UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM N-CSR

CERTIFIED

SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number: 811-10573

ALLIANCEBERNSTEIN NATIONAL MUNICIPAL INCOME FUND, INC.

(Exact name of registrant as specified in charter)

1345 Avenue

of the Americas, New York, New York 10105

(Address of principal executive offices) (Zip code)

Stephen M. Woetzel

AllianceBernstein L.P.

1345 Avenue of the Americas

New York, New York 10105

(Name and address of agent for service)

Registrant’s telephone number, including area code: (800) 221-5672

Date of fiscal year end: October 31, 2023

Date of reporting period: October 31, 2023

| ITEM 1. |

REPORTS TO STOCKHOLDERS. |

OCT 10.31.23

ANNUAL REPORT

ALLIANCEBERNSTEIN

NATIONAL MUNICIPAL INCOME FUND

(NYSE: AFB)

|

|

|

|

|

| Investment Products Offered |

|

• Are Not FDIC Insured • May Lose Value • Are Not Bank Guaranteed |

You may obtain a description of the Fund’s proxy voting policies and procedures, and information regarding how

the Fund voted proxies relating to portfolio securities during the most recent 12-month period ended June 30, without charge. Simply visit AB’s website at www.abfunds.com, or go to the Securities and

Exchange Commission’s (the “Commission”) website at www.sec.gov, or call AB at (800) 227 4618.

The Fund files its

complete schedule of portfolio holdings with the Commission for the first and third quarters of each fiscal year as an exhibit to its reports on Form N-PORT. The Fund’s Form N-PORT reports are available on the Commission’s website at

www.sec.gov.

AllianceBernstein Investments, Inc. (ABI) is the distributor of the AB family of mutual funds. ABI is a member of FINRA and

is an affiliate of AllianceBernstein L.P., the Adviser of the funds.

The [A/B] logo is a registered service mark of AllianceBernstein

and AllianceBernstein® is a registered service mark used by permission of the owner, AllianceBernstein L.P.

|

|

|

| FROM THE PRESIDENT |

|

|

Dear Shareholder,

We’re pleased to provide

this report for the AllianceBernstein National Municipal Income Fund, Inc. (the “Fund”). Please review the discussion of Fund performance, the market conditions during the reporting period and the Fund’s investment strategy.

At AB, we’re striving to help our clients achieve better outcomes by:

| + |

|

Fostering diverse perspectives that give us a distinctive approach to navigating global capital markets

|

| + |

|

Applying differentiated investment insights through a connected global research network |

| + |

|

Embracing innovation to design better ways to invest and leading-edge mutual-fund solutions |

Whether you’re an individual investor or a multibillion-dollar institution, we’re putting our knowledge and experience to work for you every day.

For more information about AB’s comprehensive range of products and shareholder resources, please log on to www.abfunds.com.

Thank you for your investment in AB mutual funds—and for placing your trust in our firm.

Sincerely,

Onur Erzan

President and Chief Executive

Officer, AB Mutual Funds

|

|

|

|

|

| abfunds.com |

|

ALLIANCEBERNSTEIN NATIONAL MUNICIPAL INCOME FUND | 1 |

ANNUAL REPORT

December 7, 2023

This report provides management’s discussion of fund performance for the AllianceBernstein National Municipal Income Fund, Inc., for the annual reporting period

ended October 31, 2023. The Fund is a closed-end fund, and its shares are listed and traded on the New York Stock Exchange.

The Fund seeks to provide high current income exempt from regular federal income tax by investing substantially all of its net

assets in municipal securities that pay interest that is exempt from federal income tax.

RETURNS AS OF OCTOBER 31, 2023 (unaudited)

|

|

|

|

|

|

|

|

|

|

|

|

| |

|

6 Months |

|

|

12 Months |

|

|

|

|

ALLIANCEBERNSTEIN

NATIONAL MUNICIPAL INCOME FUND (NAV) |

|

|

-10.87% |

|

|

|

-0.20% |

|

|

|

|

| Bloomberg Municipal Bond Index |

|

|

-4.65% |

|

|

|

2.64% |

|

The Fund’s market price per share on October 31, 2023, was $9.07. The Fund’s NAV price per share on October 31, 2023,

was $10.84. For additional Financial Highlights, please see pages 47–48.

INVESTMENT RESULTS

The table above shows the Fund’s performance compared with its benchmark, the Bloomberg Municipal Bond Index, for the six-

and 12-month periods ended October 31, 2023.

For the 12-month period, the Fund

underperformed the benchmark. Security selection in local general obligation and health care detracted, relative to the benchmark, while selection within state general obligation and miscellaneous revenue contributed. Yield-curve positioning and

duration positioning also detracted. The Fund’s overweight to mid-grade credit contributed.

For the six-month period, the Fund underperformed the benchmark. Security selection in guaranteed and industrial development revenue detracted, relative to the benchmark, while selection within health care and miscellaneous

revenue contributed. Yield-curve and duration positioning detracted for the period. The Fund’s overweight to mid-grade credit contributed.

Leverage, achieved through variable-rate municipal term preferred shares, detracted from total return over the six- and 12-month periods. Leverage achieved through

tender option bonds (“TOBs”) was immaterial over both periods.

The Fund did not use derivatives during either period.

MARKET REVIEW AND INVESTMENT STRATEGY

For the 12-month period ending October 31, 2023, the yield on a 10-Year AAA municipal bond rose to 3.61% from 3.34% and the yield on the

10-Year US Treasury rose to 4.91% from 4.06%. After-tax spreads widened on the

|

|

|

|

|

|

2 | ALLIANCEBERNSTEIN NATIONAL

MUNICIPAL INCOME FUND |

|

abfunds.com |

short end of the curve, while spreads compressed five-years and out. This indicated that municipals became cheaper relative to Treasuries on the short end, while becoming more expensive on the

intermediate and long part. Performance was particularly strong for the first 10 months of this period. However, worries that the US Federal Reserve would continue its policy tightening stance longer than anticipated caused a sell-off in September and October, leading to a lower return over the 12-month period.

The Fund’s Senior Investment

Management Team (the “Team”) continues to focus on after-tax return by investing in municipal bonds that generate income exempt from federal income taxes. The Team relies on an investment process

that combines quantitative and fundamental research to build effective bond portfolios.

The Fund may purchase municipal securities that are insured under policies

issued by certain insurance companies. Historically, insured municipal securities typically received a higher credit rating, which meant that the issuer of the securities paid a lower interest rate. As a result of declines in the credit quality and

associated downgrades of most bond insurers, insurance has less value than it did in the past. In purchasing such insured securities, the Adviser evaluates the risk and return of municipal securities through its own research. If an insurance

company’s rating is downgraded or the company becomes insolvent, the prices of municipal securities insured by the insurance company may decline. As of October 31, 2023, the Fund’s percentages of investments in municipal bonds that

are insured and in insured municipal bonds that have been pre-refunded or escrowed to maturity were 13.85% and 0.00%, respectively.

INVESTMENT POLICIES

The Fund will normally invest at least 80%, and normally substantially all, of its net assets in municipal

securities paying interest that is exempt from regular federal income tax. The Fund also normally will invest at least 75% of its assets in investment-grade municipal securities or unrated municipal securities considered to be of comparable quality.

The Fund may invest up to 25% of its net assets in municipal bonds rated below investment-grade and unrated municipal bonds considered to be of comparable quality as determined by the Adviser. The Fund intends to invest primarily in municipal

securities that pay interest that is not subject to the federal alternative minimum tax (“AMT”), but may invest without limit in municipal securities paying interest that is subject to the federal AMT. For more information regarding the

Fund’s risks, please see “Disclosures and Risks” on pages 4-9 and “Note G—Risks Involved in Investing in the Fund” of the Notes to Financial Statements on pages 40-45.

|

|

|

|

|

| abfunds.com |

|

ALLIANCEBERNSTEIN NATIONAL MUNICIPAL INCOME FUND | 3 |

DISCLOSURES AND RISKS

AllianceBernstein National Municipal Income Fund

Shareholder Information

Weekly comparative net asset value

(“NAV”) and market price information about the Fund is published each Saturday in Barron’s and in other newspapers in a table called “Closed-End Funds.” Daily NAVs

and market price information, and additional information regarding the Fund, is available at www.abfunds.com and www.nyse.com. For additional shareholder information regarding this Fund, please see pages

52-53.

