false

2024

FY

0001709628

0001709628

2024-01-01

2024-12-31

0001709628

2024-06-30

0001709628

us-gaap:CommonClassAMember

2025-03-26

0001709628

us-gaap:CommonClassBMember

2025-03-26

0001709628

2024-12-31

0001709628

2023-12-31

0001709628

us-gaap:CommonClassAMember

2024-12-31

0001709628

us-gaap:CommonClassAMember

2023-12-31

0001709628

us-gaap:CommonClassBMember

2024-12-31

0001709628

us-gaap:CommonClassBMember

2023-12-31

0001709628

2023-01-01

2023-12-31

0001709628

us-gaap:CommonClassAMember

2024-01-01

2024-12-31

0001709628

us-gaap:CommonClassBMember

2024-01-01

2024-12-31

0001709628

us-gaap:CommonClassAMember

2023-01-01

2023-12-31

0001709628

us-gaap:CommonClassBMember

2023-01-01

2023-12-31

0001709628

CSAI:ClassACommonStockMember

2022-12-31

0001709628

CSAI:ClassBCommonStockMember

2022-12-31

0001709628

us-gaap:AdditionalPaidInCapitalMember

2022-12-31

0001709628

us-gaap:RetainedEarningsMember

2022-12-31

0001709628

2022-12-31

0001709628

CSAI:ClassACommonStockMember

2023-12-31

0001709628

CSAI:ClassBCommonStockMember

2023-12-31

0001709628

us-gaap:AdditionalPaidInCapitalMember

2023-12-31

0001709628

us-gaap:RetainedEarningsMember

2023-12-31

0001709628

CSAI:ClassACommonStockMember

2023-01-01

2023-12-31

0001709628

CSAI:ClassBCommonStockMember

2023-01-01

2023-12-31

0001709628

us-gaap:AdditionalPaidInCapitalMember

2023-01-01

2023-12-31

0001709628

us-gaap:RetainedEarningsMember

2023-01-01

2023-12-31

0001709628

CSAI:ClassACommonStockMember

2024-01-01

2024-12-31

0001709628

CSAI:ClassBCommonStockMember

2024-01-01

2024-12-31

0001709628

us-gaap:AdditionalPaidInCapitalMember

2024-01-01

2024-12-31

0001709628

us-gaap:RetainedEarningsMember

2024-01-01

2024-12-31

0001709628

CSAI:ClassACommonStockMember

2024-12-31

0001709628

CSAI:ClassBCommonStockMember

2024-12-31

0001709628

us-gaap:AdditionalPaidInCapitalMember

2024-12-31

0001709628

us-gaap:RetainedEarningsMember

2024-12-31

0001709628

2024-10-23

2024-10-24

0001709628

CSAI:VisionfulAndInfrastructureProvingGroundsMember

2023-01-01

2023-12-31

0001709628

CSAI:RegulationAFilingMember

2024-12-31

0001709628

CSAI:Price450Member

2022-12-31

0001709628

CSAI:Price720Member

2022-12-31

0001709628

CSAI:Price900Member

2022-12-31

0001709628

CSAI:Price450Member

2023-01-01

2023-12-31

0001709628

CSAI:Price720Member

2023-01-01

2023-12-31

0001709628

CSAI:Price900Member

2023-01-01

2023-12-31

0001709628

CSAI:Price450Member

2023-12-31

0001709628

CSAI:Price720Member

2023-12-31

0001709628

CSAI:Price900Member

2023-12-31

0001709628

CSAI:Price450Member

2024-01-01

2024-12-31

0001709628

CSAI:Price720Member

2024-01-01

2024-12-31

0001709628

CSAI:Price900Member

2024-01-01

2024-12-31

0001709628

CSAI:Price450Member

2024-12-31

0001709628

CSAI:Price720Member

2024-12-31

0001709628

CSAI:Price900Member

2024-12-31

0001709628

CSAI:BentleyMember

2020-02-19

2020-02-20

0001709628

CSAI:BentleyMember

2020-02-20

0001709628

CSAI:BentleyMember

2024-12-31

0001709628

2023-12-30

2024-01-02

0001709628

CSAI:SurveillanceSegmentMember

us-gaap:OperatingSegmentsMember

2024-01-01

2024-12-31

0001709628

CSAI:SurveillanceSegmentMember

us-gaap:OperatingSegmentsMember

2023-01-01

2023-12-31

0001709628

2024-10-01

2024-12-31

iso4217:USD

xbrli:shares

iso4217:USD

xbrli:shares

xbrli:pure

Table of Contents

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, DC 20549

________________________

FORM 10-K

________________________

| ☒ |

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 FOR THE FISCAL YEAR ENDED December 31, 2024 |

| |

|

| ☐ |

TRANSITION REPORT PURSUANT

TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 FOR THE TRANSITION PERIOD FROM _____________ TO ____________ |

| Commission file number 001-42494 |

| ________________________ |

| Cloudastructure, Inc. |

| (Exact name of registrant as specified in its charter) |

| ________________________ |

| Delaware |

87-0690564 |

(State or other jurisdiction of

incorporation or organization) |

(I.R.S. Employer Identification No.) |

228 Hamilton Avenue, 3rd Floor

Palo Alto, California 94301 |

| (Address of principal executive offices) |

| (650) 644-4160 |

| (Registrant’s telephone number, including area code) |

| Securities registered pursuant to Section 12(b) of the Act: |

| |

| Title of each class |

|

Trading Symbol |

|

Name of each exchange on which registered |

| Class A common stock |

|

CSAI |

|

Nasdaq Capital Market |

| |

|

|

|

|

| Securities registered pursuant to section 12(g) of the Act: None |

| Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. |

Yes ☐ |

No ☒ |

| |

|

|

| Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. |

Yes ☐ |

No ☒ |

| |

|

|

| Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. |

Yes ☒ |

No ☐ |

| |

|

|

| Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). |

Yes ☒ |

No ☐ |

| |

|

|

| Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act. |

| Large accelerated filer |

☐ |

|

Accelerated filer |

☐ |

| Non-accelerated filer |

☒ |

|

Smaller reporting company |

☒ |

| |

|

|

Emerging growth company |

☒ |

| If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. |

|

| |

|

| Indicate by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report. |

☐ |

| |

|

| If securities are registered pursuant to Section 12(b) of the Act, indicate by check mark whether the financial statements of the registrant included in the filing reflect the correction of an error to previously issued financial statements. |

☐ |

| |

|

| Indicate by check mark whether any of those error corrections are restatements that required a recovery analysis of incentive-based compensation received by any of the registrant’s executive officers during the relevant recovery period pursuant to §240.10D-1(b). |

☐ |

| |

|

| Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). |

Yes ☐ |

No ☒ |

| |

|

|

The registrant finalized its direct listing on the Nasdaq Capital Market

on January 30, 2025, accordingly, as of June 30, 2024, there was no public trading market for the registrant’s Class A common stock.

As of March 26, 2025 the registrant had 15,423,725 shares of Class

A common stock, and 487,677 shares of Class B common stock outstanding.

DOCUMENTS INCORPORATED BY REFERENCE

None.

TABLE OF CONTENTS

CAUTIONARY

NOTE REGARDING FORWARD-LOOKING STATEMENTS

This Annual Report on Form 10-K (this “Form 10-K”) contains

forward-looking statements that can involve substantial risks and uncertainties. All statements other than statements of historical facts

contained in this Form 10-K, including statements regarding our future results of operations and financial position, business plan and

strategy, future revenue, timing and likelihood of success, plans and objectives of management for future operations, future results of

anticipated products and prospects, plans and objectives of management are forward-looking statements. These statements involve known

and unknown risks, uncertainties and other important factors that may cause our actual results, performance or achievements to be materially

different from any future results, performance or achievements expressed or implied by the forward-looking statements.

