PA PA false 0000820318 0000820318 2024-05-06 2024-05-06

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 8-K

CURRENT REPORT

Pursuant to Section 13 or 15(d)

of the Securities Exchange Act of 1934

Date of Report (Date of earliest event reported): May 6, 2024

Coherent Corp.

(Exact name of registrant as specified in its charter)

|

|

|

|

|

| PENNSYLVANIA |

|

001-39375 |

|

25-1214948 |

(State or Other Jurisdiction

of Incorporation) |

|

(Commission File Number) |

|

(I.R.S. Employer

Identification No.) |

375 Saxonburg Boulevard

Saxonburg, PENNSYLVANIA 16056

(Address of Principal Executive Offices) (Zip Code)

(724) 352-4455

(Registrant’s telephone number, including area code)

Not Applicable

(Former name or former address, if changed since last report)

Check the appropriate box below if the Form 8-K filing is intended to simultaneously satisfy the filing obligation of the registrant under any of the following provisions:

| ☐ |

Written communications pursuant to Rule 425 under the Securities Act (17 CFR 230.425) |

| ☐ |

Soliciting material pursuant to Rule 14a-12 under the Exchange Act (17 CFR 240.14a-12) |

| ☐ |

Pre-commencement communications pursuant to Rule 14d-2(b) under the Exchange Act (17 CFR 240.14d-2(b)) |

| ☐ |

Pre-commencement communications pursuant to Rule 13e-4(c) under the Exchange Act (17 CFR 240.13e-4(c)) |

Securities registered pursuant to Section 12(b) of the Act:

|

|

|

|

|

| Title of each class |

|

Trading

Symbol(s) |

|

Name of each exchange on which registered |

| Common Stock, no par value |

|

COHR |

|

New York Stock Exchange |

Indicate by check mark whether the registrant is an emerging growth company as defined in Rule 405 of the Securities Act of 1933 (§230.405 of this chapter) or Rule 12b-2 of the Securities Exchange Act of 1934 (§240.12b-2 of this chapter).

Emerging growth company ☐

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

| Item 2.02. |

Results of Operations and Financial Condition. |

On May 6, 2024 Coherent Corp. (the “Company”) issued a press release (“Press Release”) announcing it will publicly disseminate a shareholder letter (the “Shareholder Letter”) with its financial results for the quarter ended March 31, 2024 (the “financial results”) and that it will be holding an earnings call webcast (the “Earnings Call”) on May 7, 2024 at 8:00 a.m. Eastern Time to discuss the financial results. The Company is making reference to non-GAAP financial information in the Shareholder Letter and on the Earnings Call. A reconciliation of GAAP to non-GAAP financial measures is provided in the Shareholder Letter.

A copy of the Press Release and the Shareholder Letter are furnished as Exhibits 99.1 and 99.2, respectively, and are incorporated herein by reference.

| Item 7.01. |

Regulation FD Disclosure. |

A slide presentation to be used by senior management of the Company in connection its discussions with investors and others regarding the financial results is furnished as Exhibit 99.3.

The information in this Current Report on Form 8-K, including the exhibits furnished pursuant to Item 9.01, shall not be deemed “filed” for the purposes of Section 18 of the Securities Exchange Act of 1934 or otherwise subject to the liabilities under that Section. Furthermore, the information in this Item 2.02 of this Current Report on Form 8-K, including the exhibits furnished pursuant to Item 9.01, shall not be deemed to be incorporated by reference into the filings of the Company under the Securities Act of 1933.

| Item 9.01 |

Financial Statements and Exhibits. |

SIGNATURE

Pursuant to the requirements of the Securities Exchange Act of 1934, the registrant has duly caused this report to be signed on its behalf by the undersigned hereunto duly authorized.

|

|

|

|

|

|

|

|

|

|

|

Coherent Corp. |

|

|

|

|

| Date: May 6, 2024 |

|

|

|

By: |

|

/s/ Richard Martucci |

|

|

|

|

|

|

Richard Martucci |

|

|

|

|

|

|

Interim Chief Financial Officer and Treasurer |

Exhibit 99.1

|

|

|

|

|

Coherent Corp.

375 Saxonburg Blvd.

Saxonburg, PA 16056-9499 |

PRESS RELEASE

COHERENT CORP. RELEASES THIRD-QUARTER FISCAL YEAR 2024 FINANCIAL RESULTS

PITTSBURGH, May 6, 2024 (GLOBE NEWSWIRE) – Coherent Corp. (NYSE: COHR), a global leader in materials, networking, and lasers, announced today the

financial results for its third quarter of fiscal year 2024. These results have been posted as a letter to shareholders on the Investor Relations section of its website at coherent.com/company/investor-relations.

A conference call to discuss these results with Chair and CEO Dr. Vincent D. (Chuck) Mattera, Jr., and members of the management team will be held

on Tuesday, May 7, 2024, at 8:00 a.m. ET. Individuals wishing to listen to the live webcast of the call can access the event at the company’s website by visiting coherent.com/company/investor-relations. The call will be recorded,

and a replay will be available for a limited time.

The shareholder letter sets forth detailed financial information and disclosures for the company and

is designed to provide greater insight into the company’s operating performance and outlook in advance of the earnings call. This format allows more time for questions and answers on the earnings call.

About Coherent

Coherent empowers market

innovators to define the future through breakthrough technologies, from materials to systems. We deliver innovations that resonate with our customers in diversified applications for the industrial, communications, electronics, and instrumentation

markets. Headquartered in Saxonburg, Pennsylvania, Coherent has research and development, manufacturing, sales, service, and distribution facilities worldwide. For more information, please visit us at coherent.com.

Contact

Paul Silverstein

Vice President, Investor Relations & Corporate Communications

investor.relations@coherent.com

# # #

|

|

|

| coherent.com | T. 724 352 4455 |

|

1 |

Exhibit 99.2

|

|

|

|

|

|

|

|

|

|

Coherent Corp. 375 Saxonburg Blvd.

Saxonburg, PA 16056-9499 USA |

SHAREHOLDER LETTER – MAY 6, 2024

Related Information. The following commentary is provided to give investors and analysts further insight into the Company’s performance in advance

of the earnings call webcast. Please note the “Forward-Looking Statements” information at the end of this letter.

Fellow Coherent

Shareholders,

We are pleased to present our Coherent Corp. Shareholder Letter setting forth an overview of our Third Quarter Fiscal Year 2024 results.

Coherent was founded in 1971 to manufacture high-quality materials and optics for industrial lasers. Today, Coherent is a global leader in materials,

networking, and lasers, operating in more than 20 countries around the world. We empower market innovators to define the future through breakthrough technologies, from materials to systems, that fuel market megatrends while pursuing our mission of

enabling the world to be safer, healthier, closer, and more efficient.

We remain focused on providing industry-leading

foundational materials, networking, and laser innovations for the industrial, communications, electronics, and instrumentation markets that enable better performance and greater efficiency of our customers’ solutions. Steadfast in pursuit of

our goal to invest, manage, and position Coherent for continued growth while succeeding in the exciting markets we are targeting, we are leveraging our unique set of differentiated assets including:

| |

◾ |

Unparalleled experience in materials, photonics, and lasers; |

| |

◾ |

A vertically integrated, geographically diverse organization with scalable manufacturing platforms;

|

| |

◾ |

A history of insightful targeting and successful integration of strategic acquisitions; |

| |

◾ |

A sustained and committed track record of targeted research and development and capital expenditures to prepare

for the opportunities that lie ahead; and |

| |

◾ |

Worldwide talented and experienced teams of engineers and technologists, including over 2,000 people employed

in R&D, as well as expert manufacturing teams, and experienced business leaders. |

We continue to invest in our core assets,

including our people, while undertaking strategic moves to enhance our market opportunities and returns on invested capital; at the same time, we are proactively executing on opportunities to enhance our operating performance.

As previously announced, the Board of Directors is conducting a comprehensive process to select the fourth CEO in Coherent’s 53-year history. That process is ongoing.

We believe that the combination of our sustained efforts to transform the

Company while focusing relentlessly on targeted markets, customer intimacy, product leadership, and operational excellence will lead to enhanced operating performance and will drive long-term shareholder value. We are taking the short-term

challenges head-on, and we have made some bold moves that are characteristic of a sustainable market leader. When we look past the horizon, we remain excited and optimistic about our future.

1

Table 1

Financial Metrics

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |

|

THREE MONTHS ENDED |

|

|

NINE MONTHS ENDED |

|

| $ Millions, except per share and percentage amounts

(unaudited) |

|

Mar 31

2024 |

|

|

Dec 31

2023 |

|

|

Mar 31

2023 |

|

|

Mar 31

2024 |

|

|

Mar 31

2023 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Revenues |

|

$ |

1,208.8 |

|

|

$ |

1,131.4 |

|

|

$ |

1,240.2 |

|

|

$ |

3,393.3 |

|

|

$ |

3,955.0 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| GAAP Gross Profit |

|

$ |

366.5 |

|

|

$ |

350.6 |

|

|

$ |

420.2 |

|

|

$ |

1,024.0 |

|

|

$ |

1,274.9 |

|

| Non-GAAP Gross Profit(1) |

|

$ |

432.6 |

|

|

$ |

407.7 |

|

|

$ |

463.2 |

|

|

$ |

1,206.7 |

|

|

$ |

1,551.2 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| GAAP Operating Income(2) |

|

$ |

22.3 |

|

|

$ |

31.9 |

|

|

$ |

67.4 |

|

|

$ |

32.9 |

|

|

$ |

118.1 |

|

| Non-GAAP Operating Income(1) |

|

$ |

182.2 |

|

|

$ |

171.6 |

|

|

$ |

217.1 |

|

|

$ |

486.2 |

|

|

$ |

781.3 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| GAAP Net Earnings (Loss) Attributable to Coherent Corp. |

