UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

SCHEDULE 13E-3

RULE 13E-3 TRANSACTION STATEMENT UNDER

SECTION 13(E) OF THE SECURITIES EXCHANGE ACT OF 1934

ARC Document Solutions, Inc.

(Name of the Issuer)

ARC Document Solutions, Inc.

TechPrint Holdings, LLC

TechPrint Merger Sub, Inc.

Kumarakulasingam Suriyakumar

Dilantha Wijesuriya

Jorge Avalos

Rahul Roy

Sujeewa Sean Pathiratne

Shiyulli Suriyakumar 2013 Irrevocable Trust

Seiyonne Suriyakumar 2013 Irrevocable Trust

Suriyakumar Family Trust

(Names of Persons Filing Statement)

Common Stock, Par Value $0.001 per share

(Title of Class of Securities)

Common Stock: 00191G103

(CUSIP Number of Class of Securities)

|

ARC Document Solutions, Inc.

12657 Alcosta Blvd, Suite 200

San Ramon, CA 94583

Tel: (925) 949-5100

|

Kumarakulasingam Suriyakumar

Dilantha Wijesuriya

Jorge Avalos

Rahul Roy

c/o ARC Document Solutions, Inc.

12657 Alcosta Blvd, Suite 200

San Ramon, CA 94583

Tel: (925) 949-5100

TechPrint Holdings, LLC

TechPrint Merger Sub, Inc.

Shiyulli Suriyakumar 2013 Irrevocable Trust

Seiyonne Suriyakumar 2013 Irrevocable Trust

Suriyakumar Family Trust

c/o TechPrint Holdings, LLC

12657 Alcosta Blvd., Suite 200

San Ramon, California 94583

Tel: (925) 949-5100

|

Sujeewa Sean Pathiratne

5727 Poppy Hills Place

San Jose, CA 94583

Tel: (925) 949-5100

|

(Name, Address and Telephone Number of Person Authorized to Receive

Notices and Communications on Behalf of the Persons Filing Statement)

With copies to

|

Glenn Luinenburg

Eric Hanson

Ryan S. Brewer

Wilmer Cutler Pickering Hale and Dorr LLP

2600 El Camino Real, Suite 400

Palo Alto, CA 94306

Tel: (650) 858-6000

|

Sean M. Jones

Coleman Wombwell

K&L Gates LLP

300 S. Tryon Street, Suite 1000

Charlotte, North Carolina 28202

Tel: (704) 331-7400

|

Terrence Allen, Esq.

Angela M. Dowd, Esq.

Janeane Ferrari, Esq.

Loeb & Loeb LLP

345 Park Avenue

New York, New York 10154

Tel: (212) 407-4000

|

| This statement is filed in connection with (check the appropriate box): |

| a. |

☒ |

The filing of solicitation materials or an information statement

subject to Regulation 14A, Regulation 14C or Rule 13e-3(c) under the Securities Exchange Act of 1934. |

| b. |

☐ |

The filing of a registration statement under the Securities Act of

1933. |

| c. |

☐ |

A tender offer. |

| d. |

☐ |

None of the above. |

Check the following box if the soliciting materials or information

statement referred to in checking box (a) are preliminary copies: ☒

Check the following box if the filing is a final amendment reporting the

results of the transaction: ☐

Neither the Securities and Exchange Commission nor any state securities

commission has approved or disapproved of this transaction, passed upon the merits or fairness of this transaction, or passed upon the adequacy or accuracy of the disclosure in this transaction statement on Schedule 13E-3. Any representation to the

contrary is a criminal offense.

INTRODUCTION

This Rule 13e-3 Transaction Statement on Schedule 13E-3, together with the

exhibits hereto (this “Schedule 13E-3” or “Transaction Statement”), is being filed with the U.S. Securities and Exchange Commission (the “SEC”) pursuant to Section 13(e) of the Securities Exchange Act of 1934, as amended

(together with the rules and regulations promulgated thereunder, the “Exchange Act”), jointly by the following persons (each, a “Filing Person,” and collectively, the “Filing Persons”): (i) ARC Document Solutions, Inc. (“ARC”

or the “Company”), a Delaware corporation and the issuer of the common stock, par value $0.001 per share (the “ARC Common Stock”), that is subject to the Rule 13e-3 transaction, (ii) TechPrint Holdings, LLC, a Delaware limited liability

company (“Parent”), (iii) TechPrint Merger Sub, Inc., a Delaware corporation and wholly owned subsidiary of Parent (“Merger Sub”), (iv) Kumarakulasingam Suriyakumar, (v) Dilantha Wijesuriya, (vi) Jorge Avalos, (vii) Rahul Roy, (viii)

Sujeewa Sean Pathiratne, (ix) Shiyulli Suriyakumar 2013 Irrevocable Trust, (x) Seiyonne Suriyakumar 2013 Irrevocable Trust, and (xi) Suriyakumar Family Trust (together with Filing Persons (iv) through (x), the “Acquisition Group”).

