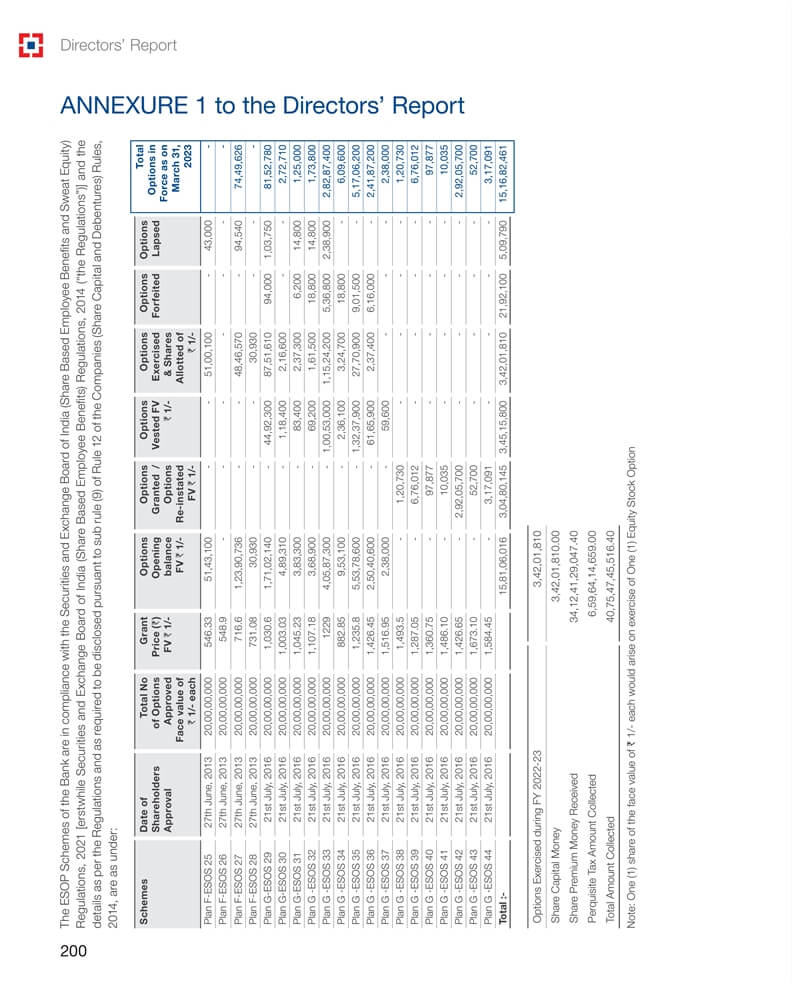

Directors’ Report ANNEXURE 1 to the Directors’ Report The ESOP Schemes of the Bank are in compliance

with the Securities and Exchange Board of India (Share Based Employee Benefits and Sweat Equity) Regulations, 2021 [erstwhile Securities and Exchange Board of India (Share Based Employee Benefits) Regulations, 2014 (“the Regulations”)] and

the details as per the Regulations and as required to be disclosed pursuant to sub rule (9) of Rule 12 of the Companies (Share Capital and Debentures) Rules, 014, are as under: Schemes Date of Total No Grant Options Options Options Options

Options Options Total - Options in Shareholders of Options Price (`) Opening Granted / Vested FV Exercised Forfeited Lapsed Approval Approved FV ` 1/- balance Options ` 1/- & Shares Force as on 003 Face value of FV ` 1/- Re-instated Allotted of March 31, ` 1/- each FV ` 1/- ` 1/- 2023 Plan F-ESOS 25 27th June, 2013 20,00,00,000 546.33 51,43,100 - 51,00,100 43,000 Plan F-ESOS 26 27th June, 2013 20,00,00,000 548.9 Plan F-ESOS 27 27th June, 2013 20,00,00,000 716.6 1,23,90,736 - 48,46,570 94,540

74,49,626 Plan F-ESOS 28 27th June, 2013 20,00,00,000 731.08 30,930 - 30,930 Plan

G-ESOS 29 21st July, 2016 20,00,00,000 1,030.6 1,71,02,140 - 44,92,300 87,51,610 94,000 1,03,750 81,52,780 Plan G-ESOS 30 21st July, 2016 20,00,00,000 1,003.03 4,89,310

- 1,18,400 2,16,600 2,72,710 Plan G-ESOS 31 21st July, 2016 20,00,00,000 1,045.23 3,83,300 - 83,400 2,37,300 6,200 14,800 1,25,000 Plan G -ESOS 32 21st July, 2016 20,00,00,000 1,107.18 3,68,900 - 69,200

1,61,500 18,800 14,800 1,73,800 Plan G -ESOS 33 21st July, 2016 20,00,00,000 1229 4,05,87,300 - 1,00,53,000 1,15,24,200 5,36,800 2,38,900 2,82,87,400 Plan G -ESOS 34 21st July, 2016 20,00,00,000 882.85 9,53,100 - 2,36,100 3,24,700 18,800 6,09,600

Plan G -ESOS 35 21st July, 2016 20,00,00,000 1,235.8 5,53,78,600 - 1,32,37,900 27,70,900 9,01,500 5,17,06,200 Plan G -ESOS 36 21st July, 2016 20,00,00,000 1,426.45 2,50,40,600 - 61,65,900 2,37,400 6,16,000 2,41,87,200 Plan G -ESOS 37 21st July, 2016

20,00,00,000 1,516.95 2,38,000 - 59,600 2,38,000 Plan G -ESOS 38 21st July, 2016 20,00,00,000 1,493.5 1,20,730 1,20,730 Plan G -ESOS 39 21st July, 2016 20,00,00,000 1,287.05 6,76,012 6,76,012 Plan G -ESOS 40 21st July, 2016 20,00,00,000 1,360.75

97,877 97,877 Plan G -ESOS 41 21st July, 2016 20,00,00,000 1,486.10 10,035 10,035 Plan G -ESOS 42 21st July, 2016 20,00,00,000 1,426.65 2,92,05,700

2,92,05,700 Plan G -ESOS 43 21st July, 2016 20,00,00,000 1,673.10 52,700 52,700 Plan G -ESOS 44 21st July, 2016 20,00,00,000 1,584.45 3,17,091 3,17,091 Total :- 15,81,06,016 3,04,80,145 3,45,15,800 3,42,01,810 21,92,100

5,09,790 15,16,82,461 Options Exercised during FY 2022-23 3,42,01,810 Share Capital Money 3,42,01,810.00 Share Premium Money Received 34,12,41,29,047.40 Perquisite Tax Amount Collected 6,59,64,14,659.00 Total

Amount Collected 40,75,47,45,516.40 Note: One (1) share of the face value of ` 1/- each would arise on exercise of One (1) Equity Stock Option 200