|

$ |

(13.2 |

) |

|

$ |

(27.0 |

) |

|

$ |

2.5 |

|

|

$ |

(107.7 |

) |

|

$ |

(81.2 |

) |

| Non-GAAP Net Earnings Attributable to Coherent Corp(1) |

|

$ |

113.2 |

|

|

$ |

86.4 |

|

|

$ |

117.6 |

|

|

$ |

254.5 |

|

|

$ |

472.6 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

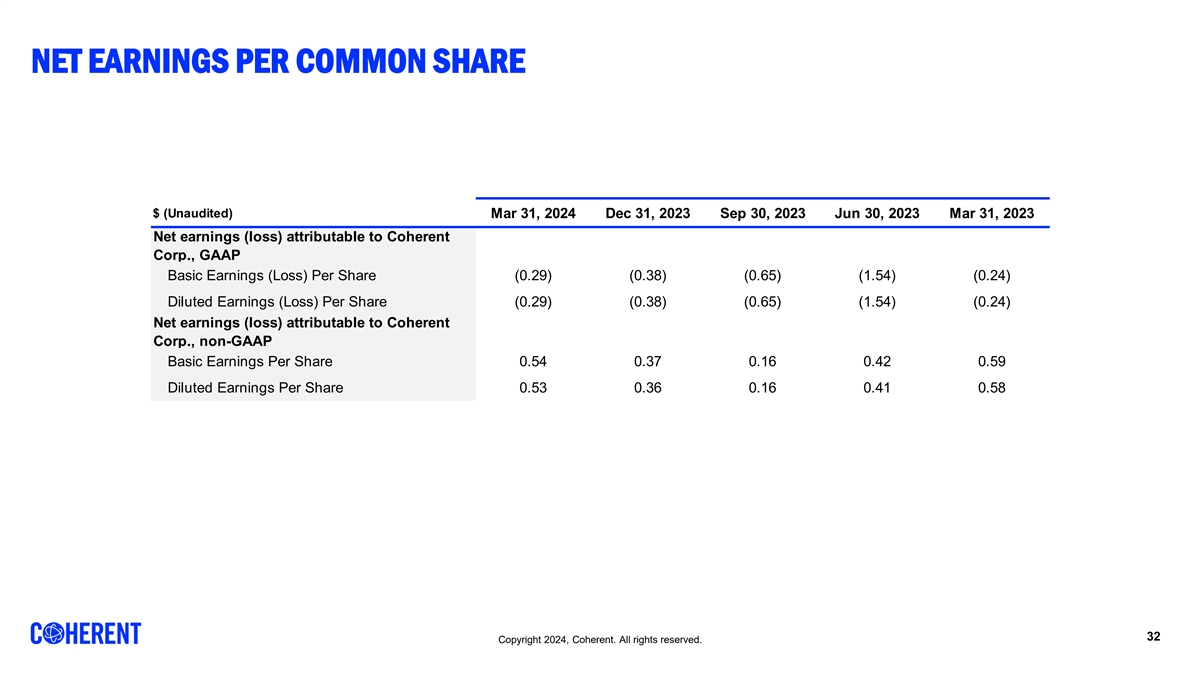

| GAAP Diluted Loss Per Share |

|

$ |

(0.29 |

) |

|

$ |

(0.38 |

) |

|

$ |

(0.24 |

) |

|

$ |

(1.32 |

) |

|

$ |

(1.38 |

) |

| Non-GAAP Diluted Earnings Per Share(1) |

|

$ |

0.53 |

|

|

$ |

0.36 |

|

|

$ |

0.58 |

|

|

$ |

1.06 |

|

|

$ |

2.57 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Other Selected Financial Metrics |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| GAAP gross margin |

|

|

30.3 |

% |

|

|

31.0 |

% |

|

|

33.9 |

% |

|

|

30.2 |

% |

|

|

32.2 |

% |

| Non-GAAP gross margin(1) |

|

|

35.8 |

% |

|

|

36.0 |

% |

|

|

37.3 |

% |

|

|

35.6 |

% |

|

|

39.2 |

% |

| GAAP operating margin |

|

|

1.8 |

% |

|

|

2.8 |

% |

|

|

5.4 |

% |

|

|

1.0 |

% |

|

|

3.0 |

% |

| Non-GAAP operating margin(1) |

|

|

15.1 |

% |

|

|

15.2 |

% |

|

|

17.5 |

% |

|

|

14.3 |

% |

|

|

19.8 |

% |

| GAAP return on sales |

|

|

(1.1 |

)% |

|

|

(2.4 |

)% |

|

|

0.2 |

% |

|

|

(3.2 |

)% |

|

|

(2.1 |

)% |

| Non-GAAP return on sales(1) |

|

|

9.4 |

% |

|

|

7.6 |

% |

|

|

9.5 |

% |

|

|

7.5 |

% |

|

|

11.9 |

% |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| (1) |

The Company has disclosed financial measurements in this letter to shareholders that present financial

information considered to be non-GAAP financial measures. These measurements are not a substitute for GAAP measurements, although the Company’s management uses these measurements as an aid in monitoring

the Company’s on-going financial performance. The non-GAAP net earnings attributable to Coherent Corp., the non-GAAP

earnings per share, the non-GAAP operating income, the non-GAAP gross margin, the non-GAAP internal research and development, the

non-GAAP selling, general and administration, the non-GAAP interest and other (income) expense, and the non-GAAP income tax

(benefit), measure earnings and operating income (loss), respectively, excluding non-recurring or unusual items that are considered by management to be outside the Company’s standard operation and

excluding certain non-cash items. EBITDA is an adjusted non-GAAP financial measurement that is considered by management to be useful in measuring the profitability

between companies within the industry by reflecting operating results of the Company excluding non-operating factors. There are limitations associated with the use of

non-GAAP financial measures, including that such measures may not be entirely comparable to similarly titled measures used by other companies, due to potential differences among calculation methodologies.

Thus, there can be no assurance whether (i) items excluded from the non-GAAP financial measures will occur in the future or (ii) there will be cash costs associated with items excluded from the non-GAAP financial measures. The Company compensates for these limitations by using these non-GAAP financial measures as supplements to GAAP financial measures and by

providing the reconciliations of the non-GAAP financial measures to their most comparable GAAP financial measures. Investors should consider adjusted measures in addition to, and not as a substitute for, or

superior to, financial performance measures prepared in accordance with GAAP. All non-GAAP amounts exclude certain adjustments for share-based compensation, acquired intangible amortization expense,

restructuring charges (recoveries), integration and site consolidation expenses, integration transaction expenses, start-up costs related to the start-up of new devices

for new customer applications, and various one-time adjustments. See Table 8 for the Reconciliation of GAAP measures to non-GAAP measures. |

| (2) |

GAAP Operating income is defined as earnings before income taxes, interest expense, and other expense or

income, net. |

2

EXECUTIVE SUMMARY

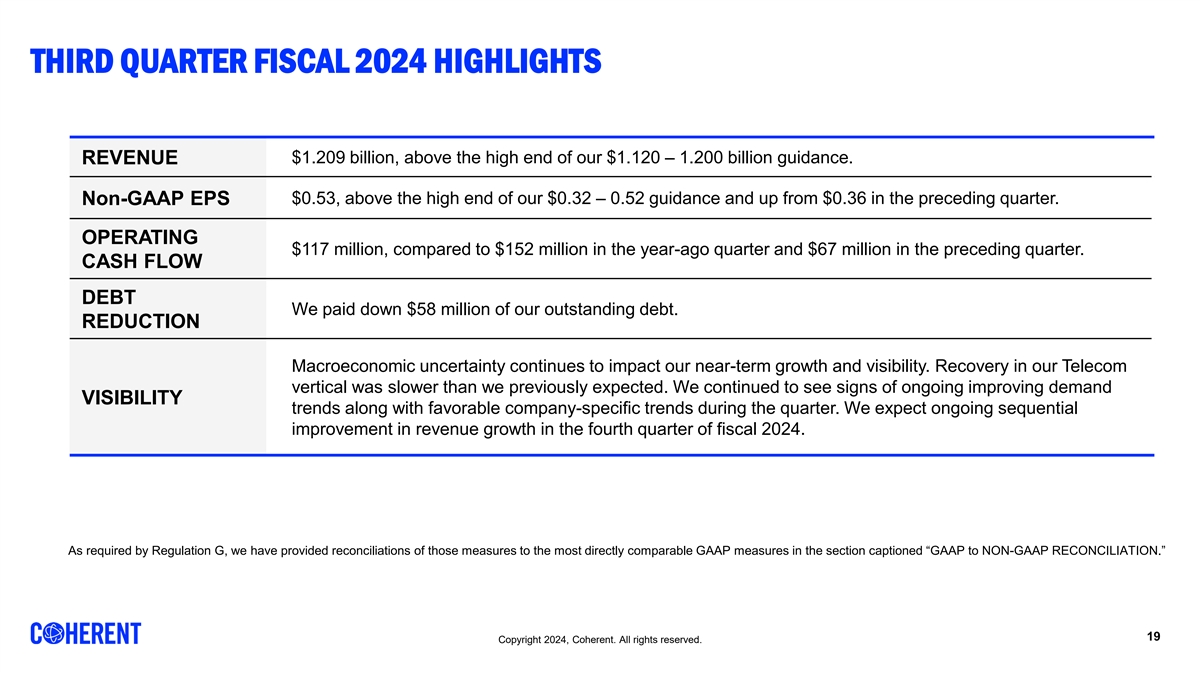

Revenue. $1.209 billion, above the high end of our $1.120 – 1.200 billion guidance and an approximate 7% sequential increase.

Non-GAAP Gross Margin. 35.8%, slightly below our 36 – 38% guidance and a 20 bp sequential decrease from

36.0%. New Datacom transceiver product introduction ramps, a power failure in a silicon carbide growth facility, slower than expected recovery in Telecom, and higher than expected inventory provisions in our Lasers segment collectively had an over

100 bps adverse impact.

Non-GAAP Operating Margin. 15.1%, within our 14 – 16% guidance and slightly

lower than the preceding quarter.

Non-GAAP EPS. $0.53, above the high end of our $0.32 – $0.52

guidance and up from $0.36 in the preceding quarter.

Operating Cash Flow. $117 million, compared to $152 million in the year-ago quarter and $67 million in the preceding quarter.

Debt Reduction. We paid down $58 million of

our outstanding debt.

Visibility. Macroeconomic uncertainty continues to impact our near-term growth and visibility. Recovery in our Telecom

vertical was slower than we previously expected. We continued to see signs of ongoing improving demand trends along with favorable company-specific trends during the quarter. We expect ongoing sequential improvement in revenue growth in the fourth

quarter of fiscal 2024.

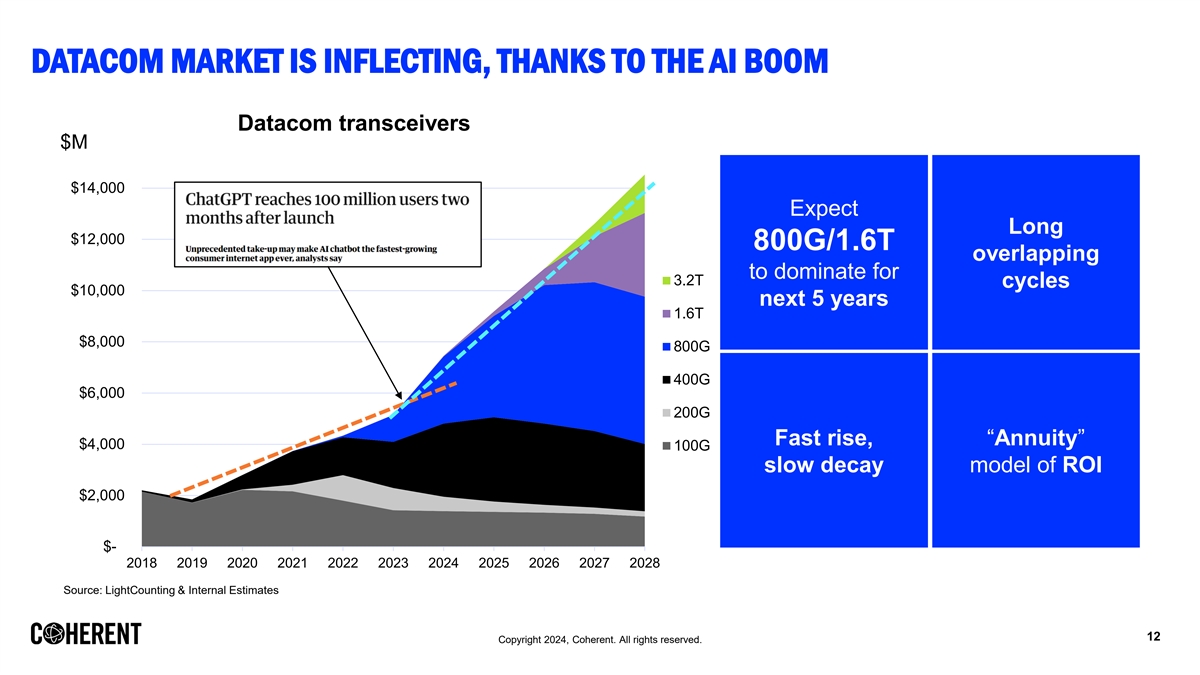

AI/ML. We enjoyed a fourth straight quarter of strong demand for our AI/ML-related

Datacom transceivers. Our 800G revenue increased sequentially by almost 80% to almost $200 million and is on track to exceed $250M in our fourth quarter of fiscal 2024. In response to customer demand, we are making progress toward commercial

launch of our 1.6T Datacom transceivers and components in calendar 2025 and expect to ship commercial samples of 1.6T products to our customers starting in the first quarter of fiscal 2025.