In some cases, you can identify forward-looking statements by terms

such as “anticipate,” “believe,” “can,” “contemplate,” “continue,” “could,”

“estimate,” “expect,” “future”, “goal,” “intend,” “may,” “outlook,”

“plan,” “potential,” “predict,” “project,” “should,” “target,”

“will,” or “would” or the negative of these terms or other similar expressions, although not all forward-looking

statements contain these words. Forward-looking statements contained in this Form 10-K include, but are not limited to, statements about:

| · | the implementation of our business model and our strategic plans for our

business, product, services and technology; |

| · | our commercialization and marketing capabilities and strategy; |

| · | our ability to establish or maintain collaborations or strategic relationships

or obtain additional funding; |

| · | our competitive position; |

| · | the scope of protection that we able to establish and maintain for intellectual

property rights covering our products, services and technology; |

| · | developments and projections relating to our competitors and our industry; |

| · | our estimates regarding expenses, future revenue, capital requirements and

needs for additional financing; |

| · | the period over which we estimate our existing cash and cash equivalents

will be sufficient to fund our future operating expenses and capital expenditure requirements; and |

| · | the impact of new or existing laws and regulations on our business and strategy. |

We have based these forward-looking statements

largely on our current expectations and projections about our business, the industry in which we operate and financial trends that we

believe may affect our business, financial condition, results of operations and prospects, and these forward-looking statements are not

guarantees of future performance or development. In addition, statements that “we believe” and similar statements reflect

our beliefs and opinions on the relevant subject. These statements are based upon information available to us as of the date of this Form

10-K, and while we believe such information forms a reasonable basis for such statements, such information may be limited or incomplete,

and our statements should not be read to indicate that we have conducted an exhaustive inquiry into, or review of, all potentially available

relevant information. These statements are inherently uncertain and you are cautioned not to unduly rely upon these statements. Except

as required by applicable law, we do not plan to publicly update or revise any forward-looking statements contained herein until after

we distribute this Form 10-K, whether as a result of any new information, future events or otherwise.

There are a number of risks, uncertainties and

other important factors that could cause our actual results to differ materially from the forward-looking statements contained in this

Form 10-K, including, among others, the risks set forth in Item 1A. “Risk Factors” and Item 7. “Management’s Discussion

and Analysis of Financial Condition and Results of Operations,” as well as from time to time in our other filings with the U.S.

Securities and Exchange Commission (“SEC”). A non-exhaustive summary of principal risk factors that make investing in our

securities risky and may cause actual results to differ materially are set forth below:

| · | Our technology continues to be developed, and it is unlikely that we will

ever develop our technology to a point at which no further development is required; |

| · | If our security measures are breached or unauthorized access to individually

identifiable biometric or other personally identifiable information is otherwise obtained, our reputation may be harmed, and we may incur

significant liabilities; |

| · | Our collection, processing, use and disclosure of individually identifiable

biometric or other personally identifiable information is subject to evolving and expanding privacy and security regulations; |

| · | Our success is highly dependent on our ability to attract and retain highly

skilled executive officers and employees; |

| · | Privacy and data security laws and regulations could require us to make changes

to our business, impose additional costs on us and reduce the demand for our software solutions; |

| · | Privacy and data security laws and regulations could require us to make changes

to our business, impose additional costs on us and reduce the demand for our software solutions; |

| · | Issues raised by the use of artificial intelligence (including machine learning)

in our platforms may result in reputational harm or liability or affect our ability to operate profitably and sustainably; |

| · | We operate in a highly competitive industry that is dominated by multiple

very large, well-capitalized market leaders and is constantly evolving; |

| · | Successful infringement claims against us could result in significant monetary

liability or prevent us from selling some of our products; |

| · | We rely on other companies to provide certain hardware and software solutions

for our products; |

| · | We will incur increased costs as a result of operating as a public company,

and our management will be required to devote substantial time to new compliance initiatives; |

| · | Intellectual property rights do not necessarily address all potential threats

to our competitive advantage; |

| · | We have a limited operating history, which may make it difficult for you

to evaluate our current business and predict our future success and viability; |

| · | We have historically operated at a loss, which has resulted in an accumulated

deficit; |

| · | We anticipate sustaining operating losses for the foreseeable future; |

| · | We will require substantial additional capital to finance our operations; |

| · | Raising additional capital may cause dilution to our existing stockholders; |

| · | We have a substantial customer concentration, with a limited number of customers

accounting for a substantial portion of our revenue; |

| · | An active trading market for our Class A common stock may not be sustained,

and the market price of shares of our Class A common stock may be volatile; |

| · | Reports published by analysts, including projections in those reports that

differ from our actual results, could adversely affect the price and trading volume of our Class A common stock; |

| · | Our internal computer systems, or those of any of our manufacturers, contractors,

consultants, collaborators or potential future collaborators, may fail or suffer security or data privacy breaches or other unauthorized

or improper access to, use of, or destruction of our proprietary or confidential data, employee data or personal data, which could result

in additional costs, loss of revenue, significant liabilities, harm to our brand and material disruption of our operations; and |

| · | Our operations are vulnerable to interruption by fire, severe weather conditions,

power loss, telecommunications failure, terrorist activity, pandemics/epidemics and other events beyond our control, which could harm

our business. |

PART I

Item 1. Business.

Overview

Cloudastructure, Inc. (“Cloudastructure,”

“we,” “us,” “our” or the “Company”) was formed under the laws of the State of Delaware

on March 28, 2003. We provide an award-winning cloud-based artificial intelligence (“AI”) video surveillance and Remote Guarding

(as described below) service built on AI and machine learning platforms.

We operated as a small Silicon Valley startup until

early 2021 when we raised over $35 million in funding under Regulation A of the Securities Act of 1933, as amended (the “Securities

Act”). With these funds we quickly built a sales, marketing and support structure and achieved a degree of early success in the

property management space. As of the date of this Form 10-K, we have contracts in place with five of the top 10 property management companies

on the National Multifamily Housing Council’s (“NMHC’s”) 2024 NMHC’s top 50 list (Greystar Real Estate Partners,

Avenue5 Residential, LLC, Cushman & Wakefield, BH Management Services, LLC and FPI Management, Inc.). Our cloud-based solutions allow

our customers to provide real-time safety and security solutions for their properties, as well as easily manage security across all of

their locations. As of the date of this Form 10-K, we are focused on expanding into more of our existing top tier customer locations,

acquiring additional customers in the property management (“proptech”) space, and we anticipate entering into additional markets

in 2025.

Our intelligent AI solution works by identifying

objects (faces, license plates, animals, guns, etc.) in video footage so that property managers can quickly search for those objects.

Additionally, our AI and Remote Guarding services provide a proactive response to crime. Remote guarding combines video surveillance,

AI analytics, monitoring centers, and security agents (“Remote Guarding”). Based on internal data comparing the total number

of actual threatening activity alerts received by our Remote Guards, against all potentially suspicious and threatening activity alerts

received by our Remote Guards, on average, from 2023 to the date of this Form 10-K, our Remote Guarding services deterred over 97% of

all threatening activity for our customers. We believe AI security delivers multiple benefits for many property owners, including, without

limitation:

| · | Deterring crime and improving overall safety; |

| · | Improving occupancy rates and rental rates; and |

| · | Reducing onsite guard costs and lowering insurance rates |

As of the date of this Form 10-K, we are the only

seamless, cloud-based, AI surveillance and Remote Guarding solution on the market of which we are aware. We also believe that our solution

is more affordable and easier to use than the various solutions that our competitors offer. Our Remote Guarding service bridges the line

between AI and human intelligence. AI has the ability to monitor all cameras at the same time and all of the time, a task from which humans

would fatigue. When the AI detects an event occurring, the Remote Guards are notified. The Remote Guards can then determine if escalation

is required. With real-time human intervention, our Remote Guarding service turns video surveillance from a forensic tool, used after

a crime has been committed, into a real time crime prevention tool. This has the potential to greatly increase value for our customers.

