false

2025-02-28

0001853962

00-0000000

i-80 Gold Corp.

0001853962

2025-02-28

2025-02-28

0001853962

exch:XASE

us-gaap:CommonStockMember

2025-02-28

2025-02-28

0001853962

exch:XTSX

us-gaap:CommonStockMember

2025-02-28

2025-02-28

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

___________________________

FORM 8-K

CURRENT REPORT

Pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934

Date of Report (Date of earliest event reported):

February 28, 2025

I-80 GOLD CORP.

(Exact Name of Registrant as Specified in Its Charter)

|

British Columbia

|

001-41382

|

Not Applicable |

| (State of incorporation) |

(Commission File Number) |

(I.R.S. Employer Identification) |

5190 Neil Road, Suite 460

Reno, Nevada, United States

89502

(Address of principal executive offices) (ZIP Code)

Registrant’s Telephone Number, Including Area Code: (775) 525-6450

Check the appropriate box below if the Form 8-K filing is intended to simultaneously satisfy the filing obligation of the registrant under any of the following provisions (see General Instruction A.2. below):

☐ Written communications pursuant to Rule 425 under the Securities Act (17 CFR 230.425)

☐ Soliciting material pursuant to Rule 14a-12 under the Exchange Act (17 CFR 240.14a-12)

☐ Pre-commencement communications pursuant to Rule 14d-2(b) under the Exchange Act (17 CFR 240.14d-2(b))

☐ Pre-commencement communications pursuant to Rule 13e-4(c) under the Exchange Act (17 CFR 240.13e-4(c))

Securities registered pursuant to Section 12(b) of the Act:

| Title of each class |

|

Trading Symbols |

|

Name of each exchange on which registered |

|

Common Shares

|

|

IAUX

|

|

NYSE American LLC

|

|

Common Shares

|

|

IAU

|

|

The Toronto Stock Exchange |

Indicate by check mark whether the registrant is an emerging growth company as defined in Rule 405 of the Securities Act of 1933 (§ 230.405 of this chapter) or Rule 12b-2 of the Securities Exchange Act of 1934 (§ 240.12b -2 of this chapter).

Emerging growth company ☑

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Item 1.01 Entry into a Material Definitive Agreement

On February 22, 2023, i-80 Gold Corp. (the "Company") and the TSX Trust Company (the "Trustee") entered into a convertible debenture indenture (the "Indenture") pursuant to which, the Company issued USD$65,000,000 aggregate principal amount of secured convertible debentures (the "Debentures"). The Indenture provided that the Debentures would bear interest at a fixed rate of 8.00% per annum and mature on February 27, 2027. Additionally, outstanding amounts under the Debentures would be convertible into common shares of the Company at any time prior to maturity at the option of the applicable respective lender (a) in the case of outstanding principal, USD$3.38 per common share, and (b) in the case of accrued and unpaid interest, subject to approval by the Toronto Stock Exchange ("TSX"), at the market price of the common shares at the time of the conversion of such interest.

As previously disclosed on a Form 8-K filed with the SEC on January 17, 2025, the Company entered into a settlement agreement, pursuant to which it was required to propose three separate amendments to the terms of its Debentures. On February 28, 2025, the Company and the Trustee entered into a First Supplemental Indenture to a Convertible Debenture Indenture (the "Supplemental Indenture") pursuant to which, the Company approved, among other things, the following material amendments to the terms of the Debentures.

The first amendment involves, changing the conversion price applicable to noteholders' conversion of outstanding and accrued interest on the Debentures to equal the volume weighted average price of the Company's common shares on the TSX during the five trading days immediately preceding the date the Debenture holders make such election, less a discount of 15% converted into US dollars. Additionally, corresponding changes were made to the provisions relating to the right of the Company to elect to convert the interest payable under the Debentures into common shares, including updating the conversion price to reflect a 15% discount to market price.

The Debentures are currently secured by the Company's McCoy-Cove project. The second amendment removes the Company's right to grant security on a pari-passu basis against the Company's McCoy-Cove Project, leaving Debenture holders as senior secured on the McCoy-Cove project with any additional debt subordinated.

The third amendment provides for a new redemption right of the Debentures, allowing the Company to redeem the Debentures for cash at its election at a 104% premium of the outstanding principal, along with accrued interest up to the redemption date. This amendment provides the Company with greater flexibility as it works towards the execution of its recapitalization plan.

Item 2.03 Creation of a Direct Financial Obligation or an Obligation under an Off-Balance Sheet Arrangement of a Registrant

The disclosures in Item 1.01 of this Form 8-K regarding the amendments to the terms of the Debentures are hereby incorporated by reference into this Item 2.03.

Item 3.02 Unregistered Sales of Equity Securities

On February 28, 2024, the Company sold 997,871 shares of its common stock at a purchase price of C$0.80 per share to certain directors and officers of the Company in a private placement exempt from registration under Section 4(a)(2) and Rule 506(b) of Regulation D under the Securities Act of 1933, as amended. The Company received proceeds of approximately C$798,297.00.

Item 7.01 Regulation FD Disclosure

Designated Press Releases

On February 28, 2025, the Company issued a press release announcing the completion of certain amendments to its USD$65 million convertible debenture dated February 22, 2023 and the closing of the private placement with certain insiders of the Company, undertaken concurrently with the previously announced prospectus offering of common shares which closed on January 31, 2025, a copy of which is attached hereto as Exhibit 99.1.

On March 5, 2025, the Company issued a press release announcing the results of the preliminary economic assessment for the Granite Creek Underground Project, Nevada, a copy of which is attached hereto as Exhibit 99.2.

On March 6, 2025, the Company issued a press release announcing the results of the preliminary economic assessment for the Granite Creek Open Pit Project, Nevada, a copy of which is attached hereto as Exhibit 99.3.

The information contained in the press releases attached hereto and the Investor Day presentation referenced below is being furnished and shall not be deemed filed for purposes of Section 18 of the Securities Exchange Act of 1934, as amended (the "Exchange Act"), or otherwise subject to the liability of that section, and shall not be incorporated by reference into any registration statement or other document filed under the Securities Act of 1933, as amended, or the Exchange Act, except as shall be expressly set forth by specific reference in such filing.

Exhibits 99.1, 99.2, 99.3 shall be deemed to be incorporated by reference into the Company's registration statement on Form F-10 (File Number 333-279567).

Investor Day Presentation

On March 6, 2025, the Company issued an Investor Day presentation, which investors can find on its website www.i80gold.com/investors.

Item 9.01 Financial Statements and Exhibits

(d) Exhibits

SIGNATURES

Pursuant to the requirements of the Securities Exchange Act of 1934, the registrant has duly caused this report to be signed on its behalf by the undersigned hereunto duly authorized.

| Dated: March 6, 2025 |

i-80 GOLD CORP. |

| |

|

|

| |

By: |

/s/ Ryan Snow |

| |

|

Ryan Snow |

| |

|

Chief Financial Officer |

i-80 Gold Completes Further Steps in Support of its Recapitalization Plan

Previously Announced Amendments to Convertible Debenture Indenture and

Closing of Concurrent Private Placement Completed

This news release constitutes a "designated news release" for the purposes of the Company's prospectus

supplement dated August 12, 2024, to its short form base shelf prospectus dated June 21, 2024

Reno, Nevada, February 28, 2025 - i-80 GOLD CORP. (TSX:IAU) (NYSE:IAUX) ("i-80 Gold", or the "Company") is pleased to announce the completion of certain amendments to its $65 million convertible debenture indenture dated February 22, 2023 (the "Indenture") as previously disclosed in the Company's press release dated January 13, 2025. Additionally, the Company announces the closing of the private placement with certain insiders of the Company, undertaken concurrently with the previously announced prospectus offering of common shares which closed on January 31, 2025, as previously disclosed in the Company's press releases dated January 27, 2025 and January 31, 2025 (the "Concurrent Private Placement").

The completion and closing of each of Indenture amendments and the Concurrent Private Placement support i-80 Gold's recapitalization plan by improving its near-term liquidity as well as facilitating its refinancing flexibility as it works towards a recapitalization plan intended to better align its capital structure with the Company's long-term growth strategy and development plan.

First Supplemental Indenture to Convertible Debenture Indenture

The Company is pleased to announce that it has entered into a first supplemental indenture to the Indenture (the "Supplemental Indenture") with the TSX Trust Company (the "Trustee") to finalize the proposed amendments to the terms of the terms of the Indenture as previously disclosed in its prior press release on January 13, 2025.

On February 22, 2023, the Company closed a private placement offering of $65 million principal amount of secured convertible debentures (the "Convertible Debentures") pursuant to the Indenture among the Company and the Trustee.

On October 15, 2024, debenture holders representing not less than 66 2/3% of the principal amount of the Convertible Debentures appointed, by written resolution, a committee of the debenture holders (the "Committee"), to exercise, and to direct the Trustee to exercise, on behalf of the debenture holders, the powers of the debenture holders set out in the Indenture.

On February 28, 2025, the Committee delivered to the Company and the Trustee an extraordinary resolution approved by the Committee, acting on behalf of the debenture holders, by instrument in writing effective, to approve the amendments to the Indenture as set forth in the Supplemental Indenture and to authorize and to direct the Trustee to enter into and execute the Supplemental Indenture (the "Amending Resolution").