On August 27, 2024, the Company, Parent and Merger Sub entered into an

Agreement and Plan of Merger (as subsequently amended on September 10, 2024) (as amended, restated, supplemented or otherwise modified from time to time, the “Merger Agreement”), pursuant to which, subject to the satisfaction or waiver of

certain conditions and on the terms set forth therein, pursuant to which Merger Sub will merge with and into ARC with ARC surviving the merger as the surviving corporation (the “Surviving Corporation”) and a wholly-owned subsidiary of Parent

(the “Merger”). Concurrently with the filing of this Transaction Statement, the Company is filing with the SEC its preliminary Proxy Statement (the “Proxy Statement”) under Regulation 14A of the Exchange Act, relating to a special

meeting of the stockholders of the Company (the “Special Meeting”) at which the stockholders of the Company will consider and vote upon a proposal to (i) approve and adopt the Merger Agreement and the transactions contemplated thereby,

including the Merger, (ii) approve, by nonbinding, advisory vote, certain compensation arrangements for ARC’s named executive officers in connection with the Merger and (iii) a proposal to adjourn the Special Meeting, if necessary or appropriate,

including adjournments to solicit additional proxies if there are insufficient votes at the time of the Special Meeting to adopt the Merger Agreement. The adoption of the Merger Agreement will require the affirmative vote of the holders of a majority

of the outstanding shares of ARC Common Stock entitled to vote, outstanding as of the close of business on the record date for the Special Meeting. A copy of the Proxy Statement is attached hereto as Exhibit (a)(2)(i) and incorporated herein by

reference. A copy of the agreement and plan of merger and the amendment thereto are attached hereto as Exhibits (d)(i) and (d)(ii), respectively, and are included as Annex A to the Proxy Statement and incorporated herein by reference.

Under the terms of the Merger Agreement, and subject to the conditions

thereof, at the effective time of the Merger (the “Effective Time”), among other things, each share of ARC Common Stock outstanding immediately prior to the Effective Time, other than as provided below, will be converted into the right to

receive $3.40 in cash (the “Merger Consideration”), without interest and less any applicable withholding taxes. The following shares of ARC Common Stock will not be converted into the right to receive the Merger Consideration in connection

with the Merger: (i) shares of ARC Common Stock held by Merger Sub or the Company or its subsidiaries as treasury stock or otherwise, (ii) shares ARC Common Stock owned by Parent immediately prior to the Effective Time of the Merger, (iii) shares of

ARC Common Stock held by members of the Acquisition Group to be contributed to Parent immediately prior to the Effective Time in exchange for common units of Parent pursuant to the rollover agreement, dated as of August 27, 2024 (as subsequently

amended on September 10, 2024), by and among Parent and the members of the Acquisition Group (such agreement, as amended, restated, supplemented or otherwise modified from time to time, the “Rollover Agreement” and such shares, the “Rollover

Shares”) and (iv) shares of ARC Common Stock that are issued and outstanding immediately prior to the Effective Time (other than Rollover Shares) and that have not been voted in favor of the adoption of the Merger Agreement or consented thereto

in writing, whose holders are entitled to demand appraisal rights with respect to such shares of ARC Common Stock, and whose holders have properly exercised and validly perfected appraisal rights with respect to such shares of ARC Common Stock in

accordance with, and who have complied in all respects with, and have not effectively withdrawn, failed to perfect, or otherwise lost such holder’s rights to appraisal with respect to such shares of ARC Common Stock, in each case, Section 262 of the

General Corporation Law of the State of Delaware (the “DGCL”), a copy of which is attached hereto as Exhibit (f) and is also included as Annex G to the Proxy Statement and incorporated herein by reference. A copy of the rollover agreement and

the amendment thereto are attached hereto as Exhibits (d)(iii) and (d)(iv), respectively, and are also included as Annex C to the Proxy Statement and incorporated herein by reference.