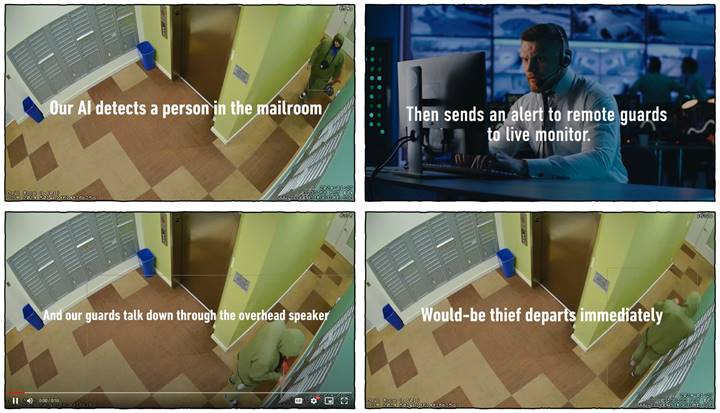

The Remote Guards follow a series of protocols

which may include announcing through a networked speaker “YOU ARE ON VIDEO SURVEILLANCE WITH A LIVE AGENT AND ARE BEING WATCHED

AND RECORDED!”. These “talk downs” are so effective that we have found that we rarely have to escalate to law enforcement.

History

and Development of the Company

In 2003, a laptop was stolen from our founder Rick

Bentley’s office. He went to the landlord to get the surveillance footage, only to discover a cleaning lady had unplugged the surveillance

system to plug in a vacuum cleaner. Dubbing the unsolved theft “The Vacuum Effect,” Rick decided surveillance footage needed

to go to the cloud. Our CTO Gregory Rayzman shared this vision for a secure, scalable suite of cloud-based video surveillance, storage,

analytics, and monitoring.

Google’s release of Tensorflow, a free and

open-source software library for machine learning and artificial intelligence, in 2015 added computer vision, AI, and machine learning

to Bentley’s and Rayzman’s vision. Rayzman hand-selected talented engineers in Silicon Valley in the fields of AI, machine

learning and user interface, and designed the Cloudastructure platform to scale, and in 2021, the Company raised funding under Regulation

A to hire a marketing, sales and implementation team.

Over twenty years later legacy, on-premises video

surveillance systems like the system that inspired our founding remain the industry standard. As a result, we believe there is an enormous

opportunity to bring innovation and new technology to the field of video surveillance security and eliminate many of the weaknesses of

today’s standard surveillance systems.

Overview of our Business and Operations

Our solutions centralize the management of video

surveillance in a collection of servers that host our software and infrastructure and can be accessed over the internet (the “Cloud”).

Our Cloud-based model allows customers to scale geographically over multiple locations without complicated or potentially insecure network

architectures.

We offer our services and support for a monthly

subscription fee, requiring no upfront licensing costs or large capital expenditure budgets. We believe that as we add additional AI capabilities,

that we will be able to increase pricing power for our Cloud-based solution.

Our Existing Products and Services

Set forth in the table below is a summary of our

existing products and services, their key features and the current target markets that they serve:

| Product / Service |

Description and Key Features |

Cloud Service:

Cloud Video Surveillance |

Video surveillance stored in the Cloud with AI Computer Vision built on Machine Learning. Key features include: Secure offsite Cloud storage. AI Computer Vision including face recognition, license plate reading, object detection and more. Multiplatform (e.g., web, phone, tablet) browser-based access. |

Cloud Service:

Remote Guarding |

Browser based Remote Guard call center software, allowing guards to work from any location or time zone. Key features include: customized AI alerts, real time Live View, other AI functions and more. |

Guard Service:

Remote Guards |

Our in-house live agents monitor incoming alerts from the AI, talk down to people onsite through networked speakers, and provide real time notifications to customers or authorities in response to any dangerous or suspicious activity. Customers can use their own guards if desired. |

Product:

Cloud Video Recorder (CVR) |

Our Cloud Video Recorder (“CVR”) is an internet of things (“IoT”) device that securely collects video from cameras and transmits it to our Cloud. The CVR is compatible with most existing or new cameras and stores data even if not connected to the internet. |

Product:

Cameras and Speakers |

We resell networked, IP-based, cameras and speakers. |

New Product:

Mobile Surveillance Trailer |

Our Mobile Surveillance Trailer solution is a solar and battery powered video surveillance tower with wireless broadband that connects to our Cloud Video Surveillance and Remote Guarding services. |

Select High-Level Product and Service Features

Select high-level features currently available

with some of our products and services include:

Tagger

Our Tagger technology generates tags for every

object it can identify in a surveillance video. For example, “animal” or “person” or “vehicle.” Enabling

our customer search surveillance videos by tag. For example, a customer can search by “person” and see only surveillance

videos with people in them.

License Plate Reading

Our License Plate Reading technology reads license

plates and then we can search surveillance videos for those license plates.

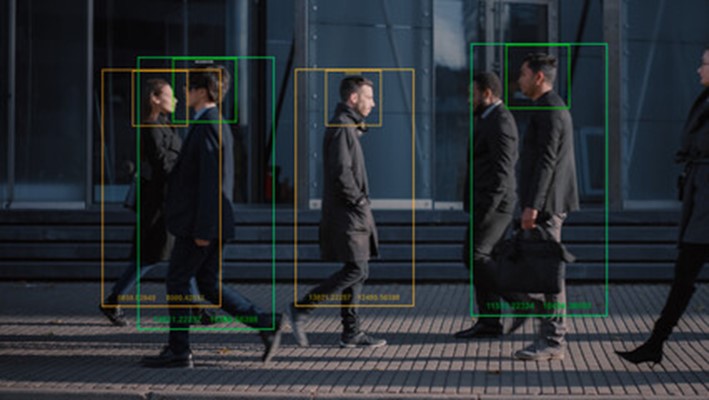

Facial Recognition

Our premium feature Facial Recognition technology

detects faces and then recognizes those faces. Customers can search for a known person in a database of faces (e.g., conducting

a search for an employee named John Doe) or unknown person tagged by the system (e.g., Unknown123). Our system also employs “supervised

learning” technologies, which allows our team and the end users to provide feedback on the face recognition. For example, the system

can be taught “that’s not Dave, that’s John”, improving accuracy significantly over less advanced systems.

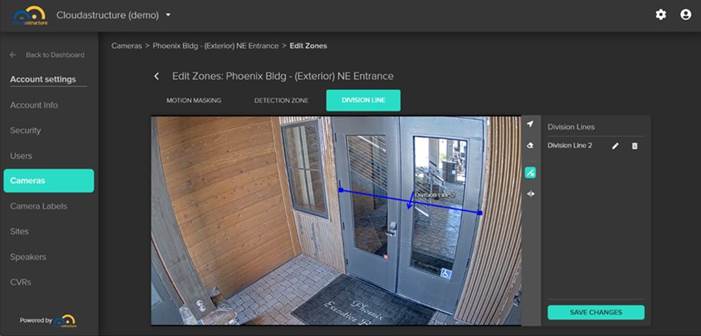

Line Crossing

Our Line Crossing technology can “draw”

a virtual line across a camera’s field of view, or a zone around any area (e.g. a door) where a customer wants access restricted.