Benchmark Disclosure

The Bloomberg Municipal Bond Index is unmanaged and does not reflect fees and expenses associated with the active management of a mutual fund portfolio. The

Bloomberg Municipal Bond Index represents the performance of the long-term tax-exempt bond market consisting of investment-grade bonds. In addition, the Index does not reflect the use of leverage, whereas the

Fund utilizes leverage. An investor cannot invest directly in an index, and its results are not indicative of the performance for any specific investment, including the Fund.

A Word About Risk

Among the risks of investing in the Fund are changes in

the general level of interest rates or changes in bond credit quality ratings. Changes in interest rates have a greater effect on bonds with longer maturities than on those with shorter maturities. Please note, as interest rates rise, existing bond

prices fall and can cause the value of your investment in the Fund to decline. While the Fund invests principally in bonds and other fixed-income securities, in order to achieve its investment objectives, the Fund may at times use certain types of

investment derivatives, such as options, futures, forwards and swaps. These instruments involve risks different from, and in certain cases, greater than, the risks presented by more traditional investments. At the discretion of the Fund’s

Adviser, the Fund may invest up to 25% of its net assets in municipal bonds that are rated below investment-grade (i.e., “junk bonds”). These securities involve greater volatility and risk than higher-quality fixed-income securities.

Financing and Related Transactions; Leverage and Other Risks: The Fund utilizes leverage to seek to enhance the yield and NAV attributable to its common stock.

These objectives may not be achieved in all interest-rate environments. Leverage creates certain risks for holders of common stock, including the likelihood of greater volatility of the NAV and market price of the common stock. If income from the

securities purchased from the funds made available by leverage is not sufficient to cover the cost of leverage, the Fund’s return will be less than if leverage had not been used.

|

|

|

|

|

|

4 | ALLIANCEBERNSTEIN NATIONAL

MUNICIPAL INCOME FUND |

|

abfunds.com |

DISCLOSURES AND RISKS (continued)

As a result, the

amounts available for distribution to common stockholders as dividends and other distributions will be reduced. During periods of rising short-term interest rates, the interest paid on the preferred shares or floaters in TOB transactions would

increase, which may adversely affect the Fund’s income and distribution to common stockholders. A decline in distributions would adversely affect the Fund’s yield and possibly the market value of its shares. If rising short-term rates

coincide with a period of rising long-term rates, the value of the long-term municipal bonds purchased with the proceeds of leverage would decline, adversely affecting the NAV attributable to the Fund’s common stock and possibly the market

value of the shares.

The Fund’s outstanding Variable Rate MuniFund Term Preferred Shares result in leverage. The Fund may also use other types of financial

leverage, including TOB transactions, either in combination with, or in lieu of, the preferred shares. In a TOB transaction, the Fund may transfer a highly rated fixed-rate municipal security into a special purpose entity (typically, a trust). The

Fund receives cash and a residual interest security (sometimes referred to as an “inverse floater”) issued by the trust in return. The trust simultaneously issues securities, which pay an interest rate that is reset each week based on an

index of high-grade short-term [seven-day] demand notes. These securities, sometimes referred to as “floaters”, are bought by third parties, including

tax-exempt money market funds, and can be tendered by these holders to a liquidity provider at par, unless certain events occur. The Fund continues to earn all the interest from the transferred bond less the

amount of interest paid on the floaters and the expenses of the trust, which include payments to the trustee and the liquidity provider and organizational costs. The Fund also uses the cash received from the transaction for investment purposes or to

retire other forms of leverage. Under certain circumstances, the trust may be terminated and collapsed, either by the Fund or upon the occurrence of certain events, such as a downgrade in the credit quality of the underlying bond, or in the event

holders of the floaters tender their securities to the liquidity provider. See Note H to the financial statements for more information about TOB transactions.

The

use of derivative instruments by the Fund, such as forwards, futures, options and swaps, may also result in a form of leverage.

Because the advisory fees received

by the Adviser are based on the adjusted net assets of the Fund (including assets supported by the proceeds of the Fund’s outstanding preferred shares), the Adviser has a financial incentive for the Fund to keep its preferred shares

outstanding, which may create a conflict of interest between the Adviser and the common shareholders of the Fund.

|

|

|

|

|

| abfunds.com |

|

ALLIANCEBERNSTEIN NATIONAL MUNICIPAL INCOME FUND | 5 |

DISCLOSURES AND RISKS (continued)

Tax Risk:

There is no guarantee that the income on the Fund’s municipal securities will be exempt from regular federal income and state income taxes. Unfavorable legislation, adverse interpretations by federal or state authorities, litigation or

noncompliant conduct by the issuer of a municipal security could affect the tax-exempt status of municipal securities. If the Internal Revenue Service or a state authority determines that an issuer of a

municipal security has not complied with applicable requirements, interest from the security could become subject to regular federal income tax and/or state personal income tax, possibly retroactively to the date the security was issued, the value

of the security could decline significantly, and a portion of the distributions to Fund shareholders could be recharacterized as taxable. Recent federal legislation included reductions in tax rates for individuals, with relatively larger reductions

in tax rates for corporations. These tax rate reductions may reduce the demand for municipal bonds which could reduce the value of municipal bonds held by the Fund.

Market Risk: The market value of a security may move up or down, sometimes rapidly and unpredictably. These fluctuations may cause a security to be worth less

than the price originally paid for it, or less than it was worth at an earlier time. Market risk may affect a single issuer, industry, sector of the economy or the market as a whole. Global economies and financial markets are increasingly

interconnected, which increases the probabilities that conditions in one country or region might adversely impact issuers in a different country or region. Conditions affecting the general economy, including political, social, or economic

instability at the local, regional, or global level may also affect the market value of a security. Health crises, such as pandemic and epidemic diseases, as well as other incidents that interrupt the expected course of events, such as natural

disasters, including fires, earthquakes and flooding, war or civil disturbance, acts of terrorism, power outages and other unforeseeable and external events, and the public response to or fear of such diseases or events, have had, and may in the

future have, an adverse effect on the Fund’s investments and NAV and can lead to increased market volatility. For example, the diseases or events themselves or any preventative or protective actions that governments may take in respect of such

diseases or events may result in periods of business disruption, inability to obtain raw materials, supplies and component parts, and reduced or disrupted operations for issuers of securities held by the Fund. The occurrence and pendency of such

diseases or events could adversely affect the economies and financial markets either in specific countries or worldwide.

Municipal Market Risk: This is the

risk that special factors may adversely affect the value of the municipal securities and have a significant effect on the yield or value of the Fund’s investments in municipal securities. These factors include economic conditions, political or

legislative changes, public

|

|

|

|

|

|

6 | ALLIANCEBERNSTEIN NATIONAL

MUNICIPAL INCOME FUND |

|

abfunds.com |

DISCLOSURES AND RISKS (continued)

health crises,

uncertainties related to the tax status of municipal securities, or the rights of investors in these securities. To the extent that the Fund invests more of its assets in a particular state’s municipal securities, the Fund may be vulnerable to

events adversely affecting that state, including economic, political and regulatory occurrences, court decisions, terrorism, public health crises (including the occurrence of a contagious disease or illness) and catastrophic natural disasters, such

as hurricanes, fires or earthquakes. For example, the novel coronavirus (COVID-19) pandemic has significantly stressed the financial resources of many issuers of municipal securities, which could impair any such issuer’s ability to meet its

financial obligations when due and adversely impact the value of its securities held by the Fund. As the full effects of the COVID-19 pandemic on state and local economies and on issuers of municipal securities are still uncertain, the financial

difficulties of issuers of municipal securities may continue or worsen, adversely affecting the performance of the Fund. The Fund’s investment in certain municipal securities with principal and interest payments that are made from the revenues

of a specific project or facility, and not general tax revenues, may have increased risks. Factors affecting the project or facility, such as local business or economic conditions, could have a significant effect on the project’s ability to

make payments of principal and interest on these securities.

