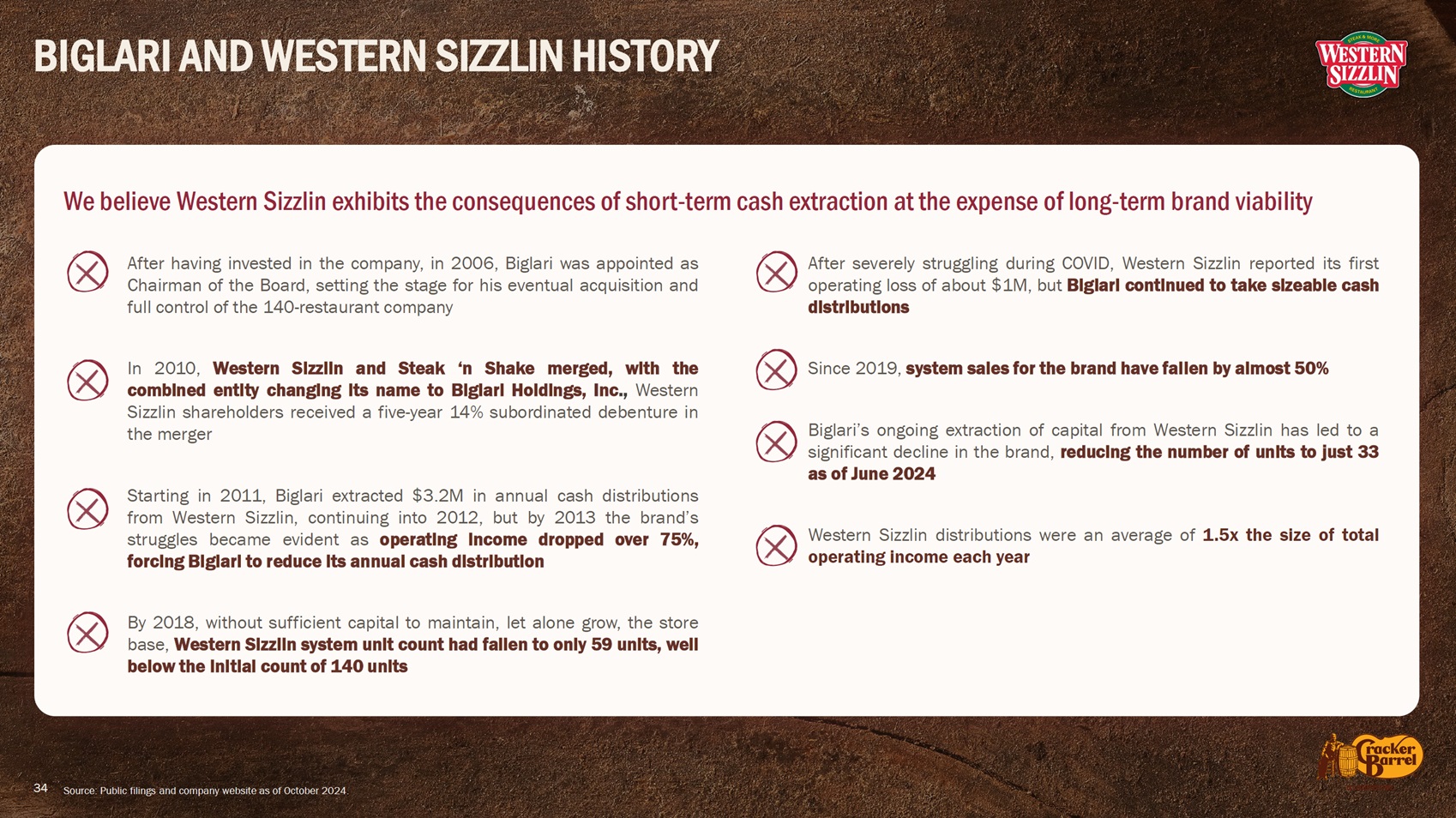

| BIGLARI AND WESTERN SIZZLIN HISTORY

34

After having invested in the company, in 2006, Biglari was appointed as

Chairman of the Board, setting the stage for his eventual acquisition and

full control of the 140-restaurant company

In 2010, Western Sizzlin and Steak ‘n Shake merged, with the

combined entity changing its name to Biglari Holdings, Inc., Western

Sizzlin shareholders received a five-year 14% subordinated debenture in

the merger

Starting in 2011, Biglari extracted $3.2M in annual cash distributions

from Western Sizzlin, continuing into 2012, but by 2013 the brand’s

struggles became evident as operating income dropped over 75%,

forcing Biglari to reduce its annual cash distribution

By 2018, without sufficient capital to maintain, let alone grow, the store

base, Western Sizzlin system unit count had fallen to only 59 units, well

below the initial count of 140 units

After severely struggling during COVID, Western Sizzlin reported its first

operating loss of about $1M, but Biglari continued to take sizeable cash

distributions

Since 2019, system sales for the brand have fallen by almost 50%

Biglari’s ongoing extraction of capital from Western Sizzlin has led to a

significant decline in the brand, reducing the number of units to just 33

as of June 2024

Western Sizzlin distributions were an average of 1.5x the size of total

operating income each year

Source: Public filings and company website as of October 2024.

We believe Western Sizzlin exhibits the consequences of short-term cash extraction at the expense of long-term brand viability |

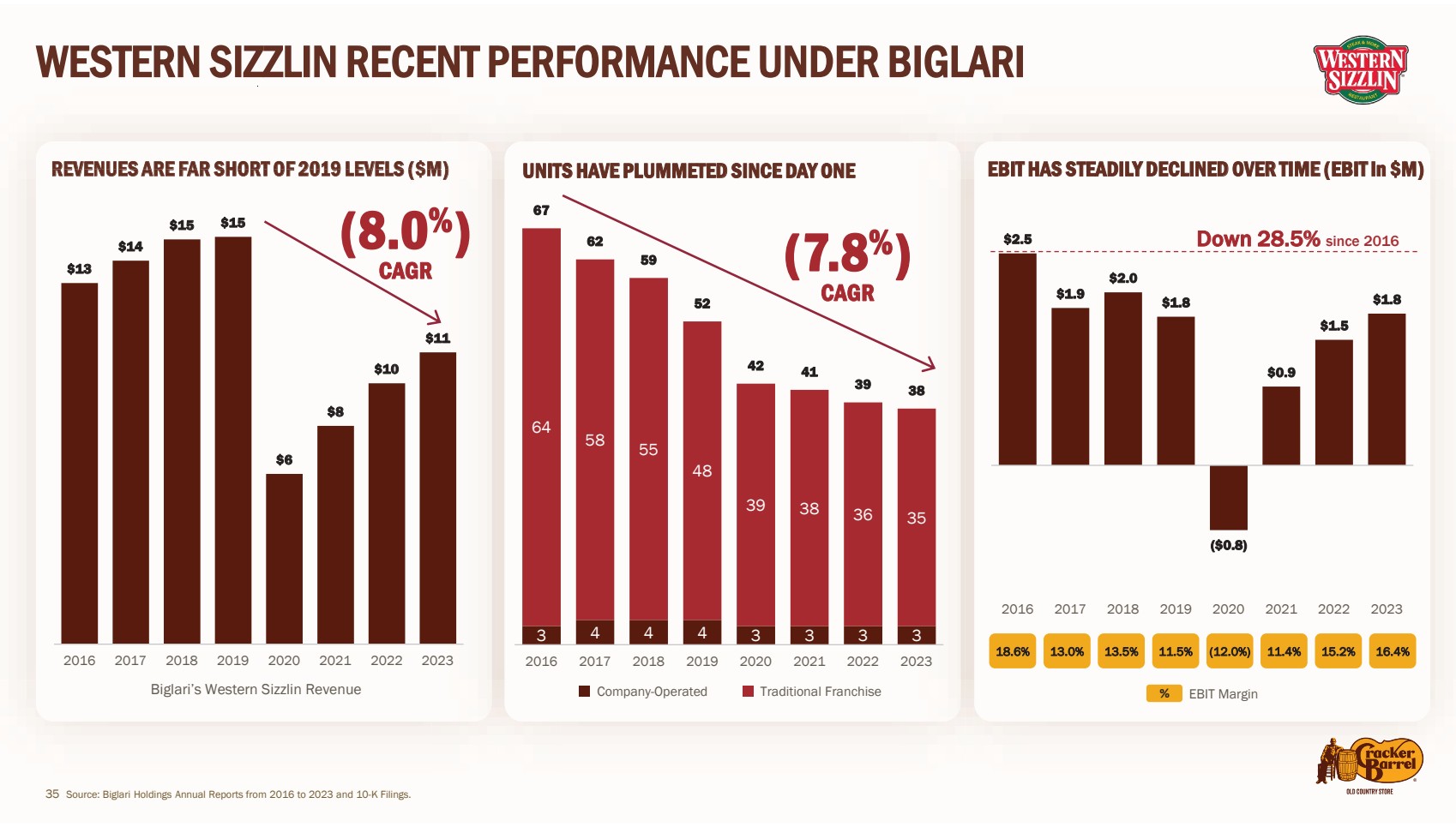

| 35

WESTERN SIZZLIN RECENT PERFORMANCE UNDER BIGLARI

Company-Operated Traditional Franchise

Source: Biglari Holdings Annual Reports from 2016 to 2023 and 10-K Filings.

