Issuer Free Writing Prospectus

Dated December

10, 2024

Filed Pursuant to Rule 433

Registration Statement No. 333-279879

Decem ber 2024 FOLLOW - ON INVESTOR PRESENTATION COASTAL FINANCIAL CORPORATION

2 LEGAL INFORMATION AND DISCLAIMER Important note regarding forward - looking statements : Statements made in this presentation (or conveyed orally) which are not purely historical are forward - looking statements, as defined in the Private Securities Litigation Reform Act of 1995 . This includes any statements regarding Coastal Financial Corporation's ("Coastal“) plans, objectives, or goals for future operations, products or services, statements regarding the consummation of the proposed offering, and forecasts of its revenues, earnings, or other measures of performance . Such forward - looking statements may be identified by the use of words such as “believe,” “expect,” “anticipate,” “plan,” “estimate,” “should,” “intend,” "target,” “outlook,” “project,” “guidance,” “forecast,” or similar expressions . Forward - looking statements are based on current management expectations and, by their nature, are subject to risks and uncertainties . Actual results may differ materially from those contained in the forward - looking statements . Factors which may cause actual results to differ materially from those contained in such forward - looking statements include those identified in the Company’s most recent annual report Form 10 - K and subsequent quarterly reports on Form 10 - Q and other filings we make with the U . S . Securities and Exchange Commission (the “SEC”), and such factors are incorporated herein by reference . If one or more events related to these or other risks or uncertainties materialize, or if Coastal’s underlying assumptions prove to be incorrect, actual results may differ materially from what Coastal anticipates . You are cautioned not to place undue reliance on forward - looking statements . Further, any forward - looking statement speaks only as of the date on which it is made and Coastal undertakes no obligation to update or revise any forward - looking statement to reflect events or circumstances after the date on which the statement is made or to reflect the occurrence of unanticipated events, except as required by law . All forward - looking statements, express or implied, herein are qualified in their entirety by this cautionary statement . Trademarks : All trademarks, service marks, and trade names referenced in this material are official trademarks and the property of their respective owners . Presentation : Within the charts and tables presented, certain numbers, segments, columns and rows may not sum to totals shown due to rounding . Non - GAAP Measures : This presentation includes certain non - GAAP financial measures . These non - GAAP measures are provided in addition to, and not as substitutes for, measures of our financial performance determined in accordance with GAAP . Our calculation of these non - GAAP measures may not be comparable to similarly titled measures of other companies due to potential differences between companies in the method of calculation . As a result, the use of these non - GAAP measures has limitations and should not be considered superior to, in isolation from, or as a substitute for, related GAAP measures . Reconciliations of these non - GAAP financial measures to the most directly comparable GAAP financial measures can be found at the end of this presentation . This presentation includes non - GAAP financial measures to illustrate the impact of BaaS loan expense on net loan income and yield on CCBX loans, and net interest margin . Net BaaS loan income divided by average CCBX loans is a non - GAAP measure that includes the impact BaaS loan expense on net BaaS loan income and the yield on CCBX loans . The most directly comparable GAAP measure is yield on CCBX loans . Net interest income net of BaaS loan expense divided by average earning assets is a non - GAAP measure that includes the impact BaaS loan expense on net interest income . The most directly comparable GAAP measure is net interest income . Net interest margin, net of BaaS loan expense is a non - GAAP measure that includes the impact of BaaS loan expense on net interest margin . The most directly comparable GAAP measure is net interest margin . This presentation includes non - GAAP financial measures to provide meaningful supplemental information regarding the Company’s operational performance and to enhance investors’ overall understanding of such financial performance . Core noninterest income is presented to illustrate the impact of BaaS credit enhancements, BaaS fraud enhancements, and unrealized gain / (loss) on equity investments net on noninterest income . The most directly comparable GAAP measure is noninterest income . Registration Statement This presentation is not an offer to sell securities, nor is it a solicitation of an offer to buy securities, in any locality, state, country or other jurisdiction where such distribution, publication, availability or use would be contrary to law or regulation or which would require any registration or licensing within such jurisdiction . Neither the SEC nor any other regulatory body has approved or disapproved of the securities of the Company or passed upon the accuracy or adequacy of this presentation . Any representation to the contrary is a criminal offense . Except as otherwise indicated, this presentation speaks as to the date hereof . The delivery of this presentation shall not, under any circumstances, create any implication that there has been no change in the affairs of the Company after the date hereof . Coastal has filed a shelf registration statement on Form S - 3 (File No . 333 - 279879 ) (including a base prospectus) and related preliminary prospectus supplement dated December 10 , 2024 with the SEC for the offering to which this communication relates . The sale of shares of common stock in the proposed underwritten public offering is being made pursuant to such prospectus supplement and accompanying base prospectus . Before you invest, you should read the prospectus in that registration statement, the related preliminary prospectus supplement and other documents that we have filed with the SEC for more complete information about Coastal and this offering . You may get these documents for free by visiting the SEC’s website at www . sec . gov . Alternatively, we, the underwriters or any dealers participating in the offering will arrange to send you the base prospectus and the related preliminary prospectus supplement if you request it by calling Keefe, Bruyette & Woods, Inc . toll free at ( 800 ) 966 - 1559 or emailing USCapitalMarkets@kbw . com .

3 OFFERING SUMMARY Company Exchange / Ticker Security Base Deal Size Option to Purchase Additional Shares Lock - up Period Use of Proceeds Lead Bookrunner Joint Bookrunner Expected Pricing Date Coastal Financial Corporation Nasdaq / CCB Common Stock 15% (100% Primary) 90 days for the Company, Directors & Executive Officers General corporate purposes, including, without limitation, supporting investment opportunities and the growth of the Bank Keefe, Bruyette & Woods, A Stifel Company Hovde Group LLC $85 million (100% Primary) December 10 th , 2024 (post - close)

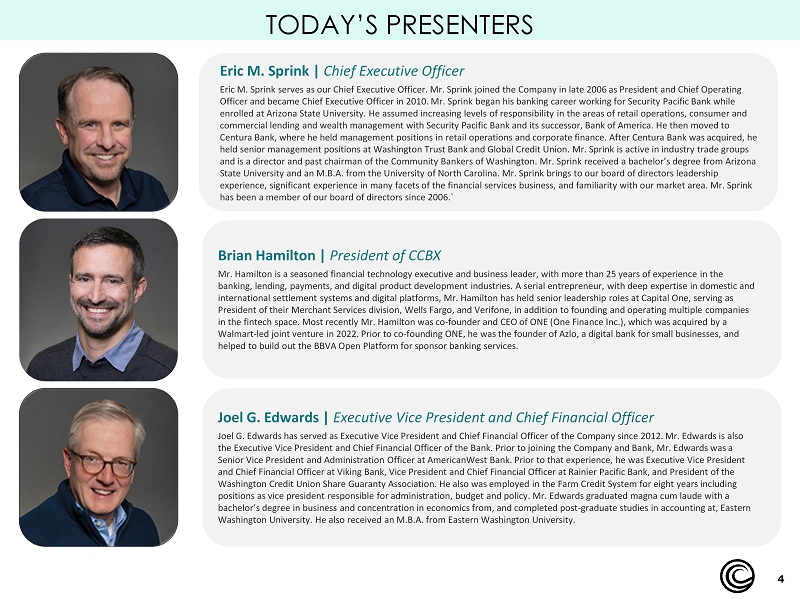

4 Joel G. Edwards | Executive Vice President and Chief Financial Officer Joel G. Edwards has served as Executive Vice President and Chief Financial Officer of the Company since 2012. Mr. Edwards is als o the Executive Vice President and Chief Financial Officer of the Bank. Prior to joining the Company and Bank, Mr. Edwards was a Senior Vice President and Administration Officer at AmericanWest Bank. Prior to that experience, he was Executive Vice Presid ent and Chief Financial Officer at Viking Bank, Vice President and Chief Financial Officer at Rainier Pacific Bank, and President of the Washington Credit Union Share Guaranty Association. He also was employed in the Farm Credit System for eight years including positions as vice president responsible for administration, budget and policy. Mr. Edwards graduated magna cum laude with a bachelor’s degree in business and concentration in economics from, and completed post - graduate studies in accounting at, Eastern Washington University. He also received an M.B.A. from Eastern Washington University. Eric M. Sprink | Chief Executive Officer Eric M. Sprink serves as our Chief Executive Officer. Mr. Sprink joined the Company in late 2006 as President and Chief Operating Officer and became Chief Executive Officer in 2010. Mr. Sprink began his banking career working for Security Pacific Bank while enrolled at Arizona State University. He assumed increasing levels of responsibility in the areas of retail operations, consu mer and commercial lending and wealth management with Security Pacific Bank and its successor, Bank of America. He then moved to Centura Bank, where he held management positions in retail operations and corporate finance. After Centura Bank was acquired, he held senior management positions at Washington Trust Bank and Global Credit Union. Mr. Sprink is active in industry trade groups and is a director and past chairman of the Community Bankers of Washington. Mr. Sprink received a bachelor’s degree from Arizona State University and an M.B.A. from the University of North Carolina. Mr. Sprink brings to our board of directors leadership experience, significant experience in many facets of the financial services business, and familiarity with our market area. M r. Sprink has been a member of our board of directors since 2006.` TODAY’S PRESENTERS Brian Hamilton | President of CCBX Mr. Hamilton is a seasoned financial technology executive and business leader, with more than 25 years of experience in the banking, lending, payments, and digital product development industries. A serial entrepreneur, with deep expertise in domesti c a nd international settlement systems and digital platforms, Mr. Hamilton has held senior leadership roles at Capital One, serving as President of their Merchant Services division, Wells Fargo, and Verifone, in addition to founding and operating multiple comp ani es in the fintech space. Most recently Mr. Hamilton was co - founder and CEO of ONE (One Finance Inc.), which was acquired by a Walmart - led joint venture in 2022. Prior to co - founding ONE, he was the founder of Azlo , a digital bank for small businesses, and helped to build out the BBVA Open Platform for sponsor banking services.

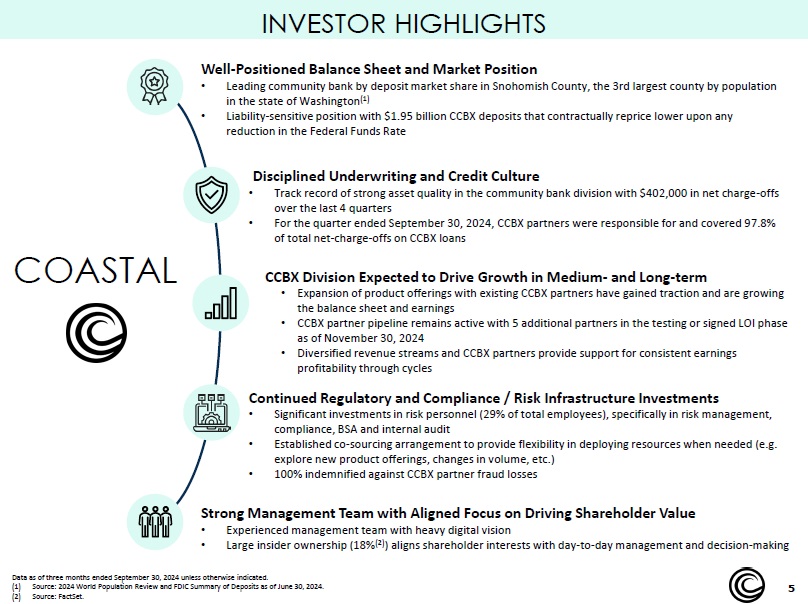

5 INVESTOR HIGHLIGHTS Strong Management Team with Aligned Focus on Driving Shareholder Value • Experienced management team with heavy digital vision • Large insider ownership (18% (2) ) aligns shareholder interests with day - to - day management and decision - making Continued Regulatory and Compliance / Risk Infrastructure Investments • Significant investments in risk personnel (29% of total employees), specifically in risk management, compliance, BSA and internal audit • Established co - sourcing arrangement to provide flexibility in deploying resources when needed (e.g. explore new product offerings, changes in volume, etc.) • 100% indemnified against CCBX partner fraud losses CCBX Division Expected to Drive Growth in Medium - and Long - term • Expansion of product offerings with existing CCBX partners have gained traction and are growing the balance sheet and earnings • CCBX partner pipeline remains active with 5 additional partners in the testing or signed LOI phase as of November 30, 2024 • Diversified revenue streams and CCBX partners provide support for consistent earnings profitability through cycles Well - Positioned Balance Sheet and Market Position • Leading community bank by deposit market share in Snohomish County, the 3rd largest county by population in the state of Washington (1) • Liability - sensitive position with $1.95 billion CCBX deposits that contractually reprice lower upon any reduction in the Federal Funds Rate Data as of three months ended September 30, 2024 unless otherwise indicated. (1) Source: 2024 World Population Review and FDIC Summary of Deposits as of June 30, 2024. (2) Source: FactSet. COASTA L Disciplined Underwriting and Credit Culture • Track record of strong asset quality in the community bank division with $402,000 in net charge - offs over the last 4 quarters • For the quarter ended September 30, 2024, CCBX partners were responsible for and covered 97.8% of total net - charge - offs on CCBX loans