Credit Risk: An issuer or guarantor of a fixed-income security, or the counterparty to a

derivatives or other contract, may be unable or unwilling to make timely payments of interest or principal, or to otherwise honor its obligations. The issuer or guarantor may default, causing a loss of the full principal amount of a security and

accrued interest. The degree of risk for a particular security may be reflected in its credit rating. There is the possibility that the credit rating of a fixed-income security may be downgraded after purchase, which may adversely affect the value

of the security. Investments in fixed-income securities with lower ratings tend to have a higher probability that an issuer will default or fail to meet its payment obligations.

Interest-Rate Risk: Changes in interest rates will affect the value of investments in fixed-income securities. When interest rates rise, the value of existing

investments in fixed-income securities tends to fall and this decrease in value may not be offset by higher income from new investments. Interest-rate risk is generally greater for fixed-income securities with longer maturities or durations. The

Fund may be subject to a greater risk of rising interest rates than would normally be the case due to the recent end of a period of historically low rates and the effect of potential central bank monetary policy, and government fiscal policy,

initiatives and resulting market reactions to those initiatives.

|

|

|

|

|

| abfunds.com |

|

ALLIANCEBERNSTEIN NATIONAL MUNICIPAL INCOME FUND | 7 |

DISCLOSURES AND RISKS (continued)

Inflation

Risk: This is the risk that the value of assets or income from investments will be less in the future as inflation decreases the value of money. As inflation increases, the value of the Fund’s assets can decline as can the value of the

Fund’s distributions. This risk is significantly greater for fixed-income securities with longer maturities.

Derivatives Risk: The Fund may enter into

derivative transactions such as forwards, options, futures and swaps. Derivatives may be difficult to price or unwind and leveraged so that small changes may produce disproportionate losses for the Fund. A short position in a derivative instrument

involves the risk of a theoretically unlimited increase in the value of the underlying asset, which could cause the Fund to suffer a potentially unlimited loss. Derivatives, especially

over-the-counter derivatives, are also subject to counterparty risk, which is the risk that the counterparty (the party on the other side of the transaction) on a

derivative transaction will be unable or unwilling to honor its contractual obligations to the Fund. Derivatives may result in significant losses, including losses that are far greater than the value of the derivatives reflected on the statement of

assets and liabilities.

Illiquid Investments Risk: Illiquid investments risk exists when particular investments are or become difficult to purchase or sell,

possibly preventing the Fund from selling out of these securities at an advantageous price. Causes of illiquid investments risk may include low trading volumes, large positions and heavy redemptions of Fund shares. Illiquid investments risk may be

magnified in a rising interest-rate environment, when the value and liquidity of fixed-income securities generally decline. Derivatives and securities involving substantial market and credit risk tend to involve greater illiquid investments risk

than most other types of investments. The Fund is subject to illiquid investments risk because the market for municipal securities is generally smaller than many other markets, which may make municipal securities more difficult to trade than other

types of securities. Illiquid securities may also be difficult to value.

Duration Risk: Duration is a measure that relates the expected price volatility of

a fixed-income security to changes in interest rates. The duration of a fixed-income security may be shorter than or equal to the full maturity of a fixed-income security. Fixed-income securities with longer durations have more risk and will

decrease in price as interest rates rise.

Management Risk: The Fund is subject to management risk because it is an actively managed investment fund. The

Adviser will apply its investment techniques and risk analyses in making investment decisions, but there is no guarantee that its techniques will produce the intended results. Some of these techniques may incorporate, or rely upon, quantitative

models,

|

|

|

|

|

|

8 | ALLIANCEBERNSTEIN NATIONAL

MUNICIPAL INCOME FUND |

|

abfunds.com |

DISCLOSURES AND RISKS (continued)

but there is no

guarantee that these models will generate accurate forecasts, reduce risk or otherwise perform as expected.

These risks are fully discussed in the Fund’s

prospectus. As with all investments, you may lose money by investing in the Fund.

An Important Note About Historical Performance

The performance shown in this report represents past performance and does not guarantee future results. Current performance may be lower or higher than the

performance information shown. All fees and expenses related to the operation of the Fund have been deducted. Performance assumes reinvestment of distributions and does not account for taxes. Historical performance does not reflect the deduction of

taxes that a shareholder would pay on fund distributions or the sale of fund shares and assumes the reinvestment of dividends and capital gains distributions at prices obtained pursuant to the Fund’s dividend reinvestment plan.

|

|

|

|

|

| abfunds.com |

|

ALLIANCEBERNSTEIN NATIONAL MUNICIPAL INCOME FUND | 9 |

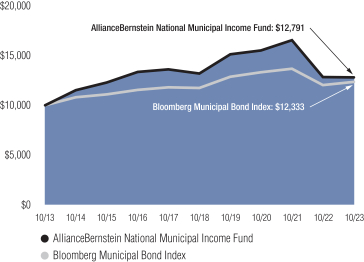

HISTORICAL PERFORMANCE

GROWTH OF A $10,000 INVESTMENT IN

THE FUND (unaudited)

10/31/2013 TO 10/31/2023

This chart illustrates the total value of an assumed $10,000 investment in AllianceBernstein National Municipal Income Fund based on

market prices (from 10/31/2013 to 10/31/2023) as compared to the performance of the Fund’s benchmark. The chart assumes the reinvestment of dividends and capital gains distributions at prices obtained pursuant to the Fund’s dividend

reinvestment plan.

AVERAGE ANNUAL RETURNS AS OF OCTOBER 31, 2023 (unaudited)

|

|

|

|

|

|

|

|

|

|

|

|

| |

|

NAV Returns |

|

|

Market Price |

|

|

|

|

| 1 Year |

|

|

-0.20% |

|

|

|

-7.75% |

|

|

|

|

| 5 Years |

|

|

-0.60% |

|

|

|

-1.23% |

|

|

|

|

| 10 Years |

|

|

2.49% |

|

|

|

1.27% |

|

AVERAGE ANNUAL RETURNS

AS OF THE MOST

RECENT CALENDAR QUARTER-END

SEPTEMBER 30, 2023 (unaudited)

|

|

|

|

|

|

|

|

|

|

|

|

| |

|

NAV Returns |

|

|

Market Price |

|

|

|

|

| 1 Year |

|

|

1.17% |

|

|

|

-6.21% |

|

|

|

|

| 5 Years |

|

|

-0.12% |

|

|

|

-1.33% |

|

|

|

|

| 10 Years |

|

|

2.95% |

|

|

|

1.61% |

|

Performance assumes the reinvestment of dividends and capital gains distributions at prices obtained pursuant to the Fund’s dividend

reinvestment plan.

|

|

|

|

|

|

10 | ALLIANCEBERNSTEIN NATIONAL

MUNICIPAL INCOME FUND |

|

abfunds.com |

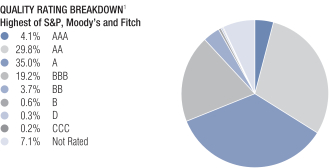

PORTFOLIO SUMMARY

October 31, 2023 (unaudited)