REVENUES ARE FAR SHORT OF 2019 LEVELS ($M) EBIT HAS STEADILY DECLINED OVER TIME (EBIT in $M)

$13

$14

$15 $15

$6

$8

$10

$11

2016 2017 2018 2019 2020 2021 2022 2023

3 444 3333

64

58 55

48

39 38 36 35

67

62

59

52

42 41

39 38

2016 2017 2018 2019 2020 2021 2022 2023

UNITS HAVE PLUMMETED SINCE DAY ONE

$2.5

$1.9

$2.0

$1.8

($0.8)

$0.9

$1.5

$1.8

2016 2017 2018 2019 2020 2021 2022 2023

Down 28.5% since 2016

18.6% 13.0% 13.5% 11.5% (12.0%) 11.4% 15.2% 16.4%

(8.0%)

CAGR (7.8%)

CAGR

Biglari’s Western Sizzlin Revenue % EBIT Margin |

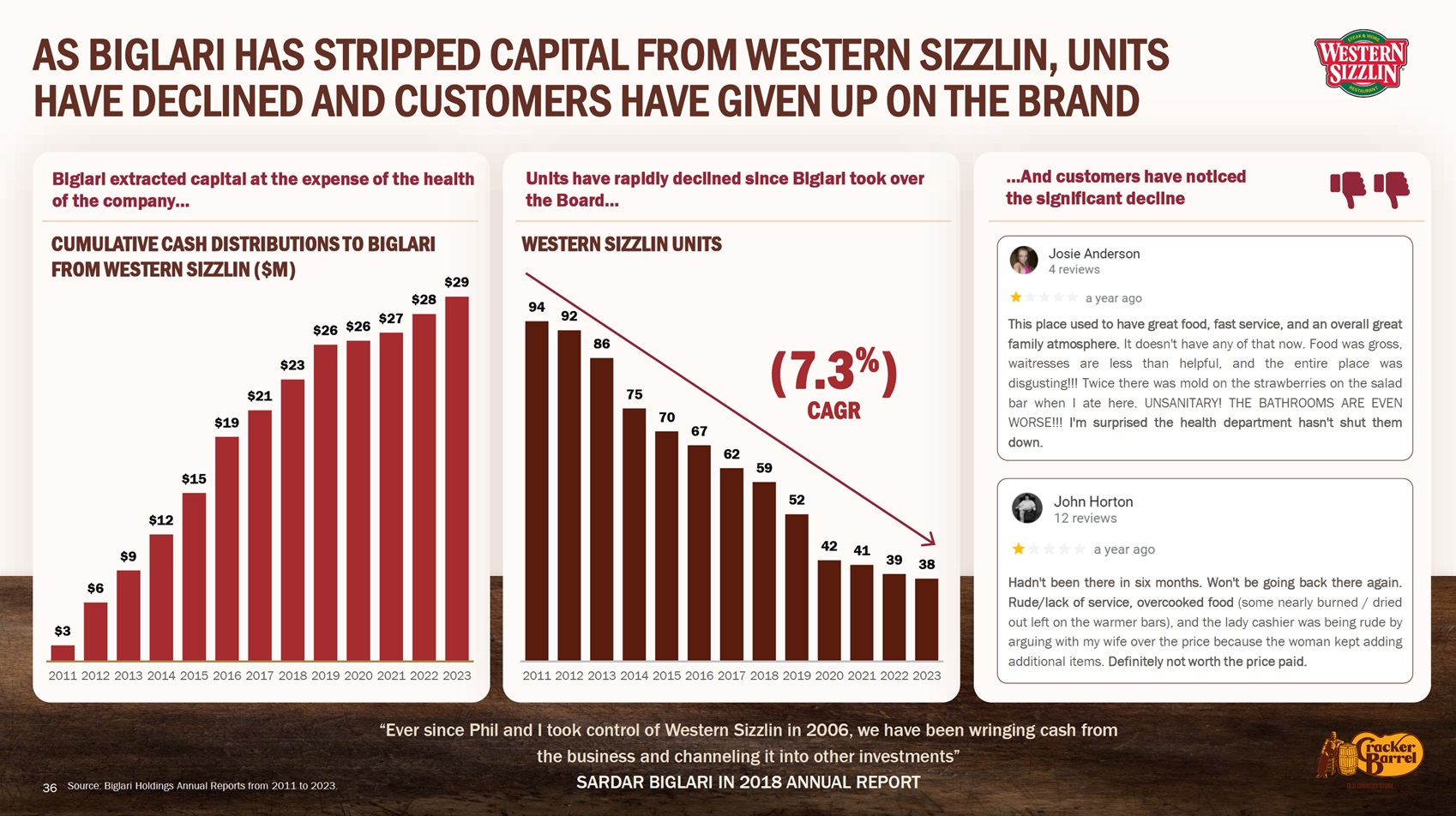

| $3

$6

$9

$12

$15

$19

$21

$23

$26 $26 $27

$28

$29

2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 2022 2023

94 92

86

75

70

67

62

59

52

42 41 39 38

2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 2022 2023

36

AS BIGLARI HAS STRIPPED CAPITAL FROM WESTERN SIZZLIN, UNITS

HAVE DECLINED AND CUSTOMERS HAVE GIVEN UP ON THE BRAND

“Ever since Phil and I took control of Western Sizzlin in 2006, we have been wringing cash from

the business and channeling it into other investments”

SARDAR BIGLARI IN 2018 ANNUAL REPORT

…And customers have noticed

the significant decline

This place used to have great food, fast service, and an overall great

family atmosphere. It doesn't have any of that now. Food was gross,

waitresses are less than helpful, and the entire place was

disgusting!!! Twice there was mold on the strawberries on the salad

bar when I ate here. UNSANITARY! THE BATHROOMS ARE EVEN

WORSE!!! I'm surprised the health department hasn't shut them

down.

Hadn't been there in six months. Won't be going back there again.

Rude/lack of service, overcooked food (some nearly burned / dried

out left on the warmer bars), and the lady cashier was being rude by

arguing with my wife over the price because the woman kept adding

additional items. Definitely not worth the price paid.

Source: Biglari Holdings Annual Reports from 2011 to 2023.

Units have rapidly declined since Biglari took over

the Board…

WESTERN SIZZLIN UNITS

Biglari extracted capital at the expense of the health

of the company…

CUMULATIVE CASH DISTRIBUTIONS TO BIGLARI

FROM WESTERN SIZZLIN ($M)

(7.3%)

CAGR |

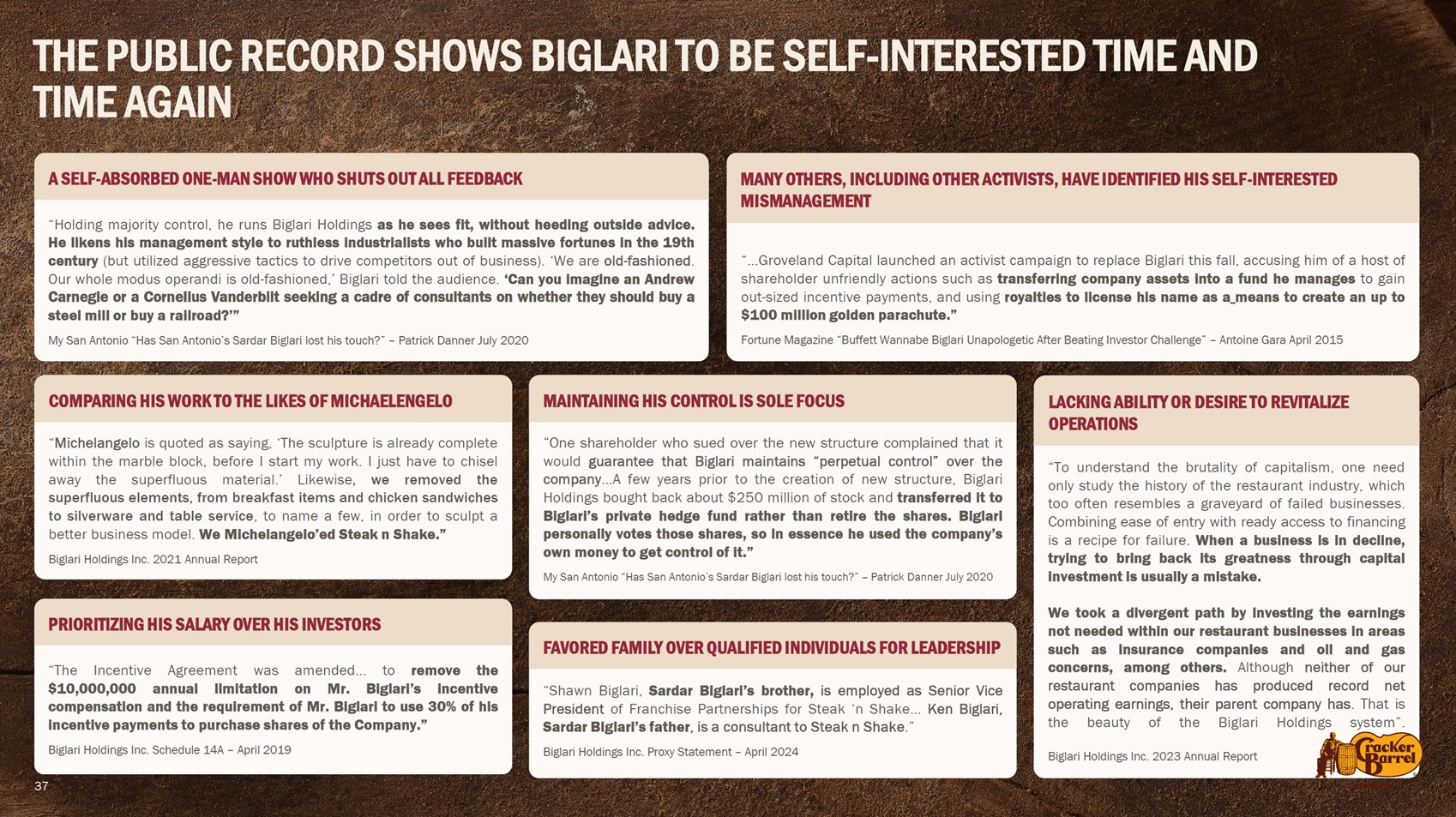

| “Holding majority control, he runs Biglari Holdings as he sees fit, without heeding outside advice.

He likens his management style to ruthless industrialists who built massive fortunes in the 19th

century (but utilized aggressive tactics to drive competitors out of business). ‘We are old-fashioned.

Our whole modus operandi is old-fashioned,’ Biglari told the audience. ‘Can you imagine an Andrew

Carnegie or a Cornelius Vanderbilt seeking a cadre of consultants on whether they should buy a

steel mill or buy a railroad?’”