3

PART I - OUTLOOK, VISIBILITY, KEY TRENDS, AND DEVELOPMENTS

OUTLOOK

These metrics are provided on a non-GAAP basis. Non-GAAP earnings per share is on a fully diluted basis. The outlook assumes that the exchange rate of the U.S. dollar to other currencies will remain

relatively stable at current levels.

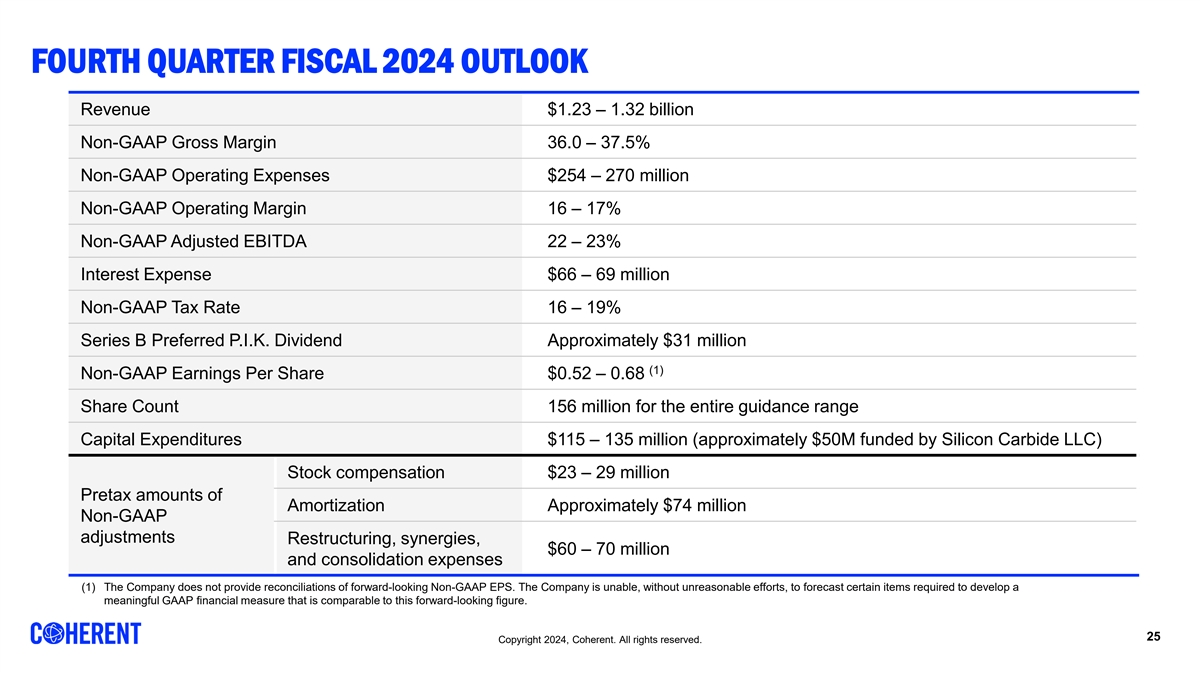

FOURTH QUARTER FISCAL 2024

Our guidance for our fourth quarter of fiscal 2024 ending June 30, 2024, is as follows:

| |

◾ |

Revenue of approximately $1.23 – 1.32 billion. |

| |

◾ |

Non-GAAP gross margin of approximately 36.0 – 37.5%.

|

| |

◾ |

Non-GAAP operating expense of approximately $254 –

270 million. |

| |

◾ |

Non-GAAP operating margin of approximately 16 – 17%

|

| |

◾ |

Non-GAAP Adjusted EBITDA of approximately 22 – 23%.

|

| |

◾ |

Interest expense of approximately $66 – 69 million. |

| |

◾ |

Non-GAAP tax rate of approximately 16 – 19%.

|

| |

◾ |

Series B Preferred P.I.K. Dividend of approximately $31 million. |

| |

◾ |

Non-GAAP earnings per share of approximately $0.52 – 0.68.1 |

| |

◾ |

Share count for the entire guidance range is 156 million. |

| |

◾ |

Capital expenditures of approximately $115 – 135 million (approximately $50 million of which

will be funded by Silicon Carbide LLC). |

Pretax amounts of non-GAAP adjustments in the fourth

quarter of fiscal 2024 include:

| |

◾ |

Stock compensation of approximately $23 – 29 million. |

| |

◾ |

Amortization of approximately $74 million. |

| |

◾ |

Restructuring, synergies, and consolidation expenses of approximately $60 – 70 million.

|

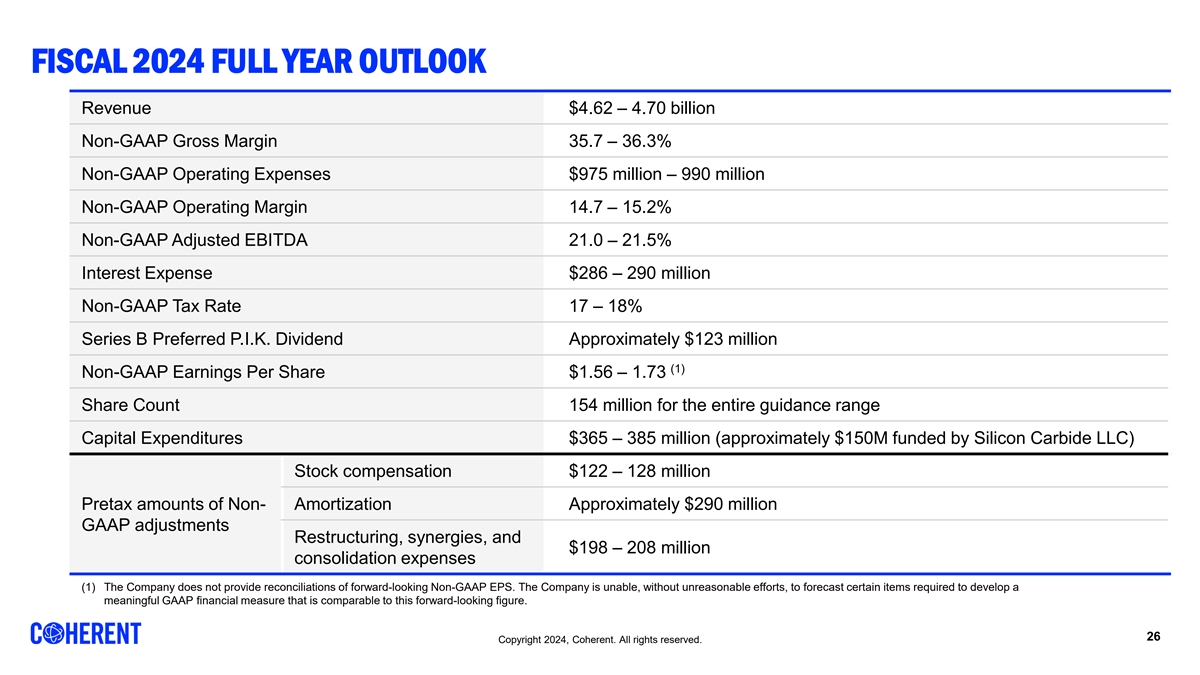

FULL YEAR FISCAL 2024

Our

guidance for fiscal 2024 ending June 30, 2024, is as follows:

| |

◾ |

Revenue of approximately $4.62 – 4.70 billion, a $70 million increase of the low end of our

previous guidance of $4.55 – 4.70 billion. |

| |

◾ |

Non-GAAP gross margin of approximately 35.7 – 36.3%.

|

| |

◾ |

Non-GAAP operating expense of approximately $975 –

990 million. |

| |

◾ |

Non-GAAP operating margin of approximately 14.7 – 15.2%.

|

| |

◾ |

Non-GAAP Adjusted EBITDA of approximately 21.0 – 21.5%.

|

| |

◾ |

Interest expense of approximately $286 – 290 million. |

| |

◾ |

Non-GAAP tax rate of approximately 17 – 18%.

|

| |

◾ |

Series B Preferred P.I.K. Dividend of approximately $123 million. |

| 1 |

The Company does not provide reconciliations of forward-looking

Non-GAAP EPS. The Company is unable, without unreasonable efforts, to forecast certain items required to develop a meaningful GAAP financial measure that is comparable to this forward-looking figure.

|

4

| |

◾ |

Non-GAAP earnings per share of approximately $1.56 – 1.73, up from

our $1.30 – 1.70 previous guidance.2 |

| |

◾ |

Share count for the entire guidance range is 154 million. |

| |

◾ |

Capital expenditures of approximately $365 – 385 million (approximately $150 million funded by

the Silicon Carbide LLC). |

Pretax amounts of Non-GAAP adjustments for full year fiscal 2024

include:

| |

◾ |

Stock compensation of approximately $122 – 128 million. |

| |

◾ |

Amortization of approximately $290 million. |

| |

◾ |

Restructuring, synergies, and consolidation expenses of approximately $198 – 208 million.

|

BIG PICTURE

In the face of

what remains a challenging macroeconomic environment, for the quarter, we delivered solid sequential revenue growth, above the high end of our guidance, and implemented rigorous controls on operating expense, which came in below the midpoint of our

guidance, and which together offset disappointing gross margin to drive strong sequential improvement in Non-GAAP EPS, above the high end of our guidance.

Demand

Our Datacom strength is more than offsetting

slower than expected revenue growth in some other markets and verticals. We remain confident in our long-term growth prospects for each of these markets and verticals. We also saw additional positive trends in each. We emerged from the third

quarter, however, relatively more cautious as to the timing of recovery in revenue growth in our Telecom vertical and as to the growth rate in fiscal 2025 for our silicon carbide revenue.

Communications Market

Datacom Vertical. We

enjoyed another quarter of strong AI-related Datacom demand for our 800G Datacom transceivers. We expect this strength to continue in the current fourth quarter and into fiscal 2025.

Telecom Vertical. While the third quarter also offered signs of improving end demand in our Telecom vertical within our Communications market, Telecom

recovery is slower than we previously expected, as our customers are still working down their inventory, but at a slower pace than we forecasted. Our Telecom revenue sequentially declined, albeit modestly, in the third quarter, and we currently

expect sequentially flat revenue in our current fourth quarter.

Industrial Market

The third quarter offered further signs of recovery in Industrial market end demand. Our Industrial orders sequentially increased by 10% following 11%

sequential growth in the second fiscal quarter, and we currently expect to end our fiscal 2024 with a third straight quarter of over 10% sequential growth. Our Industrial revenue for the third quarter and our revenue outlook for

| 2 |

The Company does not provide reconciliations of forward-looking

Non-GAAP EPS. The Company is unable, without unreasonable efforts, to forecast certain items required to develop a meaningful GAAP financial measure that is comparable to this forward-looking figure.

|

5

the fourth quarter compare favorably to the sequential decline we experienced throughout fiscal 2023 and into the first quarter of fiscal 2024. A sequential decline in our Aerospace &

Defense revenue, however, offset sequential growth in the other three verticals within our Industrial market to drive relatively flat sequential revenue in the third quarter. We expect healthy sequential revenue growth in our Industrial market in

the current fourth quarter.