PORTFOLIO STATISTICS

Net Assets ($mil): $311.7

| 1 |

The Fund’s quality rating breakdown is expressed as a percentage of the Fund’s total investments in municipal

securities and may vary over time. The quality ratings are determined by using the S&P Global Ratings (“S&P”), Moody’s Investors Services, Inc. (“Moody’s”) and Fitch Ratings, Ltd. (“Fitch”). A measure

of the quality and safety of a bond or portfolio, based on the issuer’s financial condition. AAA is highest (best) and D is lowest (worst). If applicable, the pre-refunded category includes bonds which

are secured by U.S. Government Securities and therefore have been deemed high-quality investment grade by the Adviser. If applicable, Not Applicable (N/A) includes non-creditworthy investments such as

equities, currency contracts, futures and options. If applicable, the Not Rated category includes bonds that are not rated by a Nationally Recognized Statistical Rating Organization. The Adviser evaluates the creditworthiness of non-rated securities based on a number of factors including, but not limited to, cash flows, enterprise value and economic environment. |

|

|

|

|

|

| abfunds.com |

|

ALLIANCEBERNSTEIN NATIONAL MUNICIPAL INCOME FUND | 11 |

PORTFOLIO OF INVESTMENTS

October 31, 2023

|

|

|

|

|

|

|

|

|

| |

|

Principal

Amount

(000) |

|

|

U.S. $ Value |

|

| |

|

| MUNICIPAL OBLIGATIONS – 165.3% |

|

|

|

|

|

|

|

|

| Long-Term Municipal Bonds – 165.3% |

|

|

|

|

|

|

|

|

| Alabama – 0.3% |

|

|

|

|

|

|

|

|

| Sumter County Industrial Development Authority/AL

(Enviva, Inc.)

Series 2022

6.00%, 07/15/2052 |

|

$ |

1,300 |

|

|

$ |

877,438 |

|

|

|

|

|

|

|

|

|

|

|

|

|

| Arizona – 4.2% |

|

|

|

|

|

|

|

|

| Arizona Industrial Development Authority

(Heritage Academy Laveen & Gateway Obligated Group)

Series 2021

5.00%, 07/01/2051(a) |

|

|

1,000 |

|

|

|

778,160 |

|

| Salt Verde Financial Corp.

(Citigroup, Inc.)

Series 2007

5.00%, 12/01/2032 |

|

|

1,200 |

|

|

|

1,192,970 |

|

| 5.00%, 12/01/2037 |

|

|

8,700 |

|

|

|

8,437,001 |

|

| 5.25%, 12/01/2023 |

|

|

2,665 |

|

|

|

2,665,450 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

13,073,581 |

|

|

|

|

|

|

|

|

|

|

| Arkansas – 0.6% |

|

|

|

|

|

|

|

|

| Pulaski County Public Facilities Board

(Baptist Health Obligated Group)

Series 2014

5.00%, 12/01/2042 |

|

|

2,000 |

|

|

|

1,953,053 |

|

|

|

|

|

|

|

|

|

|

|

|

|

| California – 11.3% |

|

|

|

|

|

|

|

|

| Alameda Corridor Transportation Authority

Series 2022-A

0.00%, 10/01/2050(b) |

|

|

10,000 |

|

|

|

4,614,059 |

|

| California Pollution Control Financing Authority

(Poseidon Resources Channelside LP)

Series 2012

5.00%, 07/01/2037(a) |

|

|

3,075 |

|

|

|

3,009,276 |

|

| California Statewide Communities Development

Authority

(CHF-Irvine LLC)

BAM Series 2021

3.00%, 05/15/2054 |

|

|

9,895 |

|

|

|

6,109,213 |

|

| California Statewide Communities Development Authority

(Enloe Medical Center Obligated Group)

AGM

Series 2022-A

5.375%, 08/15/2057 |

|

|

2,000 |

|

|

|

2,055,302 |

|

|

|

|

|

|

|

12 | ALLIANCEBERNSTEIN NATIONAL

MUNICIPAL INCOME FUND |

|

abfunds.com |

PORTFOLIO OF INVESTMENTS (continued)

|

|

|

|

|

|

|

|

|

| |

|

Principal

Amount

(000) |

|

|

U.S. $ Value |

|

| |

|

| California Statewide Communities Development Authority

(Loma Linda University Medical Center)

Series

2016-A

5.00%, 12/01/2036(a) |

|

$ |

800 |

|

|

$ |

762,119 |

|

| 5.25%, 12/01/2056(a) |

|

|

2,000 |

|

|

|

1,769,299 |

|

| Long Beach Bond Finance Authority

(Bank of America Corp.)

Series

2007-A

5.50%, 11/15/2037 |

|

|

2,000 |

|

|

|

2,038,445 |

|

| M-S-R Energy

Authority

(Citigroup, Inc.)

Series 2009-A

6.50%, 11/01/2039 |

|

|

1,000 |

|

|

|

1,125,177 |

|

| Series 2009-C

6.50%, 11/01/2039 |

|

|

2,000 |

|

|

|

2,250,353 |

|

| Southern California Public Power Authority

(Goldman Sachs Group Inc/The)

Series 2007-A

5.00%, 11/01/2033 |

|

|

3,335 |

|

|

|

3,301,235 |

|

| State of California

Series 2013

5.00%, 11/01/2030 |

|

|

5,800 |

|

|

|

5,804,738 |

|

| Washington Township Health Care District

AGM Series 2023-B

4.50%, 08/01/2053 |

|

|

2,625 |

|

|

|

2,454,124 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

35,293,340 |

|

|

|

|

|

|

|

|

|

|

| Colorado – 2.4% |

|

|

|

|

|

|

|

|

| City & County of Denver CO Airport System Revenue

(Denver Intl Airport)

Series 2013-B

5.25%, 11/15/2031 |

|

|

6,680 |

|

|

|

6,679,502 |

|

| Colorado Health Facilities Authority

(CommonSpirit Health)

Series

2019-A

5.00%, 08/01/2044 |

|

|

705 |

|

|

|

665,754 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

7,345,256 |

|

|

|

|

|

|

|

|

|

|

| Connecticut – 0.3% |

|

|

|

|

|

|

|

|

| Connecticut State Health & Educational Facilities Authority

(University of Hartford (The))

Series 2019

4.00%, 07/01/2049 |

|

|

1,500 |

|

|

|

983,955 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| abfunds.com |

|

ALLIANCEBERNSTEIN NATIONAL MUNICIPAL INCOME FUND | 13 |

PORTFOLIO OF INVESTMENTS (continued)

|

|

|

|

|

|

|

|

|

| |

|

Principal

Amount

(000) |

|

|

U.S. $ Value |

|

| |

|

| Florida – 10.1% |

|

|

|

|

|

|

|

|

| Brevard County Health Facilities Authority

(Health First, Inc. Obligated Group)

Series 2014

5.00%, 04/01/2033 |

|

$ |

1,000 |

|

|

$ |

1,001,879 |

|

| County of Miami-Dade FL

Series 2021

4.00%, 07/01/2050 |

|

|

6,355 |

|

|

|

5,180,969 |

|

| Florida Development Finance Corp.

(Cornerstone Charter Academy, Inc.)

Series 2022

5.125%, 10/01/2052(a) |

|

|

1,000 |

|

|

|

840,988 |

|

| Florida Development Finance Corp.

(Mater Academy Inc.)

Series

2022-A

4.00%, 06/15/2052 |

|

|

3,250 |

|

|

|

2,390,926 |

|

| Florida Development Finance Corp.

(Mater Academy, Inc.)

Series

2020-A

5.00%, 06/15/2055 |

|

|

2,500 |

|

|

|

2,191,557 |

|

| Florida Higher Educational Facilities Financial Authority

(Ringling College of Art and Design, Inc.)