My San Antonio “Has San Antonio’s Sardar Biglari lost his touch?” – Patrick Danner July 2020

THE PUBLIC RECORD SHOWS BIGLARI TO BE SELF-INTERESTED TIME AND

TIME AGAIN

37

A SELF-ABSORBED ONE-MAN SHOW WHO SHUTS OUT ALL FEEDBACK

“…Groveland Capital launched an activist campaign to replace Biglari this fall, accusing him of a host of

shareholder unfriendly actions such as transferring company assets into a fund he manages to gain

out-sized incentive payments, and using royalties to license his name as a means to create an up to

$100 million golden parachute.”

Fortune Magazine “Buffett Wannabe Biglari Unapologetic After Beating Investor Challenge” – Antoine Gara April 2015

MANY OTHERS, INCLUDING OTHER ACTIVISTS, HAVE IDENTIFIED HIS SELF-INTERESTED

MISMANAGEMENT

“Michelangelo is quoted as saying, ‘The sculpture is already complete

within the marble block, before I start my work. I just have to chisel

away the superfluous material.’ Likewise, we removed the

superfluous elements, from breakfast items and chicken sandwiches

to silverware and table service, to name a few, in order to sculpt a

better business model. We Michelangelo’ed Steak n Shake.”

Biglari Holdings Inc. 2021 Annual Report

COMPARING HIS WORK TO THE LIKES OF MICHAELENGELO

“One shareholder who sued over the new structure complained that it

would guarantee that Biglari maintains “perpetual control” over the

company…A few years prior to the creation of new structure, Biglari

Holdings bought back about $250 million of stock and transferred it to

Biglari’s private hedge fund rather than retire the shares. Biglari

personally votes those shares, so in essence he used the company’s

own money to get control of it.”

My San Antonio “Has San Antonio’s Sardar Biglari lost his touch?” – Patrick Danner July 2020

MAINTAINING HIS CONTROL IS SOLE FOCUS

“Shawn Biglari, Sardar Biglari’s brother, is employed as Senior Vice

President of Franchise Partnerships for Steak ‘n Shake… Ken Biglari,

Sardar Biglari’s father, is a consultant to Steak n Shake.”

Biglari Holdings Inc. Proxy Statement – April 2024

FAVORED FAMILY OVER QUALIFIED INDIVIDUALS FOR LEADERSHIP

“To understand the brutality of capitalism, one need

only study the history of the restaurant industry, which

too often resembles a graveyard of failed businesses.

Combining ease of entry with ready access to financing

is a recipe for failure. When a business is in decline,

trying to bring back its greatness through capital

investment is usually a mistake.

We took a divergent path by investing the earnings

not needed within our restaurant businesses in areas

such as insurance companies and oil and gas

concerns, among others. Although neither of our

restaurant companies has produced record net

operating earnings, their parent company has. That is

the beauty of the Biglari Holdings system”.

Biglari Holdings Inc. 2023 Annual Report

LACKING ABILITY OR DESIRE TO REVITALIZE

OPERATIONS

“The Incentive Agreement was amended… to remove the

$10,000,000 annual limitation on Mr. Biglari’s incentive

compensation and the requirement of Mr. Biglari to use 30% of his

incentive payments to purchase shares of the Company.”

Biglari Holdings Inc. Schedule 14A – April 2019

PRIORITIZING HIS SALARY OVER HIS INVESTORS |

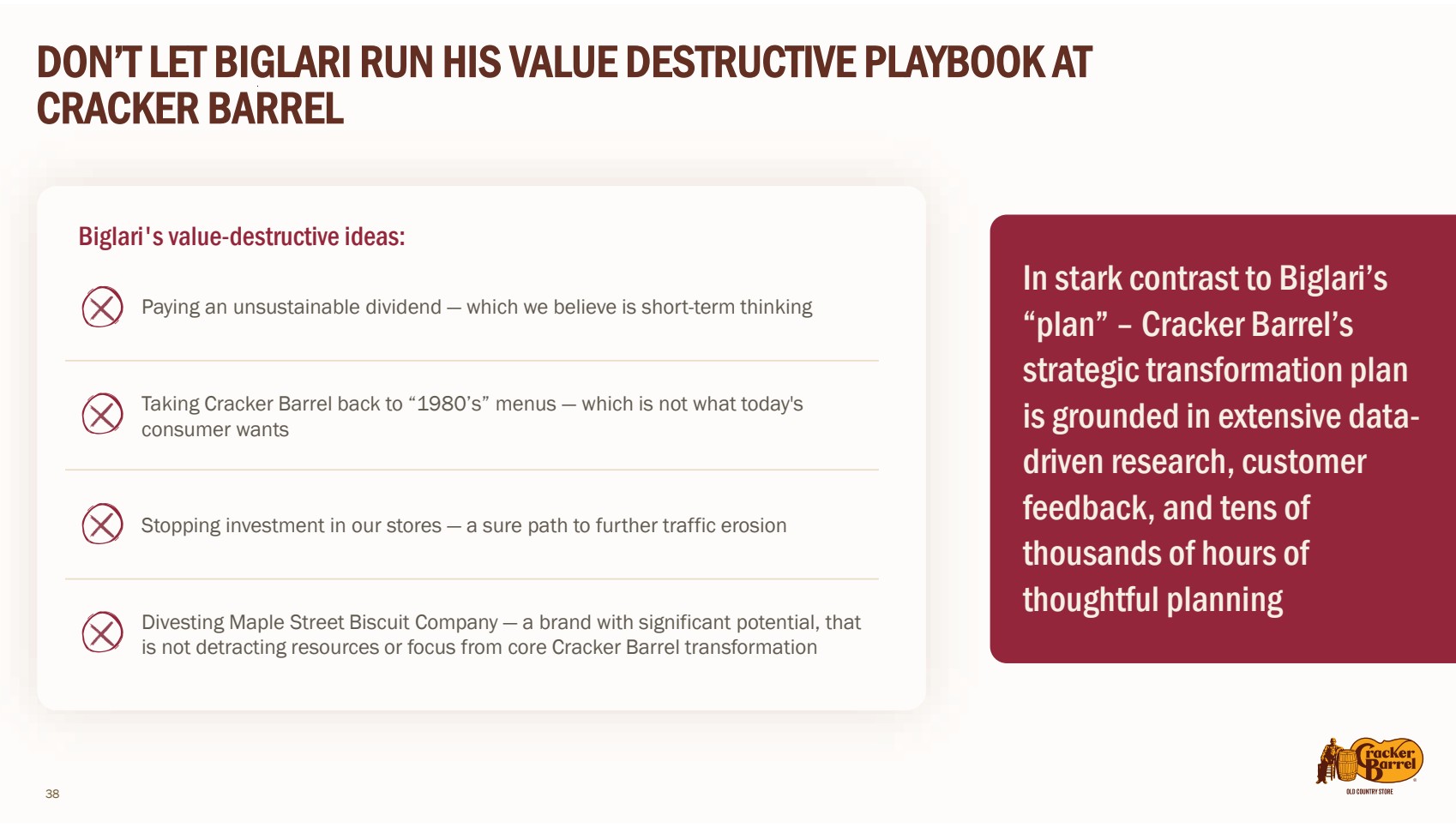

| 38

DON’T LET BIGLARI RUN HIS VALUE DESTRUCTIVE PLAYBOOK AT

CRACKER BARREL

Paying an unsustainable dividend — which we believe is short-term thinking

Taking Cracker Barrel back to “1980’s” menus — which is not what today's

consumer wants

Stopping investment in our stores — a sure path to further traffic erosion

Divesting Maple Street Biscuit Company — a brand with significant potential, that

is not detracting resources or focus from core Cracker Barrel transformation

Biglari's value-destructive ideas:

In stark contrast to Biglari’s

“plan” – Cracker Barrel’s

strategic transformation plan

is grounded in extensive data-driven research, customer

feedback, and tens of

thousands of hours of

thoughtful planning |

| THE RIGHT DIRECTORS

FOR OUR FUTURE

Highly skilled recommended nominees

will ensure Cracker Barrel thrives today,

tomorrow and well into the future

39 |

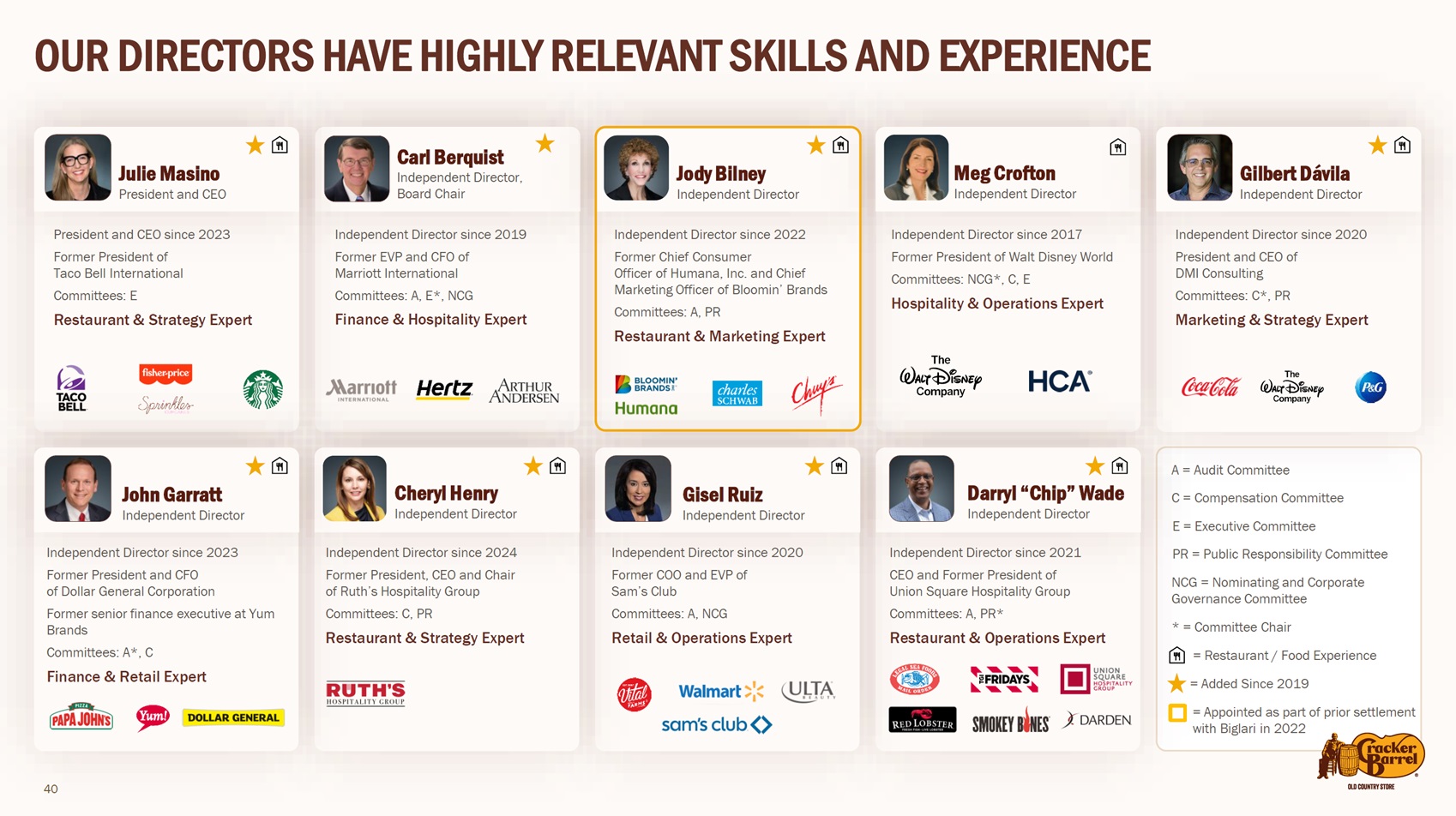

| OUR DIRECTORS HAVE HIGHLY RELEVANT SKILLS AND EXPERIENCE

Julie Masino

President and CEO

Carl Berquist

Independent Director,

Board Chair

President and CEO since 2023

Former President of

Taco Bell International

Committees: E

Restaurant & Strategy Expert

Independent Director since 2019

Former EVP and CFO of

Marriott International

Committees: A, E*, NCG

Finance & Hospitality Expert

Jody Bilney

Independent Director

Independent Director since 2022

Former Chief Consumer

Officer of Humana, Inc. and Chief

Marketing Officer of Bloomin’ Brands

Committees: A, PR

Restaurant & Marketing Expert

Independent Director since 2020

Former COO and EVP of

Sam’s Club

Committees: A, NCG

Retail & Operations Expert

John Garratt

Independent Director

Cheryl Henry

Independent Director

Gisel Ruiz

Independent Director

Darryl “Chip” Wade

Independent Director

Gilbert Dávila

Independent Director

Meg Crofton

Independent Director

Independent Director since 2021

CEO and Former President of

Union Square Hospitality Group

Committees: A, PR*

Restaurant & Operations Expert

Independent Director since 2020

President and CEO of

DMI Consulting

Committees: C*, PR

Marketing & Strategy Expert

Independent Director since 2017

Former President of Walt Disney World

Committees: NCG*, C, E

Hospitality & Operations Expert

Independent Director since 2023

Former President and CFO

of Dollar General Corporation

Former senior finance executive at Yum

Brands

Committees: A*, C

Finance & Retail Expert

Independent Director since 2024

Former President, CEO and Chair

of Ruth’s Hospitality Group

Committees: C, PR

Restaurant & Strategy Expert

A = Audit Committee

E = Executive Committee

NCG = Nominating and Corporate

Governance Committee

C = Compensation Committee

PR = Public Responsibility Committee

* = Committee Chair

= Added Since 2019

= Restaurant / Food Experience

= Appointed as part of prior settlement

with Biglari in 2022

40 |

| 41

BIGLARI IS TARGETING DIRECTORS WHO ARE CRITICAL TO OUR STABILITY

AND TRANSFORMATION

Both Mr. Berquist

and Ms. Crofton

actively contributed

to the development

of our strategic

transformation

plan and provide

key oversight and

stability for our

new CEO

Former EVP and CFO of Marriott

International

Committees: A, E*, NCG

Finance & Hospitality Expert

Carl Berquist

Independent Director,

Board Chair

Former President of Walt Disney World

Committees: NCG*, C, E

Hospitality & Operations Expert

Meg Crofton

Independent Director

A = Audit Committee E = Executive Committee NCG = C = Compensation Committee Nominating and Corporate Governance Committee * = Committee Chair

9 Independent Cracker Barrel director since 2019, elected Chairman last year

9 Brings 40 years of financial experience, with deep knowledge of hospitality industry

9 Capital allocation expert with deep financial, real estate, corporate transactions, and public company

board experience

9 Served as Executive Vice President and CFO of Marriott, overseeing the finance organization of a

complex, global Fortune 500 hospitality company

9 Previously was the Global Real Estate and Hospitality Industry Head of Arthur Andersen, and Managing

Partner of the mid-Atlantic region for Arthur Andersen during his career

9 Former director of Hertz Global Holdings, Inc. and Beacon Roofing Supply, Inc.

9 Independent Cracker Barrel director since 2017, and currently serves as Chair of the Nominating and

Corporate Governance Committee

9 Has overseen consistent and thoughtful refreshment of the Board, ensuring the right balance of

knowledge, perspectives, and industry experience

9 Spent 35 years in executive leadership roles in operating areas at The Walt Disney Company, with

accountability for over 100,000 employees in parks across the U.S. and France

9 Brings valuable leadership, industry, and public company board experience

9 Oversaw foodservice and retail operations, employee performance, and guest satisfaction at Disney

parks and resorts, with significant experience overseeing initiatives focused on driving strategic change

9 Former director at Tupperware Brands Corporation and current director at HCA Healthcare, Inc. |

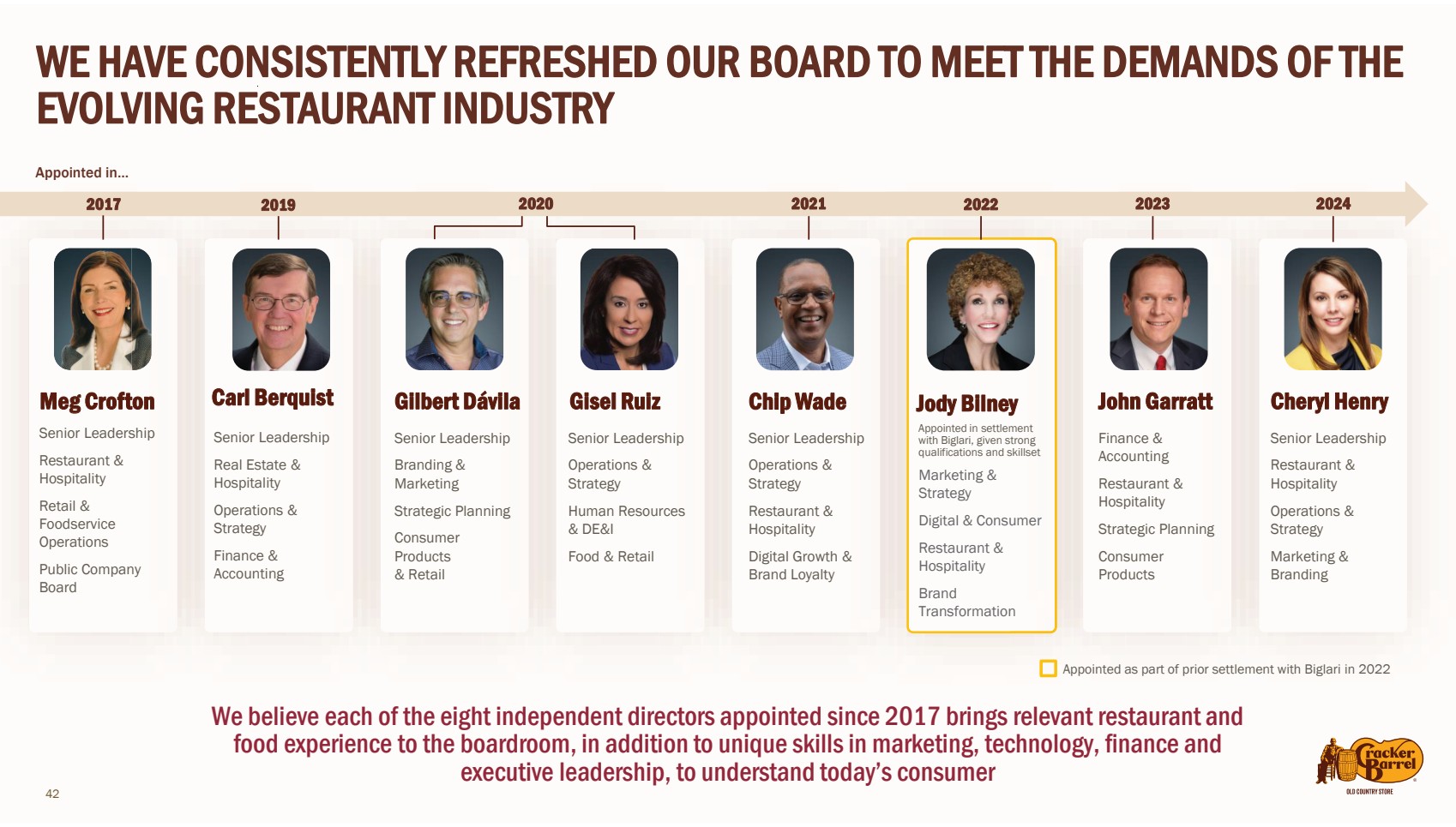

| 42

WE HAVE CONSISTENTLY REFRESHED OUR BOARD TO MEET THE DEMANDS OF THE

EVOLVING RESTAURANT INDUSTRY

Jody Bilney

Appointed in settlement

with Biglari, given strong

qualifications and skillset

Marketing &

Strategy

Digital & Consumer

Restaurant &

Hospitality

Brand

Transformation

Appointed as part of prior settlement with Biglari in 2022

Gilbert Dávila

Senior Leadership

Branding &

Marketing

Strategic Planning

Consumer

Products

& Retail

Gisel Ruiz

Senior Leadership

Operations &

Strategy

Human Resources

& DE&I

Food & Retail

Chip Wade

Senior Leadership

Operations &

Strategy

Restaurant &

Hospitality

Digital Growth &

Brand Loyalty

John Garratt

Finance &

Accounting

Restaurant &

Hospitality

Strategic Planning

Consumer

Products

Carl Berquist

Senior Leadership

Real Estate &

Hospitality

Operations &

Strategy

Finance &

Accounting

Cheryl Henry

Senior Leadership

Restaurant &

Hospitality

Operations &

Strategy

Marketing &

Branding

2019 2020 2021 2022 2023 2024

Appointed in…

We believe each of the eight independent directors appointed since 2017 brings relevant restaurant and