Electronics Market

Silicon Carbide. Our revenue growth outlook for our silicon carbide business is less than we previously expected as a result of supply constraints

limiting our ability to ramp production. We have been supply-constrained, with our ability to ramp production having been the key constraint to silicon carbide revenue growth. We still expect to out-grow the

overall silicon carbide market in both the near and longer term. We have moderated our silicon carbide revenue growth outlook for fiscal 2025, however, to take into account the industry-wide slowdown in EV demand and production.

Instrumentation Market

We remain excited regarding the

long-term growth opportunity in the Instrumentation market. Near-term, demand in our Instrumentation market appears to have stabilized with a third straight quarter of just under $100 million in revenue. Elevated inventories appear to have been

reduced to and may have reached normalized levels; however, we have yet to see a return to sequential or year-over-year growth, and our revenue remains approximately 15 – 20% below its fiscal 2023 level primarily due to macroeconomic

uncertainty.

Margins

Driving meaningful secular

improvement in our margin structure remains our primary focus. We remain confident that we will return to our previous 40% Non-GAAP gross margin and 20% Non-GAAP

operating margin structure by the end of the first half of fiscal 2026 and believe that we will eventually exceed these targets. As we noted in our Shareholder Letter in the preceding quarter, we are making significant investments and are

implementing numerous actions to drive this progression.

Third quarter gross margin was below our guidance, which we offset by solid operating expense

controls driving operating margin above the midpoint of our guidance. Our gross margin was adversely impacted by several factors that we believe we have resolved or will resolve over the next several quarters. These factors collectively had a

greater than 100 bps adverse impact on our gross margin in the quarter. They span our Datacom vertical within our Communications market, our silicon carbide business (the revenues of which are reflected within our Electronics market) and our Lasers

segment.

Accordingly, we have reduced our full year fiscal 2024 Non-GAAP gross margin outlook to

35.7 – 36.3% from 36 – 38% previously. We expect to drive sequential improvement in our current fourth quarter to 36.0 – 37.5%.

We set forth below a more detailed discussion of the specific issues by segment.

6

Materials. Lower than expected yields drove our disappointing silicon carbide gross margin in the

third quarter. Specifically, a power failure limited our silicon carbide substrate growth yield. The resulting lower production volume translated into lower overhead absorption. We have fully resolved the power failure. Our silicon carbide growth

yields are very close to plan and production volumes are increasing with, we expect, an over 50% sequential increase in our silicon carbide revenue in our fourth quarter.

Networking. Lower than expected Datacom gross margin accounted for over 50% of the total adverse impact. Specifically, lower transceiver yields was the

primary issue. We have implemented a number of corrective actions, have started to see meaningful improvement in yield, and expect to attain our targeted yield by the time we exit the first quarter of fiscal 2025.

Lasers. Lower than expected gross margin in our Lasers segment was primarily due to a number of one-off

inventory provisions related to portfolio adjustments. We do not expect these to recur.

Unchanged Long-Term Outlook; Growth Bias. Our longer-term

outlook for improved margin structure and strong secular growth in all of our markets remains unchanged, driven by both an eventual recovery in end market demand and the impact of AI along with other significant drivers discussed at greater length

below.

We are not waiting for improved end market demand to drive enhanced profitability. We have already implemented actions across virtually all of our

businesses in a drive for enhanced operating efficiency as measured by return on sales.

As discussed in our second quarter fiscal 2024 Shareholder Letter

and at greater length below, some of these actions require significant time, effort, innovation, and investment to have meaningful impact. These include our digital transformation and facilities consolidation including consolidation of multiple fabs

(which are part of our Enterprise Transformation Program) as well as our Asia Pacific Center of Excellence for materials, optics, and lasers where we are expanding our footprint to accommodate our long-term growth in the Philippines, Malaysia,

Vietnam, and Singapore. We think the near-term cost of these actions will yield meaningful long-term return in the form of significant improvement in our cost structure and operating efficiency, which in turn we expect will benefit both our margin

structure and our competitiveness and thereby our revenue growth and our profitability.

In addition, our diversification across product, technology,

customer, and regional markets allows us to redeploy capital and people from low or declining returns to higher-return market opportunities. Almost by definition, the initial “investment” phase of such a shift typically entails lower gross

margin, which eventually is followed by margin uplift as the investments and learning begin to translate into targeted yields, BOM costs and cycle times, enhanced operating efficiency, greater revenue volume, and increased overhead absorption.

Near-Term Focus on Execution; Increased FY24 Revenue Outlook Driven by Strong AI-Driven Datacom Demand. We have

increased the lower end of our fiscal 2024 revenue guidance. We are now guiding for $4.62 – 4.70 billion versus our previous guidance of $4.55 – 4.7 billion. Underlying our revised outlook, the third quarter reinforced our

confidence in the outlook for our Datacom vertical (which is within our Communications market) driven by AI-related datacenter builds by webscale, other cloud internet content providers (ICPs), and companies

that supply them.

For the fourth quarter of fiscal 2024, we are forecasting 5% sequential revenue growth and almost 13% sequential non-GAAP EPS growth over the third quarter (at the midpoint of guidance). The expected revenue growth is driven primarily by the strength in our AI-related Datacom transceiver

and silicon carbide businesses.

7

Improved Capital Structure and Ratings. On April 2, 2024, we successfully completed the

repricing of our existing $2.4 billion secured Term Loan B. We will realize almost $9 million of annual interest savings from the repricing.

On

February 21, 2024, Moody’s Investor Service upgraded the credit rating of Coherent Corp. to Ba2. Moody’s cited “The ratings upgrade reflects Moody’s expectation that Coherent’s financial metrics and cash generation will

continue to improve. This reflects a recovery in end markets along with continued strong sales growth in optical transceivers serving generative artificial intelligence (GenAI) uses.”

A table of our current credit ratings can be found below:

|

|

|

|

Credit Profile - Moody’s /

S&P / Fitch |

|

|

|

Corporate Family Rating

|

|

Ba2 / BB- / BB |

|

Secured Ratings |

|

Ba1 / BB- / BBB- |

|

Unsecured Ratings |

|

B1 / B+ / BB |

|

Outlook |

|

Stable / Negative /Stable

|

|

Last Update Date |

|

2.24 / 10.23 / 11.23

|

8

VISIBILITY, KEY TRENDS, AND DEVELOPMENTS

Margin Structure: Opex Discipline Offsets Some Transitory Gross Margin Issues

As previously noted, strong operating leverage resulting from the revenue upside and better than expected operating expense control offset weaker than expected

gross margin to drive operating margin just above the midpoint of our 14 – 16% third quarter guidance, which in turn contributed to our posting Non-GAAP EPS above the high end of our $0.32 – 0.52

guidance.

Our gross margin was adversely impacted by a number of issues that we have resolved or expect to resolve by

mid-fiscal 2025. Collectively, these issues in the aggregate had an over 100 bps adverse impact on our Non-GAAP gross margin in the third quarter.

Lower than planned yields for some of our Datacom transceivers accounted for well over 50% of the third quarter aggregate impact. We have implemented

corrective actions, and have already started to see improvement, and we expect to achieve our targeted level.

We also suffered from very low gross margin

in our silicon carbide business due to a power failure at a crystal growth facility, which also resulted in an overhead absorption issue due to the significant adverse impact on our Silicon Carbide LLC revenue in the third quarter. We have addressed

the power failure issue, and our silicon carbide revenue has returned to a positive trajectory.

Third Quarter of Fiscal 2024. Non-GAAP gross margin of 35.8% was below our 36 – 38% guidance and relatively flat with the 36.0% we reported in the second quarter of fiscal 2024. Non-GAAP operating

margin of 15.1% was in-line with our 14 – 16% guidance and essentially flat with the 15.2% we reported in the preceding quarter. As previously noted, a number of transitory issues offset the strong

sequential revenue growth to drive our disappointing gross margin. The strong sequential increase in revenue together with positive operating leverage offset the relatively weak gross margin to drive operating margin

in-line with our guidance.

Fourth Quarter of Fiscal 2024. We expect to drive to 36.0 – 37.5% Non-GAAP gross margin and 16 – 17% Non-GAAP operating margin in our fourth quarter of fiscal 2024. The primary drivers of the expected sequential increase are greater

revenue and improved operational efficiencies.

Fiscal 2024. We expect 35.7 – 36.3% Non-GAAP gross

margin and 14.7 – 15.2% Non-GAAP operating margin for all of fiscal 2024 compared to our previous guidance of 36 – 38% and 14 – 16%, respectively.

Longer-Term. Our longer-term outlook for return to 40% Non-GAAP gross margin and 20% Non-GAAP operating margin remains unchanged.

Key Drivers. Underlying our longer-term view, unchanged from the

preceding quarter, key drivers of operational excellence to attain each of the above targets are broadly focused on pricing, procurement, and productivity, and include:

| |

◾ |

continuous rationalization and refreshing of the portfolio; |

| |

◾ |

continuous rationalization of the supply base for cost and resiliency; |

9

| |

◾ |

implementation of a streamlined Asia Pacific manufacturing Center of Excellence; |

| |

◾ |

moving up the value chain; |

| |

◾ |

operating cost reductions based on a more resilient and lower-cost manufacturing footprint;

|

| |

◾ |

increased capacity utilization; |

| |

◾ |

favorable product mix, driven by product introductions with higher margins; |

| |

◾ |

productivity improvements through improvements in yields and quality; |

| |

◾ |

implementation of digital transformation and adoption of AI technology to improve efficiency in R&D,

manufacturing, and G&A; and |

| |

◾ |

leveraging our service organization into new markets. |

| |

2. |

Operating Margin: in addition to the above drivers of gross margin improvement, we expect to drive

future operating margin improvement from operating leverage by both increasing revenue and ongoing operating expense control, with the latter enhanced by the execution of: |

| |

◾ |

our Enterprise Transformation Program; |

| |

◾ |

our Synergy and Site Consolidation Plan; |

| |

◾ |

our Restructuring Plan; and |

| |

◾ |

additional cost and expense reductions underway. |

Strategic Opportunities. As previously noted, as we transform the Company to improve operating performance, restructure our production footprint

to enhance operating resiliency, and complete the integration of legacy Coherent, Inc., we are exploring other strategic opportunities—not including material acquisitions—to unlock shareholder value.

Enterprise Transformation Program. We have implemented and continue to make significant progress on our Enterprise Transformation Program. This program

encompasses rollout of a new operating model, end-to-end global process capabilities and systems, and includes digital transformation, site consolidation, and

restructuring. We expect this program, following full implementation, to drive significant operating efficiencies. We have completed the design of the program’s integrated business planning and management capability and are rolling it out in

our business units. This capability will allow us to scale our business operations, improve inter-business unit coordination given our vertically integrated structure, and unlock significant value through better inventory management, reduced cost of

goods sold (COGS), and improved long-range capacity and business planning.

In addition, as part of this program, our digital transformation is focused on

designing and implementing a new integrated digital platform throughout the Company. Implementation will start in fiscal 2025 and extend through fiscal 2027 – 2028. We expect this digital transformation to drive improved ways of working,

collaboration, and standardization of processes that should allow us to effectively scale our business while significantly reducing internal complexity.