The Supplement Indenture amends the Indenture, to among other things, provide as follows:

(i) that the definitions relating to the conversion prices applicable to the conversion of the accrued and unpaid interest on the Convertible Debentures were revised to provide:

(a) the conversion price applicable to the a debenture holder's right to elect to convert outstanding and accrued interest on the Convertible Debentures is equal to the volume weighted average price of i-80 Gold's common shares on the Toronto Stock Exchange ("TSX") during the five trading days immediately preceding the date of the debenture holder's election notice, less a discount of 15%, converted into US dollars at the Bank of Canada rate on such date;

(b) the conversion price applicable to the Company' right to elect to convert outstanding and accrued interest on the Convertible Debentures is equal to equal to the greater of (x) 85% of the average closing price of the i-80 Gold common shares as measured in US dollars on the NYSE American during the 10 business days immediately preceding the date of the Company's election notice, and (y) the volume weighted average price of i-80 Gold common shares on TSX during the five trading days immediately preceding the date of the Company's election notice, less a discount of 15%, converted into US dollars at the Bank of Canada rate on such date;

(ii) that the Company's right to grant security against the McCoy-Cove Project would rank subordinate to the security granted to the debenture holders; and

(iii) the Company with a redemption right in respect of all of the outstanding Convertible Debentures which allows the Company to redeem, in its sole discretion, all of the outstanding Convertible Debentures for cash at a 104% premium of the outstanding principal, along with accrued interest up to the redemption date.

The description of the Supplemental Indenture in this press release, is a summary only, and is not exhaustive nor is it intended as a substitute for reviewing the Supplemental Indenture and is qualified in its entirety by reference to the full text of the Supplemental Indenture, which can be found under the Company's issuer profile on SEDAR+ at www.sedarplus.ca.

Closing of Concurrent Private Placement

The Company is also pleased to announce the closing of the Concurrent Private Placement of an aggregate of 997,871 common shares to certain directors and officers of the Company at a price of C$0.80 per share for gross proceeds of approximately C$798,297. Further to its press release dated January 27, 2025 in connection with its proposed private placement of subscription receipts at a price of $0.80 per subscription receipt involving certain directors and officers of the Company, the Company subsequently received a waiver from the NYSE American from having to obtain shareholder approval for the participation of its directors and officers in an equity financing by the Company at a price that is at a discount to market price and obtained approval to complete the Concurrent Private Placement of common shares to such directors and officers.

All of the subscribers under the Concurrent Private Placement were "insiders" of the Company (the "Insider Participation"). Each of the subscriptions by an "insider" is considered to be a "related party transaction" for purposes of Multilateral Instrument 61-101 - Protection of Minority Security Holders in Special Transactions ("MI 61-101"). The Insider Participation is exempt from the formal valuation and minority shareholder requirements under MI 61-101 in reliance upon the exemptions contained in section 5.5(a) and 5.7(1)(a), respectively, of MI 61-101 as the fair market value of the transaction, insofar as it involves interested parties, is not more than the 25% of the Company's market capitalization. The Company did not file a material change report more than 21 days before the expected closing date of the Concurrent Private Placement as the details of the Concurrent Private Placement and the Insider Participation were not settled until shortly prior to the closing of the Concurrent Private Placement, and the Company wished to close the Concurrent Private Placement on an expedited basis for sound business reasons.

All securities issued under the Concurrent Private Placement are subject to a hold period in Canada expiring four months and one day from the date hereof and are subject to a hold period in the United States of at least six months from the date of issuance pursuant to the U.S. Securities Act of 1933, as amended (the "U.S. Securities Act"). The Concurrent Private Placement is subject to final acceptance by the Toronto Stock Exchange and the NYSE American.

The Company anticipates using the net proceeds of the Concurrent Private Placement for working capital and general corporate purposes.

The participation of directors and officers in the offering reflects continued confidence in the Company's strategic direction and growth potential.

The securities issued under the Concurrent Private Placement have not been registered under the U.S. Securities Act, or any state or other applicable jurisdiction's securities laws, and may not be offered or sold in the United States absent registration or an applicable exemption from the registration requirements of the U.S. Securities Act and applicable state or other jurisdictions' securities laws. This press release shall not constitute an offer to sell or the solicitation of an offer to buy these securities, nor shall there be any offer, solicitation or sale of these securities in any jurisdiction in which such offer, solicitation, or sale would be unlawful.

About i-80 Gold Corp.

i-80 Gold Corp. is a Nevada-focused mining company with the fourth largest gold mineral resources in the state of Nevada. The recapitalization plan underway is designed to unlock the value of the Company's high-grade gold deposits to create a Nevada mid-tier gold producer. i-80 Gold's common shares are listed on the TSX and the NYSE American under the trading symbol IAU:TSX and IAUX:NYSE. Further information about i-80 Gold's portfolio of assets and long-term growth strategy is available at www.i80gold.com or by email at info@i80gold.com.

For further information, please contact:

Leily Omoumi - VP Corporate Development & Strategy

1.866.525.6450

info@i80gold.com

www.i80gold.com

FORWARD LOOKING INFORMATION

Certain statements in this release constitute "forward-looking statements" or "forward-looking information" within the meaning of applicable securities laws, including but not limited to, statements regarding: the use of proceeds in connection with the Concurrent Private Placement; the Company's ability to obtain the approval of the Toronto Stock Exchange and the NYSE American for the Concurrent Private Placement; and the Company's other future plans and expectations, including its recapitalization plan. Such statements and information involve known and unknown risks, uncertainties and other factors that may cause the actual results, performance or achievements of the company, its projects, or industry results, to be materially different from any future results, performance or achievements expressed or implied by such forward-looking statements or information. Such statements can be identified by the use of words such as "may", "would", "could", "will", "intend", "expect", "believe", "plan", "anticipate", "estimate", "scheduled", "forecast", "predict" and other similar terminology, or state that certain actions, events or results "may", "could", "would", "might" or "will" be taken, occur or be achieved. These statements reflect the Company's current expectations regarding future events, performance and results and speak only as of the date of this release.

Forward-looking statements and information involve significant risks and uncertainties, should not be read as guarantees of future performance or results and will not necessarily be accurate indicators of whether or not such results will be achieved. A number of factors could cause actual results to differ materially from the results discussed in the forward-looking statements or information, including, but not limited to: material adverse changes, unexpected changes in laws, rules or regulations, or their enforcement by applicable authorities; the failure of parties to contracts with the company to perform as agreed; social or labour unrest; changes in commodity prices; and the failure of exploration programs or studies to deliver anticipated results or results that would justify and support continued exploration, studies, development or operations. For a more detailed discussion of such risks and other factors that could cause actual results to differ materially from those expressed or implied by such forward-looking statements, refer to i-80's filings with Canadian securities regulators, including the most recent Annual Information Form, available on SEDAR+ at www.sedarplus.ca.

i-80 Gold Announces Positive Preliminary Economic Assessment on

the Granite Creek Underground Project, Nevada; After-Tax NPV(5%) of $155 Million at

US$2,175/oz Au and an After-Tax NPV(5%) of $344 Million at US$2,900/oz Au

This news release constitutes a "designated news release" for the purposes of the Company's prospectus

supplement dated August 12, 2024, to its short form base shelf prospectus dated June 21, 2024.

Reno, Nevada, March 5, 2025 - i-80 GOLD CORP. (TSX:IAU) (NYSE:IAUX) ("i-80 Gold", or the "Company") is pleased to announce the results of a preliminary economic assessment (the "PEA") for the Granite Greek Underground Project ("Granite Creek Underground" or the "Project"). Granite Creek Underground is the first property within the Company's pipeline of assets to be redeveloped and is currently ramping up to full production. The Project is situated at the intersection of the highly prolific Battle Mountain-Eureka and Getchell gold trends in northern Nevada, United States.

"Our exploration results at Granite Creek Underground to-date suggest significant potential for resource growth and expansion. As a result, an extensive drill program is planned in the coming years to realize that potential. The PEA also demonstrates that once our Lone Tree autoclave is refurbished as anticipated in 2028, production and cash flow are expected to increase materially," stated Richard Young, Chief Executive Officer.

This resource employed in this PEA does not include drilling conducted in 2023 and 2024. Further, the effects of underground water management in the 2025 mine plan are not reflected in this PEA. Due to these factors, the Company's 2025 production forecast, which is still under development, differs from what is depicted in the PEA schedule. i-80 Gold expects to produce between 20,000 to 30,000 ounces of gold at Granite Creek Underground this year.

Granite Creek Underground PEA Highlights

Mineral Estimates, Production and Mine Life

-

High-grade underground gold mine with a life of mine ("LOM") of approximately 8 years.

-

Average annual gold production of approximately 60,000 ounces, following production ramp up.

-

Estimated LOM cash costs(1) of $1,366 per ounce and all-in-sustaining costs(1) of $1,597 per ounce.

-

Updated mineral resource estimate resulting in a measured and indicated gold mineral resource of 261,000 ounces at 10.5 grams per tonne ("g/t") and an inferred gold mineral resource of 326,000 ounces at 13.0 g/t.