food experience to the boardroom, in addition to unique skills in marketing, technology, finance and

executive leadership, to understand today’s consumer

Meg Crofton

Senior Leadership

Restaurant &

Hospitality

Retail &

Foodservice

Operations

Public Company

Board

2017 |

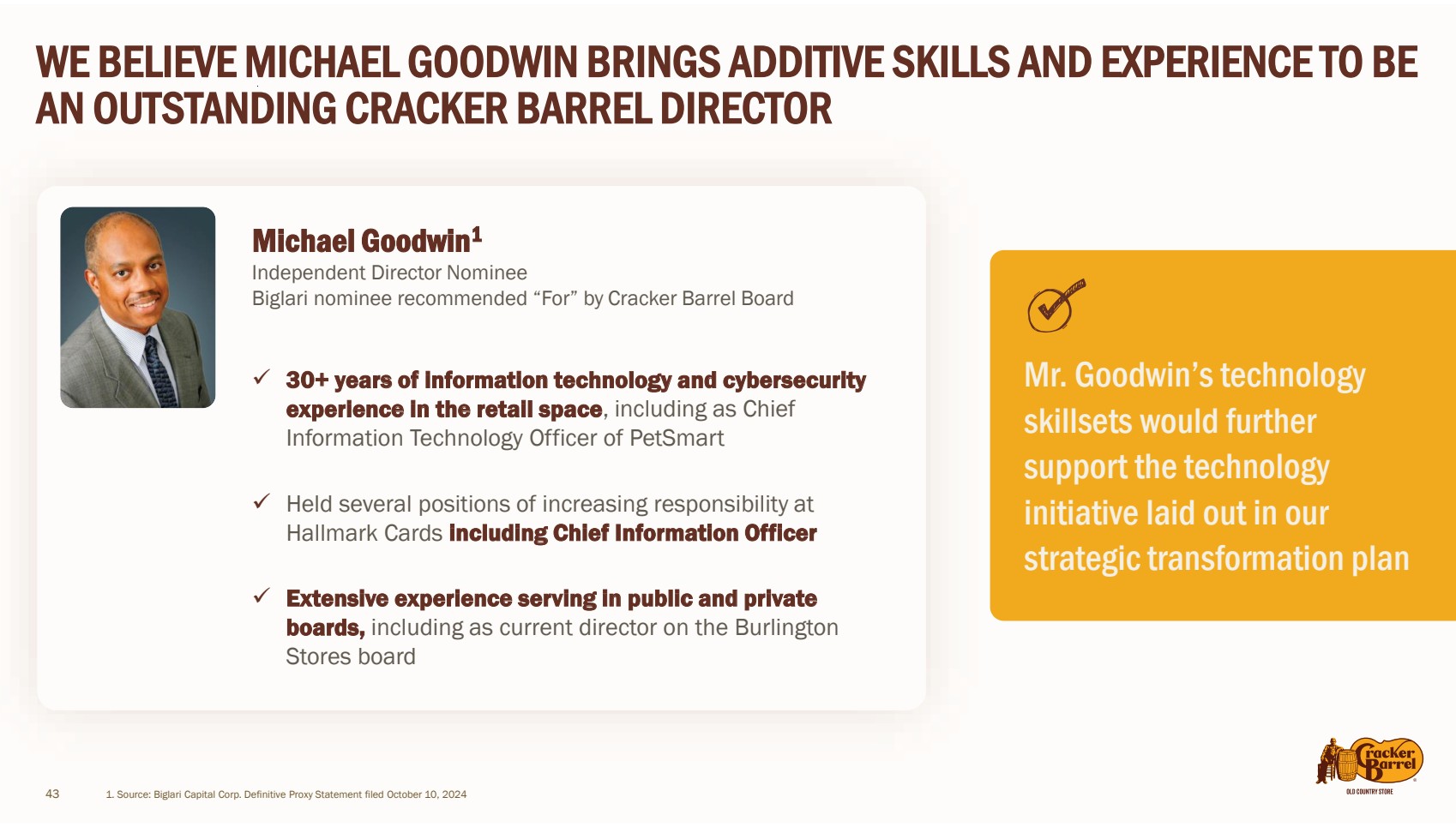

| Mr. Goodwin’s technology

skillsets would further

support the technology

initiative laid out in our

strategic transformation plan

WE BELIEVE MICHAEL GOODWIN BRINGS ADDITIVE SKILLS AND EXPERIENCE TO BE

AN OUTSTANDING CRACKER BARREL DIRECTOR

Michael Goodwin1

Independent Director Nominee

Biglari nominee recommended “For” by Cracker Barrel Board

9 30+ years of information technology and cybersecurity

experience in the retail space, including as Chief

Information Technology Officer of PetSmart

9 Held several positions of increasing responsibility at

Hallmark Cards including Chief Information Officer

9 Extensive experience serving in public and private

boards, including as current director on the Burlington

Stores board

43 1. Source: Biglari Capital Corp. Definitive Proxy Statement filed October 10, 2024 |

| PROTECT OUR STRATEGIC

TRANSFORMATION PLAN

We are taking urgent action focused

on enhancing shareholder value

44 |

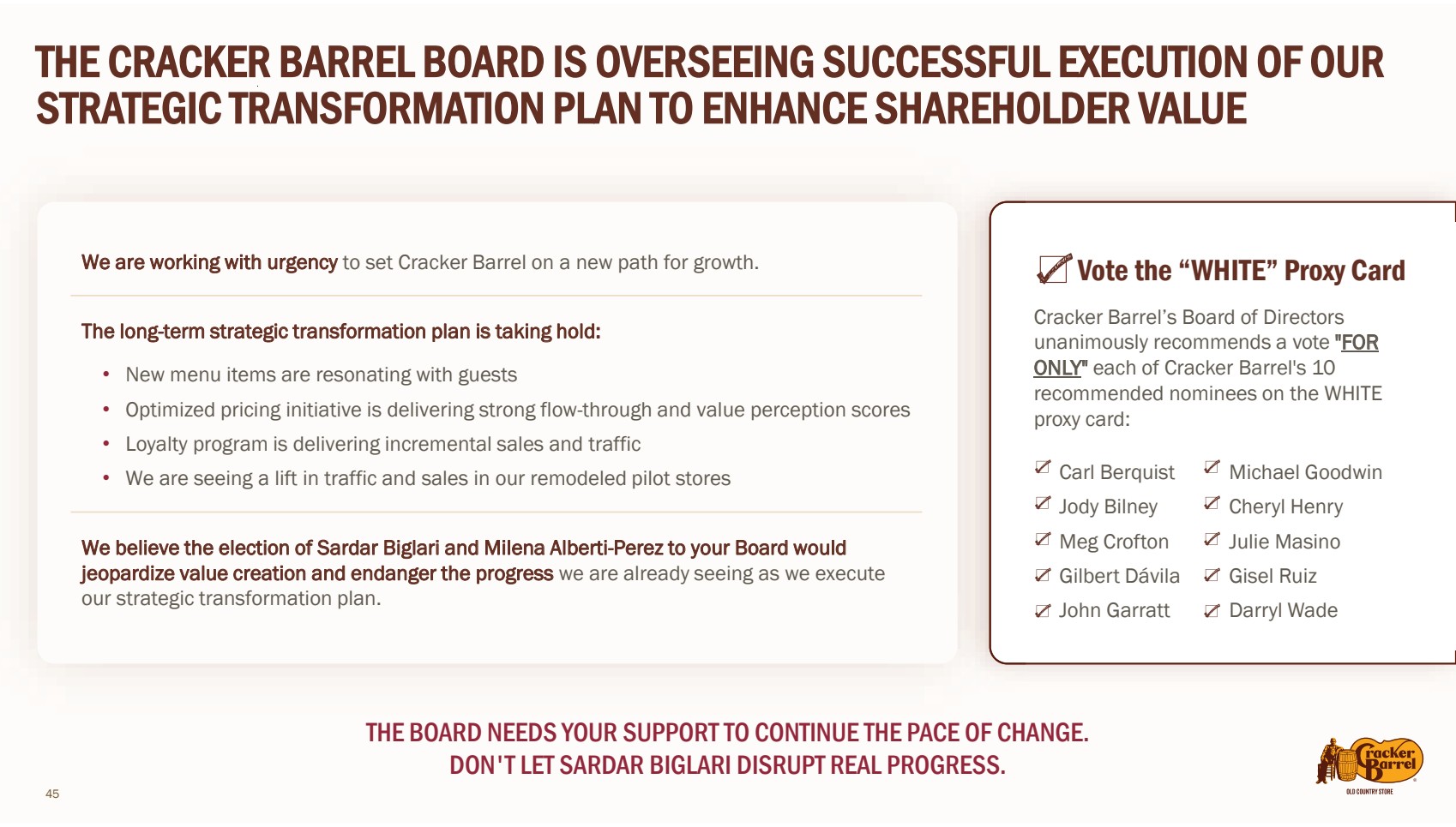

| 45

THE CRACKER BARREL BOARD IS OVERSEEING SUCCESSFUL EXECUTION OF OUR

STRATEGIC TRANSFORMATION PLAN TO ENHANCE SHAREHOLDER VALUE

Vote the “WHITE” Proxy Card

Cracker Barrel’s Board of Directors

unanimously recommends a vote "FOR

ONLY" each of Cracker Barrel's 10

recommended nominees on the WHITE

proxy card:

Carl Berquist

Jody Bilney

Meg Crofton

Gilbert Dávila

John Garratt

We are working with urgency to set Cracker Barrel on a new path for growth.