Synergy and Site Consolidation. The stated goal of our Synergy and Site Consolidation Plan for the Coherent, Inc., acquisition was to achieve

$250 million in annual synergies over three years, with $250 million of costs to achieve these synergies. We have accelerated some of the actions planned as part of our post-three-year synergy and site consolidation and relocation efforts.

These relocations and other actions are expected to help offset our lower than expected supply chain cost savings that result from lower revenue and allow us to achieve our targeted $250 million in annual synergies. At the end of the first

year, we reached $73 million of synergies for fiscal 2023. In the first nine months of fiscal 2024, we achieved another $131 million in synergies, an annualized run-rate of $175 million. To

date, synergies are split 60% cost of sales and 40% operating expenses.

10

Restructuring. In the fourth quarter of fiscal 2023, we implemented a Restructuring Plan that

includes site consolidations and closures as well as the relocation and requalification of certain manufacturing facilities. The following restructuring actions are intended to realign our cost structure as part of a transformation to a simpler,

more streamlined, resilient, and sustainable footprint and business model:

| |

◾ |

China and Rest of Asia Site Consolidation. Consolidation of sites in China and the rest of Asia,

including the closure of certain manufacturing facilities and sales offices and the establishment of new regional design centers closer to our customers in the Global South as part of a multi-year plan, are underway. The intent of these actions is

to optimize our footprint in Asia. In addition, through these actions, we will replicate the state-of-the-art manufacturing lines

we have in China to other parts of Asia to increase resiliency to our supply chain by taking advantage of the best practices of operational excellence, new product introductions, a smarter and shorter supply chain, and redundancy for sustainability.

|

| |

◾ |

Compound Semiconductor Site Consolidation. Consolidation of compound semiconductor wafer fab and device

manufacturing facilities, including the closure of half of these facilities, is a multi-year and cross-cutting initiative. We will consolidate into our most modern facilities with a stable baseline of operational excellence and will drive better

utilization of our assets while reducing our costs and improving our new product introduction and technology innovation cycle times. |

| |

◾ |

Savings. We expect total savings for fiscal 2023 – 2025 to be $200 – 250 million, with

annual savings of $110 – 140 million by fiscal 2025. We forecast savings associated with the Plan to be approximately $90 – 100 million for full fiscal year 2024. |

| |

◾ |

Costs to Achieve. We expect total costs to achieve these savings over the fiscal 2023 – 2025 period

to be $175 – 200 million, including severance, retention, facility moves, accelerated depreciation, short-term duplicate costs, lease termination costs, and IT consolidation costs. In the third quarter of fiscal 2024, we recorded

restructuring charges of $12 million, consisting primarily of employment termination costs and charges for accelerated depreciation and equipment write-offs. |

| |

◾ |

Restructuring Charges. We expect restructuring charges to be in the $25 – 35 million range for

full fiscal year 2024 mainly comprised of employment termination, facility move costs, and accelerated. We expect restructuring charges to be in the $35 – 45 million range for full fiscal year 2025, consisting primarily of employment

termination, facility move costs, and accelerated depreciation, and savings associated with the Plan to be $110 – 140 million for full fiscal year 2025. In fiscal 2023, restructuring charges were $119 million, primarily for workforce

reduction and the write-off of property and equipment, net of $65 million from reimbursement arrangements. |

11

Visibility

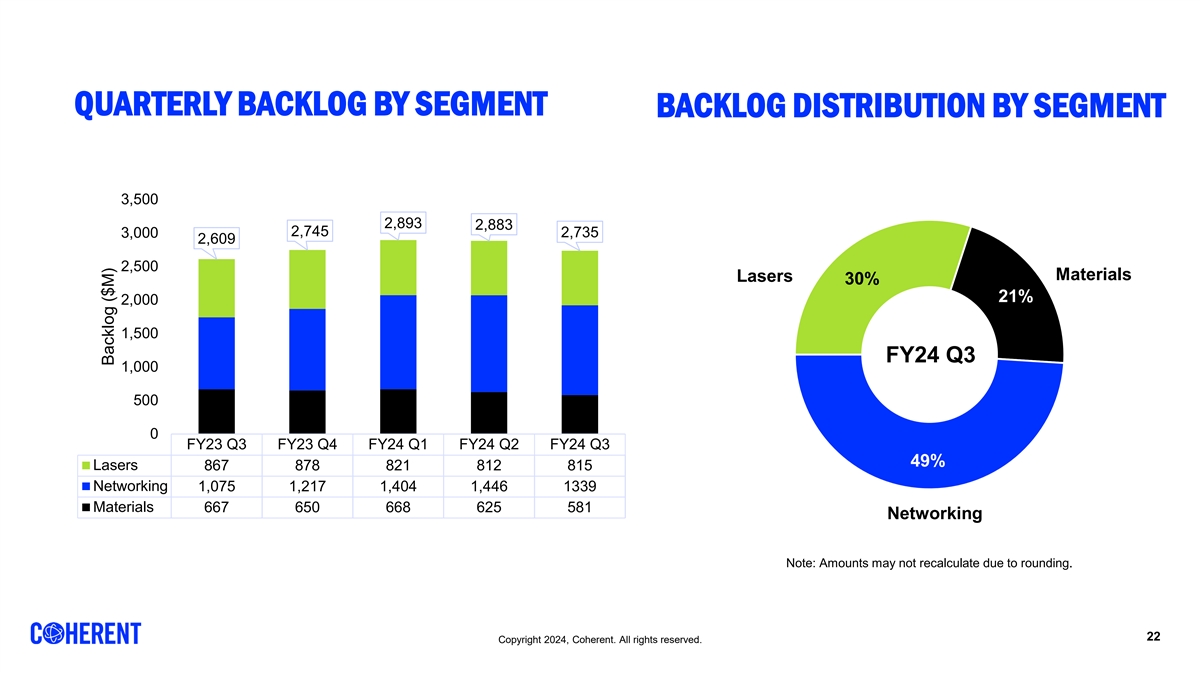

Backlog and Orders

In the third quarter, both orders and

backlog decreased sequentially but increased year-over-year. The sequential decreases were consistent with our previous expectations. They primarily reflect ongoing normalization of order levels in our Networking segment, which in turn is being

driven by ongoing moderation from the extraordinarily strong levels we have enjoyed for our 800G Datacom transceivers early in the still-young trend of AI-related datacenter builds.

| |

◾ |

Backlog. We ended the quarter with approximately $2.74 billion of backlog, an approximate

$150 million sequential decline from approximately $2.9 billion at the end of the preceding quarter and a well over $100 million increase from the year-ago quarter. |

| |

◾ |

Orders. Orders decreased sequentially by approximately 4% but increased year-over-year by approximately

11%. The sequential decline was primarily driven by decreased orders in our Networking segment due to continued decreases in lead times. We also saw a second straight quarter of double-digit order growth in our Lasers segment. The year-over-year

increase was primarily driven by strong year-over-year order growth in our Networking and Lasers segments, which offset a large year-over-year decline in orders in our Materials segment. The year-over-year Materials orders decline primarily was

driven by a product design change by our largest customer within our Consumer Electronics vertical (which we have highlighted in each of the past four quarters), along with macroeconomic uncertainty. |

Networking Segment: Ongoing AI Datacom Strength; Disappointing Telecom

We continue to enjoy strong momentum in our Networking segment driven by 800G transceivers for AI. Recovery in our Telecom business, however, is slower than we

expected.

Near-Term. Near-term, Datacom transceiver order strength offset ongoing weakness in our Telecom business to drive an over 25%

year-over-year increase in overall orders for our Networking segment. Networking orders decreased by approximately 15% sequentially primarily reflecting a contraction in customer order lead times since the initial surge in AI-related 800G orders at the end of the fourth quarter of fiscal 2023. As our 800G Datacom transceiver shipments continue to ramp against our significant backlog and as lead times shorten, we expect our backlog to

continue to decline.

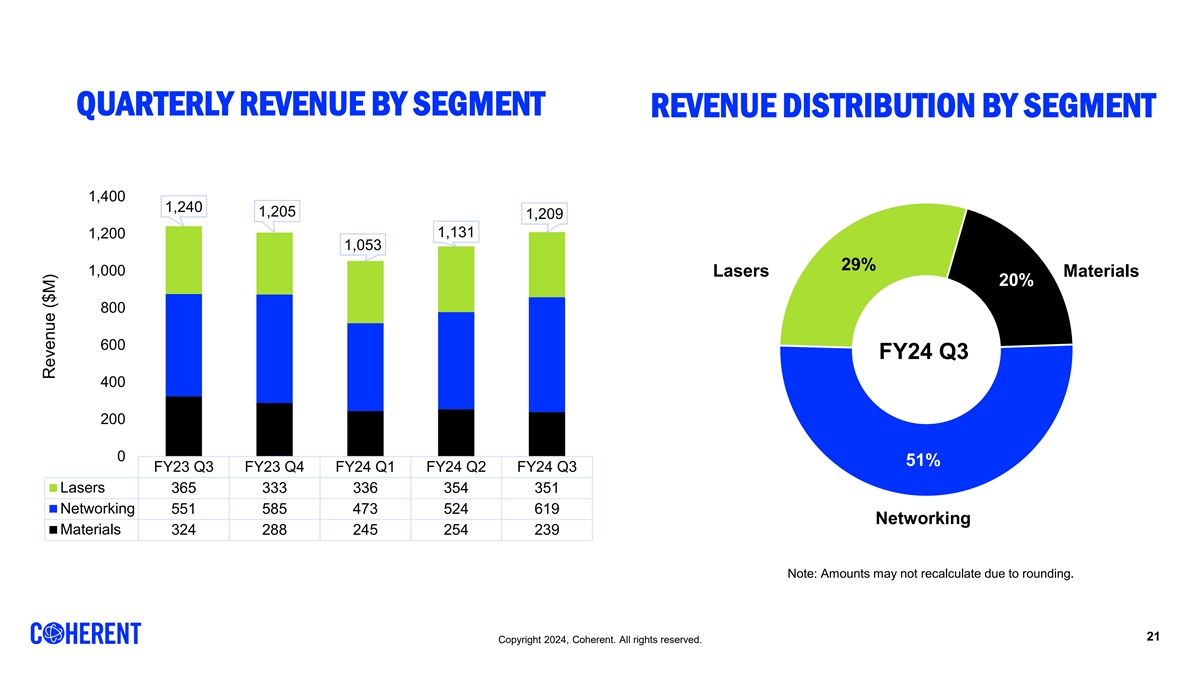

In terms of revenue, our Networking segment enjoyed strong sequential and year-over-year growth and a record quarter driven by

record Datacom transceiver revenue. Networking revenue increased sequentially by $95 million, or 18%, and year-over-year by almost $68 million, or 12%, to $619 million. We expect ongoing strong

AI-related Datacom transceiver revenue growth to drive another quarter of strong sequential revenue growth in our Networking segment in our fourth quarter of fiscal 2024.

12

Longer-Term. Our unchanged outlook for strong longer-term Networking revenue growth is based on

ongoing strength in our AI-related Datacom business along with recovery in our non- 800G Datacom and our Telecom businesses. Underlying our longer-term view are strong AI Datacom market trends; expanding AI-related customer engagements; our next-generation AI Datacom products including, in the near-term, 1.6T and, in the longer-term, 3.2T transceivers along with enabling active and passive components; ongoing

inventory digestion that we expect will lead to order normalization in our non-800G Datacom and Telecom businesses by fiscal 2025; eventual improvement in Telecom end demand trends; and market penetration and

revenue ramp of new Telecom products including our DCO transceivers and subsystems products.