-

The updated mineral resource estimate does not include infill drilling conducted within the Granite Creek Underground in 2023 and 2024. Further, infill and step out drilling on the South Pacific zone in 2025 is expected to be completed for inclusion in a feasibility study planned for Q4 2025.

-

Based on exploration work conducted to-date, Granite Creek Underground has significant potential for resource expansion; it is located only 10 kilometers from the prolific Turquoise Ridge Complex within Nevada Gold Mines' joint venture which currently hosts approximately 20 million ounces of gold(4). An extensive drill program is planned for the coming years to test this system at depth and to the north.

Project Economics

-

Based on a $2,175/oz gold price, the Project's undiscounted after-tax cash flows(2) total $197 million with an after-tax net present value(2) ("NPV") of $155 million, assuming a 5% discount rate.

-

Based on a spot gold price of $2,900/oz, the Project's undiscounted after-tax cash flows(2) total $420 million with an after-tax NPV(2) of $344 million, assuming a 5% discount rate.

-

Mine construction is complete. LOM development and sustaining capital is estimated at

$105 million.

Mining and Processing

-

The primary mining method is underhand drift and fill.

-

Over the next three years through to the end of 2027, refractory material mined is expected to be processed at a third-party autoclave facility, resulting in approximately 30% lower payability on gold produced, until i-80 Gold's Lone Tree facility(3) is commissioned as anticipated in 2028 (see Figure 1).

-

Overall average gold grade processed of 11.6 g/t with an average gold recovery of 78%, utilizing oxide processing, acidic pressure oxidation and alkaline pressure oxidation selected based on characteristics of the mineralized material. This average LOM recovery includes the 58% payability factor for years 2025 - 2027. Once the Company's autoclave facility is refurbished, process recovery rates are expected to rise to approximately 92%, significantly increasing production, lowering costs and improving cash flows from the Project.

-

The Company expects recovered gold ounces of between 20,000 to 30,000 ounces in 2025 from Granite Creek. An updated operational plan will be included in a feasibility study for Granite Creek Underground, which is currently expected to be released in Q4 2025.

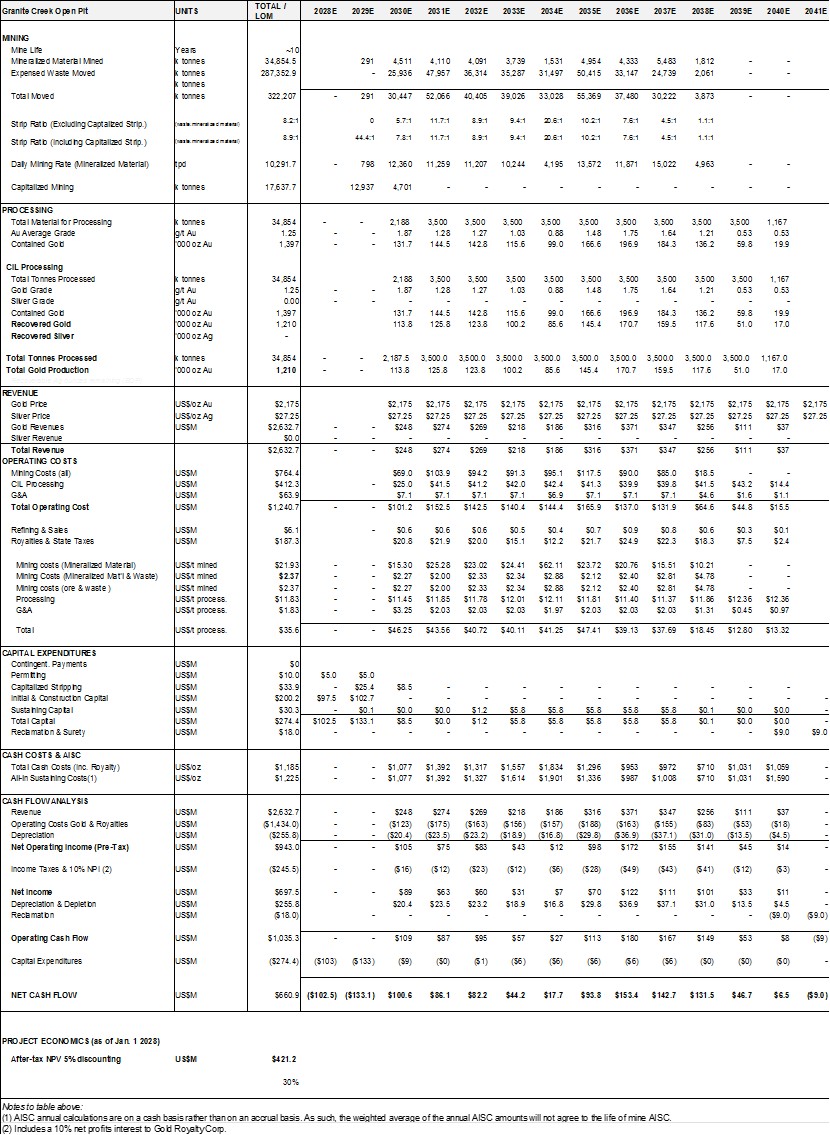

A summary of key valuation, cost, and operating metrics is presented in Table 1 below. For more detailed metrics presented on an annual basis, see Granite Creek Underground Detailed Cash Flow Model in the Appendix. All amounts are in United States dollars, unless otherwise stated.

Table 1: Summary of PEA Key Operating and Financial Metrics

|

Project Economics

|

Unit

|

|

|

Gold Price

|

$/oz

|

$2,175

|

|

Pre-Tax NPV(5%)(2)

|

$M

|

$179.9

|

|

After-Tax NPV(5%)(2)

|

$M

|

$155.1

|

|

After-Tax IRR

|

%

|

84%

|

|

After-Tax Cash Flow

|

$M

|

$196.7

|

|

Production Profile

|

|

|

|

Mine Life

|

years

|

~8

|

|

Mineralized Material Mined

|

000s

tonnes

|

1,441.8

|

|

Gold Grade of Mineralized Material Mined

|

g/t Au

|

11.6

|

|

Waste Tonnes Mined

|

000s

tonnes

|

684.4

|

|

Capitalized Tonnes Mined

|

000s

tonnes

|

488.8

|

|

Total Tonnes Mined (incl. capitalized tonnes)

|

000s

tonnes

|

2,615.0

|

|

Total Mineralized Material Processed

|

000s

tonnes

|

1,441.8

|

|

Gold Grade Processed

|

g/t Au

|

11.6

|

|

Average Gold Recovery

|

%

|

78%

|

|

Total Gold Recovered

|

000s oz

|

417.5

|

|

Average Annual Gold Production (LOM)

|

000s oz

|

52.2

|

|

Average Annual Gold Production

(following production ramp up)

|

000s oz

|

59.6

|

|

Unit Operating Costs

|

|

|

|

LOM Operating Cost

|

|

|

|

Mineralized Material Mined

|

$/t mined

|

$163.7

|

|

Mineralized Material & Waste Mined

|

$/t mined

|

$150.3

|

|

Processed

|

$/t processed

|

$90.8

|

|

Transportation

|

$/t processed

|

$14.8

|

|

Dewatering Electricity

|

$/t processed

|

$8.5

|

|

G&A

|

$/t processed

|

$44.2

|

|

LOM Total Cash Costs(1) (net of by-product credit)

|

$/oz

|

$1,366

|

|

LOM All-in Sustaining Costs(2) (net of by-product credit)

|

$/oz

|

$1,597

|

|

Total Capital Costs

|

|

|

|

Definition & Conversion Drilling

|

$M

|

$16.0

|

|

LOM Development & Sustaining Capital

|

$M

|

$88.8

|

|

Closure Costs

|

$M

|

$7.4

|

|

Total Capital & Closure Costs

|

$M

|

$112.2

|

"2024 ramp-up activities at Granite Creek Underground were hindered by water ingress into the underground workings, which slowed underground development and lowered production for the year. An extensive hydrology study was completed during the year to better understand the water sources and flows, and the Company was able to install a water treatment facility and permit the release of excess water into a local filtration system built by the Company. The dewatering system is expected to lower the water level in the working areas of the Project to allow development to ramp up in 2025. Despite these challenges, since ramp up began in 2023, reconciliation to the resource model has been excellent with slightly more tonnes, marginally lower grade resulting in few more ounces. The positive reconciliation is a credit to the conservatism in the model and the high level of competency of the Company's underground contractor," added Matthew Gili, President and Chief Operating Officer.