Series 2017

5.00%, 03/01/2042 |

|

|

1,000 |

|

|

|

909,041 |

|

| Lakewood Ranch Stewardship District

(Lakewood Ranch Stewardship District Series 2023 Assessment)

Series 2023

6.30%, 05/01/2054 |

|

|

1,000 |

|

|

|

968,456 |

|

| Miami-Dade County Expressway Authority

Series 2014-A

5.00%, 07/01/2044 |

|

|

5,000 |

|

|

|

4,700,521 |

|

| Palm Beach County Health Facilities Authority

(Baptist Health South Florida Obligated Group)

Series

2019

3.00%, 08/15/2044 |

|

|

8,000 |

|

|

|

5,268,396 |

|

| School District of Broward County/FL

Series 2022

5.00%, 07/01/2046 |

|

|

8,020 |

|

|

|

8,143,692 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

31,596,425 |

|

|

|

|

|

|

|

|

|

|

| Georgia – 4.0% |

|

|

|

|

|

|

|

|

| Augusta Development Authority

(AU Health System Obligated Group)

Series 2018

5.00%, 07/01/2036 |

|

|

4,170 |

|

|

|

4,171,300 |

|

|

|

|

|

|

|

14 | ALLIANCEBERNSTEIN NATIONAL

MUNICIPAL INCOME FUND |

|

abfunds.com |

PORTFOLIO OF INVESTMENTS (continued)

|

|

|

|

|

|

|

|

|

| |

|

Principal

Amount

(000) |

|

|

U.S. $ Value |

|

| |

|

| Main Street Natural Gas, Inc.

(Citadel LP)

Series 2022-C

4.00%, 08/01/2052(a) |

|

$ |

1,000 |

|

|

$ |

931,211 |

|

| Municipal Electric Authority of Georgia

Series 2019

5.00%, 01/01/2038 |

|

|

100 |

|

|

|

98,124 |

|

| 5.00%, 01/01/2049 |

|

|

2,000 |

|

|

|

1,895,881 |

|

| 5.00%, 01/01/2056 |

|

|

635 |

|

|

|

592,603 |

|

| 5.00%, 01/01/2063 |

|

|

3,165 |

|

|

|

2,934,569 |

|

| Series 2021

4.00%, 01/01/2046 |

|

|

330 |

|

|

|

263,138 |

|

| 4.00%, 01/01/2051 |

|

|

1,275 |

|

|

|

1,006,061 |

|

| 5.00%, 01/01/2056 |

|

|

650 |

|

|

|

591,070 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

12,483,957 |

|

|

|

|

|

|

|

|

|

|

| Illinois – 17.4% |

|

|

|

|

|

|

|

|

| Chicago Board of Education

Series 2018-D

5.00%, 12/01/2046 |

|

|

5,005 |

|

|

|

4,337,772 |

|

| Chicago O’Hare International Airport

Series 2017-D

5.00%, 01/01/2042 |

|

|

6,500 |

|

|

|

6,301,542 |

|

| Series 2022

4.625%, 01/01/2053 |

|

|

6,000 |

|

|

|

5,147,196 |

|

| Illinois Finance Authority

(Bradley University)

Series

2021-A

4.00%, 08/01/2051 |

|

|

4,750 |

|

|

|

3,525,750 |

|

| Illinois Finance Authority

(OSF Healthcare System Obligated Group)

Series 2015-A

5.00%, 11/15/2045 |

|

|

4,500 |

|

|

|

4,260,022 |

|

| Illinois Finance Authority

(University of Illinois)

Series 2020

4.00%, 10/01/2055 |

|

|

3,565 |

|

|

|

2,595,727 |

|

| Metropolitan Pier & Exposition Authority

Series 2017-A

5.00%, 06/15/2057 |

|

|

8,755 |

|

|

|

7,998,066 |

|

| State of Illinois

Series 2014

5.00%, 04/01/2030 |

|

|

1,655 |

|

|

|

1,637,486 |

|

| 5.00%, 05/01/2030 |

|

|

1,300 |

|

|

|

1,285,815 |

|

| 5.00%, 05/01/2033 |

|

|

1,150 |

|

|

|

1,124,654 |

|

| 5.00%, 02/01/2039 |

|

|

2,400 |

|

|

|

2,284,046 |

|

| Series 2017-D

5.00%, 11/01/2028 |

|

|

5,000 |

|

|

|

5,111,452 |

|

|

|

|

|

|

| abfunds.com |

|

ALLIANCEBERNSTEIN NATIONAL MUNICIPAL INCOME FUND | 15 |

PORTFOLIO OF INVESTMENTS (continued)

|

|

|

|

|

|

|

|

|

| |

|

Principal

Amount

(000) |

|

|

U.S. $ Value |

|

| |

|

| Series 2018-A

5.00%, 10/01/2027 |

|

$ |

1,000 |

|

|

$ |

1,024,028 |

|

| Series 2022-C

5.50%, 10/01/2040 |

|

|

6,250 |

|

|

|

6,392,418 |

|

| Village of Elk Grove Village IL

Series 2017

5.00%, 01/01/2028 |

|

|

1,060 |

|

|

|

1,095,809 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

54,121,783 |

|

|

|

|

|

|

|

|

|

|

| Indiana – 0.8% |

|

|

|

|

|

|

|

|

| Indiana Finance Authority

(University of Evansville)

Series 2022

5.25%, 09/01/2057 |

|

|

3,000 |

|

|

|

2,436,719 |

|

|

|

|

|

|

|

|

|

|

|

|

|

| Iowa – 1.7% |

|

|

|

|

|

|

|

|

| Iowa Finance Authority

(Iowa Fertilizer Co. LLC)

Series 2022

5.00%, 12/01/2050 |

|

|

5,000 |

|

|

|

4,419,529 |

|

| Iowa Tobacco Settlement Authority

Series 2021-A

4.00%, 06/01/2049 |

|

|

1,000 |

|

|

|

817,819 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

5,237,348 |

|

|

|

|

|

|

|

|

|

|

| Kentucky – 0.0% |

|

|

|

|

|

|

|

|

| Kentucky Economic Development Finance Authority

(CommonSpirit Health)

Series 2019-A

5.00%, 08/01/2044 |

|

|

145 |

|

|

|

136,928 |

|

|

|

|

|

|

|

|

|

|

|

|

|

| Louisiana – 5.2% |

|

|

|

|

|

|

|

|

| City of New Orleans LA

Series 2021-A

5.00%, 12/01/2046 |

|

|

15,000 |

|

|

|

14,992,072 |

|

| Parish of St. John the Baptist LA

(Marathon Oil Corp.)

Series 2019

2.10%, 06/01/2037 |

|

|

235 |

|

|

|

230,941 |

|

| 2.20%, 06/01/2037 |

|

|

950 |

|

|

|

887,314 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

16,110,327 |

|

|

|

|

|

|

|

|

|

|

| Maryland – 0.7% |

|

|

|

|

|

|

|

|

| Maryland Economic Development Corp.

(Maryland Economic Development Corp. Morgan View & Thurgood

Marshall Student Hsg)

Series 2022

6.00%, 07/01/2058 |

|

|

2,000 |

|

|

|

2,068,011 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

16 | ALLIANCEBERNSTEIN NATIONAL

MUNICIPAL INCOME FUND |

|

abfunds.com |

PORTFOLIO OF INVESTMENTS (continued)

|

|

|

|

|

|

|

|

|

| |

|

Principal

Amount

(000) |

|

|

U.S. $ Value |

|

| |

|

| Massachusetts – 4.9% |

|

|

|

|

|

|

|

|

| Commonwealth of Massachusetts

Series 2023

5.00%, 05/01/2053 |

|

$ |

10,000 |

|

|

$ |

10,089,253 |

|

| Massachusetts Development Finance Agency

(Emerson College)