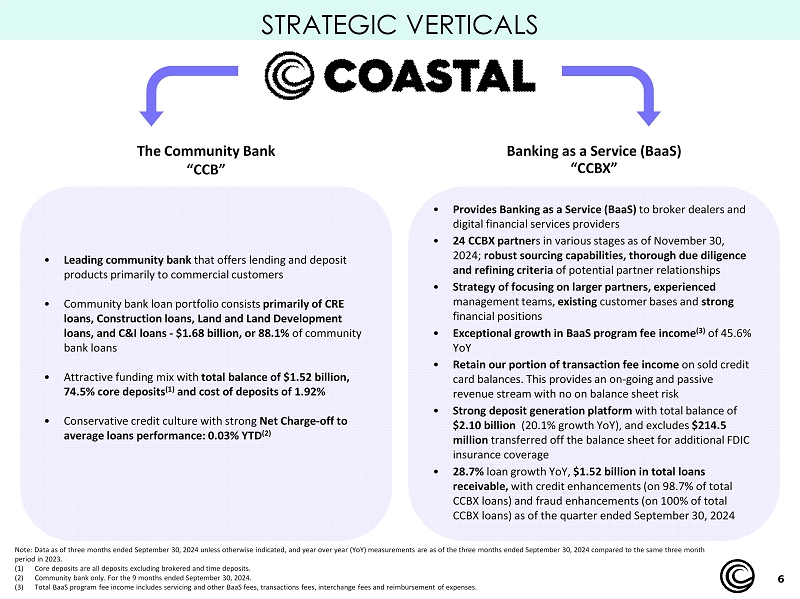

6 STRATEGIC VERTICALS The Community Bank “CCB” Banking as a Service (BaaS) “CCBX” • Leading community bank that offers lending and deposit products primarily to commercial customers • Community bank loan portfolio consists primarily of CRE loans, Construction loans, Land and Land Development loans, and C&I loans - $1.68 billion, or 88.1% of community bank loans • Attractive funding mix with total balance of $1.52 billion, 74.5% core deposits (1) and cost of deposits of 1.92% • Conservative credit culture with strong Net Charge - off to average loans performance: 0.03% YTD (2) • Provides Banking as a Service (BaaS) to broker dealers and digital financial services providers • 24 CCBX partner s in various stages as of November 30, 2024 ; r obust sourcing capabilities, thorough due diligence and refining criteria of potential partner relationships • Strategy of focusing on larger partners, experienced management teams, existing customer bases and strong financial positions • Exceptional growth in BaaS program fee income (3) of 45.6% YoY • Retain our portion of transaction fee income on sold credit card balances. This provides an on - going and passive revenue stream with no on balance sheet risk • Strong deposit generation platform with total balance of $2.10 billion (20.1% growth YoY), and excludes $214.5 million transferred off the balance sheet for additional FDIC insurance coverage • 28.7% loan growth YoY, $1.52 billion in total loans receivable, with credit enhancements (on 98.7% of total CCBX loans) and fraud enhancements (on 100% of total CCBX loans) as of the quarter ended September 30, 2024 Note: Data as of three months ended September 30, 2024 unless otherwise indicated, and year over year (YoY) measurements are as of the three months ended September 30, 2024 compared to the same three month period in 2023. (1) Core deposits are all deposits excluding brokered and time deposits. (2) Community bank only. For the 9 months ended September 30, 2024. (3) Total BaaS program fee income includes servicing and other BaaS fees, transactions fees, interchange fees and reimbursement o f e xpenses.

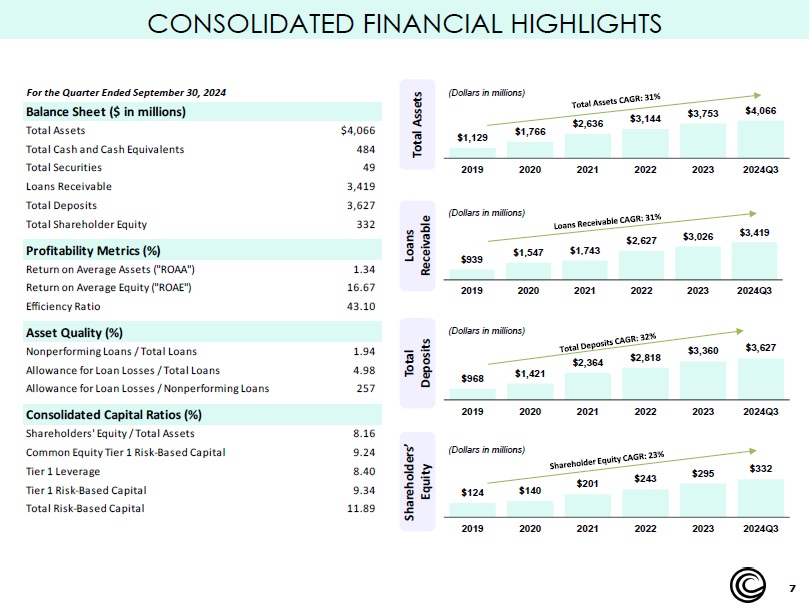

7 CONSOLIDATED FINANCIAL HIGHLIGHTS $968 $1,421 $2,364 $2,818 $3,360 $3,627 2019 2020 2021 2022 2023 2024Q3 $939 $1,547 $1,743 $2,627 $3,026 $3,419 2019 2020 2021 2022 2023 2024Q3 $1,129 $1,766 $2,636 $3,144 $3,753 $4,066 2019 2020 2021 2022 2023 2024Q3 $124 $140 $201 $243 $295 $332 2019 2020 2021 2022 2023 2024Q3 Total Assets Loans Receivable Total Deposits Shareholders’ Equity (Dollars in millions) For the Quarter Ended September 30, 2024 (Dollars in millions) (Dollars in millions) (Dollars in millions) Balance Sheet ($ in millions) Total Assets $4,066 Total Cash and Cash Equivalents 484 Total Securities 49 Loans Receivable 3,419 Total Deposits 3,627 Total Shareholder Equity 332 Profitability Metrics (%) Return on Average Assets ("ROAA") 1.34 Return on Average Equity ("ROAE") 16.67 Efficiency Ratio 43.10 Asset Quality (%) Nonperforming Loans / Total Loans 1.94 Allowance for Loan Losses / Total Loans 4.98 Allowance for Loan Losses / Nonperforming Loans 257 Consolidated Capital Ratios (%) Shareholders' Equity / Total Assets 8.16 Common Equity Tier 1 Risk-Based Capital 9.24 Tier 1 Leverage 8.40 Tier 1 Risk-Based Capital 9.34 Total Risk-Based Capital 11.89

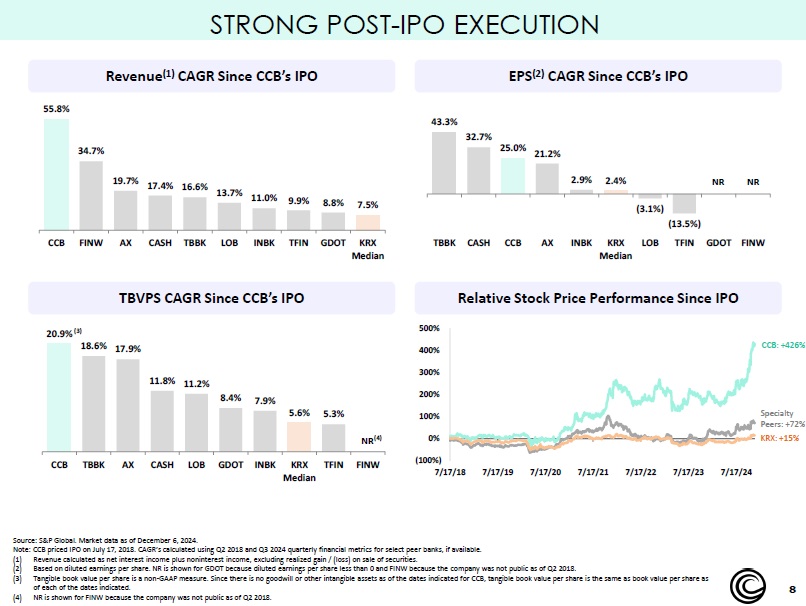

8 STRONG POST - IPO EXECUTION Source: S&P Global. Market data as of December 6, 2024. Note: CCB priced IPO on July 17, 2018. CAGR’s calculated using Q2 2018 and Q3 2024 quarterly financial metrics for select pee r b anks, if available. (1) Revenue calculated as net interest income plus noninterest income, excluding realized gain / (loss) on sale of securities. (2) Based on diluted earnings per share. NR is shown for GDOT because diluted earnings per share less than 0 and FINW because the co mpany was not public as of Q2 2018. (3) Tangible book value per share is a non - GAAP measure. Since there is no goodwill or other intangible assets as of the dates indic ated for CCB, tangible book value per share is the same as book value per share as of each of the dates indicated. (4) NR is shown for FINW because the company was not public as of Q2 2018. Revenue (1) CAGR Since CCB’s IPO EPS (2) CAGR Since CCB’s IPO 55.8% 34.7% 19.7% 17.4% 16.6% 13.7% 11.0% 9.9% 8.8% 7.5% CCB FINW AX CASH TBBK LOB INBK TFIN GDOT KRX Median 43.3% 32.7% 25.0% 21.2% 2.9% 2.4% (3.1%) (13.5%) TBBK CASH CCB AX INBK KRX Median LOB TFIN GDOT FINW TBVPS CAGR Since CCB’s IPO Relative Stock Price Performance Since IPO 20.9% 18.6% 17.9% 11.8% 11.2% 8.4% 7.9% 5.6% 5.3% CCB TBBK AX CASH LOB GDOT INBK KRX Median TFIN FINW NR NR NR (3) (4) (100%) 0% 100% 200% 300% 400% 500% 7/17/18 7/17/19 7/17/20 7/17/21 7/17/22 7/17/23 7/17/24 CCB: +426% Specialty Peers: +72% KRX: +15%

9 CCBX OVERVIEW

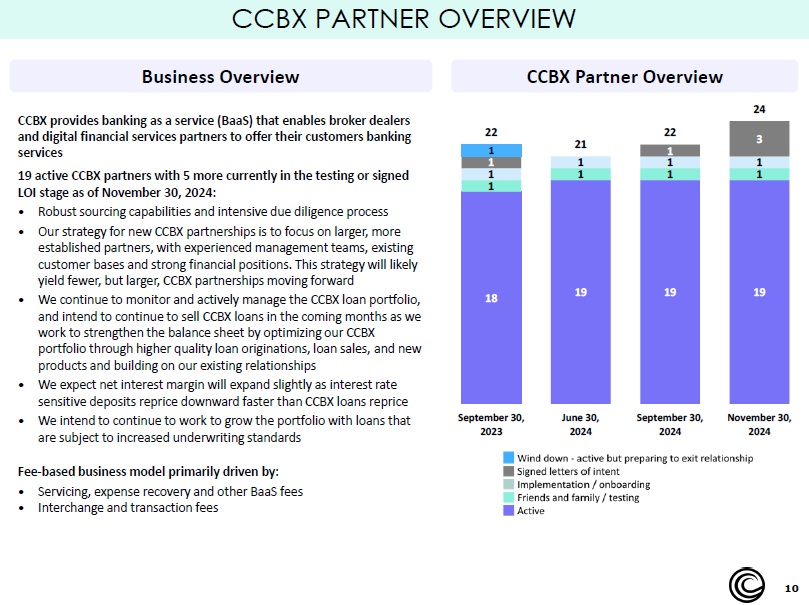

10 CCBX provides banking as a service (BaaS) that enables broker dealers and digital financial services partners to offer their customers banking services 19 active CCBX partners with 5 more currently in the testing or signed LOI stage as of November 30, 2024: • Robust sourcing capabilities and intensive due diligence process • Our strategy for new CCBX partnerships is to focus on larger, more established partners, with experienced management teams, existing customer bases and strong financial positions. This strategy will likely yield fewer, but larger, CCBX partnerships moving forward • We continue to monitor and actively manage the CCBX loan portfolio, and intend to continue to sell CCBX loans in the coming months as we work to strengthen the balance sheet by optimizing our CCBX portfolio through higher quality loan originations, loan sales, and new products and building on our existing relationships • We expect net interest margin will expand slightly as interest rate sensitive deposits reprice downward faster than CCBX loans reprice • We intend to continue to work to grow the portfolio with loans that are subject to increased underwriting standards Fee - based business model primarily driven by: • Servicing, expense recovery and other BaaS fees • Interchange and transaction fees CCBX PARTNER OVERVIEW Business Overview CCBX Partner Overview 18 19 19 19 1 1 1 1 1 1 1 1 1 1 3 1 22 21 22 24 September 30, 2023 June 30, 2024 September 30, 2024 November 30, 2024

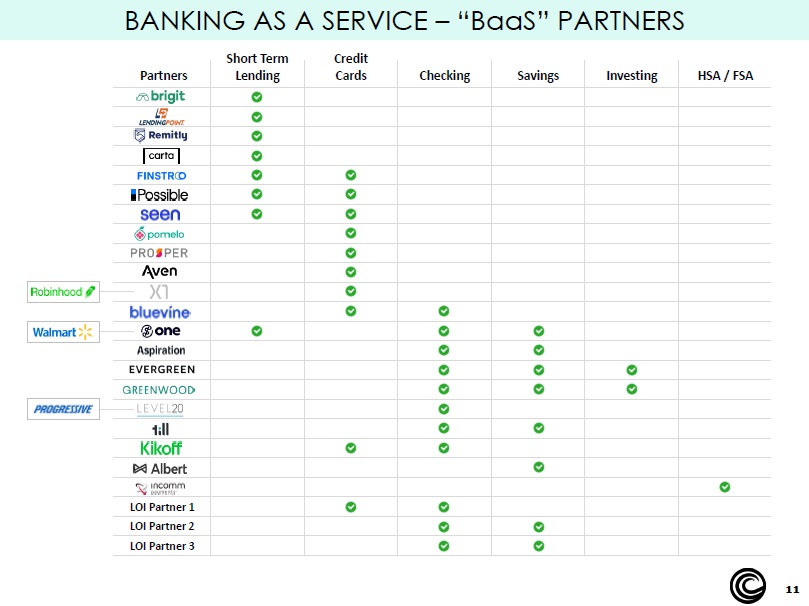

11 BANKING AS A SERVICE – “BaaS” PARTNERS 11 Partners Short Term Lending Credit Cards Checking Savings Investing HSA / FSA LOI Partner 1 LOI Partner 2 LOI Partner 3