The long-term strategic transformation plan is taking hold:

• New menu items are resonating with guests

• Optimized pricing initiative is delivering strong flow-through and value perception scores

• Loyalty program is delivering incremental sales and traffic

• We are seeing a lift in traffic and sales in our remodeled pilot stores

We believe the election of Sardar Biglari and Milena Alberti-Perez to your Board would

jeopardize value creation and endanger the progress we are already seeing as we execute

our strategic transformation plan.

Michael Goodwin

Cheryl Henry

Julie Masino

Gisel Ruiz

Darryl Wade

THE BOARD NEEDS YOUR SUPPORT TO CONTINUE THE PACE OF CHANGE.

DON'T LET SARDAR BIGLARI DISRUPT REAL PROGRESS. |

| APPENDIX

46 |

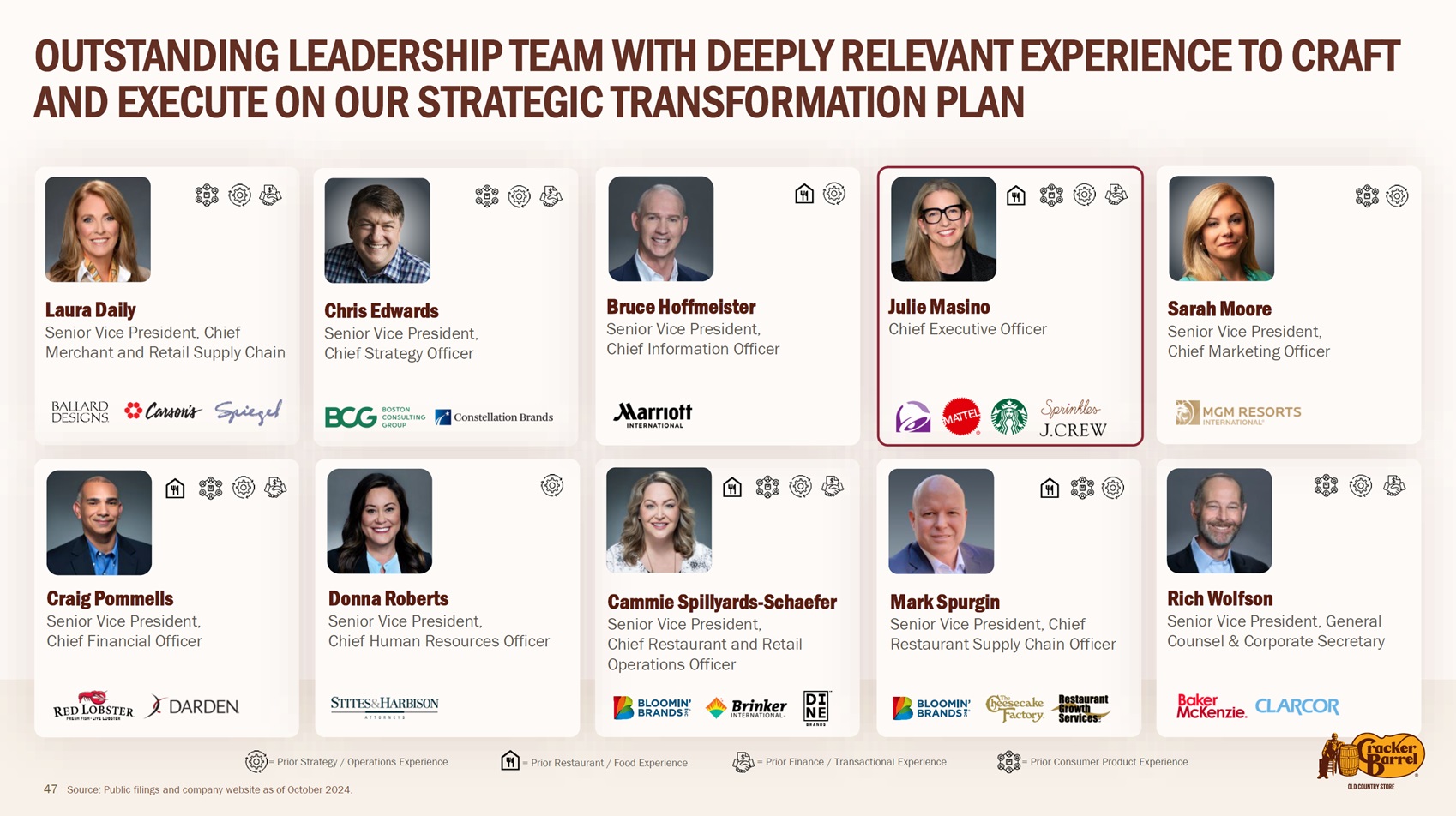

| Laura Daily

Senior Vice President, Chief

Merchant and Retail Supply Chain

OUTSTANDING LEADERSHIP TEAM WITH DEEPLY RELEVANT EXPERIENCE TO CRAFT

AND EXECUTE ON OUR STRATEGIC TRANSFORMATION PLAN

47

= Prior Strategy / Operations Experience = Prior Finance / Transactional Experience = Prior Restaurant / Food Experience = Prior Consumer Product Experience

Source: Public filings and company website as of October 2024.

Julie Masino

Chief Executive Officer f

y Chain

Chris Edwards

Senior Vice President,

Chief Strategy Officer

47 Source: Public filings and company web

Craig Pommells

Senior Vice President,

Chief Financial Officer

xperience = Prior Fina

Cammie Spillyards-Schaefer

Senior Vice President,

Chief Restaurant and Retail

Operations Officer

= Prior Strategy / Operations Experience

bsite as of October 2024.

= Prior Restaurant / Food Ex

Camm

Senio

Chief

Opera

Donna Roberts

Senior Vice President,

Chief Human Resources Officer

ance / Transactional Experience = Prior Consum

efer Mark Spurgin

Senior Vice President, Chief

Restaurant Supply Chain Officer

mer Product Experience

f

fficer

Rich Wolfson

Senior Vice President, General

Counsel & Corporate Secretary

Julie

Chief

Bruce Hoffmeister

Senior Vice President,

Chief Information Officer

Sarah Moore

Senior Vice President,

Chief Marketing Officer |

| OUR EXCITING NEW

REMODELS – A

FRESH LOOK WITH

THE SAME CRACKER

BARREL FEEL

48 |

| 49

WE MAINTAIN CORPORATE GOVERNANCE PRACTICES THAT PRIORITIZE

SHAREHOLDER ALIGNMENT AND ACCOUNTABILITY

Policy against hedging

and pledging of securities

Annually elected

directors

Compensation aligned

with performance

Shareholders can call

special meetings

All directors except CEO

are independent

Fully independent Board

committees

0-6 Years

7-10

Years

11+

Years

70s

60s

50s

TENURE

AGE

SEPARATE

CEO and Independent Chair Roles

9 of 10

Independent Directors

7

Independent Directors Joined Since the Beginning

of 2019

70%

Female or Ethnically/Racially Diverse

CORPORATE GOVERNANCE BEST PRACTICES BALANCED TENURE A REFRESHED BOARD LED BY AN

INDEPENDENT CHAIR |

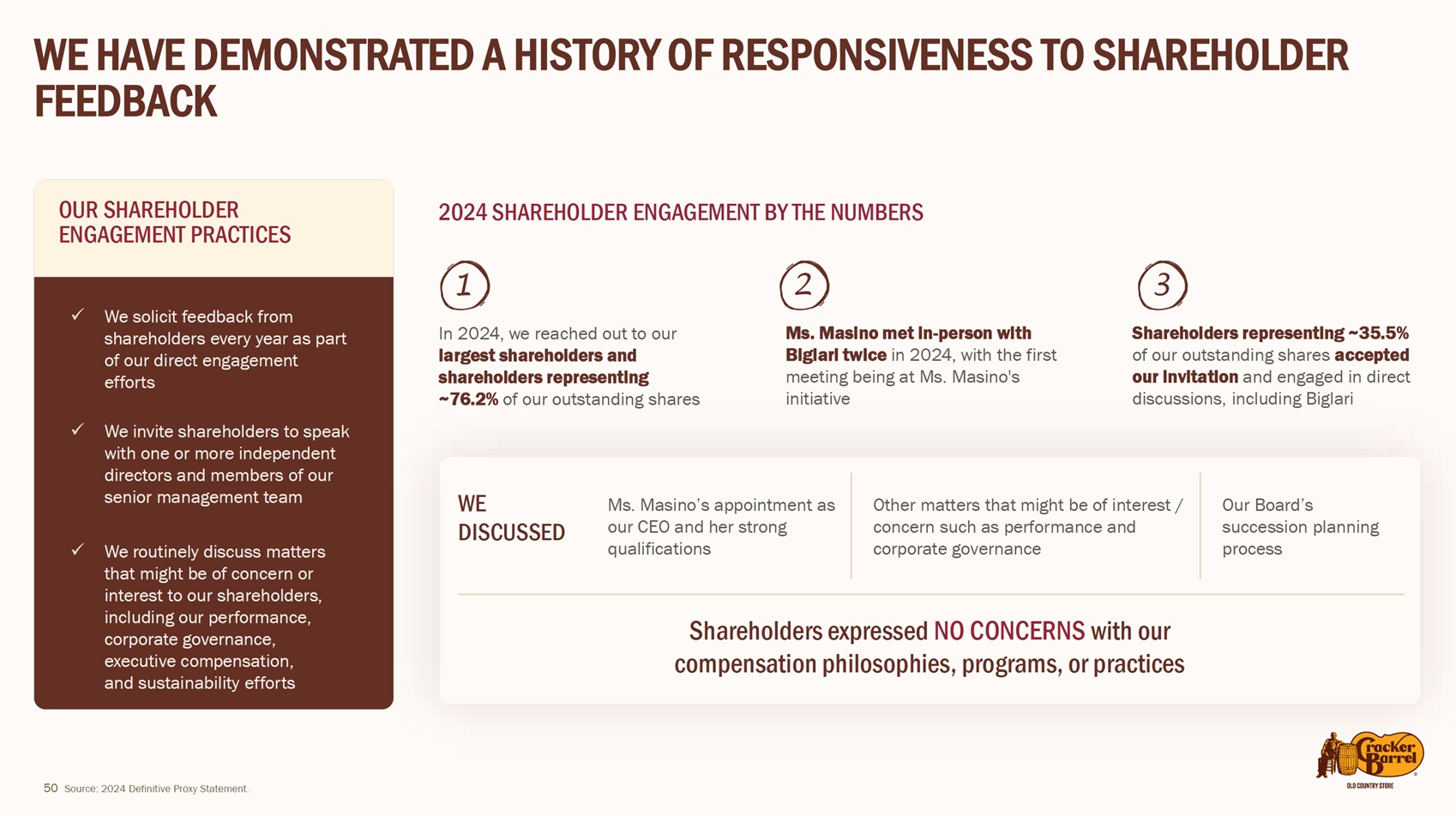

| 50

WE HAVE DEMONSTRATED A HISTORY OF RESPONSIVENESS TO SHAREHOLDER

FEEDBACK

In 2024, we reached out to our

largest shareholders and

shareholders representing

~76.2% of our outstanding shares

Ms. Masino met in-person with

Biglari twice in 2024, with the first

meeting being at Ms. Masino's

initiative

Source: 2024 Definitive Proxy Statement.