Mineral Resource Update

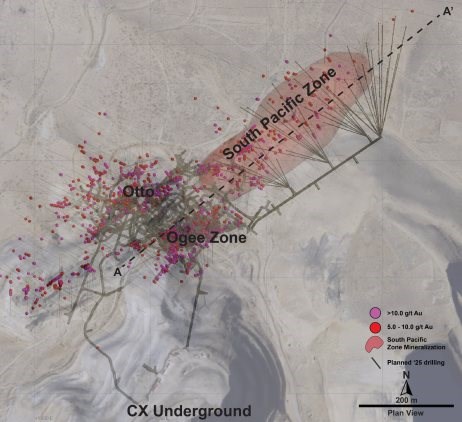

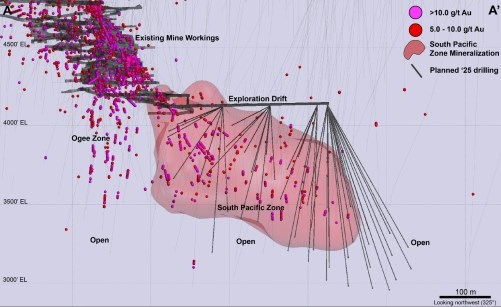

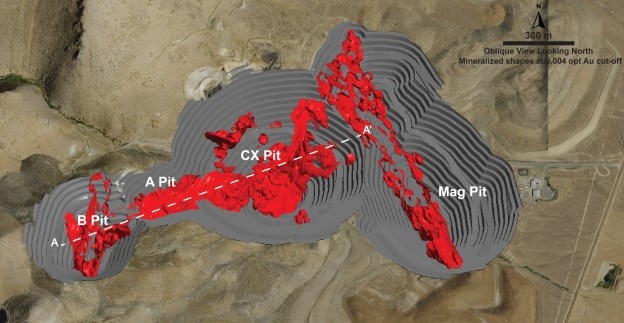

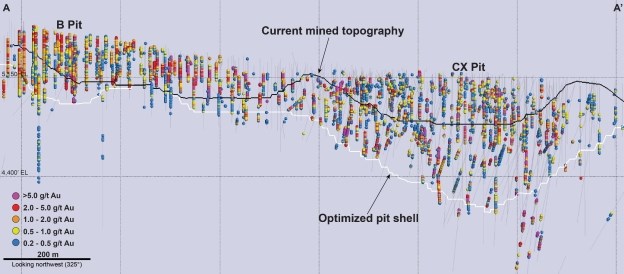

The PEA includes an updated mineral resource estimate with a total of 261,000 ounces of gold at 10.5 g/t Au in the measured and indicated categories and 326,000 ounces of gold at 13.0 g/t Au in the inferred category (see Table 2) hosted in the CX, Ogee, Otto and South Pacific zones (see Figures 1 and 2). The updated resource incorporates all drilling conducted on the underground zones to the end of 2022.

The resource estimate was prepared using stope optimization software resulting in additional mineralized body constraints. Stope optimization provides greater accuracy than previous estimation techniques and has become industry standard for underground deposits in Nevada.

Further exploration at Granite Creek Underground includes infill drilling program in the Ogee, Otto and South Pacific zones in 2023 and 2024. Additionally, a 15,000-meter infill and step out drill program targeting the South Pacific Zone, is aimed at expanding the South Pacific resource and moving a portion of the indicated mineral resources to reserves in that zone. Construction of an underground exploration drift is underway to provide drill access to the northern and down-dip extensions of the South Pacific Zone, with completion anticipated in Q2 2025.

All drilling conducted since the beginning of 2023 is anticipated to be included in the planned feasibility study for Granite Creek Underground.

Figure 1: Granite Creek Underground Project Plan View

Figure 2: Granite Creek Underground Longitudinal Section

Table 2: Granite Creek Underground Mineral Resource Estimate Statement as of December 31, 2024

|

Measured and Indicated Mineral Resources

|

|

Class

|

Zone

|

Tonnes

|

Au

|

Au

|

|

(000s)

|

(g/t)

|

(000s oz)

|

|

Measured

|

CX

|

|

|

|

|

Ogee

|

80

|

8.4

|

22

|

|

Otto

|

53

|

8.8

|

15

|

|

Total Measured

|

133

|

8.5

|

37

|

|

Indicated

|

CX

|

7

|

13.4

|

3

|

|

Ogee

|

164

|

12.1

|

64

|

|

Otto

|

268

|

10.8

|

93

|

|

South Pacific

|

203

|

9.8

|

64.0

|

|

Total Indicated

|

641

|

10.9

|

224

|

|

Total Measured & Indicated

|

775

|

10.5

|

261

|

|

|

|

|

|

|

|

Inferred Mineral Resources

|

|

Class

|

Zone

|

Tonnes

|

Au

|

Au

|

|

(000s)

|

(g/t)

|

(000s oz)

|

|

Inferred

|

CX

|

88

|

12.0

|

34

|

|

Ogee

|

38

|

19.3

|

24

|

|

Otto

|

170

|

13.7

|

75

|

|

South Pacific

|

486

|

12.4

|

194

|

|

|

Total Inferred

|

782

|

13.0

|

326

|

|

I. Notes to table above:

II. Mineral resources have been estimated at a gold price of $2,175 per troy ounce;

III. Mineral resources have been estimated using gold metallurgical recoveries ranging from 85.2 to 94.2% for pressure oxidation and 40-70% for carbon-in-leach ("CIL") toll processing;

IV. Pressure oxidation cutoff grades range from 5.40 to 7.58 Au g/t (0.157 to 0.221 opt). The cutoff grade for CIL processing under the mineralized material sales agreement is 5.85 g/t (0.171 opt);

V. The effective date of the mineral resource estimate is December 31, 2024;

VI. Mineral resources include drilling completed prior to December 31, 2022;

VII. Mineral resources, which are not mineral reserves, do not have demonstrated economic viability. The estimate of mineral resources may be materially affected by environmental, permitting, legal, title, socio-political, marketing, or other relevant factors;

VIII. An inferred mineral resource is that part of a mineral resource for which quantity and grade or quality are estimated on the basis of limited geological evidence and sampling. Geological evidence is sufficient to imply but not verify geological and grade or quality continuity. An inferred mineral resource has a lower level of confidence than that applying to an indicated mineral resource and must not be converted to a mineral reserve. It is reasonably expected that the majority of inferred mineral resources could be upgraded to indicated mineral resources with continued exploration; and

IX. The reference point for mineral resources is in situ.

|

Economic Analysis

The Project's NPV relation to fluctuations in the long-term gold price are outlined in Table 3.

Table 3: Granite Creek Underground Gold Price Sensitivity After-tax Analysis

|

|

|

Gold Price ($/oz)

|

|

|

|

$1,850

|

$2,000

|

$2,175

|

$2,500

|

$2,750

|

$2,900

|

$3,000

|

|

NPV5%

|

($M)

|

$74

|

$112

|

$155

|

$236

|

$301

|

$344

|

$373

|

Project Overview

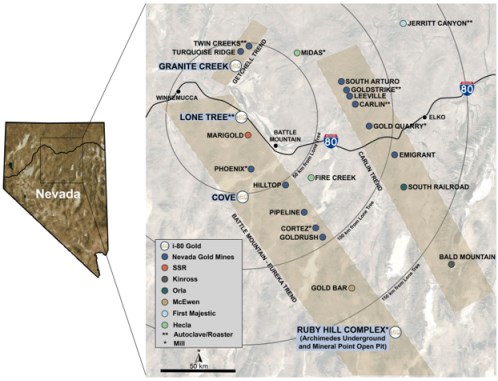

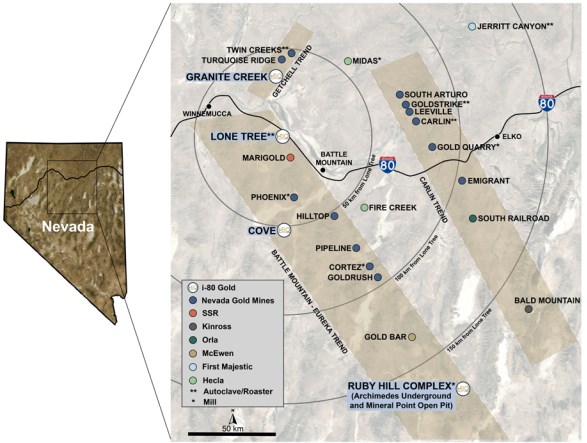

Granite Creek Underground is a fully permitted, constructed and operating mine currently in production ramp up phase. The Granite Creek property (the "Property") also includes Granite Creek Open Pit deposit adjacent to the underground mine, currently in the permitting stage. The Property is located at the intersection of the highly prolific Battle Mountain-Eureka and Getchell gold trends, near Nevada Gold Mines' Turquoise Ridge Complex (see Figure 3). Situated in the Potosi mining district, the Property lies approximately 43 km northwest of Winnemucca, within Humboldt County, Nevada.

Since 1980, the Property has produced approximately one million ounces of gold from both underground and open pit. The majority of underground resources are adjacent to, but independent of the past-producing open pits on the property. Additionally, the Property hosts the Mag and CX oxide open pit resources. An open pit resource estimate and associated preliminary economic assessment is currently planned for Q4 2025.

Figure 3: i-80 Gold Regional Map

Geology and Mineralization

Mineralization at Granite Creek is Carlin-type, with gold hosted in fine-grained arsenian pyrite similar to nearby deposit at the Turquoise Ridge Complex which hosts approximately 20 million measured and indicated ounces of gold(4) . The primary host rocks at Granite Creek are interbedded shale, siltstone, and limestone of the Ordovician Comus Formation. Higher-grade mineralization is found underground, proximal to the Cretaceous Osgood Mountains stock where the Comus Formation has been metamorphosed to marble and hornfels. Mineralization is strongly structurally controlled, typically by inverted thrust faults trending north to northeast. i-80 Gold has conducted significant exploration since acquiring the property in 2021 which led to the discovery of the South Pacific Zone, a northeastern extension of the existing underground deposit.