Series

2016-A

5.00%, 01/01/2047 |

|

|

5,750 |

|

|

|

5,190,201 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

15,279,454 |

|

|

|

|

|

|

|

|

|

|

| Michigan – 11.7% |

|

|

|

|

|

|

|

|

| Ann Arbor School District

AGM Series 2023

4.00%, 05/01/2042 |

|

|

4,170 |

|

|

|

3,634,150 |

|

| City of Detroit MI

Series 2020

5.50%, 04/01/2050 |

|

|

1,970 |

|

|

|

1,874,083 |

|

| Series 2023-C

6.00%, 05/01/2043 |

|

|

2,300 |

|

|

|

2,383,833 |

|

| Detroit City School District

AGM Series 2001-A

6.00%, 05/01/2029 |

|

|

8,795 |

|

|

|

9,412,550 |

|

| Detroit Downtown Development Authority

(Detroit Downtown Development Authority Catalyst Development

Area)

AGM Series 2018-A

5.00%, 07/01/2043 |

|

|

3,020 |

|

|

|

2,887,895 |

|

| 5.00%, 07/01/2048 |

|

|

10,000 |

|

|

|

9,303,842 |

|

| Michigan Finance Authority

(Great Lakes Water Authority Water Supply System Revenue)

AGM Series 2014-D1

5.00%, 07/01/2035 |

|

|

1,250 |

|

|

|

1,255,395 |

|

| Michigan Finance Authority

(Public Lighting Authority)

Series

2014-B

5.00%, 07/01/2034 |

|

|

2,250 |

|

|

|

2,200,629 |

|

| Plymouth Educational Center Charter School

Series 2005

5.125%, 11/01/2023(c)(d) |

|

|

2,140 |

|

|

|

1,305,400 |

|

| Troy School District/MI

Series 2023

5.00%, 05/01/2041 |

|

|

2,000 |

|

|

|

2,058,348 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

36,316,125 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| abfunds.com |

|

ALLIANCEBERNSTEIN NATIONAL MUNICIPAL INCOME FUND | 17 |

PORTFOLIO OF INVESTMENTS (continued)

|

|

|

|

|

|

|

|

|

| |

|

Principal

Amount

(000) |

|

|

U.S. $ Value |

|

| |

|

| Minnesota – 2.7% |

|

| City of Ramsey MN

(Pact Charter School)

Series 2022-A

5.00%, 06/01/2032 |

|

$ |

1,000 |

|

|

$ |

951,011 |

|

| City of Rochester MN

(Mayo Clinic)

Series 2018

4.00%, 11/15/2048 |

|

|

3,000 |

|

|

|

2,485,228 |

|

| Duluth Economic Development Authority

(Essentia Health Obligated Group)

Series 2018

5.00%, 02/15/2053 |

|

|

5,625 |

|

|

|

5,057,402 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

8,493,641 |

|

|

|

|

|

|

|

|

|

|

| Nebraska – 2.9% |

|

|

|

|

|

|

|

|

| Central Plains Energy Project

(Goldman Sachs Group Inc/The)

Series

2017-A

5.00%, 09/01/2031 |

|

|

5,000 |

|

|

|

4,971,985 |

|

| Central Plains Energy Project

(Goldman Sachs Group, Inc.)

Series

2017-A

5.00%, 09/01/2029 |

|

|

4,000 |

|

|

|

3,973,612 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

8,945,597 |

|

|

|

|

|

|

|

|

|

|

| Nevada – 2.5% |

|

|

|

|

|

|

|

|

| Las Vegas Valley Water District

Series 2022-A

4.00%, 06/01/2051 |

|

|

8,645 |

|

|

|

7,193,399 |

|

| State of Nevada Department of Business & Industry

(DesertXpress Enterprises LLC)

Series

2023

8.125%, 01/01/2050(a) |

|

|

695 |

|

|

|

697,207 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

7,890,606 |

|

|

|

|

|

|

|

|

|

|

| New Hampshire – 0.8% |

|

|

|

|

|

|

|

|

| New Hampshire Business Finance Authority

(Covanta Holding Corp.)

Series 2020-A

3.625%, 07/01/2043(a) |

|

|

1,000 |

|

|

|

693,216 |

|

| New Hampshire Health and Education Facilities Authority Act

(Dartmouth-Hitchcock Obligated Group)

Series 2020-A

5.00%, 08/01/2059 |

|

|

2,000 |

|

|

|

1,773,506 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

2,466,722 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

18 | ALLIANCEBERNSTEIN NATIONAL

MUNICIPAL INCOME FUND |

|

abfunds.com |

PORTFOLIO OF INVESTMENTS (continued)

|

|

|

|

|

|

|

|

|

| |

|

Principal

Amount

(000) |

|

|

U.S. $ Value |

|

| |

|

| New Jersey – 8.9% |

|

|

|

|

|

|

|

|

| New Jersey Economic Development Authority

(NYNJ Link Borrower LLC)

Series 2013

5.125%, 01/01/2034 |

|

$ |

1,000 |

|

|

$ |

1,000,449 |

|

| New Jersey Economic Development Authority

(Prerefunded — US Treasuries)

Series 2014-P

5.00%, 06/15/2031 |

|

|

2,500 |

|

|

|

2,514,899 |

|

| New Jersey Health Care Facilities Financing Authority

(New Jersey Transportation Trust Fund Authority

State Lease)

Series 2017

5.00%, 10/01/2036 |

|

|

2,500 |

|

|

|

2,534,613 |

|

| New Jersey Health Care Facilities Financing Authority

(RWJ Barnabas Health Obligated Group)

Series

2014

5.00%, 07/01/2044 |

|

|

6,450 |

|

|

|

6,303,315 |

|

| New Jersey Transportation Trust Fund Authority

(New Jersey Transportation Fed Hwy Grant)

Series 2016

5.00%, 06/15/2029 |

|

|

4,750 |

|

|

|

4,832,754 |

|

| New Jersey Transportation Trust Fund Authority

(New Jersey Transportation Trust Fund Authority State

Lease)

Series 2019-B

4.00%, 06/15/2037 |

|

|

800 |

|

|

|

737,235 |

|

| South Jersey Transportation Authority

Series 2022

4.625%, 11/01/2047 |

|

|

1,000 |

|

|

|

890,732 |

|

| Tobacco Settlement Financing Corp./NJ

Series 2018-A

5.25%, 06/01/2046 |

|

|

8,990 |

|

|

|

8,826,330 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

27,640,327 |

|

|

|

|

|

|

|

|

|

|

| New York – 12.2% |

|

|

|

|

|

|

|

|

| City of New York NY

Series 2023

4.125%, 08/01/2053 |

|

|

11,300 |

|

|

|

9,530,558 |

|

| 5.00%, 08/01/2051 |

|

|

2,000 |

|

|

|

1,982,643 |

|

| Long Island Power Authority

Series 2023-E

5.00%, 09/01/2053 |

|

|

3,500 |

|

|

|

3,430,924 |

|

|

|

|

|

|

| abfunds.com |

|

ALLIANCEBERNSTEIN NATIONAL MUNICIPAL INCOME FUND | 19 |

PORTFOLIO OF INVESTMENTS (continued)

|

|

|

|

|

|

|

|

|

| |

|

Principal

Amount

(000) |

|

|

U.S. $ Value |

|

| |

|

| Metropolitan Transportation Authority

Series 2014-B

5.25%, 11/15/2034 |

|

$ |

4,000 |

|

|

$ |

4,003,673 |

|

| New York City Transitional Finance Authority Future Tax Secured Revenue

Series 2015A-1

5.00%, 08/01/2034 |

|

|

6,000 |

|

|

|

6,041,688 |

|

| 5.00%, 08/01/2037 |

|

|

4,000 |

|

|

|

4,005,162 |

|

| New York State Thruway Authority

(State of New York Pers Income Tax)

Series 2022

4.125%, 03/15/2056 |

|

|

4,000 |

|

|

|

3,393,157 |

|

| Port Authority of New York & New Jersey

Series

2013-178

5.00%, 12/01/2032 |

|

|

4,400 |

|

|

|

4,404,609 |

|

| Ulster County Capital Resource Corp.