OUR SHAREHOLDER

ENGAGEMENT PRACTICES

2024 SHAREHOLDER ENGAGEMENT BY THE NUMBERS

9 We solicit feedback from

shareholders every year as part

of our direct engagement

efforts

9 We invite shareholders to speak

with one or more independent

directors and members of our

senior management team

9 We routinely discuss matters

that might be of concern or

interest to our shareholders,

including our performance,

corporate governance,

executive compensation,

and sustainability efforts

1

Shareholders representing ~35.5%

of our outstanding shares accepted

our invitation and engaged in direct

discussions, including Biglari

WE

DISCUSSED

Ms. Masino’s appointment as

our CEO and her strong

qualifications

Other matters that might be of interest /

concern such as performance and

corporate governance

Our Board’s

succession planning

process

Shareholders expressed NO CONCERNS with our

compensation philosophies, programs, or practices

2 3 |

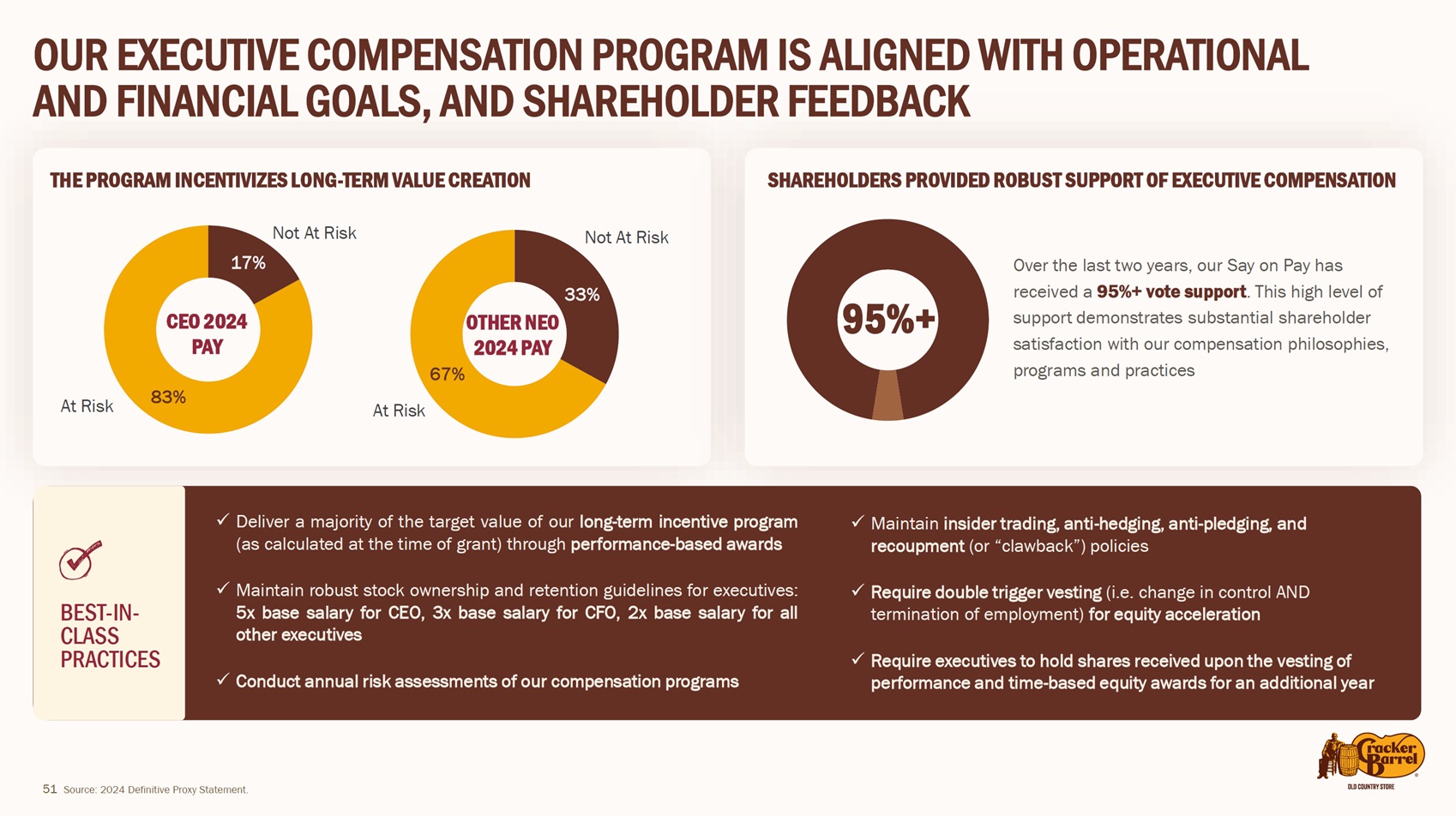

| 51

OUR EXECUTIVE COMPENSATION PROGRAM IS ALIGNED WITH OPERATIONAL

AND FINANCIAL GOALS, AND SHAREHOLDER FEEDBACK

CEO 2024

PAY

OTHER NEO

2024 PAY

Over the last two years, our Say on Pay has

received a 95%+ vote support. This high level of

support demonstrates substantial shareholder

satisfaction with our compensation philosophies,

programs and practices

9 Deliver a majority of the target value of our long-term incentive program

(as calculated at the time of grant) through performance-based awards

9 Maintain robust stock ownership and retention guidelines for executives:

5x base salary for CEO, 3x base salary for CFO, 2x base salary for all

other executives

9 Conduct annual risk assessments of our compensation programs

9 Maintain insider trading, anti-hedging, anti-pledging, and

recoupment (or “clawback”) policies

9 Require double trigger vesting (i.e. change in control AND

termination of employment) for equity acceleration

9 Require executives to hold shares received upon the vesting of

performance and time-based equity awards for an additional year

17%

83%

THE PROGRAM INCENTIVIZES LONG-TERM VALUE CREATION SHAREHOLDERS PROVIDED ROBUST SUPPORT OF EXECUTIVE COMPENSATION

BEST-IN-CLASS

PRACTICES

Source: 2024 Definitive Proxy Statement.

Not At Risk

At Risk

33%

67%

Not At Risk

At Risk

95%+ |

| NON-GAAP

RECONCILIATIONS

52 |

| EBITDA / ADJUSTED EBITDA

53

In the accompanying presentation and the below reconciliation tables, the Company makes reference to EBITDA

and adjusted EBITDA, as well as the 53rd week impact of these items. The Company defines EBITDA as net income,

calculated in accordance with GAAP, excluding depreciation and amortization, interest expense and tax expense.

The Company further adjusts EBITDA to exclude, to the extent the following items occurred during the periods

presented: (i) expenses related to share-based compensation, (ii) impairment charges and store closing costs, (iii)

the proxy contest and settlement in connection with the Company’s 2022 annual meeting of shareholders, (iv)

goodwill impairment charges, (v) the Company’s CEO transition, (vi) expenses associated with the Company’s

strategic transformation initiative, (vii) a corporate restructuring charge, and (viii) an employee benefits policy

change. The Company calculates EBITDA and adjusted EBITDA margin by dividing EBITDA and adjusted EBITDA by

consolidated GAAP revenue. The Company believes that presentation of EBITDA and adjusted EBITDA (together

with related margin figures) and presenting the 53rd week impact of these items provides investors with an

enhanced understanding of the Company's operating performance and debt leverage metrics and enhances

comparability with the Company’s historical results, and that the presentation of this non-GAAP financial measure,

when combined with the primary presentation of net income, is beneficial to an investor’s complete understanding

of the Company’s operating performance. This information is not intended to be considered in isolation or as a

substitute for net income or net income margin prepared in accordance with GAAP. |