Mining and Processing

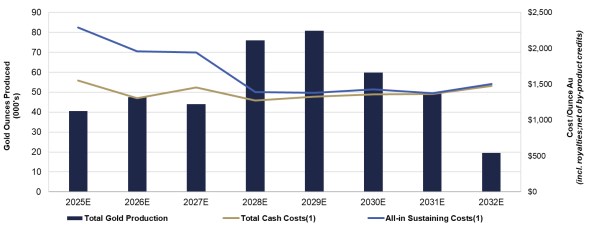

Granite Creek Underground is currently ramping up to full production and is expected to achieve commercial production in 2026. The PEA demonstrates an initial mine life of approximately 8 years with annual gold production peaking at approximately 80,000 ounces and averaging approximately 60,000 ounces of gold following ramp up. A third-party process agreement for material mined is required until the planned refurbishment of the Lone Tree autoclave is expected to be completed. As a result, annual production and cash flows are lower over the next three years until the autoclave facility is completed.

The PEA is based on a mineral resource estimate derived from drilling data through to the end of 2022 and should not be relied upon for production forecasts in 2025. The revised plan for this year, which is still under development, incorporates updated near-mine drilling information and a revised budget. The Company anticipates recovered gold ounces of between 20,000 to 30,000 ounces in 2025 from Granite Creek. An updated operational plan will be included in the feasibility study for Granite Creek Underground, which is currently expected to be released in Q4 2025.

Underground access is through portals located in the north wall of the CX pit. The main decline provides personnel and equipment access to all areas of the mine and can accommodate 30-ton haul trucks.

The majority of mining will be conducted using underhand drift and fill methods, optimized for the site's ground conditions. Drift widths will be maintained at 5 meters or less to minimize dilution and enhance recovery. Underhand drift and fill mining is well suited for the ground conditions at Granite Creek and allows for a high degree of selectivity, productivity, and safety for mine personnel. This mining method also results in backfill with superior geotechnical quality compared to the in-situ rock.

Decline development has reached the 4100-foot elevation and has developed through over 700 vertical feet of mineralization. Ultimately, the decline will extend to the 3200-foot elevation and will provide access to all four mineralized zones.

While a small component of the upper levels of the Ogee zone contains oxide mineralization, metallurgical testing has demonstrated that the Ogee, Otto and South Pacific zones of the Granite Creek Underground are generally single refractory and require an oxidation process to increase gold extraction using cyanidation of mineralized material. Additionally, testing has demonstrated that gold recovery for the Ogee and South Pacific Zone deposits have better economic recovery when an autoclave is operated in the alkaline environment, while the Otto deposit achieves better economic recovery in the acidic environment.

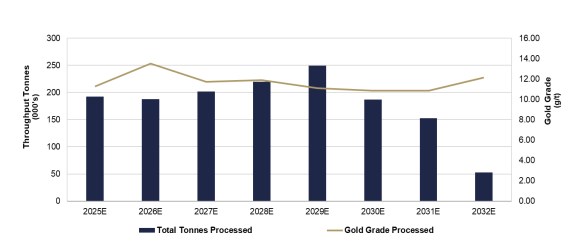

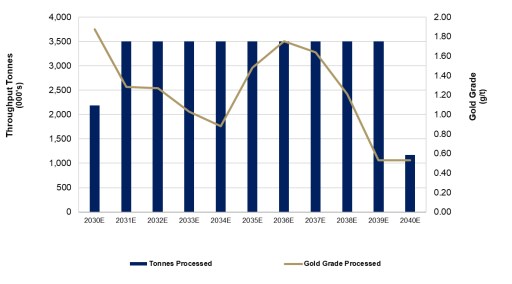

The PEA incorporates mineralized material sales arrangements and associated over-the-road trucking costs for the years 2025 through 2027. Starting in 2028, the anticipated processing costs and recoveries associated with hauling to and processing at the Company's Lone Tree autoclave(3) in the acidic or alkaline environment have been incorporated into this Study. Processing materials in the acidic environment increases per tonne processing costs by approximately $35; however, the additional cost is offset by higher recovery rates. Oxide mineralization from the upper levels will be sold to a third party under an existing sales agreement. A LOM processing schedule is illustrated in Figure 4.

Granite Creek Hydrology Update

i-80 Gold has dedicated significant resources to understand and resolve challenges encountered due to ground water at the Granite Creek Underground mine which has negatively impacted mining development. In Q3 2023 a water treatment plant was constructed to treat water from the lower dewatering wells and underground contact water, and the plant is now successfully treating dewatering water for deleterious content. Further, in 2024 an extensive underground network of piping, pumps, and sumps were installed to handle the underground contact water.

Going forward the extensive hydrological studies conducted should enable the Company to execute on its mining development plans. In February 2025, a predictive groundwater model was completed for the mine. The groundwater model is expected to allow i-80 Gold to assess various predictive scenarios prior to installing dewatering wells and the required infrastructure to meet its dewatering needs.

Figure 4: LOM Processing Schedule

Capital Cost Summary

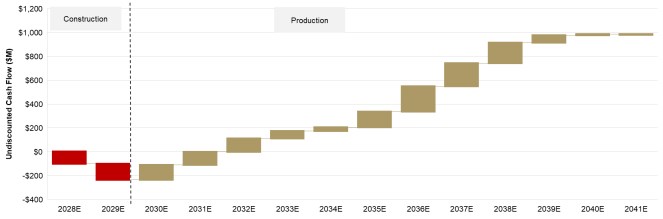

The Project is a former producing mine with a large portion of the necessary infrastructure in place. LOM sustaining capital is estimated at $105 million, with approximately 65% allocated to ongoing capital development.

Granite Creek Underground is expected to generate an estimated $197 million in after-tax cash flow over the current mine life (see Figure 5).

Table 4: LOM Capital Cost Estimates

|

|

Sustaining

Capital

|

|

($M)

|

|

Dewatering

|

$9.4

|

|

Mine Development

|

$58.9

|

|

Mine Facilities & Overhead

|

$5.5

|

|

Definition & Conversion Drilling

|

$16.0

|

|

Contingency

(15% Mine Development and Drilling; 25% Facilities)

|

$15.0

|

|

Total

|

$104.8

|

Figure 5: Granite Creek Underground LOM Annual Cash Flow

Operating Cost Summary

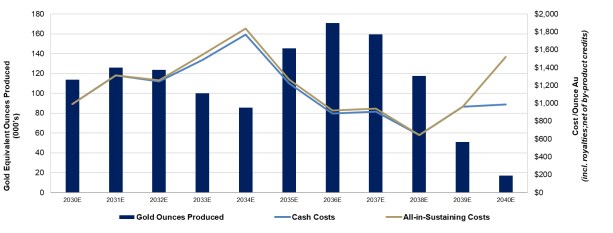

The PEA estimates cash costs(1) of $1,366 per ounce of gold and all-in sustaining costs(1) of $1,597 per ounce of gold for the LOM (see Table 5).

The annual cash waterfall above in Figure 5 demonstrates the importance of the planned refurbishment of the Company's Lone Tree autoclave which is expected to increase production and cash flows in 2028 following its planned commissioning.

Figure 6 illustrates these operating costs over the Project's estimated production profile.

Table 5: Total and Unit Operating Costs

|

|

Total Costs

|

Unit Cost

|

Cost per Ounce

|

|

($M)

|

($/t milled)

|

($/oz Au)

|

|

Mining

|

$331.7

|

$230.1

|

$794

|

|

Transportation & Processing

|

$98.8

|

$68.5

|

$237

|

|

G&A, Royalties(5) & Net Proceeds Tax

|

$140.0

|

$97.1

|

$335

|

|

Total Operating Cost/Cash Costs(1)

|

$570.5

|

$395.6

|

$1,366

|

|

Closure & Reclamation

|

$7.4

|

$5.1

|

$18

|

|

Sustaining Capital (includes contingency)(6)

|

$88.8

|

$61.6

|

$213

|

|

All-in Sustaining Costs(1)

(excludes Definition & Conversion Drilling)

|

$666.6

|

$462.4

|

$1,597

|

Figure 6: Granite Creek Underground LOM Gold Production Profile vs Cost per Ounce

Table 6: Development Cost Per Foot

|

|

Total Development

|

Cost

|

|

(feet)

|

($/foot)

|

|

Primary Capital Drifting

|

21,515

|

$2,300

|

|

Capital Raising

|

2,350

|

$4,000

|

|

Total/Weighted Average

|

23,865

|

$2,467

|

|

Excludes Contingency

|

|

|

Permitting

The Granite Creek Underground mine is fully permitted. The primary focus for the Granite Creek Underground operations remains compliance and reporting requirements associated with existing site permits. Other than potential minor modifications to existing site permits for operational purposes, no other major permitting actions are expected in the foreseeable future.