(Woodland Pond at New Paltz)

Series 2017

5.00%, 09/15/2037 |

|

|

490 |

|

|

|

367,103 |

|

| 5.25%, 09/15/2042 |

|

|

205 |

|

|

|

147,726 |

|

| 5.25%, 09/15/2047 |

|

|

355 |

|

|

|

242,688 |

|

| 5.25%, 09/15/2053 |

|

|

760 |

|

|

|

497,568 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

38,047,499 |

|

|

|

|

|

|

|

|

|

|

| North Carolina – 2.6% |

|

|

|

|

|

|

|

|

| Greater Asheville Regional Airport Authority

AGM Series 2023

5.25%, 07/01/2053 |

|

|

4,000 |

|

|

|

3,899,090 |

|

| North Carolina Medical Care Commission

(Vidant Health Obligated Group)

Series 2015

5.00%, 06/01/2045 |

|

|

4,445 |

|

|

|

4,318,571 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

8,217,661 |

|

|

|

|

|

|

|

|

|

|

| North Dakota – 0.6% |

|

|

|

|

|

|

|

|

| City of Grand Forks ND

(Altru Health System Obligated Group)

AGM Series 2023-A

5.00%, 12/01/2053 |

|

|

2,000 |

|

|

|

1,901,123 |

|

|

|

|

|

|

|

|

|

|

|

|

|

| Ohio – 3.3% |

|

|

|

|

|

|

|

|

| Buckeye Tobacco Settlement Financing Authority

Series 2020-A

4.00%, 06/01/2048 |

|

|

2,000 |

|

|

|

1,598,409 |

|

| City of Chillicothe OH

(Adena Health System Obligated Group)

Series 2017

5.00%, 12/01/2047 |

|

|

1,800 |

|

|

|

1,667,204 |

|

|

|

|

|

|

|

20 | ALLIANCEBERNSTEIN NATIONAL

MUNICIPAL INCOME FUND |

|

abfunds.com |

PORTFOLIO OF INVESTMENTS (continued)

|

|

|

|

|

|

|

|

|

| |

|

Principal

Amount

(000) |

|

|

U.S. $ Value |

|

| |

|

| County of Cuyahoga OH

(MetroHealth System (The))

Series 2017

5.00%, 02/15/2052 |

|

$ |

2,240 |

|

|

$ |

1,969,819 |

|

| County of Cuyahoga OH

(MetroHealth System/The)

Series 2017

5.50%, 02/15/2052 |

|

|

4,585 |

|

|

|

4,346,148 |

|

| Ohio Higher Educational Facility Commission

(Kenyon College)

Series 2020

4.00%, 07/01/2040 |

|

|

730 |

|

|

|

628,316 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

10,209,896 |

|

|

|

|

|

|

|

|

|

|

| Oklahoma – 2.7% |

|

|

|

|

|

|

|

|

| Oklahoma City Airport Trust

Series 2018

5.00%, 07/01/2043 |

|

|

2,000 |

|

|

|

1,926,629 |

|

| 5.00%, 07/01/2047 |

|

|

5,000 |

|

|

|

4,711,127 |

|

| Tulsa Airports Improvement Trust

(Prerefunded — US Treasuries)

BAM Series 2015-A

5.00%, 06/01/2045 |

|

|

1,700 |

|

|

|

1,706,120 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

8,343,876 |

|

|

|

|

|

|

|

|

|

|

| Oregon – 0.3% |

|

|

|

|

|

|

|

|

| Multnomah County School District No. 40

Series 2023-A

Zero Coupon, 06/15/2051 |

|

|

5,000 |

|

|

|

1,014,840 |

|

|

|

|

|

|

|

|

|

|

|

|

|

| Pennsylvania – 8.5% |

|

|

|

|

|

|

|

|

| Allegheny County Hospital Development Authority

(Allegheny Health Network Obligated Group)

Series 2018-A

5.00%, 04/01/2047 |

|

|

5,000 |

|

|

|

4,677,916 |

|

| Berks County Municipal Authority (The)

(Tower Health Obligated Group)

Series 2020-B

5.00%, 02/01/2040 |

|

|

1,000 |

|

|

|

621,096 |

|

| Bucks County Industrial Development Authority

(Grand View Hospital/Sellersville PA Obligated

Group)

Series 2021

4.00%, 07/01/2051 |

|

|

2,250 |

|

|

|

1,418,059 |

|

|

|

|

|

|

| abfunds.com |

|

ALLIANCEBERNSTEIN NATIONAL MUNICIPAL INCOME FUND | 21 |

PORTFOLIO OF INVESTMENTS (continued)

|

|

|

|

|

|

|

|

|

| |

|

Principal

Amount

(000) |

|

|

U.S. $ Value |

|

| |

|

| Chester County Industrial Development Authority

(Collegium Charter School)

Series 2022

6.00%, 10/15/2052(a) |

|

$ |

1,000 |

|

|

$ |

913,350 |

|

| Pennsylvania Economic Development Financing Authority

(Commonwealth of Pennsylvania Department of

Transportation)

AGM Series 2022

5.75%, 12/31/2062 |

|

|

7,500 |

|

|

|

7,813,169 |

|

| Pennsylvania Economic Development Financing Authority

(PA Bridges Finco LP)

Series 2015

5.00%, 12/31/2038 |

|

|

1,940 |

|

|

|

1,837,524 |

|

| 5.00%, 06/30/2042 |

|

|

6,060 |

|

|

|

5,574,453 |

|

| Pennsylvania Turnpike Commission

Series 2021-B

4.00%, 12/01/2043 |

|

|

3,200 |

|

|

|

2,764,822 |

|

| Scranton School District/PA

BAM Series 2017-E

4.00%, 12/01/2037 |

|

|

1,025 |

|

|

|

912,446 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

26,532,835 |

|

|

|

|

|

|

|

|

|

|

| Puerto Rico – 0.2% |

|

|

|

|

|

|

|

|

| Puerto Rico Sales Tax Financing Corp. Sales Tax Revenue

Series

2019-A

4.329%, 07/01/2040 |

|

|

615 |

|

|

|

531,253 |

|

|

|

|

|

|

|

|

|

|

|

|

|

| South Carolina – 5.5% |

|

|

|

|

|

|

|

|

| South Carolina Jobs-Economic Development Authority

(Prisma Health Obligated Group)

Series 2018-A

5.00%, 05/01/2048 |

|

|

5,900 |

|

|

|

5,586,616 |

|

| South Carolina Ports Authority

(Prerefunded – US Treasuries)

Series 2015

5.00%, 07/01/2045 |

|

|

5,000 |

|

|

|

5,041,613 |

|

| South Carolina Public Service Authority

Series 2016-B

5.00%, 12/01/2041 |

|

|

5,000 |

|

|

|

4,850,963 |

|

| Series 2022

3.00%, 12/01/2046 |

|

|

1,132 |

|

|

|

730,580 |

|

| 3.00%, 12/01/2049 |

|

|

1,566 |

|

|

|

977,164 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

17,186,936 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

22 | ALLIANCEBERNSTEIN NATIONAL

MUNICIPAL INCOME FUND |

|

abfunds.com |

PORTFOLIO OF INVESTMENTS (continued)

|

|

|

|

|

|

|

|

|

| |

|

Principal

Amount

(000) |

|

|

U.S. $ Value |

|

| |

|

| South Dakota – 0.2% |

|

| County of Lincoln SD

(Augustana College Association (The))

Series 2021

4.00%, 08/01/2061 |

|

$ |

1,000 |

|

|

$ |

676,097 |

|

|

|

|

|

|

|

|

|

|

|

| Tennessee – 0.1% |

|

| Chattanooga Health Educational & Housing Facility Board

(CommonSpirit Health)

Series 2019-A

4.00%, 08/01/2037 |

|

|

145 |

|

|

|

128,139 |

|

| 4.00%, 08/01/2038 |

|

|

275 |

|

|

|

239,003 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

367,142 |

|

|

|

|

|

|

|

|

|

|

| Texas – 17.5% |

|

| Arlington Higher Education Finance Corp.