The cross-references below are being supplied pursuant to General

Instruction G to Schedule 13E-3 and show the location in the Proxy Statement of the information required to be included in response to the items of Schedule 13E-3. Pursuant to General Instruction F to Schedule 13E-3, the information contained in the

Proxy Statement, including all annexes and appendices thereto, is incorporated in its entirety herein by reference, and the responses to each item in this Schedule 13E-3 are qualified in their entirety by the information contained in the Proxy

Statement and the annexes and appendices thereto.

Capitalized terms used but not expressly defined in this Schedule 13E-3

shall have the respective meanings given to them in the Proxy Statement.

The information concerning ARC contained in, or incorporated by reference

into, this Schedule 13E-3 and the Proxy Statement was supplied by ARC. Similarly, all information concerning each other Filing Person contained in, or incorporated by reference into this Schedule 13E-3 and the Proxy Statement was supplied by such

Filing Person. No Filing Person, including ARC, is responsible for the accuracy of any information supplied by any other Filing Person.

While each of the Filing Persons acknowledges that the Merger is a “going

private” transaction for purposes of Rule 13e-3 under the Exchange Act, the filing of this Transaction Statement shall not be construed as an admission by any Filing Person, or by any affiliate of a Filing Person, that the Company is “controlled” by

any Filing Person.

| Item 1. |

Summary Term Sheet |

The information set forth in the Proxy Statement under the following

captions is incorporated herein by reference:

“SUMMARY TERM SHEET”

“QUESTIONS AND ANSWERS ABOUT THE PROPOSALS AND THE

SPECIAL MEETING”

| Item 2. |

Subject Company Information |

(a) Name and Address. The information set forth in the Proxy

Statement under the following caption is incorporated herein by reference:

“PARTIES TO THE MERGER”

(b) Securities. The information set forth in the Proxy Statement

under the following captions is incorporated herein by reference:

“SUMMARY TERM SHEET”

“QUESTIONS AND ANSWERS ABOUT THE PROPOSALS AND THE

SPECIAL MEETING”

“THE SPECIAL MEETING - Voting”

“THE SPECIAL MEETING - Record Date and Quorum”

“OTHER IMPORTANT INFORMATION REGARDING ARC - Market

for ARC Common Stock and Dividends”

“OTHER IMPORTANT INFORMATION REGARDING

ARC - Security Ownership of Certain Beneficial Owners and Management”

(c) Trading Market and Price. The information set forth in the Proxy

Statement under the following caption is incorporated herein by reference:

“SUMMARY TERM SHEET – Other Important Information Regarding ARC”

“OTHER IMPORTANT INFORMATION REGARDING ARC- Market for ARC

Common Stock and Dividends”

(d) Dividends. The information set forth in the Proxy Statement

under the following caption is incorporated herein by reference:

“OTHER IMPORTANT INFORMATION REGARDING ARC - Market for ARC

Common Stock and Dividends”

“THE MERGER AGREEMENT - Conduct of Business Pending the Merger”

(e) Prior Public Offerings. The information set forth in the Proxy

Statement under the following caption is incorporated herein by reference:

“OTHER IMPORTANT INFORMATION REGARDING ARC - Prior

Public Offerings”

(f) Prior Stock Purchases. The information set forth in the Proxy

Statement under the following caption is incorporated herein by reference:

“OTHER IMPORTANT INFORMATION REGARDING ARC - Stock

Repurchases”

“OTHER IMPORTANT INFORMATION REGARDING ARC - Certain Transactions in

the Shares of ARC Common Stock”

| Item 3. |

Identity and Background of Filing Person |

(a)-(c) Name and Address; Business and Background of Entities; Business

and Background of Natural Persons. ARC is the subject company. The information set forth in the Proxy Statement under the following captions is incorporated herein by reference:

“SUMMARY TERM SHEET – Parties to the Merger”

“PARTIES TO THE MERGER”

“OTHER IMPORTANT INFORMATION REGARDING ARC”

“OTHER IMPORTANT INFORMATION REGARDING THE PURCHASER

FILING PARTIES”

(d) Tender Offer. Not applicable.

| Item 4. |

Terms of the Transaction |

(a)(1) Material Terms. Tender Offers. Not Applicable.