Next Steps to Feasibility Study

A feasibility study in accordance with National Instrument 43-101 - Standards of Disclosure for Mineral Projects ("NI 43-101") and Subpart 1300 of Regulation S-K ("S-K 1300") with an updated mineral resource estimate which is currently expected to be completed in Q4 2025. In addition to the infilling drilling conducted in 2023 and 2024, the updated resource is expected to include 15,000 meters of infill and step out drilling targeting the South Pacific Zone. Below is a summary of additional work to be conducted.

Resource Delineation and Exploration

• Begin resource conversion and step out drilling as the exploration drift advances and drill platforms become available. Incorporate this data into an updated resource model.

Technical Disclosure and Qualified Persons

The PEA was prepared in accordance with NI 43-101. The PEA will be filed within 45 days of the press release under the Company's issuer profile on SEDAR+ at www.sedarplus.ca. An Initial Assessment for the Granite Creek Underground ("S-K 1300 Report") was also prepared in accordance with S-K 1300 and Item 601 of the Regulation S-K and the S-K 1300 Report will be filed on EDGAR at www.sec.gov. Both reports will be available on the Company's website at www.i80gold.com. The mineral estimates and project economics are the same under the PEA and the S-K 1300 Report.

The technical information contained in this press release has been prepared under the supervision of, and has been reviewed and approved by Dagny Odell, P.E., (NV 13708 & SME No. 2402150) Practical Mining LLC, and Tyler Hill CPG., Vice President Geology for the Company, who are all qualified persons within the meaning of NI 43-101 and S-K 1300.

For a description of the data verification, assay procedures and the quality assurance program and quality control measures applied by the Company, please see the Company's Annual Information Form dated March 12, 2024 filed under the Company's profile on SEDAR+ at www.sedarplus.ca and filed with the Company's Form 40-F under the Company's profile on EDGAR at www.sec.gov. Further information about the PEA referenced in this news release, including information in respect of data verification, key assumptions, parameters, risks and other factors, will be contained in the PEA.

The PEA is preliminary in nature and includes an economic analysis that is based, in part, on inferred mineral resources. Inferred mineral resources that are considered too speculative geologically to have for the application of economic considerations applied to them that would enable them to be categorized as mineral reserves, and there is no certainty that the results of the PEA will be realized. Mineral resources do not have demonstrated economic viability and are not mineral reserves.

Endnotes

(1) This is a non-IFRS/non-GAAP measure. Please see the section titled "Non-IFRS Performance Measures/Non-GAAP Financial Performance Measures" below.

(2) Cash flow and NPV are calculated as of January 2025.

(3) Following the completion of a planned refurbishment class 3 engineering study, a series of trade-off scenarios will be considered comparing full autoclave refurbishment to alternate toll milling and purchase agreement options that could potentially be available to the Company.

(4) Turquoise Ridge Complex gold mineral resource estimate of approximately 20 million ounces (110 Mt at 5.42 g/t Au) as at December 31, 2023 based on publicly filed technical reports of Barrick Gold Corporation available on SEDAR+ at www.sedarplus.ca and www.barrick.com. No qualified person of the Company has independently verified any mineral resource information in respect of the Turquoise Ridge Complex contained in this news release and such information is not necessarily indicative of the mineralization on the property subject to such technical reports.

(5) Royalties include a 10% net profits interest to Gold Royalty Corp.

(6) Includes contingency of $15 million.

About i-80 Gold Corp.

i-80 Gold Corp. is a Nevada-focused mining company committed to building a mid-tier gold producer through a new development plan to advance its high-quality asset portfolio. The Company is the fourth largest gold mineral resource holder in the state with a pipeline of high-grade development and production-stage projects strategically located in Nevada's most prolific gold-producing trends. Leveraging its fully permitted central processing facility, i-80 Gold is executing a hub-and-spoke regional mining and processing strategy to maximize efficiency and growth. i-80 Gold's shares are listed on the Toronto Stock Exchange (TSX: IAU) and the NYSE American (NYSE: IAUX). For more information, visit www.i80gold.com.

For further information, please contact:

Leily Omoumi, VP Corporate Development & Strategy

1.866.525.6450

info@i80gold.com

www.i80gold.com

Forward-Looking Information

Certain statements in this release constitute "forward-looking statements" or "forward-looking information" within the meaning of applicable securities laws, including but not limited to, statements regarding the updated results of the PEA on the Project, such as future estimates of internal rates of return, net present value, future production, estimates of cash cost, proposed mining plans and methods, mine life estimates, cash flow forecasts, metal recoveries, estimates of capital and operating costs, timing for permitting and environmental assessments, timing, completion and results of feasibility studies, and the size and timing of phased development of the Project. Furthermore, forward-looking statements are necessarily based upon a number of estimates and assumptions that, while considered reasonable by the Company as of the date of such statements, are inherently subject to significant business, economic and competitive uncertainties and contingencies. With respect to this specific forward-looking information concerning the development of the Project, the Company has based its assumptions and analysis on certain factors that are inherently uncertain. Uncertainties include: (i) the adequacy of infrastructure; (ii) geological characteristics; (iii) metallurgical characteristics of the mineralization; (iv) the ability to develop adequate processing capacity; (v) the price of gold, silver and other commodities; (vi) the availability of equipment and facilities necessary to complete development; (vii) the cost of consumables and mining and processing equipment; (viii) unforeseen technological and engineering problems; (ix) natural disasters and/or accidents; (x) currency fluctuations; (xi) changes in regulations; (xii) the compliance by and/or key suppliers with terms of agreements; (xiii) the availability and productivity of skilled labour; (xiv) the regulation of the mining industry by various governmental agencies, including permitting and environmental assessments; (xv) the ability to raise sufficient capital to develop such projects; (xiv) changes in project scope or design; and (xv) political factors.

Such statements can be identified by the use of words such as "may", "would", "could", "will", "intend", "expect", "believe", "plan", "anticipate", "estimate", "scheduled", "forecast", "predict" and other similar terminology, or state that certain actions, events or results "may", "could", "would", "might" or "will" be taken, occur or be achieved. These statements reflect the Company's current expectations regarding future events, performance and results and speak only as of the date of this release and are expressly qualified in their entirety by this cautionary statement. Subject to applicable securities laws, the Company does not assume any obligation to update or revise the forward-looking statements contained herein to reflect events or circumstances occurring after the date of this release.

This release also contains references to estimates of mineral resources. The estimation of mineral resources is inherently uncertain and involves subjective judgments about many relevant factors. Mineral resources that are not mineral reserves do not have demonstrated economic viability. The accuracy of any such estimates is a function of the quantity and quality of available data, and of the assumptions made and judgments used in engineering and geological interpretation (including estimated future production from the Project, the anticipated tonnages and grades that will be mined and the estimated level of recovery that will be realized), which may prove to be unreliable and depend, to a certain extent, upon the analysis of drilling results and statistical inferences that may ultimately prove to be inaccurate. Mineral resource estimates may have to be re-estimated based on: (i) fluctuations in commodities prices; (ii) results of drilling, (iii) metallurgical testing and other studies; (iv) proposed mining operations, including dilution; (v) the evaluation of mine plans subsequent to the date of any estimates; and (vi) the possible failure to receive required permits, approvals and licenses or changes to existing mining licenses.

Forward-looking statements and information involve significant known and unknown risks and uncertainties, should not be read as guarantees of future performance or results and will not necessarily be accurate indicators of whether or not such results will be achieved. A number of factors could cause actual results to differ materially from the results expressed or implied by such forward-looking statements or information, including, but not limited to: the Company's ability to finance the development of its mineral properties; assumptions and discount rates being appropriately applied to the PEA and S-K 1300 Report, uncertainty as to whether there will ever be production at the Company's mineral exploration and development properties; risks related to the Company's ability to commence production at the Project and generate material revenues or obtain adequate financing for its planned exploration and development activities; uncertainties relating to the assumptions underlying resource and reserve estimates; mining and development risks, including risks related to infrastructure, accidents, equipment breakdowns, labour disputes, bad weather, non-compliance with environmental and permit requirements or other unanticipated difficulties with or interruptions in development, construction or production; the geology, grade and continuity of the Company's mineral deposits; the uncertainties involving success of exploration, development and mining activities; permitting timelines; government regulation of mining operations; environmental risks; unanticipated reclamation expenses; prices for energy inputs, labour, materials, supplies and services; uncertainties involved in the interpretation of drilling results and geological tests and the estimation of reserves and resources; unexpected cost increases in estimated capital and operating costs; the need to obtain permits and government approvals; material adverse changes, unexpected changes in laws, rules or regulations, or their enforcement by applicable authorities; the failure of parties to contracts with the company to perform as agreed; social or labour unrest; changes in commodity prices; and the failure of exploration programs or studies to deliver anticipated results or results that would justify and support continued exploration, studies, development or operations. For a more detailed discussion of such risks and other factors that could cause actual results to differ materially from those expressed or implied by such forward-looking statements, refer to i-80 Gold's filings with Canadian securities regulators, including the most recent Annual Information Form, available on SEDAR+ at www.sedarplus.ca.