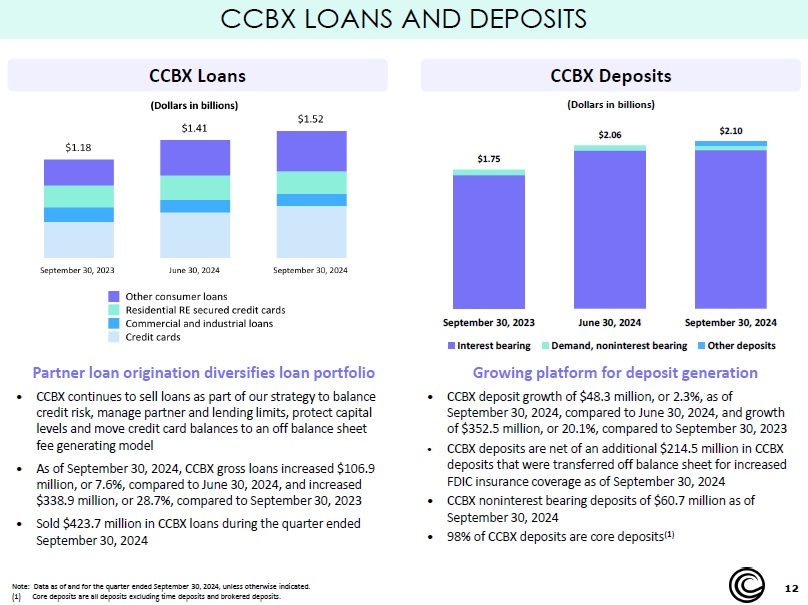

12 Growing platform for deposit generation • CCBX deposit growth of $48.3 million, or 2.3%, as of September 30, 2024, compared to June 30, 2024, and growth of $352.5 million, or 20.1%, compared to September 30, 2023 • CCBX deposits are net of an additional $214.5 million in CCBX deposits that were transferred off balance sheet for increased FDIC insurance coverage as of September 30, 2024 • CCBX noninterest bearing deposits of $60.7 million as of September 30, 2024 • 98% of CCBX deposits are core deposits (1) Partner loan origination diversifies loan portfolio • CCBX continues to sell loans as part of our strategy to balance credit risk, manage partner and lending limits, protect capital levels and move credit card balances to an off balance sheet fee generating model • As of September 30, 2024, CCBX gross loans increased $106.9 million, or 7.6%, compared to June 30, 2024, and increased $338.9 million , or 28.7%, compared to September 30, 2023 • Sold $423.7 million in CCBX loans during the quarter ended September 30, 2024 CCBX Loans CCBX LOANS AND DEPOSITS CCBX Deposits Note: Data as of and for the quarter ended September 30, 2024, unless otherwise indicated. (1) Core deposits are all deposits excluding time deposits and brokered deposits. $1.75 $2.06 $2.10 September 30, 2023 June 30, 2024 September 30, 2024 Interest bearing Demand, noninterest bearing Other deposits (Dollars in b illions )

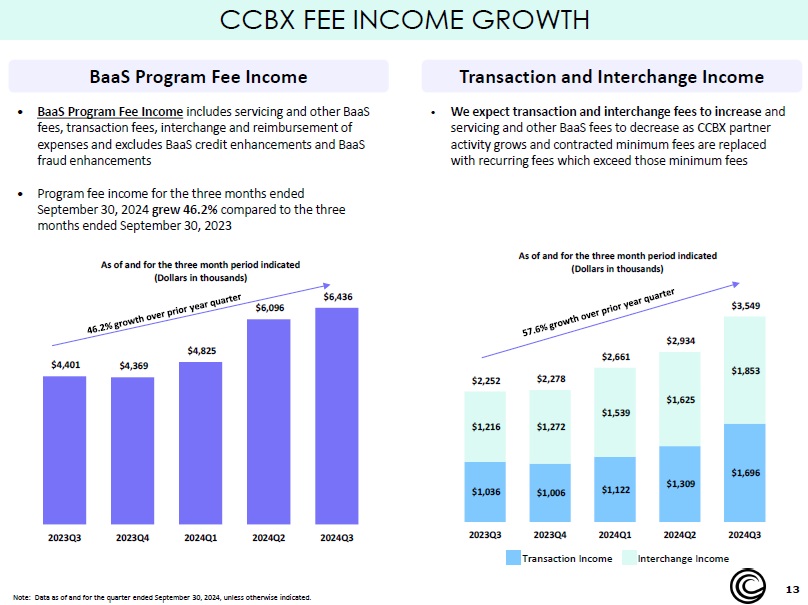

13 $1,036 $1,006 $1,122 $1,309 $1,696 $1,216 $1,272 $1,539 $1,625 $1,853 $2,252 $2,278 $2,661 $2,934 $3,549 2023Q3 2023Q4 2024Q1 2024Q2 2024Q3 As of and for the three month period indicated (Dollars in thousands) CCBX FEE INCOME GROWTH $4,401 $4,369 $4,825 $6,096 $6,436 2023Q3 2023Q4 2024Q1 2024Q2 2024Q3 As of and for the three month period indicated (Dollars in thousands) Transaction and Interchange Income BaaS Program Fee Income Note: Data as of and for the quarter ended September 30, 2024, unless otherwise indicated. • BaaS Program Fee Income includes servicing and other BaaS fees, transaction fees, interchange and reimbursement of expenses and excludes BaaS credit enhancements and BaaS fraud enhancements • Program fee income for the three months ended September 30, 2024 grew 46.2% compared to the three months ended September 30, 2023 • We expect transaction and interchange fees to increase and servicing and other BaaS fees to decrease as CCBX partner activity grows and contracted minimum fees are replaced with recurring fees which exceed those minimum fees Transaction Income Interchange Income

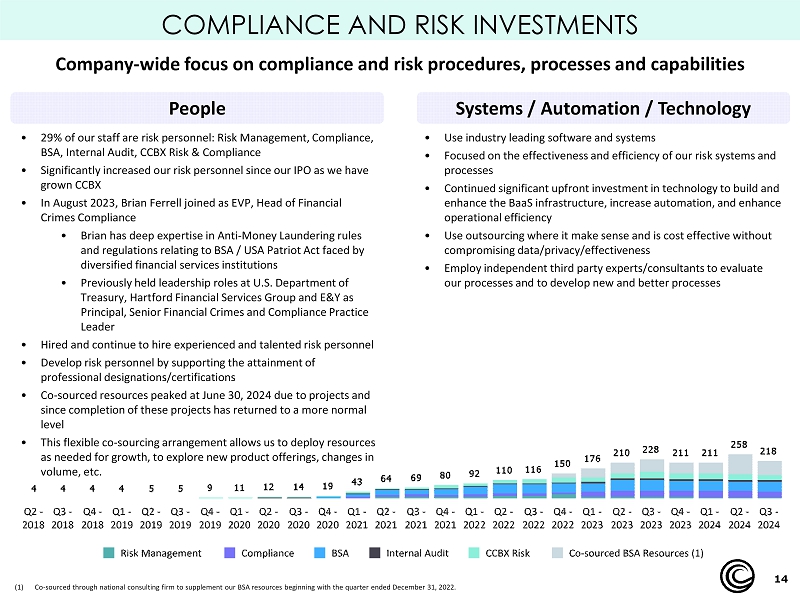

14 COMPLIANCE AND RISK INVESTMENTS • 29% of our staff are risk personnel: Risk Management, Compliance, BSA, Internal Audit, CCBX Risk & Compliance • Significantly increased our risk personnel since our IPO as we have grown CCBX • In August 2023, Brian Ferrell joined as EVP, Head of Financial Crimes Compliance • Brian has deep expertise in Anti - Money Laundering rules and regulations relating to BSA / USA Patriot Act faced by diversified financial services institutions • Previously held leadership roles at U.S. Department of Treasury, Hartford Financial Services Group and E&Y as Principal, Senior Financial Crimes and Compliance Practice Leader • Hired and continue to hire experienced and talented risk personnel • Develop risk personnel by supporting the attainment of professional designations/certifications • Co - sourced resources peaked at June 30, 2024 due to projects and since completion of these projects has returned to a more normal level • This flexible co - sourcing arrangement allows us to deploy resources as needed for growth, to explore new product offerings, changes in volume, etc. • Use industry leading software and systems • Focused on the effectiveness and efficiency of our risk systems and processes • Continued significant upfront investment in technology to build and enhance the BaaS infrastructure, increase automation, and enhance operational efficiency • Use outsourcing where it make sense and is cost effective without compromising data/privacy/effectiveness • Employ independent third party experts/consultants to evaluate our processes and to develop new and better processes Company - wide focus on compliance and risk procedures, processes and capabilities People Systems / Automation / Technology (1) Co - sourced through national consulting firm to supplement our BSA resources beginning with the quarter ended December 31, 2022.

15 COMMUNITY BANK OVERVIEW

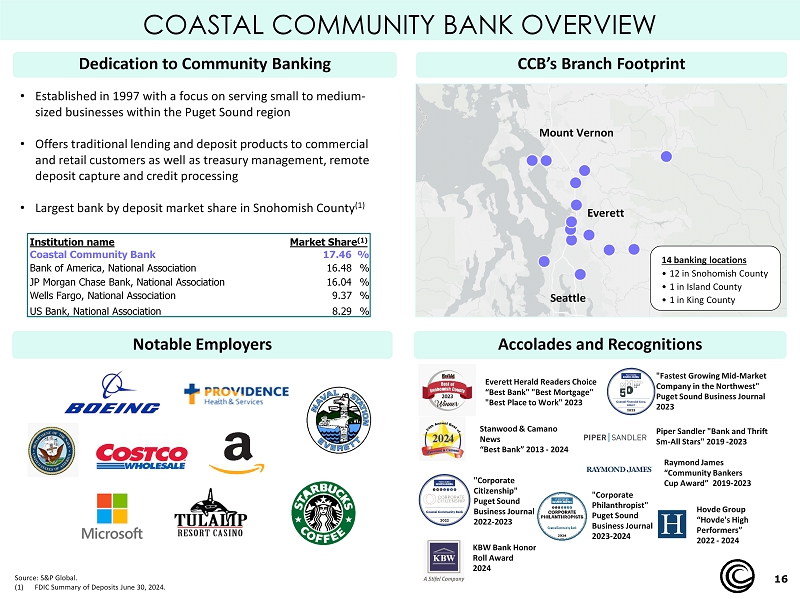

16 • E stablished in 1997 with a focus on serving small to medium - sized businesses within the Puget Sound region • Offers traditional lending and deposit products to commercial and retail customers as well as treasury management, remote deposit capture and credit processing • Largest bank by deposit market share in Snohomish County (1) Accolades and Recognitions Stanwood & Camano News “Best Bank” 2013 - 2024 COASTAL COMMUNITY BANK OVERVIEW Raymond James “Community Bankers Cup Award” 2019 - 2023 Piper Sandler "Bank and Thrift Sm - All Stars" 2019 - 2023 Dedication to Community Banking CCB’s Branch Footprint "Corporate Citizenship" Puget Sound Business Journal 2022 - 2023 Everett Herald Readers Choice “Best Bank" "Best Mortgage" "Best Place to Work" 2023 Market Share (1) Institution name 17.46 % Coastal Community Bank 16.48 % Bank of America, National Association 16.04 % JP Morgan Chase Bank, National Association 9.37 % Wells Fargo, National Association 8.29 % US Bank, National Association Hovde Group “Hovde's High Performers” 2022 - 2024 Notable Employers "Corporate Philanthropist" Puget Sound Business Journal 2023 - 2024 "Fastest Growing Mid - Market Company in the Northwest" Puget Sound Business Journal 2023 Everett Seattle Mount Vernon 14 banking locations • 12 in Snohomish County • 1 in Island County • 1 in King County Source: S&P Global. (1) FDIC Summary of Deposits June 30, 2024. KBW Bank Honor Roll Award 2024

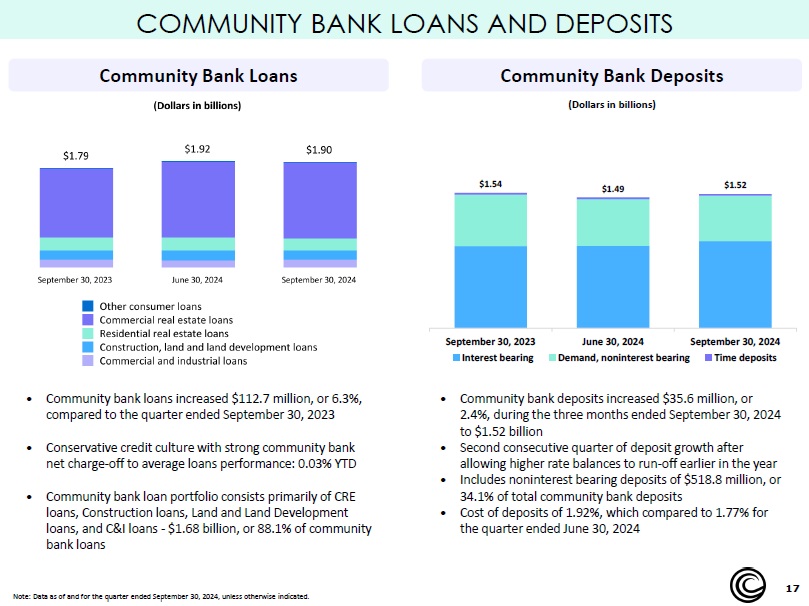

17 • Community b ank loans increased $112.7 million, or 6.3%, compared to the quarter ended September 30, 2023 • Conservative credit culture with strong community bank n et c harge - off to average loans performance: 0.03% YTD • Community bank loan portfolio consists primarily of CRE loans, Construction loans, Land and Land Development loans, and C&I loans - $1.68 billion, or 88.1% of community bank loans • Community bank deposits increased $35.6 million, or 2.4%, during the three months ended September 30, 2024 to $1.52 billion • Second consecutive quarter of deposit growth after allowing higher rate balances to run - off earlier in the yea r • Includes noninterest bearing deposits of $518.8 million, or 34.1% of total community bank deposits • Cost of deposits of 1.92%, which compared to 1.77% for the quarter ended June 30, 2024 COMMUNITY BANK LOANS AND DEPOSITS Community Bank Loans Community Bank Deposits Note: Data as of and for the quarter ended September 30, 2024, unless otherwise indicated. $1.54 $1.49 $1.52 September 30, 2023 June 30, 2024 September 30, 2024 Interest bearing Demand, noninterest bearing Time deposits (Dollars in b illions )