Datacom Vertical

AI-Related Datacom Transceivers: Ongoing Strong Demand. Another quarter of strong orders and the further

expansion of our customer engagements during the quarter reinforced our confidence in strong near- and longer-term demand for our AI-related Datacom transceivers. Our total Datacom transceiver revenue

increased by well over $100 million, or well over 30%, sequentially and by well over $100 million, or almost 50%, year-over-year. We continue to expect AI-related revenue to account for more than 50%

of our Datacom transceiver revenue for all of fiscal 2024 and to enjoy strong growth in fiscal 2025 and beyond. 800G comprises the bulk but not all of our AI-related Datacom transceiver revenue.

800G. Datacom strength was driven by a third straight quarter of strong AI/ML-related orders for our 800G

Datacom transceivers from webscale, cloud ICPs, and other companies in the webscale and cloud ICP ecosystem. Speaking to ongoing strength in demand and strong ramp in production, our 800G Datacom transceiver revenue increased sequentially by almost

80% to almost $200 million in the third quarter, which followed over 100% sequential growth in the preceding quarter. We expect well over 30% sequential growth to $250 million for our fourth quarter of fiscal 2024.

1.6T on the Horizon. We also are excited by the active engagement we are seeing from key customers for 1.6T transceivers and components. In response to

customer demand, we continue to make progress toward expected commercial launch and revenue in calendar 2025 and expect to ship commercial samples of 1.6T products to our customers starting in the first quarter of fiscal 2025 of our 1.6T

transceivers including designs based on silicon photonics, 200G EMLs, and DFB-MZ lasers. We see the opportunity for, and expect, these 1.6T solutions to increase our share of the

AI-related Datacom transceiver and component opportunity by relying on our broad and deep level of vertical integration relative to our direct transceiver competitors.

AI-Customer Diversification. While the revenue opportunity remains concentrated in a relatively limited number

of potential customers within the AI-related Datacom transceiver market, four different customers are on track to generate meaningful AI-related Datacom revenue for our

full year fiscal 2024.

Market-Leading Position. Our transceivers are designed to be compatible with all of the protocols and standards that are

currently used for AI connectivity. We believe that we are equally well-positioned—in terms of technology, products, and customer relationships—to address anticipated evolutions of AI connectivity architectures. We believe our competitive

advantages and strategic key customer engagements are due to the breadth of our solutions, our technology innovation, and our broad vertical integration, which improve our ability to ramp volume production and to offer the highest performance and

most cost-competitive solutions to the market. The retooling of datacenter architectures and integration of AI clusters by webscale and other cloud companies represent an immediate and direct growth opportunity for our Datacom business—both our

transceivers and our enabling active and passive components, especially leading-edge high-speed lasers.

13

Mix Heavily Weighted to Faster Growth, Higher Line Rate Transceivers. 800G Datacom transceiver

revenue accounted for almost 50% and together with 200G and 400G Datacom transceivers accounted for almost 80% of our total Datacom transceiver revenue in the quarter.

AI Transceiver Ramp Progression

As expected, we realized

meaningful improvements in both our supply chain constraints and our ability to ramp production in the third quarter. Our external supply chain shortages had less than a $10M adverse revenue impact in the quarter. All of the shortages impacted our

Datacom transceivers business. We expect an immaterial level of supply constraints going forward assuming, as always, no large spikes in customer demand or product design/configuration changes.

Telecom: Disappointing Near-Term; Unchanged Strong Longer-Term Outlook

Recovery in our Telecom vertical is proving slower than we had previously projected. Our Telecom revenue sequentially decreased in the third quarter and fell

short of our internal forecast, albeit modestly on both counts, and we expect relatively flat revenue growth in our current fourth quarter. The primary issue is soft end demand as communication service providers (CSPs), webscale, and other ICP

customers continue to delay projects and reduce or keep a tight rein on their capital expenditures.

Now Expect Start of Recovery in FY25. While

there remains some uncertainty regarding the timing of market recovery, we expect improvement in our Telecom revenue in fiscal 2025. Underlying our view, we see a number of drivers including ongoing rebound in Telecom revenue from China driven by

400G C+L-band network upgrades, increasing revenue contribution from our new transceivers targeted to the ZR and ZR+ coherent transceiver market opportunity, and share gains in certain key Telecom product

segments.

Unchanged Longer-Term Outlook. Unchanged from the preceding quarter, longer-term, we expect to benefit from ongoing market recovery;

strong customer traction for several new products that expand our addressable market; new market opportunities with a number of new, industry-leading products; and a variety of key emerging opportunities at new prospective direct customers. We are

especially excited about the number and quality of customer design win opportunities for our new 100G ZR and high-power 400G ZR/ZR+ pluggable transceivers at CSPs, webscale companies, and large NEMs. The 100G ZR transceivers are based on our

own internally developed Steelerton DSP, which represents a disruptive product in our portfolio. We currently are qualified and shipping our 400G ZR/ZR+ transceivers, and we expect to commence ramping production and commercial shipments of our new

100G ZR transceivers in the fourth quarter of fiscal 2024.

14

Lasers Segment: Sustained Improvement

In our Lasers segment, while the macroeconomic environment continues to impact demand, we saw additional signs of improvement in the quarter and continue to

expect to see further improvement in the fourth quarter of fiscal 2024 and beyond. Orders in our Lasers segment increased by over 7% sequentially and 17% year-over-year, and marked the highest level since our second quarter of fiscal 2023. Lasers

segment revenue was essentially unchanged from the preceding quarter but declined (by less than 5%) from the year-ago quarter. While having modestly declined on a sequential basis, our Display service revenue

increased by almost 30% from the year-ago quarter primarily driven by the ongoing increase in OLED fab utilization and depletion of service spare parts inventory.

Underlying our expectation for further Lasers improvement in the fourth quarter of fiscal 2024 and throughout fiscal 2025 and beyond, the sequential and

year-over-year order strength in the quarter reflects a number of key positive trends in our Display Capital Equipment and Semiconductor Capital Equipment verticals within our Industrial market. While macroeconomic uncertainty continues to restrain

current demand trends both in our Precision Manufacturing vertical within our Industrial market and in our Instrumentation market, we also expect favorable underlying trends in each of these to eventually contribute to meaningful incremental

improvement in our Lasers segment operating performance.

The key driver of demand for our Display Capital Equipment revenue is capacity expansion in

existing OLED fabs as well as the buildout of new Gen 8 OLED fabs. OLED growth is being driven by further adoption of OLED into smartphones, increasing OLED adoption into tablet and laptop computers, and a rebound in smartphone sales volumes from

the lowest levels in a decade.

We expect our excimer laser revenue in our Semiconductor Capital Equipment vertical to further strengthen in fiscal 2025.

We expect our Lasers segment also to benefit from ongoing penetration of the welding market opportunity with our ARM (Adjustable Ring Mode) laser system

particularly as it relates to battery welding. We are enjoying increasing market breadth and depth of customer adoption, which we expect to drive a corresponding ongoing strong ramp in revenue generation.

As discussed at greater length below, we remain excited as to our longer-term outlook for both our Industrial and Instrumentation markets.

Materials Segment: Enabling the 800G AI Ramp and Executing Multi-Year Fab Consolidation

While our Materials segment remains challenged, we saw a 7% sequential increase in orders in the quarter and expect additional improvement in our current

fourth quarter followed by more meaningful improvement throughout fiscal 2025. The sequential increase in orders marked the first quarter of improvement following a six-quarter downtrend including an over 20%

sequential decline in the preceding quarter. The sequential order increase in the quarter was primarily driven by strong demand for AI-related Datacom VCSELs. The increase also reflects the winding down of the

previously disclosed significant reduction in demand in our Consumer Electronics business driven by a design change by our largest Consumer Electronics customer. A key driver of our Materials segment revenue outlook for this initial rebound to

extend into and strengthen in fiscal 2025 is the demand for lasers for our internal Datacom transceiver ramp, combined with the substantial increase in demand from other transceiver manufacturers; this is requiring a substantial increase in

investment and a strong focus on product development and NPI ramps in our wafer fabs as we invest to expand capacity to support not only 800G and 1.6T for the next few years, but also the development of 3.2T technologies.

15

As part of our Synergies and Site Consolidation Plan, we have initiated consolidation of certain wafer fabs

to increase utilization and thereby profitability.

Silicon Carbide: Near-Term Challenges

We continue to be excited for the long-term growth outlook for our silicon carbide business based on what we expect to be robust silicon carbide end demand and

our strong competitive position. As we expected, however, the previously noted power failure adversely impacted our Silicon Carbide LLC revenue in the quarter. This issue also adversely impacted our third quarter gross margin for this business. We

are making progress working through the issue and expect a greater than 50% increase in our Silicon Carbide LLC revenue, which should also drive sequential improvement in our silicon carbide gross margin. We have moderated our fiscal 2025 silicon

carbide revenue growth outlook to take into account the industrywide slowdown in EV demand and production.