(Uplift Education)

Series

2023-A

4.375%, 12/01/2058 |

|

|

3,000 |

|

|

|

2,453,602 |

|

| Baytown Municipal Development District

(Baytown Municipal Development District Baytown Convention Center

Hotel Revenue Hotel Occupancy Tax)

Series 2021

4.00%, 10/01/2050 |

|

|

2,910 |

|

|

|

2,063,845 |

|

| City of El Paso TX

Series 2021-C

4.00%, 08/15/2047 |

|

|

10,540 |

|

|

|

8,572,370 |

|

| County of Smith TX

Series 2023

5.00%, 08/15/2048 |

|

|

7,000 |

|

|

|

7,051,421 |

|

| Decatur Hospital Authority

Series 2021

4.00%, 09/01/2044 |

|

|

2,000 |

|

|

|

1,494,826 |

|

| Denton Independent School District

Series 2023

5.00%, 08/15/2048 |

|

|

10,000 |

|

|

|

10,169,655 |

|

| Hidalgo County Regional Mobility Authority

Series 2022-A

Zero Coupon, 12/01/2043 |

|

|

2,000 |

|

|

|

571,096 |

|

| Zero Coupon, 12/01/2044 |

|

|

2,420 |

|

|

|

647,888 |

|

| Zero Coupon, 12/01/2045 |

|

|

3,360 |

|

|

|

843,230 |

|

| Melissa Independent School District

Series 2023

4.25%, 02/01/2053 |

|

|

12,780 |

|

|

|

10,893,338 |

|

|

|

|

|

|

| abfunds.com |

|

ALLIANCEBERNSTEIN NATIONAL MUNICIPAL INCOME FUND | 23 |

PORTFOLIO OF INVESTMENTS (continued)

|

|

|

|

|

|

|

|

|

| |

|

Principal

Amount

(000) |

|

|

U.S. $ Value |

|

| |

|

| New Hope Cultural Education Facilities Finance

Corp.

(CHF-Collegiate Housing Denton LLC)

AGM Series 2018-A1

5.00%, 07/01/2038 |

|

$ |

500 |

|

|

$ |

490,345 |

|

| 5.00%, 07/01/2048 |

|

|

1,100 |

|

|

|

1,004,903 |

|

| Pflugerville Independent School District

Series 2023-A

4.00%, 02/15/2044 |

|

|

5,000 |

|

|

|

4,372,349 |

|

| Texas Private Activity Bond Surface Transportation Corp.

(NTE Mobility Partners Segments 3 LLC)

Series 2013

6.75%, 06/30/2043 |

|

|

3,000 |

|

|

|

3,003,921 |

|

| Texas Water Development Board

(State Water Implementation Revenue Fund for Texas)

Series 2022

5.00%, 10/15/2057 |

|

|

1,000 |

|

|

|

1,004,171 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

54,636,960 |

|

|

|

|

|

|

|

|

|

|

| Utah – 2.1% |

|

|

|

|

|

|

|

|

| City of Salt Lake City UT Airport Revenue

Series 2018-A

5.00%, 07/01/2048 |

|

|

2,500 |

|

|

|

2,348,201 |

|

| BAM Series 2018-A

5.00%, 07/01/2043 |

|

|

4,500 |

|

|

|

4,356,264 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

6,704,465 |

|

|

|

|

|

|

|

|

|

|

| Virginia – 2.4% |

|

|

|

|

|

|

|

|

| Virginia Small Business Financing Authority

(Capital Beltway Express LLC)

Series 2022

5.00%, 12/31/2047 |

|

|

5,000 |

|

|

|

4,708,143 |

|

| Virginia Small Business Financing Authority

(Elizabeth River Crossings OpCo LLC)

Series 2022

3.00%, 01/01/2041 |

|

|

3,950 |

|

|

|

2,745,089 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

7,453,232 |

|

|

|

|

|

|

|

|

|

|

| Washington – 2.8% |

|

|

|

|

|

|

|

|

| King County Rural Library District

Series 2012

4.00%, 12/01/2023 |

|

|

825 |

|

|

|

824,945 |

|

| State of Washington

Series 2023-2

5.00%, 08/01/2048 |

|

|

7,685 |

|

|

|

7,797,000 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

8,621,945 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

24 | ALLIANCEBERNSTEIN NATIONAL

MUNICIPAL INCOME FUND |

|

abfunds.com |

PORTFOLIO OF INVESTMENTS (continued)

|

|

|

|

|

|

|

|

|

| |

|

Principal

Amount

(000) |

|

|

U.S. $ Value |

|

| |

|

| West Virginia – 1.2% |

|

|

|

|

|

|

|

|

| West Virginia Hospital Finance Authority

(West Virginia United Health System Obligated Group)

Series

2018-A

5.00%, 06/01/2052 |

|

$ |

3,875 |

|

|

$ |

3,674,850 |

|

|

|

|

|

|

|

|

|

|

|

|

|

| Wisconsin – 9.7% |

|

|

|

|

|

|

|

|

| Wisconsin Center District

AGM Series 2020-C

Zero Coupon,

12/15/2038 |

|

|

3,155 |

|

|

|

1,454,409 |

|

| Zero Coupon, 12/15/2040 |

|

|

3,300 |

|

|

|

1,347,017 |

|

| Wisconsin Public Finance Authority

(CFC-SA LLC)

Series 2022

5.00%, 02/01/2062 |

|

|

10,000 |

|

|

|

8,400,671 |

|

| Wisconsin Public Finance Authority

(CHF – Wilmington LLC)

AGM Series 2018

5.00%, 07/01/2058 |

|

|

10,000 |

|

|

|

9,343,648 |

|

| Wisconsin Public Finance Authority

(Moses H Cone Memorial Hospital Obligated Group)

Series 2022-A

5.00%, 10/01/2052 |

|

|

5,000 |

|

|

|

4,730,778 |

|

| Wisconsin Public Finance Authority

(Prerefunded – US Treasuries)

Series 2022

4.00%, 04/01/2052(a) |

|

|

90 |

|

|

|

91,748 |

|

| Wisconsin Public Finance Authority

(Queens University of Charlotte)

Series 2022

5.25%, 03/01/2047 |

|

|

2,000 |

|

|

|

1,761,229 |

|

| Wisconsin Public Finance Authority

(Roseman University of Health Sciences)

Series 2022

4.00%, 04/01/2052(a) |

|

|

3,260 |

|

|

|

2,241,463 |

|

| Wisconsin Public Finance Authority

(Southeastern Regional Medical Center Obligated Group)

Series

2021

4.00%, 02/01/2037 |

|

|

1,055 |

|

|

|

798,439 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

30,169,402 |

|

|

|

|

|

|

|

|

|

|

| Total Municipal Obligations

(cost $567,042,192) |

|

|

|

|

|

|

515,040,605 |

|

|

|

|

|

|

|

|

|

|

|

|

| abfunds.com |

|

ALLIANCEBERNSTEIN NATIONAL MUNICIPAL INCOME FUND | 25 |

PORTFOLIO OF INVESTMENTS (continued)

|

|

|

|

|

|

|

|

|

| |

|

Principal

Amount

(000) |

|

|

U.S. $ Value |

|

| |

|

| COMMERCIAL MORTGAGE-BACKED SECURITIES – 3.8% |

|

|

|

|

|

|

|

|

| Non-Agency Fixed Rate CMBS – 3.8% |

|

|

|

|

|

|

|

|

| California Housing Finance Agency

Series 2019-2, Class A

4.00%, 03/20/2033 |

|

$ |

1,102 |

|

|

$ |

1,038,478 |

|

| Series 2021-1, Class A

3.50%, 11/20/2035 |

|

|

962 |

|

|

|

832,134 |

|

| National Finance Authority

Series 2023-2

3.875%, 01/20/2038 |

|

|

2,992 |

|

|

|