18 CONSOLIDATED COMPANY DETAIL

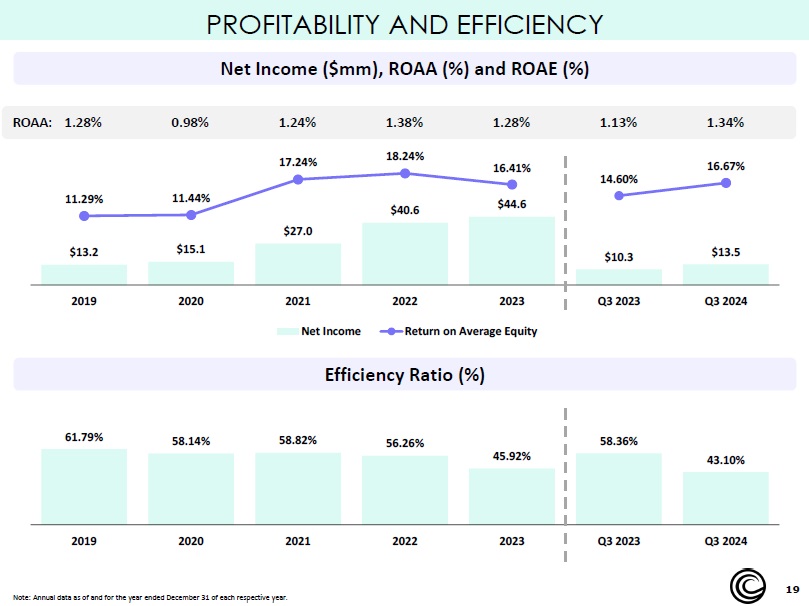

19 Net Income ($mm), ROAA (%) and ROAE (%) $13.2 $15.1 $27.0 $40.6 $44.6 $10.3 $13.5 11.29% 11.44% 17.24% 18.24% 16.41% 14.60% 16.67% 2019 2020 2021 2022 2023 Q3 2023 Q3 2024 Net Income Return on Average Equity Efficiency Ratio (%) 61.79% 58.14% 58.82% 56.26% 45.92% 58.36% 43.10% 2019 2020 2021 2022 2023 Q3 2023 Q3 2024 Note: Annual data as of and for the year ended December 31 of each respective year. ROAA: 1.28% 0.98% 1.24% 1.38% 1.28% 1.13% 1.34% PROFITABILITY AND EFFICIENCY

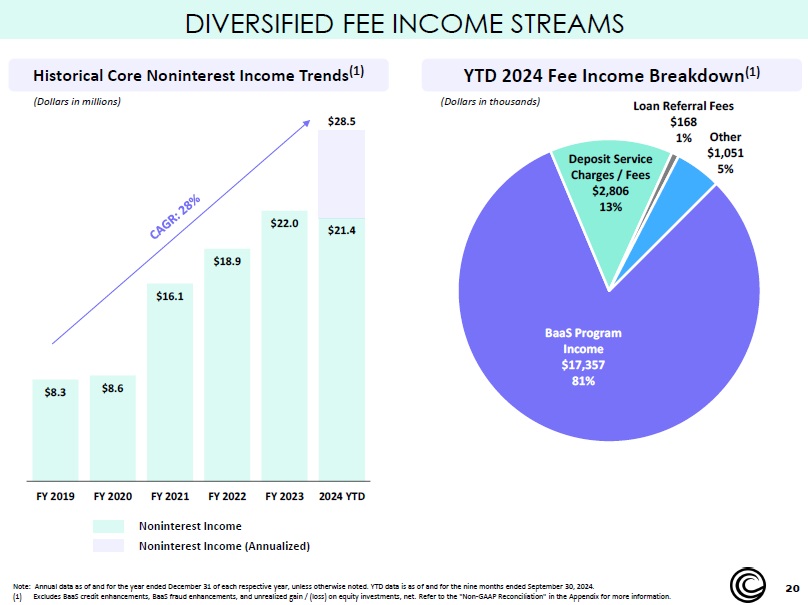

20 BaaS Program Income $17,357 81% Deposit Service Charges / Fees $2,806 13% Loan Referral Fees $168 1% Other $1,051 5% $8.3 $8.6 $16.1 $18.9 $22.0 $21.4 $28.5 FY 2019 FY 2020 FY 2021 FY 2022 FY 2023 2024 YTD DIVERSIFIED FEE INCOME STREAMS Historical Core Noninterest Income Trends (1) YTD 2024 Fee Income Breakdown (1) (Dollars in millions ) (Dollars in thousands) Note: Annual data as of and for the year ended December 31 of each respective year, unless otherwise noted. YTD data is as o f a nd for the nine months ended September 30, 2024. (1) Excludes BaaS credit enhancements, BaaS fraud enhancements, and unrealized gain / (loss) on equity investments, net. Refer to the "Non - GAAP Reconciliation" in the Appendix for more information. Noninterest Income Noninterest Income (Annualized)

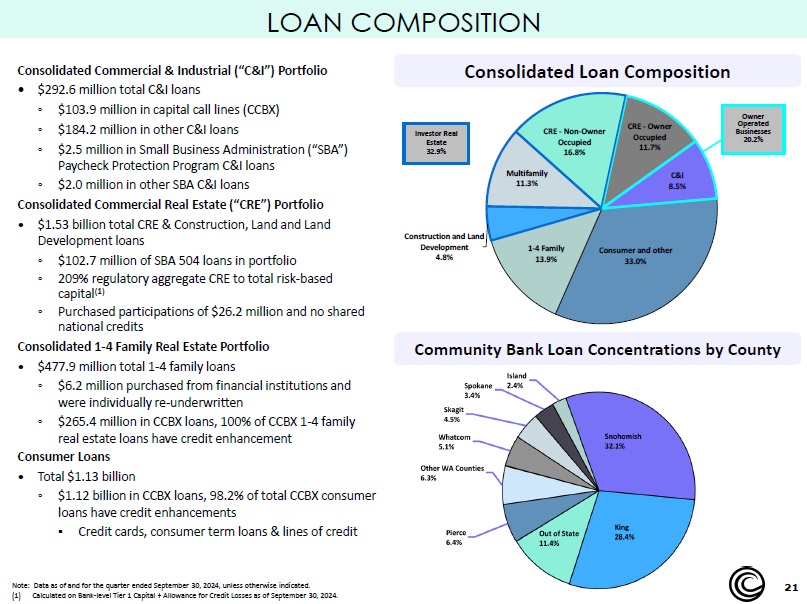

21 LOAN COMPOSITION Consolidated Commercial & Industrial (“C&I”) Portfolio • $292.6 million total C&I loans ◦ $103.9 million in capital call lines (CCBX) ◦ $184.2 million in other C&I loans ◦ $2.5 million in Small Business Administration (“SBA”) Paycheck Protection Program C&I loans ◦ $2.0 million in other SBA C&I loans Consolidated Commercial Real Estate (“CRE”) Portfolio • $1.53 billion total CRE & Construction, Land and Land Development loans ◦ $102.7 million of SBA 504 loans in portfolio ◦ 209% regulatory aggregate CRE to total risk - based capital (1) ◦ Purchased participations of $26.2 million and no shared national credits Consolidated 1 - 4 Family Real Estate Portfolio • $477.9 million total 1 - 4 family loans ◦ $6.2 million purchased from financial institutions and were individually re - underwritten ◦ $265.4 million in CCBX loans, 100% of CCBX 1 - 4 family real estate loans have credit enhancement Consumer Loans • Total $1.13 billion ◦ $1.12 billion in CCBX loans, 98.2% of total CCBX consumer loans have credit enhancements ▪ Credit cards, consumer term loans & lines of credi t Consumer and other 33.0% 1 - 4 Family 13.9% Construction and Land Development 4.8% Multifamily 11.3% CRE - Non - Owner Occupied 16.8% CRE - Owner Occupied 11.7% C&I 8.5% Investor Real Estate 32.9% Owner Operated Businesses 20.2% Consolidated Loan Composition Community Bank Loan Concentrations by County Note: Data as of and for the quarter ended September 30, 2024, unless otherwise indicated. (1) Calculated on Bank - level Tier 1 Capital + Allowance for Credit Losses as of September 30, 2024.

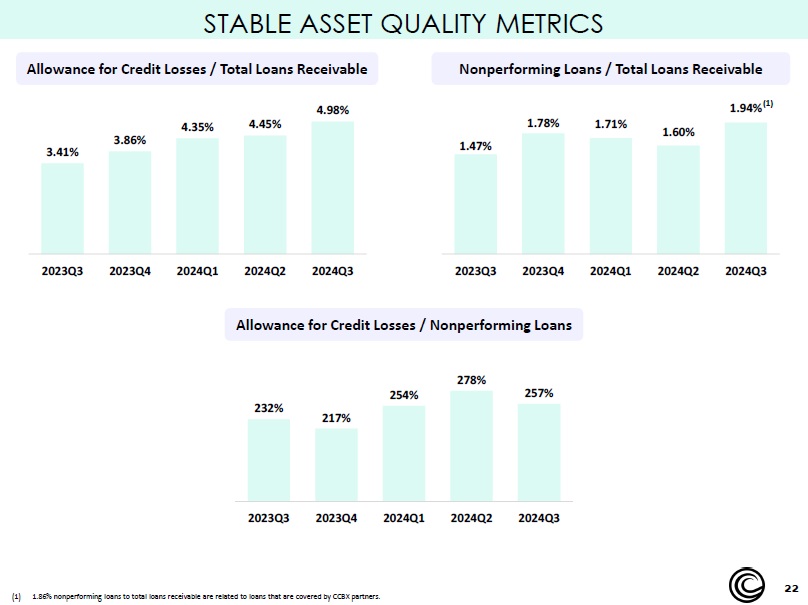

22 STABLE ASSET QUALITY METRICS Allowance for Credit Losses / Total Loans Receivable Nonperforming Loans / Total Loans Receivable Allowance for Credit Losse s / Nonperforming Loans 232% 217% 254% 278% 257% 2023Q3 2023Q4 2024Q1 2024Q2 2024Q3 1.47% 1.78% 1.71% 1.60% 1.94% 2023Q3 2023Q4 2024Q1 2024Q2 2024Q3 3.41% 3.86% 4.35% 4.45% 4.98% 2023Q3 2023Q4 2024Q1 2024Q2 2024Q3 (1) 1.86% nonperforming loans to total loans receivable are related to loans that are covered by CCBX partners. (1)

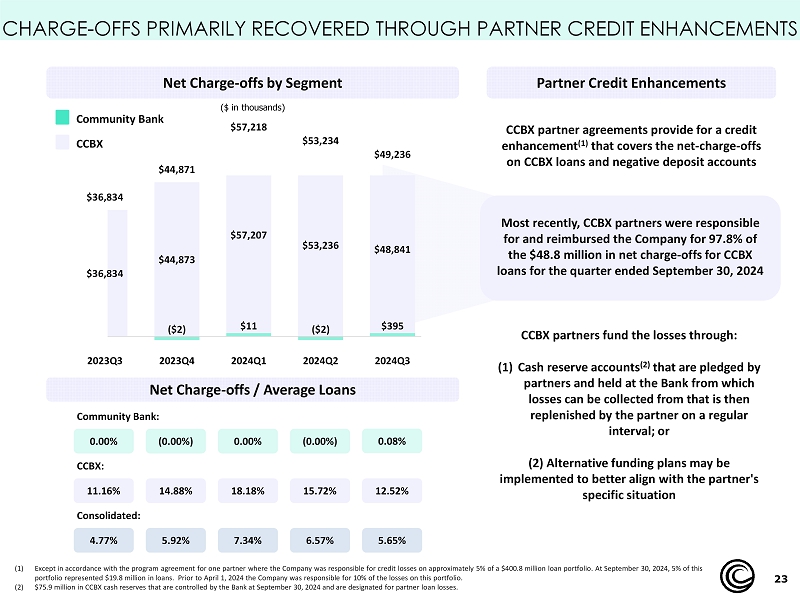

23 CHARGE - OFFS PRIMARILY RECOVERED THROUGH PARTNER CREDIT ENHANCEMENTS CCBX partner agreements provide for a credit enhancement (1) that covers the net - charge - offs on CCBX loans and negative deposit accounts Most recently, CCBX partners were responsible for and reimbursed the Company for 97.8% of the $48.8 million in net charge - offs for CCBX loans for the quarter ended September 30, 2024 CCBX p artners fund the losses through: (1) Cash reserve accounts (2) that are pledged by partners and held at the Bank from which losses can be collected from that is then replenished by the partner on a regular interval; or (2) Alternative funding plans may be implemented to better align with the partner's specific situation (1) Except in accordance with the program agreement for one partner where the Company was responsible for credit losses on approx ima tely 5% of a $400.8 million loan portfolio. At September 30, 2024, 5% of this portfolio represented $19.8 million in loans. Prior to April 1, 2024 the Company was responsible for 10% of the losses on th is portfolio. (2) $75.9 million in CCBX cash reserves that are controlled by the Bank at September 30, 2024 and are designated for partner loan lo sses. Net Charge - offs by Segment Community Bank: CCBX: Consolidated: ( $ in thousands ) 0.00% (0.00%) 0.00% (0.00%) 0.08% 11.16% 14.88% 18.18% 15.72% 12.52% 4.77% 5.92% 7.34% 6.57% 5.65% ($2) $11 ($2) $395 $36,834 $44,873 $57,207 $53,236 $48,841 $36,834 $44,871 $57,218 $53,234 $49,236 2023Q3 2023Q4 2024Q1 2024Q2 2024Q3 Community Bank CCBX Net Charge - offs / Average Loans Partner Credit Enhancements