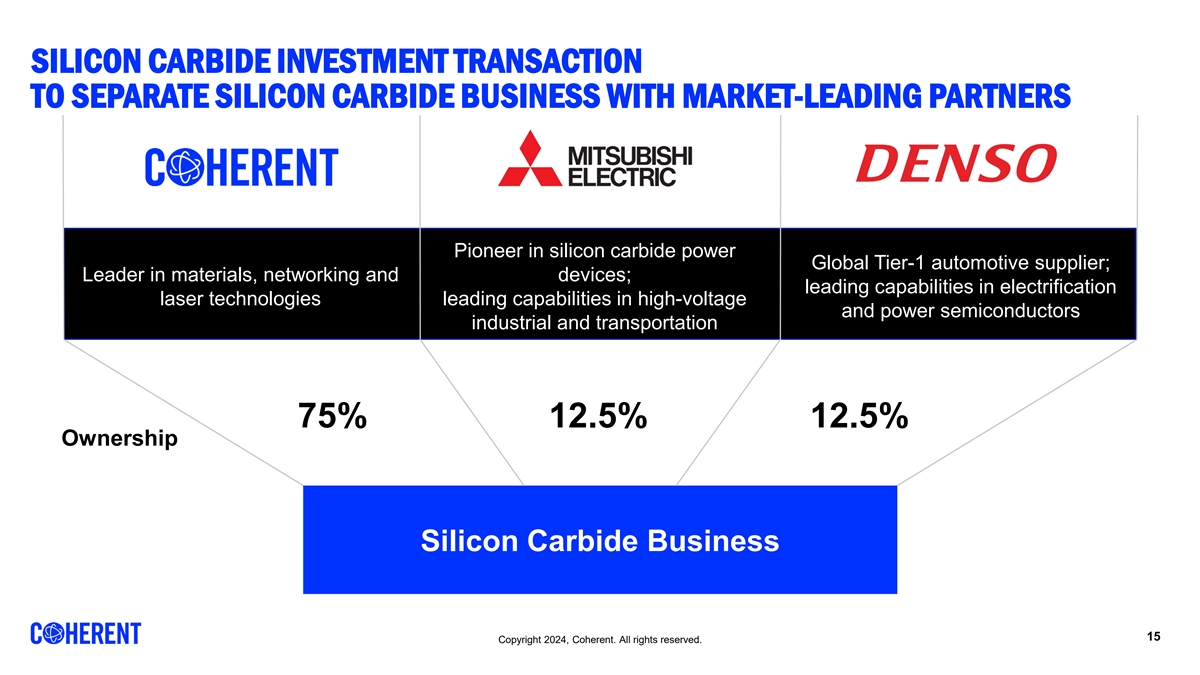

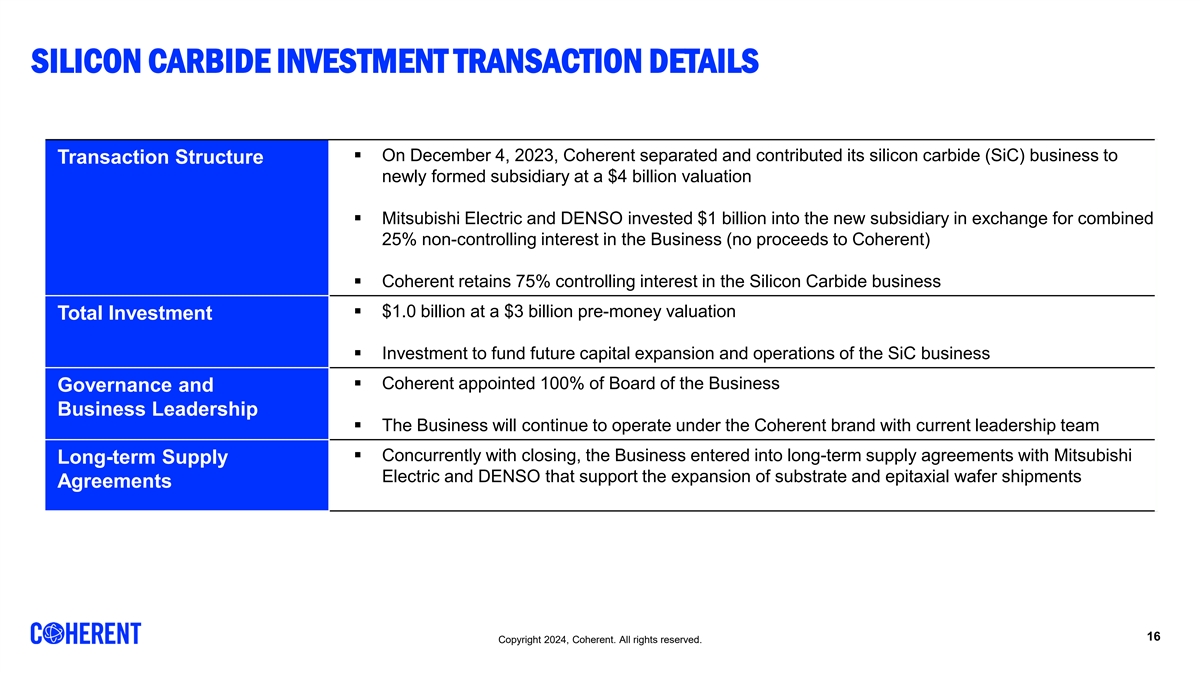

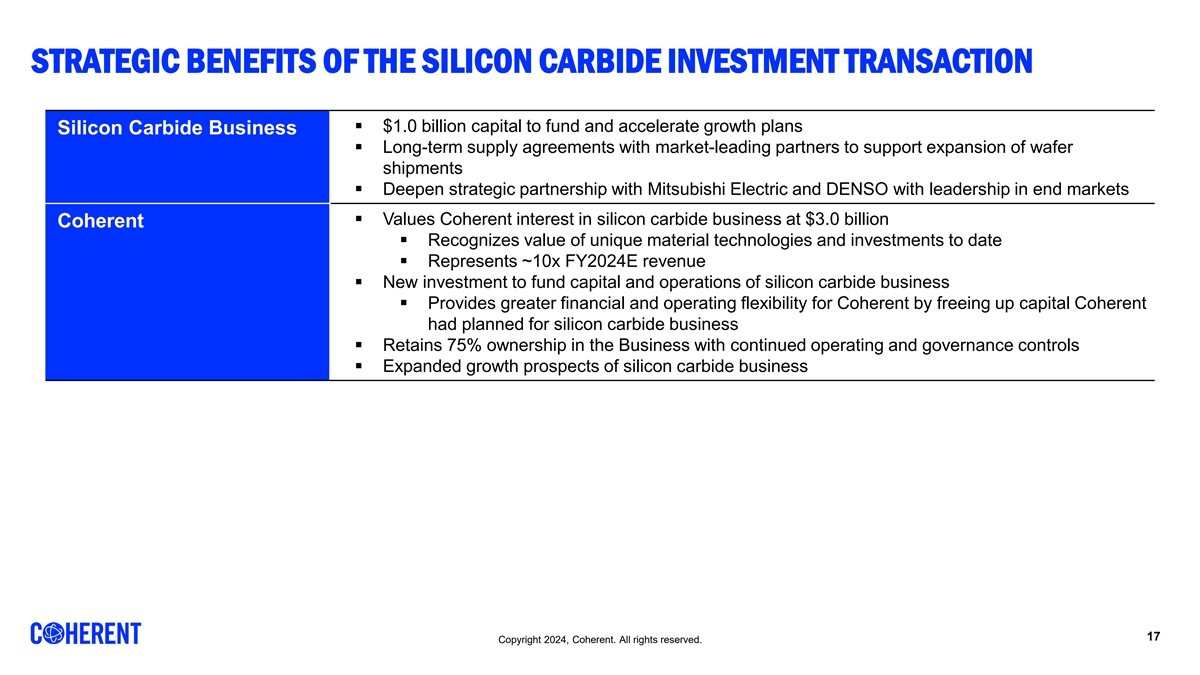

As a reminder, during the second quarter of

fiscal 2024, we consummated the previously announced transactions (the “Transactions”) with Mitsubishi Electric and DENSO Corporation pursuant to which those entities invested an aggregate of $1 billion in exchange for noncontrolling

ownership interests of 12.5% each in Silicon Carbide LLC, a newly formed LLC into which we contributed our silicon carbide business, and entered into long-term supply agreements that will support their demand for silicon carbide substrates and

epitaxial wafers.

The operating results of Silicon Carbide LLC are consolidated in our income statement with Mitsubishi Electric’s and DENSO’s

noncontrolling interests in Silicon Carbide LLC reported as “Net Loss Attributable to Noncontrolling Interests” below the Net Loss line on our income statement. The aggregate $1 billion of cash we received is reported as

“Restricted Cash (current and noncurrent)” on our balance sheet.

Capital Expenditure and Debt Reduction Outlook

We are tightening our capital expenditure outlook for fiscal 2024 to $365 – 385 million, with our Silicon Carbide LLC funding approximately

$150 million of this amount. In the third quarter of fiscal 2024, our total capital expenditure was $93 million, of which $52 million was funded by Silicon Carbide LLC. We expect capital expenditures of $115 – 135 million

for the current fourth quarter with Silicon Carbide LLC funding approximately $50 million of this amount.

We now expect aggregate debt repayment

between $225 – 250 million for all of fiscal 2024 compared to our previous expectation of $225 – 275 million from the preceding quarter. This outlook compares to approximately $200 million prior to our closing of the Silicon

Carbide Transactions.

As a reminder, the Transactions are expected to allow Coherent to increase its available free cash flow to provide greater

financial and operational flexibility to execute its capital allocation priorities including debt reduction. And as we have noted on previous occasions, the Transactions relieve the need for Coherent to fund future operating or capital expenditures

of Silicon Carbide LLC.

16

Trade Compliance Update on U.S. Restrictions: New Semiconductor-Related Export Controls – No

Meaningful Impact Expected

Unchanged from the preceding quarter, at present, we do not expect a meaningful adverse impact from the new round of export

control restrictions announced by the U.S. Department of Commerce on October 17, 2023. These newest restrictions target exports of certain integrated circuits and semiconductor manufacturing equipment to China and impose new end use and end

user controls to constrain certain technology development in China. As with others in the industry, we continue to assess these new rules and to update our compliance controls and actions to account for them.

17

PART II—FINANCIAL OVERVIEW

THIRD QUARTER FISCAL

Revenue. We generated

$1.209 billion in revenue, above our $1.020 – $1.200 billion guidance range and a 7% sequential increase but a 3% year-over-year decrease. Strong Networking segment revenue drove both the upside and the sequential growth. On a

year-over-year basis, a significant decrease in Materials revenue and modest decrease in Lasers revenue more than offset strong growth in Networking revenue to drive the overall revenue decline. Our revenue growth continues to be impacted by soft

end market demand due to the uncertain macroeconomic environment, inventory digestion in certain end markets including, most prominently, non-AI Datacom and Telecom, and a design change by a prominent customer

in our Consumer Electronics vertical.

| |

◾ |

Materials. Revenue of $239 million for our Materials segment decreased by approximately 6%

sequentially and by approximately 26% year-over-year but was only slightly below our internal forecast. The sequential and year-over-year decreases were primarily driven by sequential and year-over-year decreases in our Consumer Electronics revenue,

as we had expected, along with the production ramp issue that adversely impacted our Silicon Carbide LLC revenue in our Automotive vertical. |

| |

◾ |

Networking. Revenue of $619 million for our Networking segment healthily exceeded our internal

forecast, increased by approximately 18% sequentially and by approximately 12% year-over-year, and marked a quarterly record. The sequential increase was primarily driven by the almost 80% sequential increase in our

AI-related 800G Datacom transceiver revenue to almost $200 million for the quarter, which was partially offset by a sequential decrease in our Telecom revenue and ongoing weakness in our non-800G Datacom business. The year-over-year increase was primarily driven by the year-over-year increase in our AI-related Datacom revenue partially offset by significant

year-over-year revenue decreases for both our Telecom and non-800G Datacom businesses, both of which are primarily due to customer inventory digestion along with some project delays by customers in our Telecom

vertical. |

| |

◾ |

Lasers. Revenue of $351 million for our Lasers segment was essentially flat compared to the

preceding quarter, and a 4% decrease compared to the year-ago quarter. The slight sequential decrease was driven by our Industrial market. The year-over-year decrease was primarily driven by macroeconomic

uncertainty. As we observed in the preceding quarter, encouragingly, we are starting to see improvement in our Laser service revenue, primarily driven by increasing fab utilization and depleted inventory in our Display Capital Equipment market

segment, which in turn is driven by further OLED adoption in smartphones and the inception of OLED adoption in laptop computers and tablets. |

Non-GAAP EPS. Non-GAAP diluted earnings per share was $0.53, above the

high end of our $0.32 – 0.52 guidance range and up from $0.36 in the preceding quarter driven by the revenue upside partially offset by lower than expected gross margin.

Non-GAAP Gross Margin. 35.8%, which was below our 36 – 38% guidance range and a 20 bps sequential decrease

and over 150 bps year-over-year decrease. The primary drivers of the

18

sequential decrease were higher than expected COGS, which more than offset the sequential revenue increase. The primary drivers of the year-over-year decline were lower revenue, which resulted in

lower fixed cost absorption and higher than expected COGS, including lower yields in the datacom vertical and higher inventory provisions.

Non-GAAP Operating Expenses. $250 million or 20.7% of revenue, which is below the midpoint of our $246 – 262 million guidance but represents a sequential increase of $14 million and a

year-over-year increase of $4 million. Operating expenses as a percentage of revenue decreased by 15 bps sequentially but increased by 87 bps year-over-year. The primary driver of the sequential decrease was strong revenue growth partially

offset by higher IR&D expenses. The primary driver of the year-over-year increase was the rate of decrease in revenue combined with a slight increase in operating expenses.