This restriction can be set for specific time periods such as after hours. If the line is crossed or the zone is entered, an alert will

be sent to the user and/or remote guards. The technology also possesses directional awareness, so for example, if a customer wishes to

only receive an alert when someone enters the pool or enters a parking garage afterhours, they can customize and reduce the number of

alerts they receive.

Remote Guarding

Our cloud-based Remote Guarding solution is seamlessly

integrated with our AI surveillance system to make remote guarding more efficient and effective.

| · | Our AI monitors all of the cameras all of the time. |

| · | We are at the forefront of AI and human intelligence, but recognize when

humans should be involved. |

| · | When the AI detects an event requiring human intervention, the Remote Guards

are notified. |

| · | Our Remote Guard solution can then verify if there is an issue and escalate

as appropriate, for example: |

| o | Our AI monitors all of the cameras all of the time. |

o

| o | We are at the forefront of AI and human intelligence, but recognize when humans should be involved. |

| o | When the AI detects an event requiring human intervention, the Remote Guards are notified. |

| o | Our Remote Guard solution can then verify if there is an issue and escalate as appropriate, for example: |

| • | Our AI monitors all of the cameras all of the time. |

| • | We are at the forefront of AI and human intelligence, but recognize when

humans should be involved. |

| • | When the AI detects an event requiring human intervention, the Remote Guards

are notified. |

| • | Our Remote Guard solution can then verify if there is an issue and escalate

as appropriate, for example: |

| § | Communicating to anyone on site through our system’s speakers; |

| § | Escalating the response to customer onsite personnel, if warranted; and |

| § | Calling for emergencies services when required. |

Based on internal data comparing the total number

of actual threatening activity alerts received by our Remote Guards, against all potentially suspicious and threatening activity alerts

received by our Remote Guards, on average, from 2023 to the date of this Form 10-K, our Remote Guarding services deterred over 97% of

all threatening activity for our customers.

Other

Specialized Features

Our products and services employ advanced technology,

such as:

| · | AI and machine learning to simultaneously decrease false positives and false

negatives, improving overall accuracy; |

| · | Lower light, lower contrast and lower resolution computer vision abilities; |

| · | persistent computer vision, whereby previous and future frames provide context

for the analysis of the current frame; |

| · | Increased granularity in search sensitivity on a per object basis; and |

| · | Reducing latency for real time operation like alerts for our Remote Guarding

services. |

Our Product and Service Installation and Delivery Processes

Our typical product and service installation and

delivery process is as follows:

First, we install our custom, on-premises CVR,

which is configured to work with a customer’s existing video surveillance cameras, is network secure, and simply requires a power

source and ethernet connection. The CVR replaces any NVR’s (Network Video Recorder) or other recording devices.

Our CVR then sends all motion viewed by a customer’s

surveillance cameras to our Cloud-based systems. Once a customer’s video is on our Cloud, we have a unique advantage over most on-premises

solutions in that we can run our customer’s surveillance video through powerful computational devices—e.g., NVIDIA®

GPU clusters—which would be impractical and cost-prohibitive for customers to deploy on site. We operate our services through both

Cloudastructure owned facilities and third-party facilities (e.g., Amazon Web Services and Google Cloud Platform). Our machine

learning software can see across countless cameras more efficiently than humans ever could.

Next, our Cloud-based system indexes objects and

faces in a customer’s surveillance video. This means that the video can be searched by tag, for example: “person,” “animal,”

“vehicle,” etc. and even by individual faces.

Once our Cloud-based system detects a person, it

will attempt to match that person’s face to a face in our database, which allows us to potentially identify a specific person, name,

and face.

As part of our product and service installation

and delivery process we also provide comprehensive customer onboarding and training to make sure that our customers know how to use our

services most effectively.

For customers that also take advantage of our Remote

Guarding services, we can set up alerts based on a variety of custom triggers, such as a perimeter being crossed (e.g., someone walking

into a restricted area), or movement detection within a designated zone (e.g., tracking to see if anyone enters a swimming pool) with

alarms set to any period of the day that our customer would like (e.g., alerts could be set to detect anyone in the pool between 10 PM

and 6 AM). Our remote guards monitor customer alarms and warn off intruders in real time (if a speaker is installed) and notify the appropriate

response group (law enforcement or otherwise, depending upon the situation) as appropriate. Our Remote Guarding services provide our customers

with an opportunity for significant savings when compared to the cost of an on-site physical guard.

Our Reporting Segment

As of December 31, 2024, we have organized our

operations into one reporting segment, focused on cloud-based AI video surveillance and remote guarding security services, based on the

way we organize and evaluate our business internally.

Our Business Model

We operate under a Cloud services delivery model.

We have found that we can compete most effectively with industry incumbents by pricing our products and services on a per camera per year

basis. We believe that under this model we can generate greater recurring revenue than our competitors while simultaneously providing

a lower total cost of ownership to our customers. In addition, by leveraging our AI features we are able to achieve security guard-level

pricing for our Remote Guarding services which can be 400% or more than we achieve with our surveillance service alone.

We deliver a one-stop security solution to our

customers which we believe provides greater quality control over the entire product and service installation and delivery processes. If

an installer is required (typically for additional cameras, speakers and conduit/cable), we bundle these services using our trusted partners.

In terms of hardware, in addition to our CVR, we also sell cameras and speakers, which are often required at each location.

Our Market

Our Cloudastructure solutions fall between the

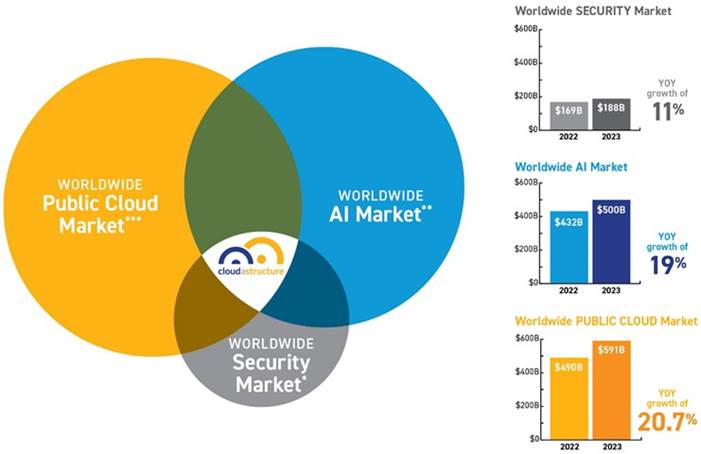

intersection of three very large and growing industries AI, Public Cloud, and Security. The worldwide AI market was estimated at $500

billion in 2023, growing at an annual rate of 19% (Worldwide Semiannual Artificial Intelligence Tracker; February 2022 IDC). According

to Gartner Research, the public cloud market was estimated at around $490 billion in 2023, growing at an annual rate of 20.7% (Gartner

Forecasts Worldwide Public Cloud End-User Spending to Reach Nearly $500 billion in 2023; Gartner, October 31, 2022). The worldwide security

market was estimated at $188 billion in 2023, growing at an annual rate of 11 percent (Gartner Identifies Three Factors Influencing Growth

in Security Spending; Gartner October 13, 2022).

We

are primarily focused on the multi-family and commercial property markets. According to a 2023 report by Fortune Business Insights, the

global proptech market (real estate focused only) is projected to grow from $36.6 billion for 2024 and reach $89.93 billion by 2033, for

a compounded annual growth rate of 11.9% during the period (see PropTech Market Report). We believe the rapid advancement of AI,

machine learning, and digitization of data is fueling much of this growth.