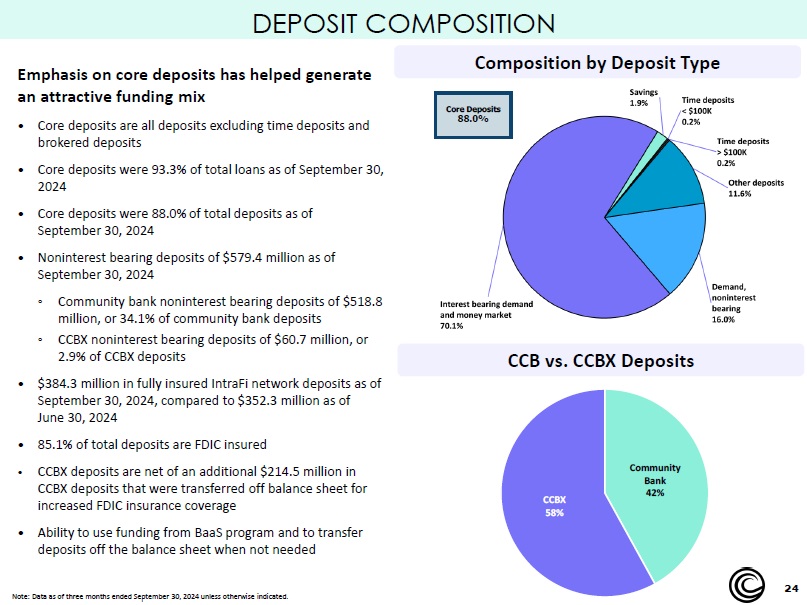

24 DEPOSIT COMPOSITION Emphasis on core deposits has helped generate an attractive funding mix • Core deposits are all deposits excluding time deposits and brokered deposits • Core deposits were 93.3% of total loans as of September 30, 2024 • Core deposits were 88.0% of total deposits as of September 30, 2024 • Noninterest bearing deposits of $579.4 million as of September 30, 2024 ◦ Community bank noninterest bearing deposits of $518.8 million, or 34.1% of community bank deposits ◦ CCBX noninterest bearing deposits of $60.7 million, or 2.9% of CCBX deposits • $384.3 million in fully insured IntraFi network deposits as of September 30, 2024, compared to $352.3 million as of June 30, 2024 • 85.1% of total deposits are FDIC insured • CCBX deposits are net of an additional $214.5 million in CCBX deposits that were transferred off balance sheet for increased FDIC insurance coverage • Ability to use funding from BaaS program and to transfer deposits off the balance sheet when not neede d Core Deposits 88.0% Composition by Deposit Type Note: Data as of three months ended September 30, 2024 unless otherwise indicated. Community Bank 42% CCBX 58% CCB vs. CCBX Deposits

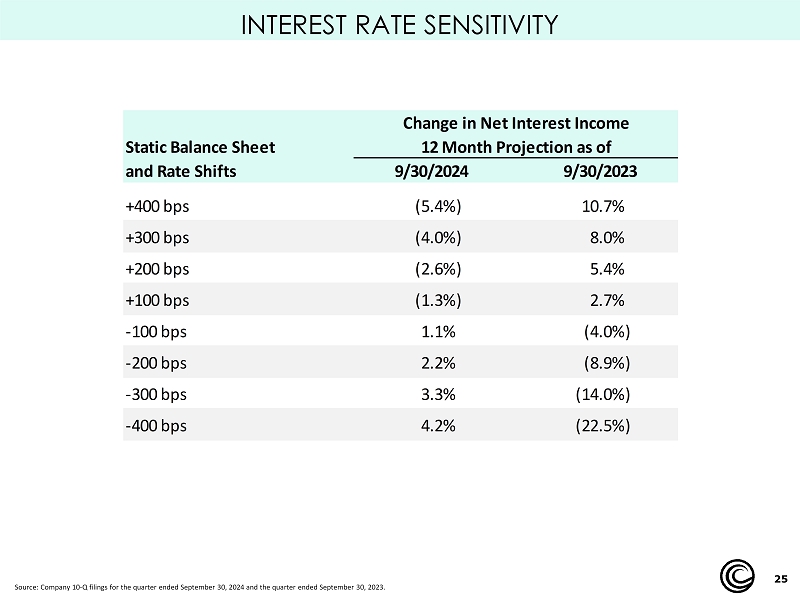

25 INTEREST RATE SENSITIVITY Change in Net Interest Income Static Balance Sheet 12 Month Projection as of and Rate Shifts 9/30/2024 9/30/2023 +400 bps (5.4%) 10.7% +300 bps (4.0%) 8.0% +200 bps (2.6%) 5.4% +100 bps (1.3%) 2.7% -100 bps 1.1% (4.0%) -200 bps 2.2% (8.9%) -300 bps 3.3% (14.0%) -400 bps 4.2% (22.5%) Source: Company 10 - Q filings for the quarter ended September 30, 2024 and the quarter ended September 30, 2023.

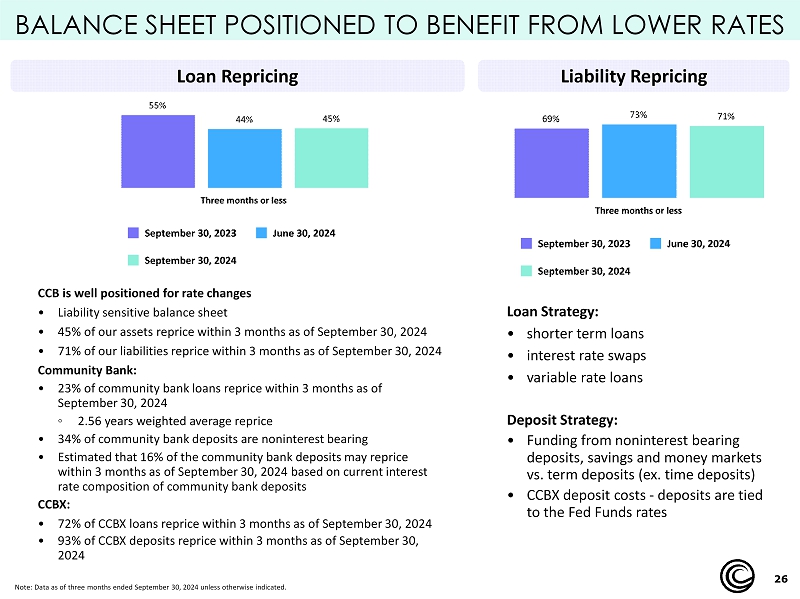

26 BALANCE SHEET POSITIONED TO BENEFIT FROM LOWER RATES CCB is well positioned for rate changes • Liability sensitive balance sheet • 45% of our assets reprice within 3 months as of September 30, 2024 • 71% of our liabilities reprice within 3 months as of September 30, 2024 Community Bank: • 23% of community bank loans reprice within 3 months as of September 30, 2024 ◦ 2.56 years weighted average reprice • 34% of community bank deposits are noninterest bearing • Estimated that 16% of the community bank deposits may reprice within 3 months as of September 30, 2024 based on current interest rate composition of community bank deposits CCBX: • 72% of CCBX loans reprice within 3 months as of September 30, 2024 • 93% of CCBX deposits reprice within 3 months as of September 30, 2024 Loan Strategy: • shorter term loans • interest rate swaps • variable rate loans Deposit Strategy: • Funding from noninterest bearing deposits, savings and money markets vs. term deposits (ex. time deposits) • CCBX deposit costs - deposits are tied to the Fed Funds rate s Loan Repricing Liability Repricing Note: Data as of three months ended September 30, 2024 unless otherwise indicated.

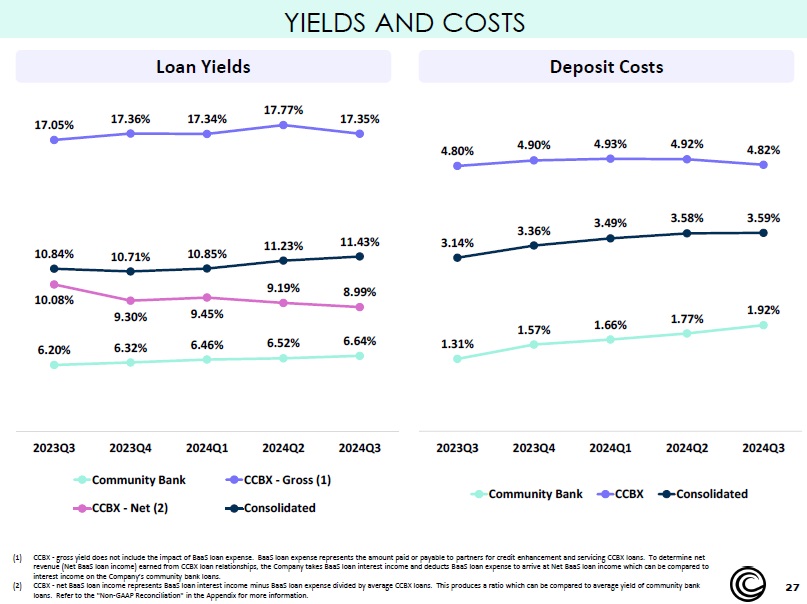

27 YIELDS AND COSTS Deposit Costs Loan Yields 1.31% 1.57% 1.66% 1.77% 1.92% 4.80% 4.90% 4.93% 4.92% 4.82% 3.14% 3.36% 3.49% 3.58% 3.59% 2023Q3 2023Q4 2024Q1 2024Q2 2024Q3 Community Bank CCBX Consolidated 6.20% 6.32% 6.46% 6.52% 6.64% 17.05% 17.36% 17.34% 17.77% 17.35% 10.08% 9.30% 9.45% 9.19% 8.99% 10.84% 10.71% 10.85% 11.23% 11.43% 2023Q3 2023Q4 2024Q1 2024Q2 2024Q3 Community Bank CCBX - Gross (1) CCBX - Net (2) Consolidated (1) CCBX - gross yield does not include the impact of BaaS loan expense. BaaS loan expense represents the amount paid or payable to partners for credit enhancement and servicing CCBX loans. To determine net revenue (Net BaaS loan income) earned from CCBX loan relationships, the Company takes BaaS loan interest income and deducts B aaS loan expense to arrive at Net BaaS loan income which can be compared to interest income on the Company’s community bank loans. (2) CCBX - net BaaS loan income represents BaaS loan interest income minus BaaS loan expense divided by average CCBX loans. This pr oduces a ratio which can be compared to average yield of community bank loans. Refer to the "Non - GAAP Reconciliation" in the Appendix for more information.

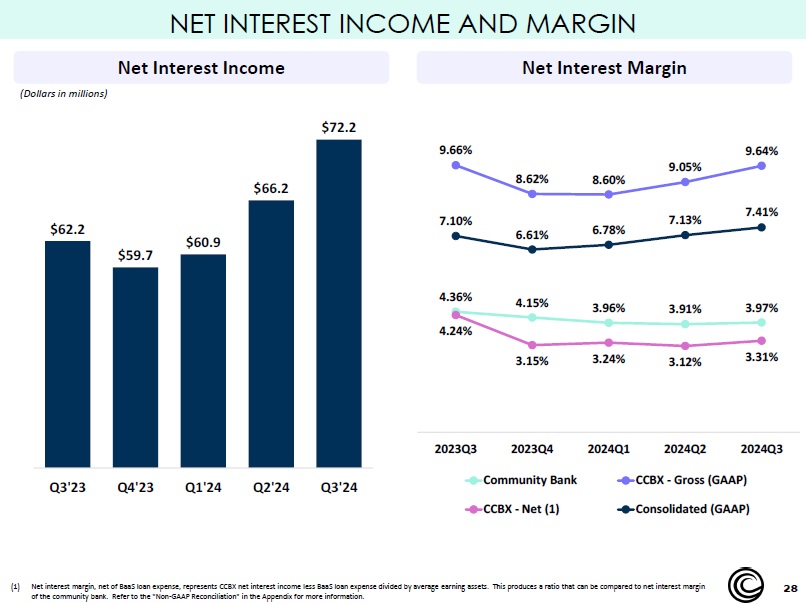

28 NET INTEREST INCOME AND MARGIN Net Interest Income Net Interest Margin 4.36% 4.15% 3.96% 3.91% 3.97% 9.66% 8.62% 8.60% 9.05% 9.64% 4.24% 3.15% 3.24% 3.12% 3.31% 7.10% 6.61% 6.78% 7.13% 7.41% 2023Q3 2023Q4 2024Q1 2024Q2 2024Q3 Community Bank CCBX - Gross (GAAP) CCBX - Net (1) Consolidated (GAAP) (1) Net interest margin, net of BaaS loan expense, represents CCBX net interest income less BaaS loan expense divided by average ear ning assets. This produces a ratio that can be compared to net interest margin of the community bank. Refer to the "Non - GAAP Reconciliation" in the Appendix for more information. $62.2 $59.7 $60.9 $66.2 $72.2 Q3'23 Q4'23 Q1'24 Q2'24 Q3'24 (Dollars in millions )