Non-GAAP Operating Margin. 15.1%, which is just above the midpoint of our 14 – 16% guidance and is

a sequential decrease of 10 bps and a year-over-year decrease of 240 bps. The relatively flat sequential performance was driven by higher operating leverage from higher revenue and solid operating expense discipline which offset slightly lower gross

margin compared to the preceding quarter. The year-over-year decrease was primarily due to the year-over-year decrease in gross margin and to slightly higher operating expenses.

Operating Cash Flow. $117 million, compared to $152 million in the year-ago quarter and

$67 million in the preceding quarter.

Capital Expenditures. $93 million, $52 million of which was funded by our silicon carbide

business. As previously noted, we have tightened our capital expenditure outlook for fiscal 2024 to $365 – 385 million and we continue to expect the Silicon Carbide LLC to fund approximately $150 million of this amount.

Debt Reduction. In the quarter, we paid down $58 million of our outstanding debt.

Debt. Gross debt was approximately $4.2 billion and net debt was approximately $3.3 billion at the end of the quarter, compared to

$4.3 billion and $3.4 billion, respectively, at the end of the preceding quarter.

Leverage. Gross leverage was 4.4x and net leverage was

3.5x at the end of the quarter on a calculated basis, using the trailing 12 months of adjusted EBITDA at March 31, 2024, unchanged from the preceding quarter. Including the cost savings and synergy credit of $326 million allowed in the

credit facility, gross leverage was 3.3x and net leverage was 2.6x at the end of the quarter compared to 3.2x and 2.5x, respectively, at the end of the preceding quarter. The Company’s credit agreement allows for customary add backs to Adjusted

Consolidated EBITDA including cost savings, operating expense reductions, and synergies in connection with any restructuring, cost-saving initiative, or other initiatives.

| |

◾ |

Target: Our long-term leverage target remains 2.5x synergized gross leverage. |

19

Table 2

Other Financial Statistics

|

|

|

|

|

|

|

|

|

|

|

|

|

| $ Millions, except per share and percentage amounts

(unaudited) |

|

Q3 FY24 |

|

|

Q2 FY24 |

|

|

Q3 FY23 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Inventory |

|

|

1,292 |

|

|

|

1,292 |

|

|

|

1,394 |

|

| Cash |

|

|

899 |

|

|

|

856 |

|

|

|

884 |

|

| Restricted Cash - Total |

|

|

894 |

|

|

|

964 |

|

|

|

21 |

|

| Gross Debt |

|

|

4,234 |

|

|

|

4,292 |

|

|

|

4,520 |

|

| Net Debt |

|

|

3,335 |

|

|

|

3,436 |

|

|

|

3,636 |

|

| Calculated - Gross/Net leverage |

|

|

4.4x / 3.5x |

|

|

|

4.4x / 3.5x |

|

|

|

3.6x / 2.8x |

|

| Credit Facility - Gross/Net Leverage |

|

|

3.3x /2.6x |

|

|

|

3.2x /2.5x |

|

|

|

2.9x /2.3x |

|

| Debt Payments |

|

|

58 |

|

|

|

89 |

|

|

|

79 |

|

| Operating Cash Flow |

|

|

117 |

|

|

|

67 |

|

|

|

152 |

|

| Capital expenditures |

|

|

93 |

|

|

|

91 |

|

|

|

97 |

|

| Depreciation |

|

|

67 |

|

|

|

67 |

|

|

|

68 |

|

| Amortization |

|

|

72 |

|

|

|

72 |

|

|

|

93 |

|

| Fully diluted shares for NG EPS |

|

|

156 |

|

|

|

153 |

|

|

|

141 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

As previously noted, the Company has responded to the macroeconomic-driven impact on revenue growth that started in the second

half of fiscal 2023 with a major restructuring plan for fiscal 2023 – 2025, an acceleration of the site consolidation portion of our Synergy and Site Consolidation Plan, and other targeted strategic actions.

20

PART III—NEAR & LONG-TERM TRENDS BY MARKETS & REGIONS

MARKETS

We report in four major end markets, which

comprise ten verticals to provide transparency to investors.

INDUSTRIAL

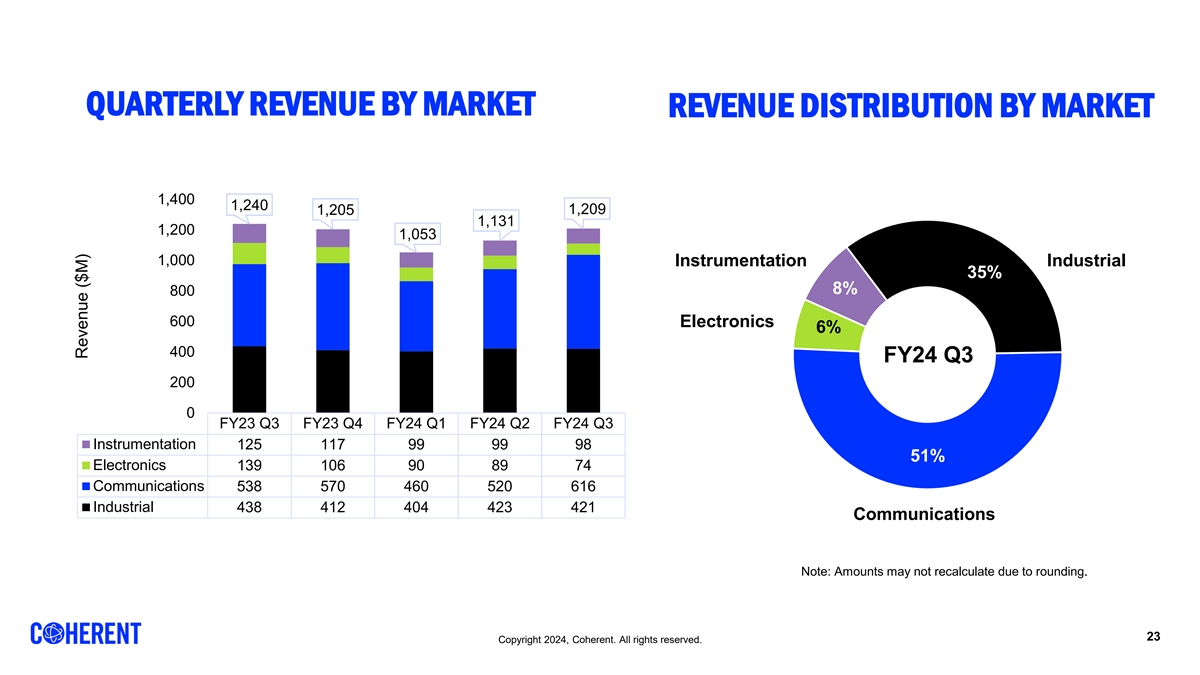

Revenue. Third quarter revenue of $421 million for our Industrial market was flat sequentially but decreased by 4% year-over-year. The flat

sequential revenue was driven by revenue decline in our Aerospace & Defense vertical offset by modest revenue growth in our Semiconductor Capital Equipment vertical while our Display Capital Equipment and Precision Manufacturing verticals

were essentially flat. The modest year-over-year revenue decline in our Industrial revenue was driven by decreases in our Semiconductor Capital Equipment (specifically driven by reduced revenue for products used in EUV applications) and Precision

Manufacturing verticals partially offset by year-over-year revenue growth in our Display Capital Equipment and Aerospace & Defense verticals.

Industrial Market Overview Webcast. As part of our ongoing effort to increase transparency and enhance the understanding of our investors, we discussed

our Industrial market in greater detail on our December 14, 2023, Industrial Market Overview webcast. A replay and investor presentation are available on our website at coherent.com/company/investor-relations/financial-webcasts.

Demand Trends. While the near-term outlook for our Industrial business remains challenged by the macroeconomic backdrop, we enjoyed another quarter of

improving demand trends in the third quarter, expect additional improvement in the fourth quarter of fiscal 2024 and expect even greater improvement in fiscal 2025, and are excited by a number of longer-term trends. Near-term, we are encouraged by a

strong order trend in our Industrial market. The third quarter marked another quarter of double-digit sequential order growth, and we expect this trend to extend into our current fiscal fourth quarter. We are seeing an especially strong demand trend

for our excimer lasers and related service revenue, which in turn are being driven by strong demand in our Display Capital Equipment vertical. The third quarter marked a third straight quarter of exceptionally strong double-digit order growth for

our Display vertical. Following strong sequential growth in the preceding fiscal second quarter, our Semicap orders were relatively flat in the third quarter, and we expect them to remain relatively unchanged in our current fourth quarter. While

orders in our Precision Manufacturing vertical slightly declined from the preceding quarter, we expect strong double-digit sequential improvement in our current fourth quarter.

A more in-depth discussion of trends within each of our Industrial verticals follows.

| |

1. |

Semiconductor Capital Equipment Vertical: Beyond the near-term growth we expect for our Semicap

vertical, we see favorable long-term demand trends for our Semicap business. We expect these trends to drive strong double-digit annual revenue growth in our Semicap vertical. |

| |

◾ |

Revenue. Revenue in our Semicap vertical increased by 4% sequentially but decreased by 4% compared to a year-ago record quarter. As discussed at greater length below, the sequential increase was driven by an initial rebound in back-end applications of this vertical while revenue

for front-end applications was relatively flat. |

21

| |

◾ |

Market Overview. As previously noted, over the long term, we expect strong annual revenue growth

in our Semicap vertical. Since fiscal 2020 we have driven record revenue every year in this vertical driven by the increased use of lasers, materials, and optics in advanced semicap tools. Near-term, we expect to see relatively flat revenue in our

current fourth quarter followed by improved revenue growth throughout fiscal 2025 with the benefit of the start of recovery in the semiconductor market following the current cyclical downturn. We have started to see recovery in the back-end assembly and packaging equipment segment of our Semicap vertical. Key Semicap end market drivers include increased demand for leading-edge chips for AI, high-performance computing, and automotive. We also

see favorable long-term demand trends for our Semicap business augmented by government policy-driven fab investments (i.e., government subsidies for expanding production capacity) and, most importantly, our increasing serviceable addressable market

(SAM) driven by portfolio expansion and the increased adoption of high-performance lasers, over the longer term. We enjoy a strong NRE-funded design-win pipeline from

existing and new customers across both front-end wafer processing and wafer inspection, among new applications. |

| |

◾ |

Front-End. We enjoy a particularly strong competitive position

in front-end Semicap, which accounts for most of our Semicap vertical revenue. We have a number of new programs and design wins on track to drive future incremental revenue. Our semiconductor wafer inspection

backlog remains strong. Our front-end laser business posted another quarter of solid sequential growth driven by a record quarter for laser shipments into wafer inspection. This growth was partially offset by

ongoing softness in our EUV business. |

| |

◾ |

EUV Rebound. Consistent with public statements by our end customer, we expect to see EUV inventory

normalization starting in our current fourth quarter of fiscal 2024 and expect to enjoy a rebound in EUV demand in fiscal 2025 as our end customer ramps up shipments of its EUV systems. Dozens of our solutions spanning our Materials and Lasers

segments are designed into these EUV systems. |

| |

◾ |

Back-End Rebound. As previously noted, we also expect to benefit

from recovery in the back-end assembly and packaging segment of our Semiconductor Capital Equipment vertical. After a prolonged period of softness, the back-end segment