Additionally, city and county ordinances for mandated

surveillance (such as the laws in Prince George County, Maryland, DeKalb County, Georgia, etc., that require multi-family dwellings to

install and maintain 24-hour security cameras) are increasing given the availability, affordability and accessibility of advanced security

solution.

Cloudastructure contracts with both the ownership

and asset management groups of large multi-family properties such as Greystar Real Estate Partners, Avenue5 Residential, LLC, Cushman

& Wakefield, BH Management Services, LLC, FPI Management, Inc. and more, each with portfolios of properties in the several hundreds,

if not thousands. These groups are looking for cloud-based advanced AI and remote guarding services to increase the security of their

properties and improve the overall tenant experience. Security is often one of the most frequently cited problems at multi-family properties

as it can lead to higher costs from increased vacancy rates, vandalism, and rising insurance rates.

Although we are primarily focused on the multi-family

real estate and commercial property markets, we think it is noteworthy that video surveillance systems can be used in nearly any environment.

In our view security and surveillance are necessary for nearly all organizations worldwide. Governments, enterprises, financial institutions

and healthcare organizations are all expected or required to have a certain level of security and monitoring measures. As a result, there

has been an increase in the demand for security applications, such as video surveillance to monitor and record borders, ports, transportation

infrastructure, cities, corporate houses, educational institutes, public places, buildings and others, which is expected to drive the

video surveillance market growth globally.

With a technological solution that use AI, machine

learning and digitization of data, Cloudastructure is capitalizing on this growing market need for an end-to-end centralized security

system.

Our Competition

Entities with competing solutions include: Avigilon

(a subsidiary of Motorola Solutions, Inc. and our primary competitors in the multi-family space), Milestone Systems A/S (a Canon Inc.

subsidiary), Verkada, Inc., Tyco Integrated Security LLC (a business unit of Johnson Controls International plc) and Stealth Monitoring,

Inc. The markets for our products and services are highly competitive, and we are confronted by aggressive competition in all areas of

our business. These markets are characterized by frequent product introductions and rapid technological advances that have substantially

increased the capabilities and use of AI security and cloud-based video surveillance.

Principal competitive factors important to us include

price, product features, relative price/performance, product quality and reliability, design innovation, a strong third-party software

and accessories ecosystem, marketing and distribution capability, service and support and corporate reputation.

Our Customer Base

We focus on selling our products and services in

the multifamily and commercial property management markets. In our experience, these markets are close-knit and relationship-based, with

sales being highly reliant on word-of-mouth recommendations and customer testimonials. Larger property management firms in these markets

are very protective of their reputations, and often require a meaningful amount diligence before selecting new, significant vendors. As

part of that diligence process, property management firms almost always require references in the form of existing customer interviews,

and will likewise generally serve as references to other property management firms for services that they use and enjoy. In our experience,

as a newer market entrant, establishing a strong customer list is a critical requirement to ramp up sales, and an important metric used

by property management firms when evaluating a prospective vendor. As of the date of this Form 10-K, we have been vetted through an extensive

diligence process by, and signed contracts with, some of the largest property management and ownership groups in the markets in which

we operate. Now that we have landed five of the top 10 property management firms (based on National Multifamily Housing Council’s

2024 NMCH 50 list) as clients, as well as many mid-tier property management firms, our strategy is to expand our relationships with these

accounts with the goal of becoming the standardized AI security solution across their entire portfolios.

For the year ended December 31, 2023, SunRoad

Enterprises accounted for approximately 18%, and CONAM Management accounted for approximately 9% of our revenues, respectively. As of

December 31, 2024, SunRoad Enterprises accounted for approximately 18%, Fairfield Properties accounted for approximately 9%, Wingate

accounted for approximately 9%, and RV Mobile Power accounted for approximately 7% of our revenues, respectively. Other of our customers

include the following, with the approximate percentage of revenue generated by each as of December 31, 2024, noted next to their names:

● Greystar Real Estate Partners* – 1%

● Cushman & Wakefield* – 2%

● FPI Management, Inc.* – 1%

● BH Management Services, LLC* – 1%

● Avenue5 Residential, LLC* – 11%

● Federal Capital Partners – 2%

● CONAM Management – 6%

● The Wolff Company – 6%

● Wingate – 9%

● The Habitat Company – 1% |

|

| |

|

● American Landmark Apartments – 2%

● AJ Capital Partners – 1%

● Fairfield Properties – 9%

● MBK Rental Living – 1%

● SunRoad Enterprises – 7%

● RVMP – 7%

● The Breeden Company –

2%

● Gold Crown Management, Inc. – 3% |

|

*Top 10 property management company on the National Multifamily

Housing Council’s 2024 NMCH 50 list.

Select Customer Accolades

“Our package thefts have disappeared almost

entirely, which is amazing!”

—Zahra Alhisnawi, CONAM

“We are able to stop a crime if it’s

in progress!”

—Britney Kalberer, VP Kalberer Properties

“...A gate was damaged multiple times.

With Cloudastructure, we were able to identify the responsible party and recover the funds.”

—Alex Allione, Asset Manager CONAM

“I was able to open the platform on my

laptop at home, see who was there [at the pool] ... and resolve the situation right away. I absolutely love it. Five stars on the whole

thing.”

—Morgan Kottowitz, American Landmark

Typically, our customers pay up front annually

for services and sign our subscription and remote guarding agreements which govern the terms of service. Some of our larger customers

require monthly billing arrangements. We allow cancellation of our services at any time unless a three-year contract is signed, in which

case penalties occur. Specifically, for CONAM, our agreement operates on a month-to-month basis and may be terminated by either party

upon thirty days’ written notice. Immediate termination is possible under circumstances like non-payment or insolvency. For SunRoad,

pricing is structured around an annual commitment, with services prepared and prepaid on an annual basis, and similarly, either party

may terminate the agreement upon thirty days’ written notice without penalty. Additionally, we may terminate the agreement if SunRoad

fails to pay fees or becomes insolvent. While these agreements are nominally annual contracts that auto-renew, they remain cancellable

without penalty, as noted. We do not believe that we are substantially financially dependent on our relationship with any of our customers.

Our remote guarding agreements focus on utilizing advanced technology, such as AI-driven surveillance and real-time monitoring, to actively

protect property and escalate security incidents to law enforcement. In contrast, our subscription agreements are designed to give customers

access to our broader suite of services, including video storage, real-time viewing, and account management features. While both agreements

have similar legal structures, the remote guarding agreements are more specialized, emphasizing physical security and monitoring services.

Our ideal customer for our solutions is an enterprise business with multiple locations in the multi-family real estate and commercial

market space. The material terms of our remote guarding and subscription agreements are summarized below.

Remote Guarding Agreement

The remote guarding agreement includes strict confidentiality

provisions, defining “Confidential Information” to encompass all business, financial, and personal details of the customer

and related parties, including any recordings made during our services. We agree not to disclose this information without written consent,

except as required by law. All intellectual property developed or used under the agreement remains the exclusive property of us and our

subcontractors. Late payments incur interest at 1.5% per month, and the customer is responsible for collection costs, including legal

fees. We reserve the right to suspend services for non-payment. The agreement operates on a month-to-month basis, terminable by either

party with 30 days’ notice. Immediate termination may occur if the customer fails to pay, becomes insolvent, or enters bankruptcy.