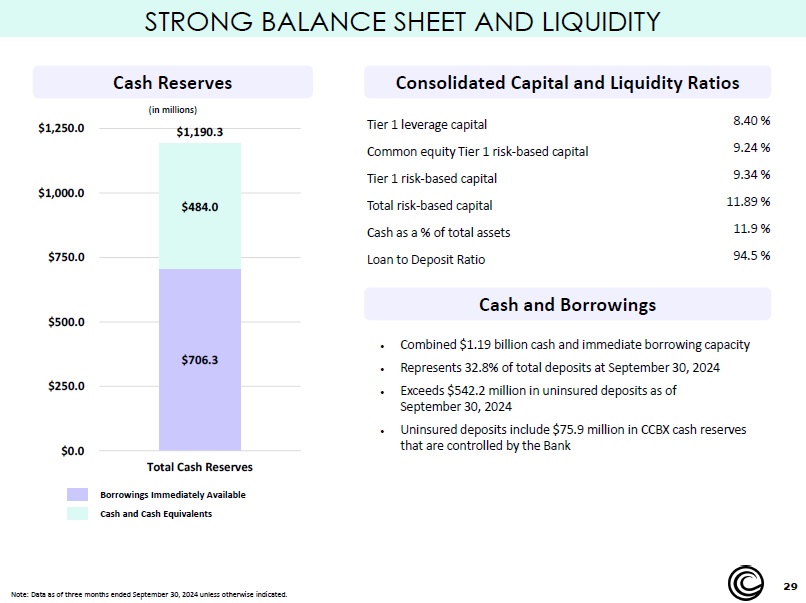

29 STRONG BALANCE SHEET AND LIQUIDITY (in millions) • Combined $1.19 billion cash and immediate borrowing capacity • Represents 32.8 % of total deposits at September 30, 2024 • Exceeds $542.2 million in uninsured deposits as of September 30, 2024 • Uninsured deposits include $75.9 million in CCBX cash reserves that are controlled by the Bank 8.40 % Tier 1 leverage capital 9.24 % Common equity Tier 1 risk - based capital 9.34 % Tier 1 risk - based capital 11.89 % Total risk - based capital 11.9 % Cash as a % of total assets 94.5 % Loan to Deposit Ratio Consolidated Capital and Liquidity Ratios Cash and Borrowings Note: Data as of three months ended September 30, 2024 unless otherwise indicated. Cash Reserves $706.3 $484.0 $1,190.3 $0.0 $250.0 $500.0 $750.0 $1,000.0 $1,250.0 Total Cash Reserves Borrowings Immediately Available Cash and Cash Equivalents

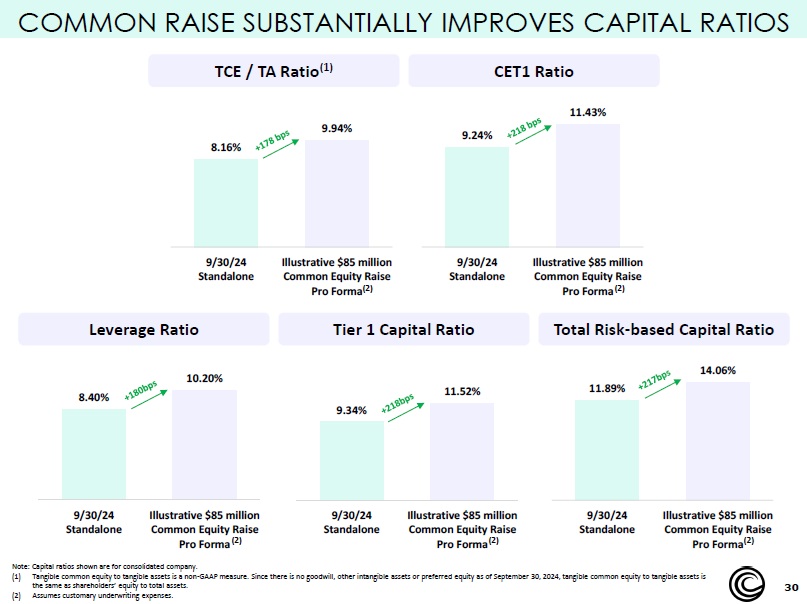

30 COMMON RAISE SUBSTANTIALLY IMPROVES CAPITAL RATIOS Note: Capital ratios shown are for consolidated company. (1) Tangible common equity to tangible assets is a non - GAAP measure. Since there is no goodwill, other intangible assets or preferre d equity as of September 30, 2024, tangible common equity to tangible assets is the same as shareholders’ equity to total assets. (2) Assumes customary underwriting expenses. Leverage Ratio Tier 1 Capital Ratio Total Risk - based Capital Ratio TCE / TA Ratio (1) CET1 Ratio 8.16% 9.94% 9/30/24 Standalone Illustrative $85 million Common Equity Raise Pro Forma 9.24% 11.43% 9/30/24 Standalone Illustrative $85 million Common Equity Raise Pro Forma 8.40% 10.20% 9/30/24 Standalone Illustrative $85 million Common Equity Raise Pro Forma 9.34% 11.52% 9/30/24 Standalone Illustrative $85 million Common Equity Raise Pro Forma 11.89% 14.06% 9/30/24 Standalone Illustrative $85 million Common Equity Raise Pro Forma (2) (2) (2) (2) (2)

31 APPENDIX

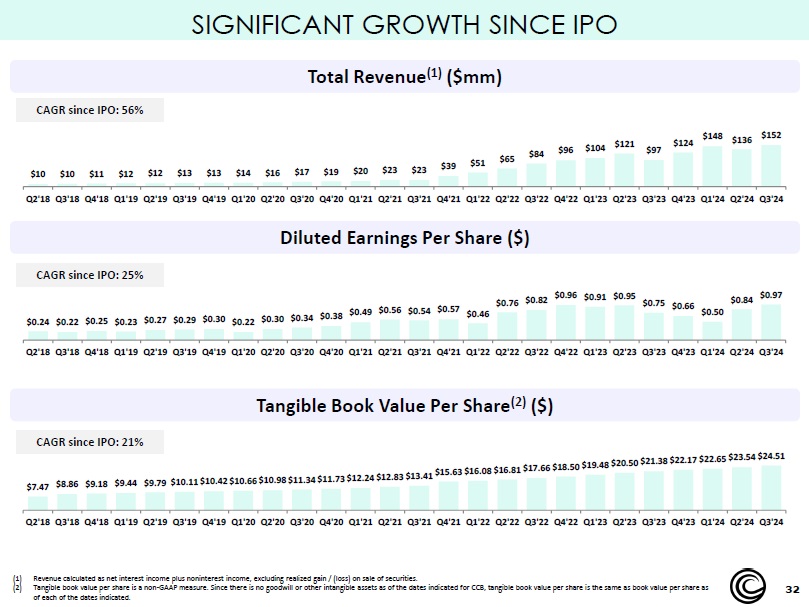

32 SIGNIFICANT GROWTH SINCE IPO Total Revenue (1) ($mm) Diluted Earnings Per Share ($) Tangible Book Value Per Share (2) ($) $10 $10 $11 $12 $12 $13 $13 $14 $16 $17 $19 $20 $23 $23 $39 $51 $65 $84 $96 $104 $121 $97 $124 $148 $136 $152 Q2'18 Q3'18 Q4'18 Q1'19 Q2'19 Q3'19 Q4'19 Q1'20 Q2'20 Q3'20 Q4'20 Q1'21 Q2'21 Q3'21 Q4'21 Q1'22 Q2'22 Q3'22 Q4'22 Q1'23 Q2'23 Q3'23 Q4'23 Q1'24 Q2'24 Q3'24 $0.24 $0.22 $0.25 $0.23 $0.27 $0.29 $0.30 $0.22 $0.30 $0.34 $0.38 $0.49 $0.56 $0.54 $0.57 $0.46 $0.76 $0.82 $0.96 $0.91 $0.95 $0.75 $0.66 $0.50 $0.84 $0.97 Q2'18 Q3'18 Q4'18 Q1'19 Q2'19 Q3'19 Q4'19 Q1'20 Q2'20 Q3'20 Q4'20 Q1'21 Q2'21 Q3'21 Q4'21 Q1'22 Q2'22 Q3'22 Q4'22 Q1'23 Q2'23 Q3'23 Q4'23 Q1'24 Q2'24 Q3'24 $7.47 $8.86 $9.18 $9.44 $9.79 $10.11 $10.42 $10.66 $10.98 $11.34 $11.73 $12.24 $12.83 $13.41 $15.63 $16.08 $16.81 $17.66 $18.50 $19.48 $20.50 $21.38 $22.17 $22.65 $23.54 $24.51 Q2'18 Q3'18 Q4'18 Q1'19 Q2'19 Q3'19 Q4'19 Q1'20 Q2'20 Q3'20 Q4'20 Q1'21 Q2'21 Q3'21 Q4'21 Q1'22 Q2'22 Q3'22 Q4'22 Q1'23 Q2'23 Q3'23 Q4'23 Q1'24 Q2'24 Q3'24 CAGR since IPO: 56% CAGR since IPO: 25% CAGR since IPO: 21% (1) Revenue calculated as net interest income plus noninterest income, excluding realized gain / (loss) on sale of securities. (2) Tangible book value per share is a non - GAAP measure. Since there is no goodwill or other intangible assets as of the dates indic ated for CCB, tangible book value per share is the same as book value per share as of each of the dates indicated.

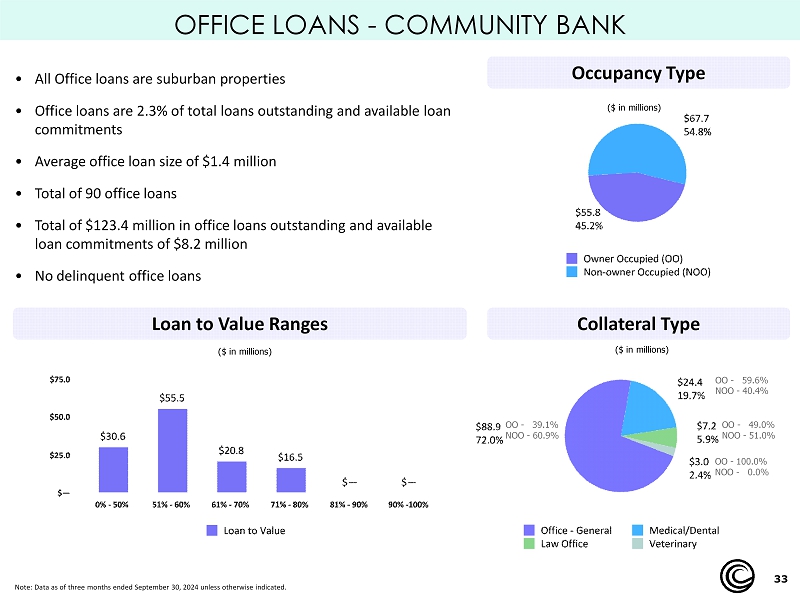

33 OFFICE LOANS - COMMUNITY BANK ( $ in millions) • All Office loans are suburban properties • Office loans are 2.3% of total loans outstanding and available loan commitments • Average office loan size of $1.4 million • Total of 90 office loans • Total of $123.4 million in office loans outstanding and available loan commitments of $8.2 million • No delinquent office loans ($ in millions) ($ in millions) OO - 49.0% NOO - 51.0% OO - 100.0% NOO - 0.0% OO - 59.6% NOO - 40.4% OO - 39.1% NOO - 60.9% Occupancy Type Collateral Type Loan to Value Ranges Note: Data as of three months ended September 30, 2024 unless otherwise indicated.

34 ENVIRONMENTAL, SOCIAL AND GOVERNANCE ("ESG") INITIATIVES For Coastal, ESG is a complex initiative across the whole organization. Addressing the issue of the approximately 5.9 million un banked households (1) in the United States cannot be tackled with merely adding products or providing diversity, equity and inclusion training. Nor can re al environmental impact happen through mere board level policies and simply changing our investment portfolio. We are choosing to tackle our ESG initiative s t hroughout our company with meaningful actions and collaboration. CCBX – Working with our CCBX partners allows us to provide a broader range of services to different demographics through their offer ing s. Developing the kind of unique offerings to specific under - served or under - banked populations would be difficult for a bank our size, but by partnering with third - party fintech partners like Brigit, Greenwood and One we are able to use our banking charter to support this effort in a much broader scope. Coastal Community Bank – Our community bank has always had close ties to the communities we serve with our employees actively volunteering in those communities, and we have been recognized as a corporate philanthropist by the Puget Sound Business Journal. We are now evolvi ng to offer affiliated products through our third - party fintech partners that are more inclusive and meet their needs of a broader range of consumers. Once agai n, our scope and reach is multiplied by collaborating with our third - party fintech partners to offer inclusive products. Financial Inclusion We see financial inclusion as providing access to useful and affordable financial products and services to meet the needs of the under - served . However, overcoming a widespread distrust of banks, lack of financial education, and barriers to entry are all part of the process to bring the underserved in our communities the financial products and services they need to thrive. We are actively working to address: • Accessibility to services • Needs - based solutions • Education In collaboration with the Cities for Financial Empowerment and the Bank On national platform, this past year, a Coastal team worked to develop the Access checking product to support the financial stability of unbanked and underbanked residents in our communities by providing a safe, affordable and functional product. In January 2023, our Access checking product passed product certification and met the National Account Standards and was launched with the official Bank On certification . Climate Change Coastal is approaching our responsibility in many ways from understanding our carbon footprint and identifying potential offsets, reductions and to developing strong partnerships with ESG focused fintechs . In January 2023 we completed a Sustainable Impact Survey to understand our GHG impact and ways we can offset it. Working with our partners, we are exploring ways to develop customer facing - solutions that enable climate action and are able to participate in developing and implementing meaningful changes to help turn the tide on climate change, doing our part to help transition to a net - zero economy. Additionally, we have and will continue to consider climate change and its impact on our loan portfolio and customers. ESG Social Responsibility Environmental Responsibility Source: 2021 National Survey of Unbanked and Underbanked Households by the Federal Deposit Insurance Corporation (FDIC) in No vem ber 2022.