(a)(2) Material Terms. Mergers or Similar Transactions. The

information set forth in the Proxy Statement under the following captions is incorporated herein by reference:

“SUMMARY TERM SHEET”

“QUESTIONS AND ANSWERS ABOUT THE PROPOSALS AND THE

SPECIAL MEETING”

“SPECIAL FACTORS - Background of the Merger”

“SPECIAL FACTORS - Purpose and Reasons of ARC for the Merger;

Recommendations of the ARC Board and the Special Committee; Fairness of the Merger”

“SPECIAL FACTORS - Position of the Purchaser Filing Parties as to

the Fairness of the Merger”

“SPECIAL FACTORS - Purpose and Reasons of the Purchaser Filing

Parties for the Merger”

“SPECIAL FACTORS - Plans for ARC After the Merger”

“SPECIAL FACTORS - Certain Effects of the Merger”

“SPECIAL FACTORS - Interests of Executive Officers and Directors of

ARC in the Merger”

“SPECIAL FACTORS - Material U.S. Federal Income Tax Consequences of

the Merger”

“SPECIAL FACTORS - Financing of the Merger”

“SPECIAL FACTORS - Accounting Treatment”

“THE MERGER AGREEMENT”

“THE SPECIAL MEETING - Vote Required”

Annex A – Merger Agreement

(c) Different Terms. The information set forth in the Proxy

Statement under the following captions is incorporated herein by reference:

“SUMMARY TERM SHEET”

“SPECIAL FACTORS - Plans for ARC After the Merger”

“SPECIAL FACTORS - Certain Effects of the Merger”

“SPECIAL FACTORS - Interests of Executive Officers and Directors of

ARC in the Merger”

“SPECIAL FACTORS - Financing of the Merger”

“SPECIAL FACTORS – Limited Guarantee”

“SPECIAL FACTORS – Voting Agreement”

Annex A – Merger Agreement

Annex C – Rollover Agreement

Annex E –Voting Agreement

Annex H – Limited Guarantee

(d) Appraisal Rights. The information set forth in the Proxy

Statement under the following captions is incorporated herein by reference:

“SPECIAL FACTORS - Appraisal Rights”

“THE MERGER AGREEMENT - Merger Consideration”

“THE SPECIAL MEETING - Appraisal Rights”

“THE MERGER (THE MERGER AGREEMENT PROPOSAL - PROPOSAL 1) - Appraisal

Rights”

Annex A – Merger Agreement

Annex G - Section 262 of the DGCL

(e) Provisions for Unaffiliated Security Holders. The information

set forth in the Proxy Statement under the following captions is incorporated herein by reference:

“SPECIAL FACTORS - Purpose and Reasons of ARC for the Merger;

Recommendations of the ARC Board and the Special Committee; Fairness of the Merger”

“PROVISIONS FOR UNAFFILIATED STOCKHOLDERS”

(f) Eligibility for Listing or Trading. Not Applicable.

| Item 5. |

Past Contacts, Transactions, Negotiations and Agreements |

(a) Transactions. The information set forth in the Proxy Statement

under the following captions is incorporated herein by reference:

“SUMMARY TERM SHEET”

“SPECIAL FACTORS - Background of the Merger”

“SPECIAL FACTORS - Interests of Executive Officers and Directors of

ARC in the Merger”

“SPECIAL FACTORS - Financing of the Merger”

“SPECIAL FACTORS – Voting Agreement”

“THE MERGER AGREEMENT”

“OTHER IMPORTANT INFORMATION REGARDING ARC - Certain Transactions in

the Shares of ARC Common Stock”

“WHERE YOU CAN FIND MORE INFORMATION”

Annex A – Merger Agreement

Annex C – Rollover Agreement

Annex D –Voting Agreement

(b) Significant Corporate Events. The information set forth in the

Proxy Statement under the following captions is incorporated herein by reference:

“SUMMARY TERM SHEET”

“QUESTIONS AND ANSWERS ABOUT THE PROPOSALS AND THE SPECIAL MEETING”

“SPECIAL FACTORS - Background of the Merger”

“SPECIAL FACTORS - Purpose and Reasons of ARC for the Merger;

Recommendations of the ARC Board and the Special Committee; Fairness of the Merger”

“SPECIAL FACTORS - Purpose and Reasons of the Purchaser Filing

Parties for the Merger”

“SPECIAL FACTORS - Plans for ARC After the Merger”

“SPECIAL FACTORS - Certain Effects of the Merger”

“SPECIAL FACTORS - Interests of Executive Officers and Directors of

ARC in the Merger”

“SPECIAL FACTORS - Financing of the Merger”