Liability is limited, with us and our affiliates not responsible for any indirect, incidental, punitive, special, or consequential damages,

and total liability is capped at fees paid in the preceding 12 months. We make no warranties whatsoever regarding the services provided,

including any implied warranties of merchantability or fitness for a particular purpose. If the customer feels that the service is not

meeting agreed-upon levels, they may notify the Company, which will have 30 days to remedy the situation. If unresolved, the customer

will not be responsible for fees from the time of notice until the issue is resolved. Disputes are resolved through arbitration in San

Francisco under JAMS rules, though provisional remedies may be sought in court.

Subscription Agreement

The terms of our subscription agreement stipulates

that any disputes will be resolved through binding arbitration, with both parties waiving the right to a jury trial. Subscribers agree

to a subscription service with automatic recurring payments and must ensure payment information is kept current. If a subscriber’s

account is delinquent, we reserve the right to suspend access. We grant subscribers a non-transferable license to use our services, subject

to compliance with applicable laws and our terms. All intellectual property remains ours, and subscribers are prohibited from unauthorized

use or distribution of our materials. Third-party components may be integrated into the service, but we are not responsible for third-party

content or software. Prohibited conduct includes unauthorized access, violation of intellectual property rights, and interference with

security features. The agreement can be terminated by either party with 30 days’ notice, and we reserve the right to modify or discontinue

services without liability for service changes. Subscribers are responsible for indemnifying us for any unauthorized use, while we indemnify

subscribers for intellectual property infringement claims. The service is provided “as is,” and we disclaim all implied warranties,

limiting our liability to the fees paid in the prior 12 months. We do not assume liability for indirect, consequential, or punitive damages.

Additionally, the terms of sale specify that products are sold under FCA (Free Carrier) terms, with title passing upon delivery to the

carrier. We retain a security interest in the products until payment is received in full. Subscribers are responsible for complying with

U.S. export control laws, sanctions, and anti-corruption regulations, and must not sell or promote our products through unauthorized means,

including illegal platforms. Any returns are subject to a 20% restocking charge, and late payments incur interest at a rate of 5% per

month.

Our Employees

As of December 31, 2024, we had 16 full-time employees

and two part-time employees. We also use a considerable number of globally-sourced contractors from high-value regions such as India,

Brazil and Eastern Europe who are not included in our employee count. None of our employees are represented by labor unions or covered

by collective bargaining agreements. We consider the relationship with our employees to be good. We generally enter into agreements with

our employees that contain confidentiality provisions to control access to, and invention or work product assignment provisions to clarify

ownership of, our proprietary information.

Outsourcing

We currently outsource a number of our key functions

to third parties, including some software development, legal and payroll.

In addition, we host our services on cloud platforms

provided by Google LLC and Amazon.com, Inc. There are a number of alternative cloud providers that we could also utilize if necessary.

We have been moving more of our services to our own computers in co-location facilities to achieve the same result at lower costs.

Suppliers

We currently utilize third-party suppliers of standard,

off-the-shelf computers onto which we install software to turn them into our cloud video recorders. To date, we have bought computers

primarily through Amazon.com. Inc., Exxact Corporation, and Newegg Commerce, Inc., but there are a large number of other suppliers from

whom we could source these computers should we have to source from alternative providers for any reason. Similarly, we source cameras

and speakers primarily from Shenzhen Sunell Technology Corporation, but there are a large number of suppliers from whom we could source

for these cameras and speakers should we have to source from alternative providers for any reason.

Strategic Acquisitions

Our core focus is to grow Cloudastructure organically.

However, we may selectively evaluate strategic acquisition opportunities that would allow us to expand our footprint, broaden our client

base and deepen our product and service offerings. We believe that there are meaningful synergies that result from acquiring small companies

that provide unique solutions and opportunities for the Company and our clients. Integrating these solutions into our broader technology

and client base and integrating acquisitions into our plan of operations may potentially result in revenues and cost synergies. In 2022,

we completed acquisitions of two businesses: Visionful Holding Inc., a company that provided smart parking solutions for transit providers,

and Infrastructure Proving Grounds, Inc., an internet-of-things cybersecurity company. However, we are not currently utilizing the assets

we acquired from these businesses in our core operations. As of the date of this Form 10-K, we have not acquired any other businesses

and are not currently pursuing any other acquisitions.

Regulatory Environment

We are subject to a number of U.S. federal and

state and foreign laws and regulations that involve matters central to our business. These laws and regulations involve privacy, data

protection, intellectual property, competition, consumer protection and other subjects. Although our business is not currently subject

to licensing requirements in any of the jurisdictions in which we operate, this does not mean that licensing requirements may not be introduced

in one or more jurisdiction in which we operate. Any such licensing requirements, if introduced, could be burdensome and expensive or

even impose requirements that we are unable to meet.

In the ordinary course of business we and customers

using our solutions access, collect, store, analyze, transmit and otherwise process certain types of data, including personal information,

which subjects us and our customers to certain privacy and information security laws in the United States and internationally, including,

for example, the California Consumer Privacy Act (the “CCPA”), which took effect January 1, 2020, and the California Privacy

Rights Act (the “CPRA”) which took effect January 1, 2023, and which significantly amended the CCPA, and imposes additional

data protection obligations on companies doing business in California, including additional consumer rights processes and opt outs for

certain uses of sensitive data and imposes significant data privacy and potential statutory damages related to data protection for the

data of California residents.

The CPRA also created a new California data protection

agency specifically tasked to enforce the law, which will likely result in increased regulatory scrutiny of California businesses in the

areas of data protection and security and may increase our compliance costs and potential liability. In addition to the CCPA, numerous

other states’ legislatures have passed or are considering similar laws that will require ongoing compliance efforts and investment.

For example, Virginia passed the Virginia Consumer Data Protection Act, and Colorado passed the Colorado Privacy Act, both of which differ

from the CPRA and became effective in 2023. Similar laws have been proposed in other states as well and at the federal level. Other international

laws are also in place or pending, and such laws may have potentially conflicting requirements that would make compliance challenging.

Under these data protection and privacy laws, we

and our customers are required to maintain appropriate technical and organizational measures to ensure the security and protection of

personal data and information, and we must comply (either directly or indirectly in support of our customers’ compliance efforts,

as may be provided for the agreements we enter into with our customers) with a number of requirements with respect to individuals whose

personal data or information we collect and process. Many of these laws and regulations are still evolving and being tested in courts

and could be interpreted in ways that could harm our business. In addition, the application and interpretation of these laws and regulations

are often uncertain, particularly in the new and rapidly evolving industry in which we operate.

Intellectual Property

We do not have any patents or trademarks on which

our business relies. We have engaged intellectual property counsel and pursue intellectual property filings that we and our counsel deem

appropriate.

We rely on confidentiality procedures, contractual

commitments, and other legal rights to establish and protect our intellectual property. We generally enter into agreements with our employees

and consultants that contain confidentiality provisions to control access to, and invention or work product assignment provisions to clarify

ownership of, our proprietary information.

Available Information

Holders of our Class A units may obtain copies

of our filings with the SEC, free of charge, from the SEC’s website, www.sec.gov, or from our website, www.cloudastructure.com.

The contents of our website are solely for informational

purposes and the information on our website is not part of or incorporated by reference into this Form 10-K.

From time to time we may use our website as a distribution

channel for material company information, accordingly investors should monitor our website in addition to following our press releases

and SEC filings.

Item 1A. Risk Factors.