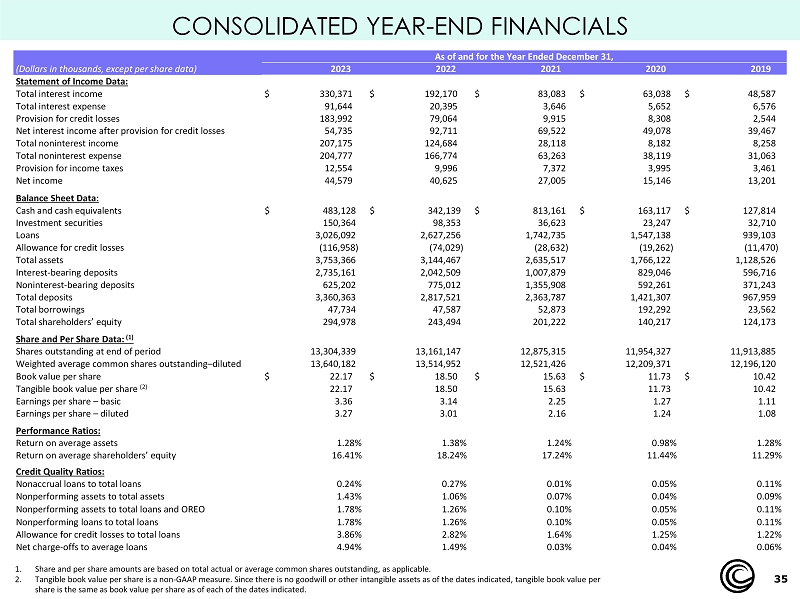

35 1. Share and per share amounts are based on total actual or average common shares outstanding, as applicable. 2. Tangible book value per share is a non - GAAP measure. Since there is no goodwill or other intangible assets as of the dates indic ated, tangible book value per share is the same as book value per share as of each of the dates indicated. As of and for the Year Ended December 31, 2019 2020 2021 2022 2023 (Dollars in thousands, except per share data) Statement of Income Data: $ 48,587 $ 63,038 $ 83,083 $ 192,170 $ 330,371 Total interest income 6,576 5,652 3,646 20,395 91,644 Total interest expense 2,544 8,308 9,915 79,064 183,992 Provision for credit losses 39,467 49,078 69,522 92,711 54, 735 Net interest income after provision for credit losses 8,258 8,182 28,118 124,684 207,175 Total noninterest income 31,063 38,119 63,263 166,774 204,777 Total noninterest expense 3,461 3,995 7,372 9,996 12,554 Provision for income taxes 13,201 15,146 27,005 40,625 44,579 Net income Balance Sheet Data: $ 127,814 $ 163,117 $ 813,161 $ 342,139 $ 483,128 Cash and cash equivalents 32,710 23,247 36,623 98,353 150,364 Investment securities 939,103 1,547,138 1,742,735 2,627,256 3,026,092 Loans (11,470) (19,262) (28,632) (74,029) (116,958) Allowance for credit losses 1,128,526 1,766,122 2,635,517 3,144,467 3,753,366 Total assets 596,716 829,046 1,007,879 2,042,509 2,735,161 Interest - bearing deposits 371,243 592,261 1,355,908 775,012 625,202 Noninterest - bearing deposits 967,959 1,421,307 2,363,787 2,817,521 3,360,363 Total deposits 23,562 192,292 52,873 47,587 47,734 Total borrowings 124,173 140,217 201,222 243,494 294,978 Total shareholders’ equity Share and Per Share Data: (1) 11,913,885 11,954,327 12,875,315 13,161,147 13,304,339 Shares outstanding at end of period 12,196,120 12,209,371 12,521,426 13,514,952 13,640,182 Weighted average common shares outstanding – diluted $ 10.42 $ 11.73 $ 15.63 $ 18.50 $ 22.17 Book value per share 10.42 11.73 15.63 18.50 22.17 Tangible book value per share (2) 1.11 1.27 2.25 3.14 3.36 Earnings per share – basic 1.08 1.24 2.16 3.01 3.27 Earnings per share – diluted Performance Ratios: 1.28% 0.98% 1.24% 1.38% 1.28% Return on average assets 11.29% 11.44% 17.24% 18.24% 16.41% Return on average shareholders’ equity Credit Quality Ratios: 0.11% 0.05% 0.01% 0.27% 0.24% Nonaccrual loans to total loans 0.09% 0.04% 0.07% 1.06% 1.43% Nonperforming assets to total assets 0.11% 0.05% 0.10% 1.26% 1.78% Nonperforming assets to total loans and OREO 0.11% 0.05% 0.10% 1.26% 1.78% Nonperforming loans to total loans 1.22% 1.25% 1.64% 2.82% 3.86% Allowance for credit losses to total loans 0.06% 0.04% 0.03% 1.49% 4.94% Net charge - offs to average loans CONSOLIDATED YEAR - END FINANCIALS

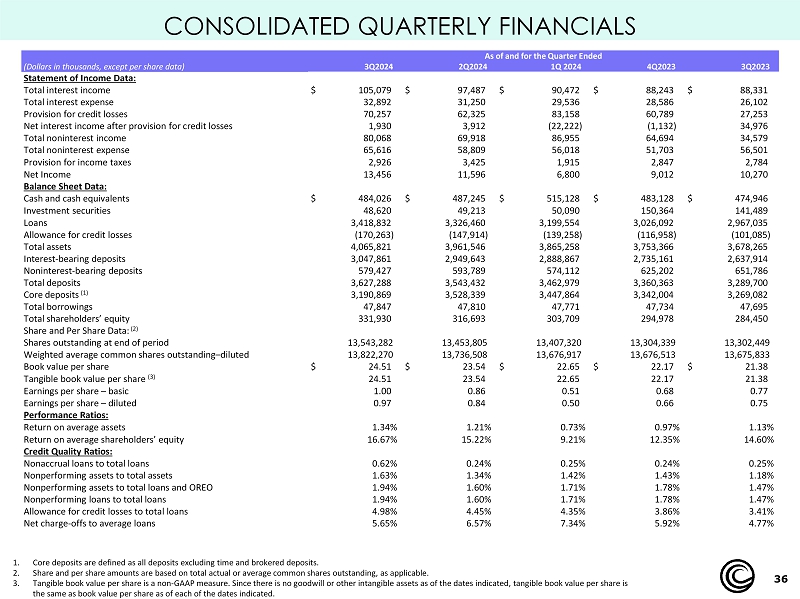

36 1. Core deposits are defined as all deposits excluding time and brokered deposits. 2. Share and per share amounts are based on total actual or average common shares outstanding, as applicable. 3. Tangible book value per share is a non - GAAP measure. Since there is no goodwill or other intangible assets as of the dates indic ated, tangible book value per share is the same as book value per share as of each of the dates indicated. As of and for the Quarter Ended 3Q2023 4Q2023 1Q 2024 2Q2024 3Q2024 (Dollars in thousands, except per share data) Statement of Income Data: $ 88,331 $ 88,243 $ 90,472 $ 97,487 $ 105,079 Total interest income 26,102 28,586 29,536 31,250 32,892 Total interest expense 27,253 60,789 83,158 62,325 70,257 Provision for credit losses 34,976 (1,132) (22,222) 3,912 1,930 Net interest income after provision for credit losses 34,579 64,694 86,955 69,918 80,068 Total noninterest income 56,501 51,703 56,018 58,809 65,616 Total noninterest expense 2,784 2,847 1,915 3,425 2,926 Provision for income taxes 10,270 9,012 6,800 11,596 13,456 Net Income Balance Sheet Data: $ 474,946 $ 483,128 $ 515,128 $ 487,245 $ 484,026 Cash and cash equivalents 141,489 150,364 50,090 49,213 48,620 Investment securities 2,967,035 3,026,092 3,199,554 3,326,460 3,418,832 Loans (101,085) (116,958) (139,258) (147,914) (170,263) Allowance for credit losses 3,678,265 3,753,366 3,865,258 3,961,546 4,065,821 Total assets 2,637,914 2,735,161 2,888,867 2,949,643 3,047,861 Interest - bearing deposits 651,786 625,202 574,112 593,789 579,427 Noninterest - bearing deposits 3,289,700 3,360,363 3,462,979 3,543,432 3,627,288 Total deposits 3,269,082 3,342,004 3,447,864 3,528,339 3,190,869 Core deposits (1) 47,695 47,734 47,771 47,810 47,847 Total borrowings 284,450 294,978 303,709 316,693 331,930 Total shareholders’ equity Share and Per Share Data: (2) 13,302,449 13,304,339 13,407,320 13,453,805 13,543,282 Shares outstanding at end of period 13,675,833 13,676,513 13,676,917 13,736,508 13,822,270 Weighted average common shares outstanding – diluted $ 21.38 $ 22.17 $ 22.65 $ 23.54 $ 24.51 Book value per share 21.38 22.17 22.65 23.54 24.51 Tangible book value per share (3) 0.77 0.68 0.51 0.86 1.00 Earnings per share – basic 0.75 0.66 0.50 0.84 0.97 Earnings per share – diluted Performance Ratios: 1.13% 0.97% 0.73% 1.21% 1.34% Return on average assets 14.60% 12.35% 9.21% 15.22% 16.67% Return on average shareholders’ equity Credit Quality Ratios: 0.25% 0.24% 0.25% 0.24% 0 .62 % Nonaccrual loans to total loans 1.18% 1.43% 1.42% 1.34% 1.63 % Nonperforming assets to total assets 1.47% 1.78% 1.71% 1.60% 1.94 % Nonperforming assets to total loans and OREO 1.47% 1.78% 1.71% 1.60% 1.94 % Nonperforming loans to total loans 3.41% 3.86% 4.35% 4.45% 4.98% Allowance for credit losses to total loans 4.77% 5.92% 7.34% 6.57% 5.65% Net charge - offs to average loans CONSOLIDATED QUARTERLY FINANCIALS

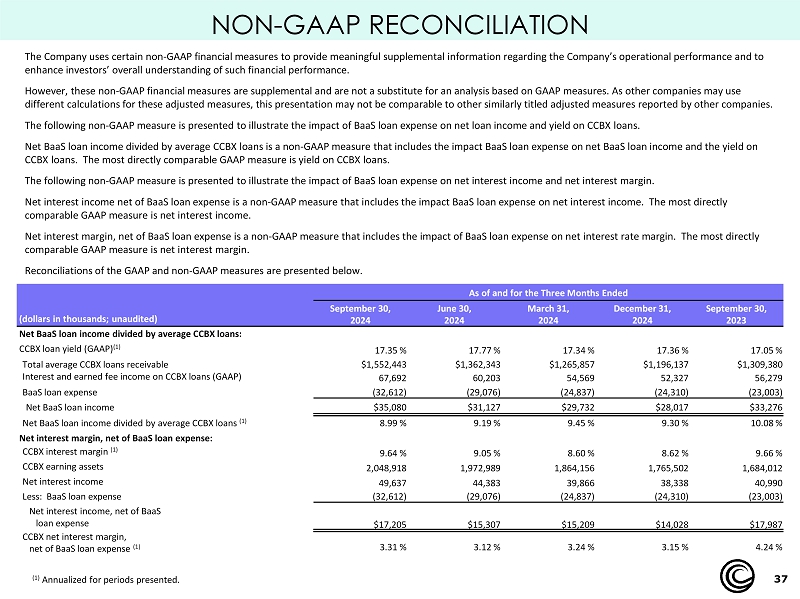

37 NON - GAAP RECONCILIATION As of and for the Three Months Ended September 30, 2023 December 31, 2024 March 31, 2024 June 30, 2024 September 30, 2024 (dollars in thousands; unaudited) Net BaaS loan income divided by average CCBX loans: 17.05 % 17.36 % 17.34 % 17.77 % 17.35 % CCBX loan yield (GAAP) (1) $ 1,309,380 $1,196,137 $1,265,857 $ 1,362,343 $1,552,443 Total average CCBX loans receivable 56,279 52,327 54,569 60,203 67,692 Interest and earned fee income on CCBX loans (GAAP) (23,003 ) (24,310) (24,837) (29,076 ) ( 32,612) BaaS loan expense $33,276 $28,017 $29,732 $31,127 $ 35,080 Net BaaS loan income 10.08 % 9.30 % 9.45 % 9.19 % 8.99 % Net BaaS loan income divided by average CCBX loans (1) Net interest margin, net of BaaS loan expense: 9.66 % 8.62 % 8.60 % 9.05 % 9.64 % CCBX interest margin (1) 1,684,012 1,765,502 1,864,156 1,972,989 2,048,918 CCBX earning assets 40,990 38,338 39,866 44,383 49,637 Net interest income (23,003) (24,310) (24,837) (29,076) (32,612) Less: BaaS loan expense $17,987 $14,028 $15,209 $15,307 $17,205 Net interest income, net of BaaS loan expense 4.24 % 3.15 % 3.24 % 3.12 % 3.31 % CCBX net interest margin, net of BaaS loan expense (1) (1) Annualized for periods presented. The Company uses certain non - GAAP financial measures to provide meaningful supplemental information regarding the Company’s oper ational performance and to enhance investors’ overall understanding of such financial performance. However, these non - GAAP financial measures are supplemental and are not a substitute for an analysis based on GAAP measures. As other companies may use different calculations for these adjusted measures, this presentation may not be comparable to other similarly titled adjuste d m easures reported by other companies. The following non - GAAP measure is presented to illustrate the impact of BaaS loan expense on net loan income and yield on CCBX l oans. Net BaaS loan income divided by average CCBX loans is a non - GAAP measure that includes the impact BaaS loan expense on net BaaS loan income and the yield on CCBX loans. The most directly comparable GAAP measure is yield on CCBX loans. The following non - GAAP measure is presented to illustrate the impact of BaaS loan expense on net interest income and net interes t margin. Net interest income net of BaaS loan expense is a non - GAAP measure that includes the impact BaaS loan expense on net interest in come. The most directly comparable GAAP measure is net interest income. Net interest margin, net of BaaS loan expense is a non - GAAP measure that includes the impact of BaaS loan expense on net interes t rate margin. The most directly comparable GAAP measure is net interest margin. Reconciliations of the GAAP and non - GAAP measures are presented below.