“SPECIAL FACTORS - Limited Guarantee”

“SPECIAL FACTORS – Voting Agreement”

“THE MERGER AGREEMENT”

Annex A – Merger Agreement

Annex C – Rollover Agreement

Annex D –Voting Agreement

Annex H – Limited Guarantee

(c) Negotiations or Contacts. The information set forth in the Proxy

Statement under the following captions is incorporated herein by reference:

“SPECIAL FACTORS - Background of the Merger”

“SPECIAL FACTORS - Purpose and Reasons of ARC for the Merger;

Recommendations of the ARC Board and the Special Committee; Fairness of the Merger”

“SPECIAL FACTORS - Purpose and Reasons of the Purchaser Filing

Parties for the Merger”

“SPECIAL FACTORS - Plans for ARC After the Merger”

“SPECIAL FACTORS - Interests of Executive Officers and Directors of

ARC in the Merger”

“THE MERGER AGREEMENT”

(e) Agreements Involving the Subject Company’s Securities. The

information set forth in the Proxy Statement under the following captions is incorporated herein by reference:

“SUMMARY TERM SHEET”

“QUESTIONS AND ANSWERS ABOUT THE PROPOSALS AND THE SPECIAL MEETING”

“SPECIAL FACTORS - Background of the Merger”

“SPECIAL FACTORS - Plans for ARC After the Merger”

“SPECIAL FACTORS - Certain Effects of the Merger”

“SPECIAL FACTORS - Interests of Executive Officers and Directors of

ARC in the Merger”

“SPECIAL FACTORS - Intent of the Directors and Executive Officers to

Vote in Favor of the Merger”

“SPECIAL FACTORS - Intent of the Purchaser Filing Parties to Vote in

Favor of the Merger”

“SPECIAL FACTORS - Financing of the Merger”

“SPECIAL FACTORS - Limited Guarantee”

“SPECIAL FACTORS – Voting Agreement”

“THE MERGER AGREEMENT”

“OTHER IMPORTANT INFORMATION REGARDING ARC - Certain Transactions in

the Shares of ARC Common Stock”

“WHERE YOU CAN FIND MORE INFORMATION”

Annex A – Merger Agreement

Annex C – Rollover Agreement

Annex D –Voting Agreement

Annex H – Limited Guarantee

| Item 6. |

Purposes of the Transaction and Plans or Proposals |

(b) Use of Securities Acquired. The information set forth in the

Proxy Statement under the following captions is incorporated herein by reference:

“QUESTIONS AND ANSWERS ABOUT THE PROPOSALS AND THE SPECIAL MEETING”

“SPECIAL FACTORS - Purpose and Reasons of the Purchaser Filing

Parties for the Merger”

“SPECIAL FACTORS - Plans for ARC After the Merger”

“SPECIAL FACTORS - Certain Effects of the Merger”

“SPECIAL FACTORS - Exchange and Payment Procedures”

“THE MERGER AGREEMENT”

“DELISTING AND DEREGISTRATION OF COMMON STOCK”

Annex A – Merger Agreement

(c)(1)-(8) Plans. The information set forth in the Proxy Statement

under the following captions is incorporated herein by reference:

“SUMMARY TERM SHEET”

“QUESTIONS AND ANSWERS ABOUT THE PROPOSALS AND THE SPECIAL MEETING”

“SPECIAL FACTORS - Background of the Merger”

“SPECIAL FACTORS - Purpose and Reasons of ARC for the Merger;

Recommendations of the ARC Board and the Special Committee; Fairness of the Merger”

“SPECIAL FACTORS - Position of the Purchaser Filing Parties as to

the Fairness of the Merger”

“SPECIAL FACTORS - Purpose and Reasons of the Purchaser Filing

Parties for the Merger”

“SPECIAL FACTORS - Plans for ARC After the Merger”

“SPECIAL FACTORS - Certain Effects of the Merger”

“SPECIAL FACTORS - Interests of Executive Officers and Directors of

ARC in the Merger”

“SPECIAL FACTORS - Intent of the Directors and Executive Officers to

Vote in Favor of the Merger”

“SPECIAL FACTORS - Intent of the Purchaser Filing Parties to Vote in

Favor of the Merger”

“SPECIAL FACTORS - Financing of the Merger”

“SPECIAL FACTORS - Limited Guarantee”

“SPECIAL FACTORS – Voting Agreement”

“THE MERGER AGREEMENT”

“THE SPECIAL MEETING”