An investment in our Class A common stock involves

a high degree of risk. You should carefully consider the following risks and uncertainties, together with all of the other information

contained in this Form 10-K, including our financial statements and related notes appearing elsewhere in this Form 10-K, before deciding

whether to invest in our Class A common stock. The occurrence of one or more of the events or circumstances described in these risk factors,

alone or in combination with other events or circumstances, may have a material adverse effect on our business, reputation, revenue, financial

condition, results of operations and future prospects, in which event you could lose all or part of your investment. The risks and uncertainties

described below are not intended to be exhaustive and are not the only ones we face. Additional risks and uncertainties not presently

known to us or that we currently deem immaterial may also impair our business operations. This Report also contains forward-looking statements

that involve risks and uncertainties. See “Cautionary Note Regarding Forward-Looking Statements.” Our actual results could

differ materially and adversely from those anticipated in these forward-looking statements as a result of certain factors, including those

described below.

Risks Related to Our Business

Our technology continues to be developed, and it is unlikely

that we will ever develop our technology to a point at which no further development is required.

We are developing complex technology that requires

significant technical and regulatory expertise to develop, commercialize and update to meet evolving market and regulatory requirements.

If we are unable to successfully develop and commercialize our technology and products, it could have a material adverse effect on our

business operations and financial condition.

If our security measures are breached or unauthorized access

to individually identifiable biometric or other personally identifiable information is otherwise obtained, our reputation may be harmed,

and we may incur significant liabilities.

In the ordinary course of our business, we may

collect and store sensitive data, including personally identifiable information (“PII”), owned or controlled by ourselves

or our customers, and other parties. We communicate sensitive data electronically, and through relationships with multiple third-party

vendors and their subcontractors. These applications and data encompass a wide variety of business-critical information, including commercial

information, and business and financial information. We face a number of risks relative to protecting this critical information, including

loss of access risk, inappropriate use or disclosure, inappropriate modification, and the risk of our being unable to adequately monitor,

audit, and modify our controls over our critical information. This risk extends to the third-party vendors and subcontractors we use to

manage this sensitive data. As a custodian of this data, we therefore inherit responsibilities related to this data, exposing ourselves

to potential threats. Data breaches occur at all levels of corporate sophistication (including at companies with significantly greater

resources and security measures than our own) and the resulting fallout stemming from these breaches can be costly, time-consuming, and

damaging to a company’s reputation. Further, data breaches need not occur from malicious attacks or phishing only. Often, employee

carelessness can result in sharing PII with a much wider audience than intended. Consequences of such data breaches could result in fines,

litigation expenses, costs of implementing better systems, and the damage of negative publicity, all of which could have a material adverse

effect on our business operations and financial condition.

Our collection, processing, use and disclosure of individually

identifiable biometric or other personally identifiable information is subject to evolving and expanding privacy and security regulations.

Data privacy remains an evolving landscape, with

new regulations coming into effect at both the domestic and international level. For example, various states, such as California, Massachusetts,

and others, have implemented similar privacy laws and regulations, such as the California Consumer Privacy Act, which took effect January

1, 2020 (the “CCPA”), and creates new data privacy rights for users. The CCPA requires covered businesses that process personal

information of California residents to disclose their data collection, use and sharing practices. Further, the CCPA provides California

residents with new data privacy rights (including the ability to opt out of certain disclosures of personal data), imposes new operational

requirements for covered businesses, provides for civil penalties for violations as well as a private right of action for data breaches

and statutory damages (which is expected to increase data breach class action litigation and result in significant exposure to costly

legal judgements and settlements). Aspects of the CCPA and its interpretation and enforcement remain uncertain. In addition, the California

Privacy Rights Act of 2020 (the “CPRA”), which took effect January 1, 2023, expanded the CCPA. The CPRA, among other things,

gives California residents the ability to limit use of certain sensitive personal information, further restricts the use of cross-contextual

advertising, establishes restrictions on the retention of personal information, expands the types of data breaches subject to the CCPA’s

private right of action, provides for increased penalties for CPRA violations concerning California residents under the age of 16, and

establishes a new California Privacy Protection Agency to implement and enforce the CPRA. The CCPA and other similar laws could impact

our business activities depending on how they are interpreted. New legislation proposed or enacted in various other states will continue

to shape the data privacy environment nationally. For example, Virginia recently passed its Consumer Data Protection Act, and Colorado

recently passed the Colorado Privacy Act, both of which differ from the CPRA and became effective in 2023. Additional states have since

also passed comprehensive privacy laws with additional obligations and requirements on businesses. Certain state laws may be more stringent

or broader in scope, or offer greater individual rights, with respect to confidential, sensitive and personal information than federal,

international or other state laws, and such laws may differ from each other, which may complicate compliance efforts.

Additionally, all U.S. states and the District

of Columbia have enacted breach notification laws that may require that we notify customers, employees or regulators in the event of unauthorized

access to or disclosure of personal or confidential information experienced by us or our service providers. These laws are not consistent,

and compliance in the event of a widespread data breach is difficult and may be costly. Moreover, states have been frequently amending

existing laws, requiring attention to changing regulatory requirements. We also may be contractually required to notify customers of a

security breach. Although we may have contractual protections with our service providers, any actual or perceived security breach could

harm our reputation and brand, expose us to potential liability or require us to expend significant resources on data security and in

responding to any such actual or perceived breach. Any contractual protections we may have from our service providers may not be sufficient

to adequately protect us from any such liabilities and losses, and we may be unable to enforce any such contractual protections. In addition

to government regulation, privacy advocates and industry groups have and may in the future propose self-regulatory standards from time

to time. These and other industry standards may legally or contractually apply to us, or we may elect to comply with such standards.

Our success is highly dependent on our ability to attract and

retain highly skilled executive officers and employees.

To succeed, we must recruit, retain, manage and

motivate qualified technical and management personnel, and we face significant competition for experienced personnel. We are highly dependent

on the principal members of our management. If we do not succeed in attracting and retaining qualified personnel, particularly at the

management level, it could adversely affect our ability to execute our business plan and harm our operating results. In particular, the

loss of one or more of our executive officers could be detrimental to us if we cannot recruit suitable replacements in a timely manner.

We could in the future have difficulty attracting experienced personnel to our company and may be required to expend significant financial

resources in our employee recruitment and retention efforts.

We face intense competition for qualified personnel.

We may incur significant costs to attract and recruit skilled personnel, and we may lose new personnel to our competitors or other technology

companies before we realize the benefit of our investment in recruiting and training them. Many of the other technology companies that

we compete against for qualified personnel have greater financial and other resources, different risk profiles and a longer operating

history than we do. They also may provide more diverse opportunities and better prospects for career advancement. Some of these characteristics

may be more appealing to high-quality candidates than what we have to offer. Additionally, laws and regulations, such as restrictive immigration

laws, may limit our ability to recruit outside of the United States. If we are unable to continue to attract and retain high-quality personnel,

the rate and success at which we develop and commercialize our products and services could be limited and our potential for successfully

growing our business could be harmed.

Volatility in the trading price of our Class A

common stock may also affect our ability to attract and retain qualified personnel. Many of members of our management and other key personnel

hold equity awards that have vested in part or are exercisable, which could adversely affect our ability to retain these personnel. Personnel

may be more likely to leave us if the shares they own or the shares underlying their vested options have significantly appreciated in

value. In addition, many of our personnel may be able to receive significant proceeds from sales of our equity in the public markets,

which may reduce their motivation to continue to work for us. Any of these factors could harm our business, financial condition and results

of operations.

Privacy and data security laws and regulations could require

us to make changes to our business, impose additional costs on us and reduce the demand for our software solutions.