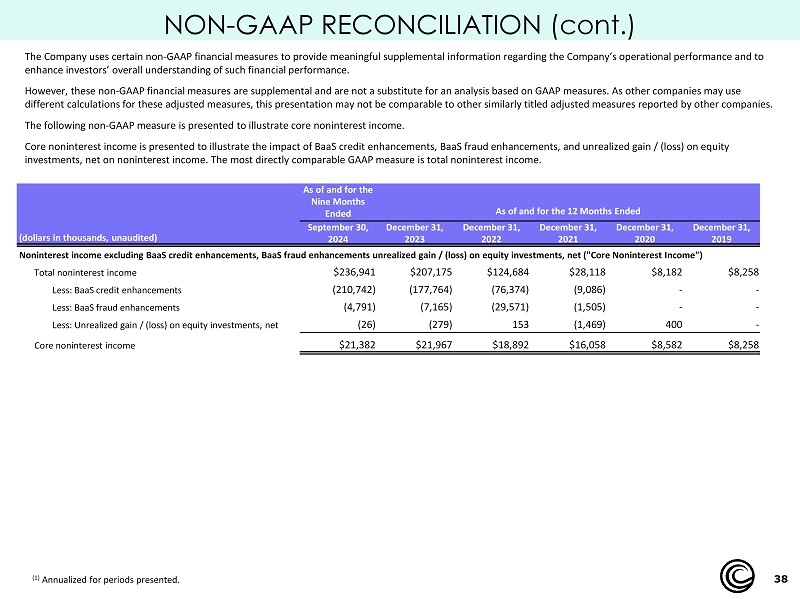

38 NON - GAAP RECONCILIATION (cont.) (1) Annualized for periods presented. The Company uses certain non - GAAP financial measures to provide meaningful supplemental information regarding the Company’s oper ational performance and to enhance investors’ overall understanding of such financial performance. However, these non - GAAP financial measures are supplemental and are not a substitute for an analysis based on GAAP measures. As other companies may use different calculations for these adjusted measures, this presentation may not be comparable to other similarly titled adjuste d m easures reported by other companies. The following non - GAAP measure is presented to illustrate core noninterest income . Core noninterest income is presented to illustrate the impact of BaaS credit enhancements, BaaS fraud enhancements, and unrealized gain / (loss) on equity investments, net on noninterest income. The most directly comparable GAAP measure is total noninterest income. As of and for the 12 Months Ended As of and for the Nine Months Ended December 31, 2019 December 31, 2020 December 31, 2021 December 31, 2022 December 3 1 , 202 3 September 30, 2024 (dollars in thousands, unaudited) Noninterest income excluding BaaS credit enhancements, BaaS fraud enhancements unrealized gain / (loss) on equity investments, net ("Core Noninterest Income ") $8,258 $8,182 $28,118 $124,684 $207,175 $236,941 Total noninterest income - - (9,086) (76,374) (177,764) ( 210,742 ) Less: BaaS credit enhancements - - (1,505) (29,571) (7,165) ( 4,791 ) Less: BaaS fraud enhancements - 400 (1,469) 153 (279) ( 26 ) Less : Unrealized gain / (loss) on equity investments, net $8,258 $8,582 $16,058 $18,892 $21,967 $21,382 Core noninterest income

39 BOARD OF DIRECTORS Christopher D. Adams, Chairman of the Board Christopher D. Adams is a partner in the law firm of Adams & Duncan, Inc., P.S. in Everett, Washington. Mr. Adams practices i n t he areas of corporate law, commercial real estate and tax matters. He graduated from the University of Washington with a bachelor’s degree in business and received his J.D. and M.B.A. from Gonzag a U niversity. Mr. Adams also holds a Masters in Tax Law from the University of Washington School of Law. Mr. Adams brings to the board of directors legal expertise and familiarity with our m ark et area. Mr. Adams has been a member of our board of directors since 2016. Steven Donald Hovde , Vice Chairman of the Board Steven D. Hovde is the Chairman and Chief Executive Officer at Hovde Group, LLC, an investment banking and advisory firm that serves bank and thrift clients across the United States, where he is responsible for managing its investment banking activities, the strategic development of mergers and acquisitions of bank and th rift institutions, and its private equity activities. He serves as a director of H Bancorp and as a trustee of several charitable foundations. Before co - founding Hovde Group in 1987, Mr. Hovde was Regional General Counsel and Vice President of a national commercial real estate development firm. Previous to that, Mr. Hovde served as an attorney with, Rudnick & Wolfe, which is today DLA Piper, specializing in real estate law. Prior to that, Mr. Hovde practiced accounting in Chicago as a Certified Public Accountant with Touche Ross LLP, which is today Deloitte & Touche LLP. Mr. Hovde graduated summa cum laude with a Bachelor of Business Administration, majoring in Accounting, from the School of Business at the University of Wisconsin, Madison. He also earned h is law degree, cum laude, at Northwestern University. Mr. Hovde provides the board of directors with important experience and insight into the financial services industry. Mr. Hovde has been a member of our board of directors since 2011. Eric M. Sprink , CEO & Board Director Eric M. Sprink serves as our Chief Executive Officer. Mr. Sprink joined the Company in late 2006 as President and Chief Operating Officer and became Chief Executive Officer in 2010. Mr. Sprink began his banking career working for Security Pacific Bank while enrolled at Arizona State University. He assumed increasing lev els of responsibility in the areas of retail operations, consumer and commercial lending and wealth management with Security Pacific Bank and its successor, Bank of America. He then moved to Centura Bank, where he held management positions in retail operations and corporate finance. After Centura Bank was acquired, he held senior management positions at Washington Trust Bank and Global Credit Union. Mr. Sprink is active in industry trade groups and is a director and past chairman of the Community Bankers of Washington. Mr. Sprink received a bachelor’s degree from Arizona State University and an M.B.A. from the University of North Carolina. Mr. Sprink brings to our board of directors leadership experience, significant experience in many facets of the financial services busin es s, and familiarity with our market area. Mr. Sprink has been a member of our board of directors since 2006. Sadhana Akella - Mishra, Board Director Sadhana Akella - Mishra has served as the Chief Information Security and Compliance Officer for Finxact , Inc., a core banking software company, since July 2018. From May 2018 to June 2018, Ms. Akella - Mishra was the Chief Compliance Officer for Sunlight Payments (now Purposeful), an electronic payments company. Prior to that t ime, Ms. Akella - Mishra served as the Chief Compliance Officer (Global) of Geoswift Ltd. from June 2017 to April 2018 and as the U.S. Head of Compliance for Geoswift US Inc. from N ove mber 2016 to June 2017. From April 2016 to November 2016, Ms. Akella - Mishra served as the Senior Manager, General Compliance of Ripple, Inc. Prior to that time, she served as the Chief Complianc e Officer of Zenbanx Holding Ltd. from March 2014 to April 2016 and as a Senior Compliance Manager for Zenbanx Holding Ltd. from August 2013 to February 2014. From July 2007 to July 2013, Ms. Akella - Mishra served in various positions with Deutsche Bank, including as Americas Regional Head, Anti Financial Crime - Fraud from September 2012 to July 2013. Ms. Akella - Mishra brings to the Board of Directors compliance and information security expertise and familiarity with the financial services industry. Rilla Delorier , Board Director Rilla Delorier is an experienced C - suite leader with more than 30 years of executive experience and has served in a range of capacities includ ing managing the P&L of a $2.7 billion retail banking business, Chief Strategy and Digital Transformation Officer, Chief Marketing Officer, healthcare business leader, and strateg y c onsulting with Bain & Co. A graduate of the University of Virginia, with an MBA from Harvard, Delorier lead innovation initiatives at Umpqua Bank and SunTrust Bank and is a sought - after speaker on leadership, purpose, innovation, and business transformation. Delorier’s experience in developing new products, automating operations, implementing enhanced cyber - security practices, establishing stra tegic partnerships, and modernized use of analytics will help advise Coastal as it navigates within the highly regulated and ever - changing banking environment.

40 BOARD OF DIRECTORS Thomas D. Lane, Board Director Thomas D. Lane is the owner and president and chief executive officer of Dwayne Lane’s Auto Family, which operates six automo bil e dealerships. He is active in community organizations and currently serves on the Economic Alliance Snohomish County board of trustees. Mr. Lane graduated from Western Washington Univ ers ity with a bachelor’s degree in business administration. Mr. Lane brings to the board of directors leadership experience and familiarity with our market area. Mr. Lane has been a member of our board of directors since the Bank’s formation in 1997. Stephan Klee, Board Director Stephan Klee is the Chief Financial Officer at Portag3 Ventures, which makes investments in innovative financial services com pan ies. Prior to joining Portag3, Mr. Klee served as Chief Financial Officer of Zenbanx Holding, Inc. and remained in an executive capacity after its merger with SoFi, Inc., one of the largest U.S. fintech compani es . Previously, Mr. Klee served as a Senior Vice President at Bank of Nova Scotia, at ING Direct Canada, where he was CFO and Treasurer from 2011 to 2014, and at ING Direct USA, where he ser ved as Chief of Staff from 2002 to 2011. He began his career at Deutsche Bank in Germany. Mr. Klee attended the University of Applied Sciences in Germany before earning an MBA at the Ivey B usi ness School. He is also an AMP graduate from Harvard Business School. Mr. Klee adds his expertise in emerging technologies and digital banking to the company’s board, bringing a new persp ect ive as banking and customer access to banking services continues to evolve. He joined our board of directors in July 2018. Gregory A. Tisdel , Board Director Gregory A. Tisdel is the owner of Tiz’s Door Sales, Inc. and a member of the City of Everett Planning Commission. He serves on the Advisory Board of the Puget Sound Cl ean Air Agency and is past Special Advisor to the Economic Alliance Snohomish County. Mr. Tisdel is an active supporter of social, civic and cultural programs and was honored with the 2008 Henry M. Jackson Citizen of the Year Award. Mr. Tisdel has been active in community organization, including the YMCA, American Red Cross Snohomish County Chapter and Volunteers of Am erica. Mr. Tisdel brings to the board of directors leadership experience and familiarity with our market area. Mr. Tisdel has been a member of our board of directors since 2002. Pamela Unger, Board Director Pamela Unger is a Certified Public Accountant who supports venture capital funds with tax planning, compliance, and related i nve stor issues and inquiries. She is currently the Managing Director and was previously the Tax Director at Belltower Fund Group, Ltd the Seattle based fund administrator for over 4,000 venture capi tal funds launched on the AngelList Venture platform. She has been employed with Belltower since January 2019. From September 2007 to January 2019, Ms. Unger held various positions at PwC, a n etw ork of accounting firms. While at PWC she worked in the broader asset management sector handling taxes for a variety of clients within the industry, with a focus on venture capital, pr ivate equity, and heavy experience related to foreign investing inbound and outbound compliance. Ms. Unger graduated from the University of Washington with a bachelor's degree in business, and a ma ste rs in tax. She brings to the Board of Directors financial expertise and familiarity with the financial services industry. Brian Hamilton, Board Director Mr. Hamilton is a seasoned financial technology executive and business leader, with more than 25 years of experience in the b ank ing, lending, payments, and digital product development industries. A serial entrepreneur, with deep expertise in domestic and international settlement systems and digital platforms, Mr. Hamilt on has held senior leadership roles at Capital One, serving as President of their Merchant Services division, Wells Fargo, and Verifone, in addition to founding and operating multiple companies in t he fintech space. Most recently Mr. Hamilton was co - founder and CEO of ONE (One Finance Inc.), which was acquired by a Walmart - led joint venture in 2022. Prior to co - founding ONE, he was the founder of Azlo , a digital bank for small businesses, and helped to build out the BBVA Open Platform for sponsor banking services. Michael Patterson, Board Director Michael Patterson is a seasoned global business leader with more than 38 years of cross - sector experience in strategy, P&L manag ement, and international operations with deep expertise in risk management, compliance, governance, and financial control. A graduate of Pace University, he led EY LLP’s Compliance Risk Man age ment business in the firm’s Financial Services Office and was appointed to the role at the height of the 2008 crisis. Before that he served as the First VP of the Risk and Control functio n i n the institutional business for Merrill Lynch & Co and served several leadership roles at other leading consulting firms.

Grafico Azioni Coastal Financial (NASDAQ:CCB)

Storico

Da Mar 2025 a Apr 2025

Grafico Azioni Coastal Financial (NASDAQ:CCB)

Storico

Da Apr 2024 a Apr 2025