Non-IFRS/Non-GAAP Financial Performance Measures

The Company has included certain terms or performance measures in this news release that commonly used in the gold mining industry that are not defined under International Financial Reporting Standards ("IFRS") or United States Generally Accepted Accounting Principles ("US GAAP"). This includes: all-in sustaining costs per ounce and cash cost per ounce. Non-IFRS/Non-GAAP financial performance measures do not have any standardized meaning prescribed under IFRS or US GAAP, and therefore, they may not be comparable to similar measures employed by other companies. The data presented is intended to provide additional information and should not be considered in isolation or as a substitute for measures prepared in accordance with IFRS US GAAP and should be read in conjunction with the Company's financial statements. Because the Company has provided these measures on a forward-looking basis, it is unable to present a quantitative reconciliation to the most directly comparable financial measure calculated and presented in accordance with IFRS or US GAAP without unreasonable efforts. This is due to the inherent difficulty of forecasting the timing or amount of various reconciling items that would impact the most directly comparable forward-looking IFRS or US GAAP measure that have not yet occurred, are outside of the Company's control and/or cannot be reasonably predicted.

Definitions

"All-in sustaining costs" is a non-IFRS or US GAAP financial measure calculated based on guidance published by the World Gold Council ("WGC"). The WGC is a market development organization for the gold industry and is an association whose membership comprises leading gold mining companies. Although the WGC is not a mining industry regulatory organization, it worked closely with its member companies to develop these metrics. Adoption of the all-in sustaining cost metric is voluntary and not necessarily standard, and therefore, this measure presented by the Company may not be comparable to similar measures presented by other issuers. The Company believes that the all-in sustaining cost measure complements existing measures and ratios reported by the Company. All-in sustaining cost includes both operating and capital costs required to sustain gold production on an ongoing basis. Sustaining operating costs represent expenditures expected to be incurred at the Project that are considered necessary to maintain production. Sustaining capital represents expected capital expenditures comprising mine development costs, including capitalized waste, and ongoing replacement of mine equipment and other capital facilities, and does not include expected capital expenditures for major growth projects or enhancement capital for significant infrastructure improvements.

"Cash cost per gold ounce" is a common financial performance measure in the gold mining industry but has no standard meaning under IFRS or US GAAP. The Company believes that, in addition to conventional measures prepared in accordance with IFRS or US GAAP, certain investors use this information to evaluate the Company's performance and ability to generate cash flow. Cash cost figures are calculated in accordance with a standard developed by The Gold Institute. The Gold Institute ceased operations in 2002, but the standard is considered the accepted standard of reporting cash cost of production in North America. Adoption of the standard is voluntary, and the cost measures presented may not be comparable to other similarly titled measures of other companies.

For a more detailed breakdown on how these measures were calculated, please see the table below:

|

|

Total Costs

|

Unit Cost

|

Cost per Ounce

|

|

($M)

|

($/t milled)

|

($/oz Au)

|

|

Mining

|

$331.7

|

$230.1

|

$794

|

|

Transportation & Processing

|

$98.8

|

$68.5

|

$237

|

|

G&A, Royalties(5) & Net Proceeds Tax

|

$140.0

|

$97.1

|

$335

|

|

Total Operating Cost/Cash Costs(1)

|

$570.5

|

$395.6

|

$1,366

|

|

Closure & Reclamation

|

$7.4

|

$5.1

|

$18

|

|

Sustaining Capital (includes contingency)(6)

|

$88.8

|

$61.6

|

$213

|

|

All-in Sustaining Costs(1)

(excludes Definition & Conversion Drilling)