Our business model contemplates that we will transmit

a significant amount of PII through our platform. Privacy and data security have become significant issues in the United States and in

other jurisdictions where we may offer our video surveillance solutions. The regulatory framework relating to privacy and data security

issues worldwide is evolving rapidly and is likely to remain uncertain for the foreseeable future. Federal, state and foreign government

bodies and agencies have in the past adopted, or may in the future adopt, laws and regulations regarding the collection, use, processing,

storage and disclosure of personal or identifying information obtained from customers and other individuals. In addition to government

regulation, privacy advocates and industry groups may propose various self-regulatory standards that may legally or contractually apply

to our business. Because the interpretation and application of many privacy and data security laws, regulations and applicable industry

standards are uncertain, it is possible that these laws, regulations and standards may be interpreted and applied in a manner inconsistent

with our existing privacy and data management practices. As we expand into new jurisdictions or verticals, we will need to understand

and comply with various new requirements applicable in those jurisdictions or verticals.

To the extent applicable to our business or the

businesses of our customers, these laws, regulations and industry standards could have negative effects on our business, including by

increasing our costs and operating expenses, and delaying or impeding our deployment of new core products or services. Compliance with

these laws, regulations and industry standards requires significant management time and attention, and failure to comply could result

in negative publicity, subject us to fines or penalties or result in demands that we modify or cease existing business practices. In addition,

the costs of compliance with, and other burdens imposed by, such laws, regulations and industry standards may adversely affect our customers’

ability or desire to collect, use, process and store PII using our products and services, which could reduce overall demand for them.

Even the perception of privacy and data security concerns, whether or not valid, may inhibit market acceptance of our products and services

in certain verticals. In particular, some regulatory bodies have recently become more interested in technologies that we employ including

artificial intelligence (“AI”) and face recognition. Any of these outcomes could adversely affect our business and operating

results.

If our products and services do not achieve broad

acceptance both domestically and internationally, we will not be able to achieve our anticipated level of growth. Our revenues are primarily

derived from a cloud-based services model for our products and technology. We also receive some hardware revenue as well as revenue for

remote guarding services. We cannot accurately predict the future growth rate or the size of the market for our products and services.

The expansion of the market for our solutions depends on a number of factors, such as:

| · | the cost, performance and reliability of our products and services and the

solutions offered by our competitors; |

| · | customers’ perceptions regarding the benefits of cloud-based video

surveillance solutions; |

| · | public perceptions regarding the intrusiveness of these solutions and the

manner in which organizations use biometric and other identity information collected; |

| · | public perceptions regarding the confidentiality of private information; |

| · | proposed or enacted legislation related to privacy of information; |

| · | customers’ satisfaction regarding our cloud-based video surveillance

system; and |

| · | marketing efforts and publicity regarding our video surveillance solutions. |

Even if our products and services gain wide market

acceptance, our solutions may not adequately address market requirements and may not continue to gain market acceptance. If cloud-based

video surveillance solutions generally or our solutions specifically do not gain wide market acceptance, we may not be able to achieve

our anticipated level of growth and our revenues and results of operations would suffer.

Issues raised by the use of artificial intelligence (“AI”)

(including machine learning) in our platforms may result in reputational harm or liability.

AI is integrated into our surveillance systems

and Remote Guarding services and is a significant element of our business. As with many developing technologies, AI presents risks and

challenges that could affect its further development, adoption, and use, and therefore our business. AI algorithms may be flawed. Datasets

may be insufficient, of poor quality or contain biased information. Inappropriate or controversial data practices by, or practices reflecting

inherent biases of, data scientists, engineers and end-users of our systems could impair the acceptance of AI solutions. If the recommendations,

forecasts or analyses that AI applications assist in producing are deficient or inaccurate, we could be subjected to competitive harm,

potential legal liability and brand or reputational harm. Some AI scenarios present ethical issues. If we enable or offer AI solutions

that are controversial because of their purported or real impact on human rights, privacy, employment or other social issues, we may experience

brand or reputational harm.

We operate in a highly competitive industry that is dominated

by multiple very large, well-capitalized market leaders and is constantly evolving. New entrants to the market, existing competitor actions,

or other changes in market dynamics could adversely impact us.

The level of competition in the security industry

is high, with multiple exceptionally large, well-capitalized competitors holding a majority share of the market, such as Avigilon (a subsidiary

of Motorola Solutions, Inc.) Tyco Integrated Security (a business unit of Johnson Controls International plc), Stealth Monitoring, GardaWorld

Security Corporation (doing business as ECAMSECURE), EyeQ Monitoring and Watchtower. Many of the companies in the video surveillance market

have longer operating histories, larger customer bases, significantly greater financial, technological, sales, marketing, and other resources

than we do. At any point, these companies may decide to devote their resources to creating a competing solution which will impact our

ability to maintain or gain market share in this industry. Further, such companies will be able to respond more quickly than we can to

new or changing opportunities, technologies, standards, or client requirements, more quickly develop new products, or devote greater resources

to the promotion and sale of their products and services than we can. Likewise, their greater capabilities in these areas may enable them

to better withstand periodic downturns in the video surveillance industry and compete more effectively on the basis of price and production.

In addition, new companies may enter the markets in which we compete, further increasing competition in the video surveillance industry.

We believe that our ability to compete successfully

depends on a number of factors, including the type and quality of our products and services and the strength of our brand names, as well

as many factors beyond our control. We may not be able to compete successfully against current or future competitors, and increased competition

may result in price reductions, reduced profit margins, loss of market share and an inability to generate cash flows that are sufficient

to maintain or expand the development and marketing of new products or services, any of which would adversely impact our results of operations

and financial condition.

We may not be as successful as our competitors incorporating

AI into our business or adapting to a rapidly changing marketplace.

Our competitors may be larger, more diversified,

better funded and have access to more advanced technology, including AI. These competitive advantages may enable our competition to innovate

better and more quickly and to compete more effectively on quality and price, causing us to lose business and profitability. Burgeoning

interest in AI may increase our competition and disrupt our business model. AI may lower barriers to entry in our industry, and we may

be unable to effectively compete with the products or services offered by new competitors. AI-related changes to the products and services

we offer may affect our customers’ expectations, requirements or tastes in ways we cannot adequately anticipate or adapt to, causing

our business to lose sales, market share or the ability to operate profitably and sustainably.

Successful infringement claims against us could result in significant

monetary liability or prevent us from selling some of our products.

We believe our products and services may be highly

disruptive to a very large and growing market. Our competitors are well capitalized with significant intellectual property protection

and resources, and they (or patent trolls) may initiate infringement lawsuits against us. Such litigation could be expensive, time-consuming

and could prevent us from selling our products and services, which would significantly harm our ability to grow our business as planned.

We rely on other companies to provide certain hardware and software

solutions for our products.

We depend on certain third-party suppliers and

subcontractors to meet our contractual obligations to our customers and conduct our business. While we are not dependent on any one supplier

for any of our hardware or software solutions, our ability to meet our obligations to our customers may be adversely affected if one or

more suppliers or subcontractors does not provide the agreed-upon supplies or perform the agreed-upon services in compliance with customer

requirements and in a timely and cost-effective manner. Likewise, the quality of our products and services may be adversely impacted if

companies to whom we delegate manufacture of major components or subsystems for our products, or from whom we acquire such items, do not

provide major components and subsystems which meet required specifications and perform to our and our customers’ expectations. If

we encounter problems with one or more of these parties and they fail to perform to expectations, it could have a material adverse effect

on our business operations and financial condition.

We plan to implement new lines of business or offer new products

and services within existing lines of business.

We plan on introducing new computer vision algorithms,

or improving existing ones, such as face recognition and object detection, that must be executed at sustainable computational costs. We

also plan on introducing machine learning algorithms that combine information from our video surveillance system. There are substantial