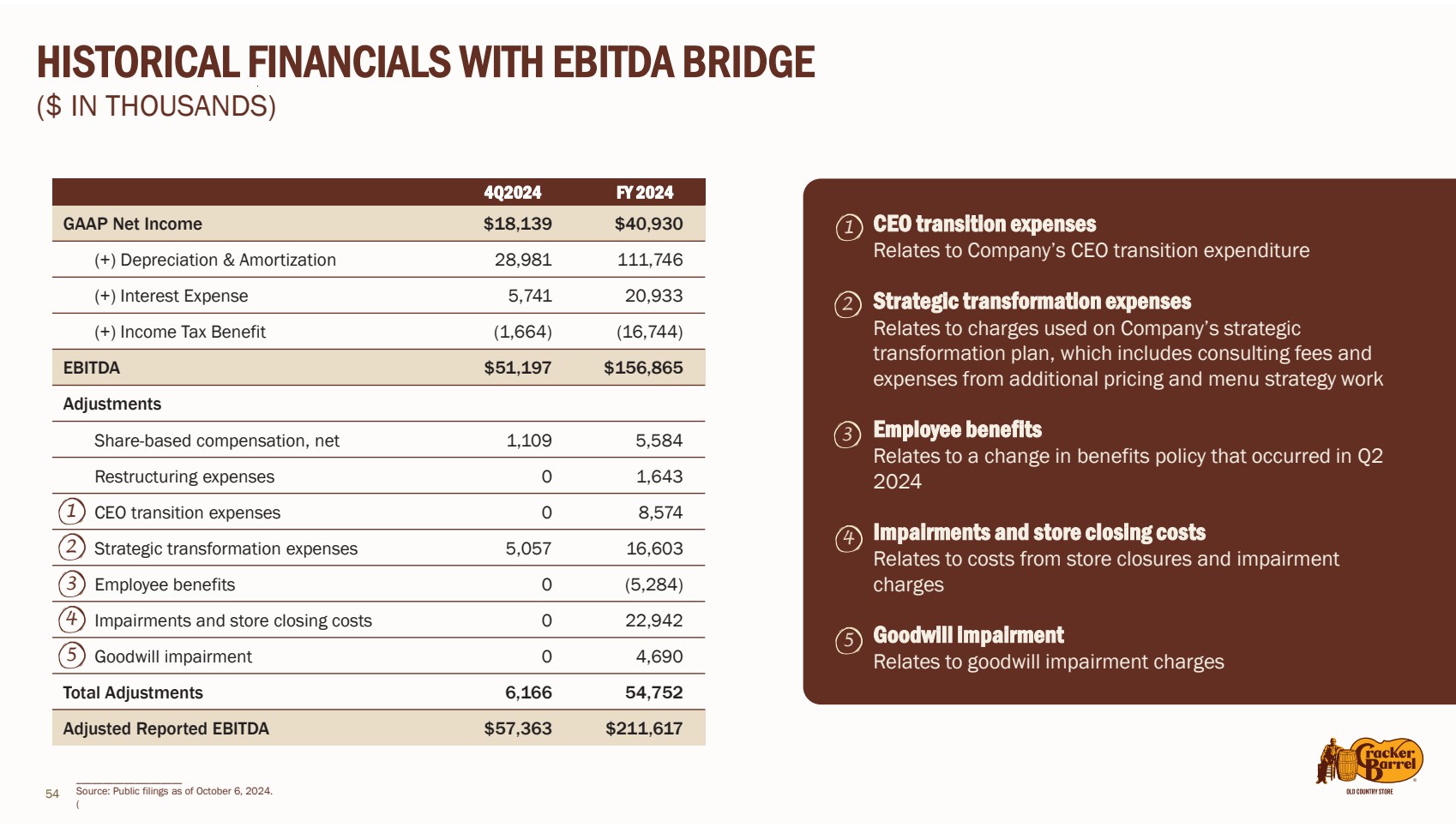

| HISTORICAL FINANCIALS WITH EBITDA BRIDGE

____________________

Source: Public filings as of October 6, 2024.

(

CEO transition expenses

Relates to Company’s CEO transition expenditure

Strategic transformation expenses

Relates to charges used on Company’s strategic

transformation plan, which includes consulting fees and

expenses from additional pricing and menu strategy work

Employee benefits

Relates to a change in benefits policy that occurred in Q2

2024

Impairments and store closing costs

Relates to costs from store closures and impairment

charges

Goodwill impairment

Relates to goodwill impairment charges

1

2

3

4

5

4Q2024 FY 2024

GAAP Net Income $18,139 $40,930

(+) Depreciation & Amortization 28,981 111,746

(+) Interest Expense 5,741 20,933

(+) Income Tax Benefit (1,664) (16,744)

EBITDA $51,197 $156,865

Adjustments

Share-based compensation, net 1,109 5,584

Restructuring expenses 0 1,643

CEO transition expenses 0 8,574

Strategic transformation expenses 5,057 16,603

Employee benefits 0 (5,284)

Impairments and store closing costs 0 22,942

Goodwill impairment 0 4,690

Total Adjustments 6,166 54,752

Adjusted Reported EBITDA $57,363 $211,617

($ IN THOUSANDS)

1

2

3

4

5

54 |

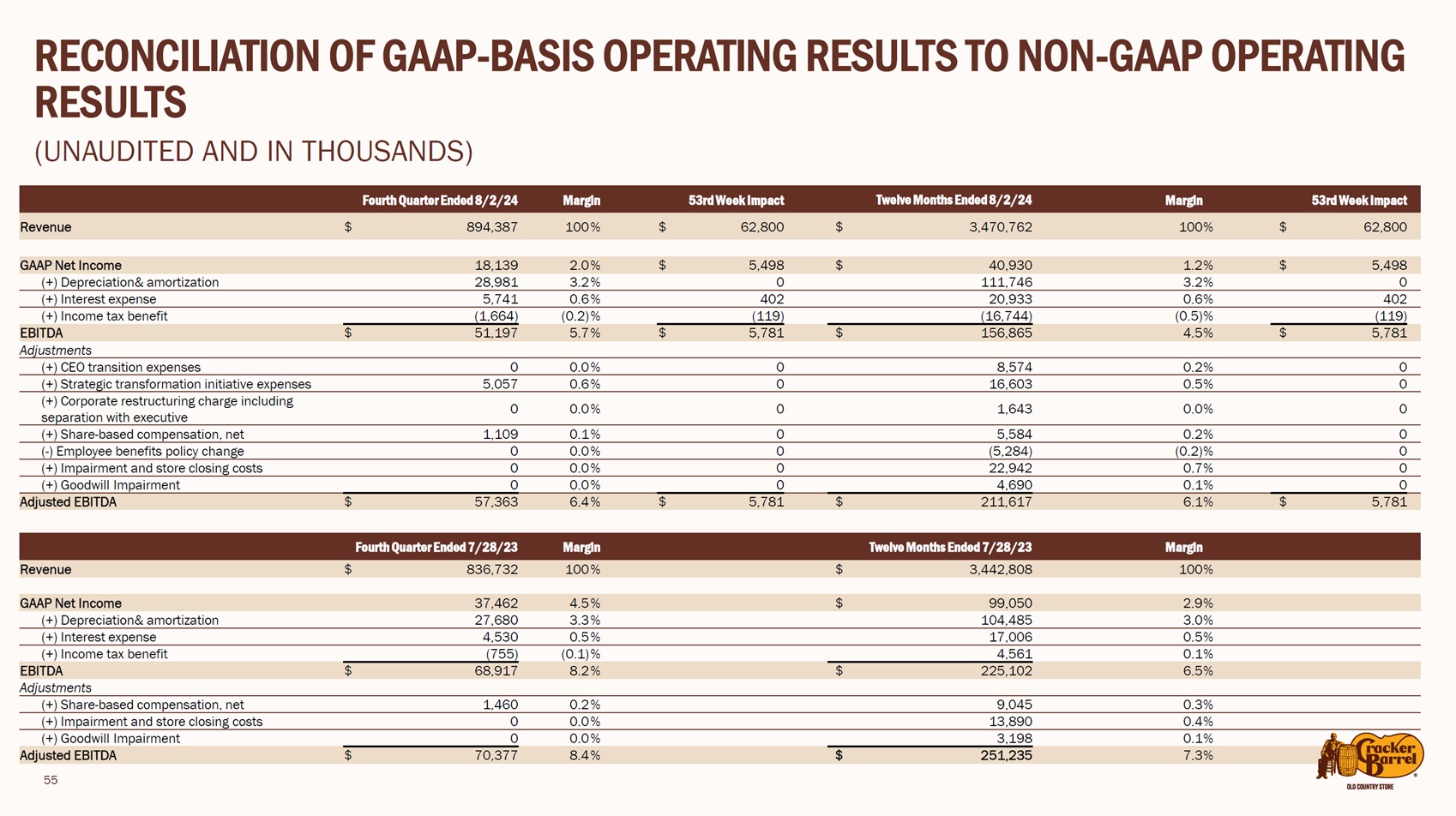

| 55

RECONCILIATION OF GAAP-BASIS OPERATING RESULTS TO NON-GAAP OPERATING

RESULTS

(UNAUDITED AND IN THOUSANDS)

Fourth Quarter Ended 8/2/24 Margin 53rd Week Impact Twelve Months Ended 8/2/24 Margin 53rd Week Impact

Revenue $ 894,387 100% $ 62,800 $ 3,470,762 100% $ 62,800

GAAP Net Income 18,139 2.0% $ 5,498 $ 40,930 1.2% $ 5,498

(+) Depreciation& amortization 28,981 3.2% 0 111,746 3.2% 0

(+) Interest expense 5,741 0.6% 402 20,933 0.6% 402

(+) Income tax benefit (1,664) (0.2)% (119) (16,744) (0.5)% (119)

EBITDA $ 51,197 5.7% $ 5,781 $ 156,865 4.5% $ 5,781

Adjustments

(+) CEO transition expenses 0 0.0% 0 8,574 0.2% 0

(+) Strategic transformation initiative expenses 5,057 0.6% 0 16,603 0.5% 0

(+) Corporate restructuring charge including

separation with executive 0 0.0% 0 1,643 0.0% 0

(+) Share-based compensation, net 1,109 0.1% 0 5,584 0.2% 0

(-) Employee benefits policy change 0 0.0% 0 (5,284) (0.2)% 0

(+) Impairment and store closing costs 0 0.0% 0 22,942 0.7% 0

(+) Goodwill Impairment 0 0.0% 0 4,690 0.1% 0

Adjusted EBITDA $ 57,363 6.4% $ 5,781 $ 211,617 6.1% $ 5,781

Fourth Quarter Ended 7/28/23 Margin Twelve Months Ended 7/28/23 Margin

Revenue $ 836,732 100% $ 3,442,808 100%

GAAP Net Income 37,462 4.5% $ 99,050 2.9%

(+) Depreciation& amortization 27,680 3.3% 104,485 3.0%

(+) Interest expense 4,530 0.5% 17,006 0.5%

(+) Income tax benefit (755) (0.1)% 4,561 0.1%

EBITDA $ 68,917 8.2% $ 225,102 6.5%

Adjustments

(+) Share-based compensation, net 1,460 0.2% 9,045 0.3%

(+) Impairment and store closing costs 0 0.0% 13,890 0.4%

(+) Goodwill Impairment 0 0.0% 3,198 0.1%

Adjusted EBITDA $ 70,377 8.4% $ 251,235 7.3% |

On

October 29, 2024, the Company issued the following press release. The press release was also posted by the Company to the Campaign