|

$666.6

|

$462.4

|

$1,597

|

APPENDIX

Granite Greek Underground Project Detailed Cash Flow Model

| Granite Creek Underground |

UNITS |

TOTAL

LOM |

2025E |

2026E |

2027E |

2028E |

2029E |

2030E |

2031E |

2032E |

2033E |

2034E |

2035+1 |

| |

|

|

|

|

|

|

|

|

|

|

|

|

|

| MINING |

|

|

|

|

|

|

|

|

|

|

|

|

|

| Mine Life |

Years |

~8 |

|

|

|

|

|

|

|

|

|

|

|

Mineralized Material Mined

(incl. marginal) |

k tonnes |

1,442 |

192.7 |

187.6 |

201.3 |

219.7 |

248.9 |

186.5 |

152.2 |

53.0 |

- |

- |

- |

| Waste Moved |

k tonnes |

684 |

104.3 |

90.6 |

100.9 |

100.6 |

112.7 |

81.2 |

68.6 |

25.4 |

- |

- |

|

| Total Moved |

k tonnes |

2,126 |

297.0 |

278.2 |

302.3 |

320.3 |

361.6 |

267.7 |

220.8 |

78.5 |

- |

- |

- |

| |

|

|

|

|

|

|

|

|

|

|

|

|

|

| Daily Mining Rate |

tpd |

494 |

527.9 |

513.8 |

551.6 |

602.0 |

681.9 |

510.8 |

416.9 |

145.3 |

- |

- |

- |

| |

|

|

|

|

|

|

|

|

|

|

|

|

|

| Backfill Placed |

k tonnes |

1,442 |

192.7 |

187.6 |

201.3 |

219.7 |

248.9 |

186.5 |

152.2 |

53.0 |

- |

- |

|

| Capitalized Mining |

k tonnes |

489 |

163.5 |

182.9 |

105.6 |

35.0 |

1.0 |

1.0 |

- |

- |

- |

|

|

| |

|

|

|

|

|

|

|

|

|

|

|

|

|

| PROCESSING |

|

|

|

|

|

|

|

|

|

|

|

|

|

Total Material for

Processing |

k tonnes |

1,442 |

193 |

188 |

201 |

220 |

249 |

186 |

152 |

53 |

- |

- |

- |

| Gold Average Grade |

g/t Au |

11.6 |

11.26 |

13.51 |

11.71 |

11.87 |

11.11 |

10.84 |

10.83 |

12.13 |

- |

- |

- |

| Contained Gold |

'000 oz Au |

538 |

69.7 |

81.4 |

75.8 |

83.9 |

88.9 |

65.0 |

53.0 |

20.7 |

- |

- |

- |

| |

|

|

|

|

|

|

|

|

|

|

|

|

|

| Toll Mill Processing |

|

|

|

|

|

|

|

|

|

|

|

|

|

| Total Tonnes Processed |

k tonnes |

573 |

192 |

180 |

201 |

|

|

|

|

|

|

|

|

| Gold Grade |

g/t Au |

12.09 |

11.25 |

13.44 |

11.67 |

|

|

|

|

|

|

|

|

| Contained Gold |

'000 oz Au |

223 |

69.4 |

77.9 |

75.2 |

|

|

|

|

|

|

|

|

| Gold Average Recovery |

% |

58% |

58% |

58% |

58% |

|

|

|

|

|

|

|

|

| Recovered Gold |

'000 oz Au |

129 |

40.3 |

45.2 |

43.6 |

|

|

|

|

|

|

|

|

| |

|

|

|

|

|

|

|

|

|

|

|

|

|

| Autoclave Processing |

|

|

|

|

|

|

|

|

|

|

|

|

|

| Total Tonnes Processed |

k tonnes |

853 |

|

|

|

217 |

246 |

184 |

152 |

53 |

- |

- |

- |

| Gold Grade |

g/t Au |

11.21 |

|

|

|

11.79 |

11.04 |

10.82 |

10.83 |

12.13 |

- |

- |

- |

| Contained Gold |

'000 oz Au |

307 |

|

|

|

82.4 |

87.5 |

63.9 |

53.0 |

20.7 |

- |

- |

- |

| Gold Average Recovery |

% |

92% |

|

|

|

92% |

92% |

92% |

92% |

92% |

- |

- |

- |

| Recovered Gold |

'000 oz Au |

283 |

|

|

|

75.0 |

79.7 |

59.0 |

49.4 |

19.5 |

- |

- |

- |

| |

|

|

|

|

|

|

|

|

|

|

|

|

|

| Granite Creek Underground |

UNITS |

TOTAL

LOM |

2025E |

2026E |

2027E |

2028E |

2029E |

2030E |

2031E |

2032E |

2033E |

2034E |

2035+1 |

| CIL Processing |

|

|

|

|

|

|

|

|

|

|

|

|

|

(Third-party purchase

agreement) |

|

|

|

|

|

|

|

|

|

|

|

|

|

| Total Tonnes Processed |

k tonnes |

16 |

1 |

7 |

1 |

2 |

3 |

3 |

- |

- |

- |

- |

|

| Gold Grade |

g/t Au |

15.95 |

13.99 |

15.17 |

20.84 |

19.64 |

17.44 |

12.72 |

- |

- |

- |

- |

|

| Contained Gold |

'000 oz Au |

8.4 |

0.3 |

3.5 |

0.5 |

1.4 |

1.4 |

1.1 |

- |

- |

- |

- |

|

| Gold Average Recovery |

% |

68% |

68% |

68% |

68% |

68% |

68% |

68% |

- |

- |

- |

- |

|

| Recovered Gold |

'000 oz Au |

6 |

0.22 |

2.4 |

0.4 |

1.0 |

1.0 |

0.7 |

- |

- |

- |

- |

|

| |

|

|

|

|

|

|

|

|

|

|

|

|

|

| Total Tonnes Processed |

k tonnes |

1,442 |

192.7 |

187.6 |

201.3 |

219.7 |

248.9 |

186.5 |

152.2 |

53.0 |

- |

- |

- |

| Total Gold Production(3) |

'000 oz Au |

417.5 |

40.5 |

47.6 |

44.0 |

76.0 |

80.7 |

59.8 |

49.4 |

19.5 |

- |

- |

- |

| |

|

|

|

|

|

|

|

|

|

|

|

|

|

| REVENUE |

|

|

|

|

|

|

|

|

|

|

|

|

|

| Gold Price |

US$/oz Au |

$2,175 |

$2,175 |

$2,175 |

$2,175 |

$2,175 |

$2,175 |

$2,175 |

$2,175 |

$2,175 |

$2,175 |

$2,175 |

$2,175 |

| Silver Price |

US$/oz Ag |

$27.25 |

$27.25 |

$27.25 |

$27.25 |

$27.25 |

$27.25 |

$27.25 |

$27.25 |

$27.25 |

$27.25 |

$27.25 |

$27.25 |

| Revenues |

US$M |

$908 |

$88 |

$103 |

$96 |

$165 |

$176 |

$130 |

$107 |

$42 |

- |

- |

- |

| OPERATING COSTS |

|

|

|

|

|

|

|

|

|

|

|

|

|

| Mining Costs (Mineralized Material incl. Backfill) |

US$M |

$236 |

$31.5 |

$30.7 |

$33.0 |

$36.0 |

$40.8 |

$30.5 |

$24.9 |

$8.7 |

- |

- |

- |

| Mining Costs (Waste) |

US$M |

$83 |

$12.7 |

$11.0 |

$12.3 |

$12.3 |

$13.7 |

$9.9 |

$8.4 |

$3.1 |

- |

- |

- |

| Processing Autoclave |

US$M |

$77 |

- |

- |

- |

$20.2 |

$23.0 |

$16.9 |

$13.2 |

$4.1 |

- |

- |

- |

| Transportation |

US$M |

$21 |

$1.7 |

$1.7 |

$1.8 |

$4.1 |

$4.7 |

$3.5 |

$2.9 |

$1.0 |

- |

- |

- |

| Electrical Power |

US$M |

$12 |

$1.3 |

$1.4 |

$1.6 |

$1.7 |

$1.7 |

$1.7 |

$1.5 |

$1.2 |

- |

- |

- |

| G&A |

US$M |

$64 |

$8.6 |

$8.6 |

$7.7 |

$7.7 |

$7.7 |

$7.7 |

$7.7 |

$7.7 |

- |

- |

- |

| Total Operating Cost |

US$M |

$494 |

$55.9 |

$53.5 |

$56.4 |

$82.1 |

$91.6 |

$70.3 |

$58.5 |

$25.9 |

- |

- |

- |

| |

|

|

|

|

|

|

|

|

|

|

|

|

|

| Refining & Sales |

US$M |

$0.8 |

$0.1 |

$0.1 |

$0.1 |

$0.1 |

$0.1 |

$0.1 |

$0.1 |

$0.0 |

- |

- |

- |

| Royalties & State Taxes(4) |

US$M |

$75.5 |

$6.8 |

$8.6 |

$7.5 |

$14.8 |

$15.5 |

$10.7 |

$8.7 |

$2.9 |

- |

- |

- |

| |

|

|

|

|

|

|

|

|

|

|

|

|

|

Mining Costs

(Mineralized Material) |

US$/t mined |

$163.7 |

$164 |

$164 |

$164 |

$164 |

$164 |

$164 |

$164 |

$164 |

- |

- |

- |

| Mining Costs (Waste) |

US$/t mined |

$121.9 |

$122 |

$122 |

$122 |

$122 |

$122 |

$122 |

$122 |

$122 |

- |

- |

- |

| Granite Creek Underground |

UNITS |

TOTAL

LOM |

2025E |

2026E |

2027E |

2028E |

2029E |

2030E |

2031E |

2032E |

2033E |

2034E |

2035+1 |

| Mining Costs (Mineralized material & Waste ) |

US$/t mined |

$150.3 |

$149 |

$150 |

$150 |

$151 |

$151 |

$151 |

$151 |

$150 |

- |

- |

- |

| Processing (Heap leach) |

US$/t milled |

$0.0 |

- |

- |

- |

- |

- |

- |

- |

- |

- |

- |

- |

| Processing (Autoclave) |

US$/t milled |

$90.8 |

- |

- |

- |

$93 |

$93 |

$92 |

$87 |

$78 |

- |

- |

- |

| Transportation |

US$/t milled |

$14.8 |

$9 |

$9 |

$9 |

$19 |

$19 |

$19 |

$19 |

$19 |

- |

- |

- |

| Electrical Power |

US$/t milled |

$8.5 |

$7 |

$7 |

$8 |

$8 |

$7 |

$9 |

$10 |

$23 |

- |

- |

- |

| G&A |

US$/t milled |

$44.2 |

$45 |

$46 |

$38 |

$35 |

$31 |

$42 |

$51 |

$146 |

- |

- |

- |

| |

|

|

|

|

|

|

|

|

|

|

|

|

|

| Total |

US$/t milled |

$342.7 |

$290 |

$285 |

$280 |

$374 |

$368 |

$377 |

$385 |

$488 |

- |

- |

- |

| |

|

|

|

|

|

|

|

|

|

|

|

|

|

| CAPITAL EXPENDITURES |

|

|

|

|

|

|

|

|

|

|

|

|

|

| Construction Capital |

US$M |

$0.0 |

|

|

|

|

|

|

|

|

|

|

|

Definition & Conversion

Drilling |

US$M |

$16.0 |

$6.0 |

$2.0 |

$2.0 |

$2.0 |

$2.0 |

$2.0 |

- |

- |

- |

- |

- |

| Sustaining Capital |

US$M |

$88.8 |

$29.5 |

$30.4 |

$19.0 |

$6.4 |

$1.7 |

$1.7 |

- |

- |

- |

- |

- |

| Total Capital |

US$M |

$104.8 |

$35.5 |

$32.4 |

$21.0 |

$8.4 |

$3.7 |

$3.7 |

- |

- |

- |

- |

- |

| Reclamation |

US$M |

$7.4 |

$0.5 |

$0.5 |

$0.5 |

$0.5 |

$0.5 |

$0.5 |

$0.5 |

$0.5 |

$0.4 |

$0.4 |

$2.5 |

| |

|

|

|

|

|

|

|

|

|

|

|

|

|

| CASH COSTS & AISC |

|

|

|

|

|

|

|

|

|

|

|

|

|

Total Cash Costs (Inc.

Royalty)(1) |

US$/oz |

$1,366 |

$1,551 |

$1,307 |

$1,455 |

$1,275 |

$1,328 |

$1,357 |

$1,363 |

$1,479 |

- |

- |

- |

| All-in Sustaining Costs(1)(5) |

US$/oz |

$1,597 |

$2,292 |

$1,957 |

$1,899 |

$1,366 |

$1,356 |

$1,395 |

$1,374 |

$1,506 |

- |

- |

- |

| |

|

|

|

|

|

|

|

|

|

|

|

|

|

| CASH FLOW ANALYSIS |

|

|

|

|

|

|

|

|

|

|

|

|

|

| Revenue |

US$M |

$908.1 |

$88 |

$103 |

$96 |

$165 |

$176 |

$130 |

$107 |

$42 |

- |

- |

- |

Operating Costs and

Royalties(4) |

US$M |

($570.5) |

($63) |

($62) |

($64) |

($97) |

($107) |

($81) |

($67) |

($29) |

- |

- |

- |

| Reclamation Accrual |

US$M |

($7.4) |

($1) |

($1) |

($1) |

($1) |

($1) |

($1) |

($1) |

($0) |

- |

- |

- |

| Depreciation |

US$M |

($262.1) |

($19) |

($26) |

($27) |

($49) |

($53) |

($41) |

($34) |

($13) |

- |

- |

- |

| Net Operating Income |

US$M |

$68.1 |

$6 |

$14 |

$4 |

$18 |

$14 |

$7 |

$5 |

($0) |

- |

- |

- |

| |

|

|

|

|

|

|

|

|

|

|

|

|

|

| Income Taxes |

US$M |

($28.7) |

($3) |

($5) |

($2) |

($7) |

($6) |

($3) |

($3) |

($1) |

- |

- |

- |

| |

|

|

|

|

|

|

|

|

|

|

|

|

|

| Net Income |

US$M |

$39.4 |

$3 |

$10 |

$2 |

$12 |

$8 |

$3 |

$2 |

($1) |

- |

- |

- |

| Depreciation |

US$M |

$262.1 |

$18.7 |

$26.1 |

$26.9 |

$48.7 |

$53.2 |

$41.1 |

$34.0 |

$13.4 |

- |

- |

- |

| Granite Creek Underground |

UNITS |

TOTAL LOM |

2025E |

2026E |

2027E |

2028E |

2029E |

2030E |

2031E |

2032E |

2033E |

2034E |

2035+1 |

| Reclamation |

US$M |