“DELISTING AND DEREGISTRATION OF COMMON STOCK”

Annex A – Merger Agreement

Annex C – Rollover Agreement

Annex E –Voting Agreement

| Item 7. |

Purposes, Alternatives, Reasons and Effects |

(a) Purposes. The information set forth in the Proxy Statement under

the following captions is incorporated herein by reference:

“SUMMARY TERM SHEET”

“QUESTIONS AND ANSWERS ABOUT THE PROPOSALS AND THE SPECIAL MEETING”

“SPECIAL FACTORS - Background of the Merger”

“SPECIAL FACTORS - Purpose and Reasons of ARC for the Merger;

Recommendations of the ARC Board and the Special Committee; Fairness of the Merger”

“SPECIAL FACTORS - Position of the Purchaser Filing Parties as to

the Fairness of the Merger”

“SPECIAL FACTORS - Purpose and Reasons of the Purchaser Filing

Parties for the Merger”

“SPECIAL FACTORS - Plans for ARC After the Merger”

“SPECIAL FACTORS - Certain Effects of the Merger”

(b) Alternatives. The information set forth in the Proxy Statement

under the following captions is incorporated herein by reference:

“SPECIAL FACTORS - Background of the Merger”

“SPECIAL FACTORS - Purpose and Reasons of ARC for the Merger;

Recommendations of the ARC Board and the Special Committee; Fairness of the Merger”

“SPECIAL FACTORS - Position of the Purchaser Filing Parties as to

the Fairness of the Merger”

“SPECIAL FACTORS - Purpose and Reasons of the Purchaser Filing

Parties for the Merger”

“SPECIAL FACTORS - Certain Effects on ARC if the Merger is Not

Completed”

(c) Reasons. The information set forth in the Proxy Statement under

the following captions is incorporated herein by reference:

“SPECIAL FACTORS - Background of the Merger”

“SPECIAL FACTORS - Purpose and Reasons of ARC for the Merger;

Recommendations of the ARC Board and the Special Committee; Fairness of the Merger”

“SPECIAL FACTORS - Opinion of the Special Committee’s Financial

Advisor”

“SPECIAL FACTORS - Position of the Purchaser Filing Parties as to

the Fairness of the Merger”

“SPECIAL FACTORS - Purpose and Reasons of the Purchaser Filing

Parties for the Merger”

“SPECIAL FACTORS - Plans for ARC After the Merger”

“SPECIAL FACTORS - Certain Effects of the Merger”

Annex B - Opinion of William Blair & Company, L.L.C.

(d) Effects. The information set forth in the Proxy Statement under

the following captions is incorporated herein by reference:

“SUMMARY TERM SHEET”

“QUESTIONS AND ANSWERS ABOUT THE PROPOSALS AND THE SPECIAL MEETING”

“SPECIAL FACTORS - Background of the Merger”

“SPECIAL FACTORS - Purpose and Reasons of ARC for the Merger;

Recommendations of the ARC Board and the Special Committee; Fairness of the Merger”

“SPECIAL FACTORS - Position of the Purchaser Filing Parties as to

the Fairness of the Merger”

“SPECIAL FACTORS - Purpose and Reasons of the Purchaser Filing

Parties for the Merger”

“SPECIAL FACTORS - Plans for ARC After the Merger”

“SPECIAL FACTORS - Certain Effects of the Merger”

“SPECIAL FACTORS - Certain Effects on ARC if the Merger is Not

Completed”

“SPECIAL FACTORS - Financing of the Merger”

“SPECIAL FACTORS - Interests of Executive Officers and Directors of

ARC in the Merger”

“SPECIAL FACTORS - Material U.S. Federal Income Tax Consequences of

the Merger”

“SPECIAL FACTORS - Fees and Expenses”

“SPECIAL FACTORS - Accounting Treatment”

“SPECIAL FACTORS - Exchange and Payment Procedures”

“THE MERGER AGREEMENT”

“DELISTING AND DEREGISTRATION OF COMMON STOCK”

Annex A – Merger Agreement

| Item 8. |

Fairness of the Transaction |

(a), (b) Fairness; Factors Considered in Determining Fairness. The

information set forth in the Proxy Statement under the following captions is incorporated herein by reference:

“SUMMARY TERM SHEET”

“QUESTIONS AND ANSWERS ABOUT THE PROPOSALS AND THE SPECIAL MEETING”

“SPECIAL FACTORS - Background of the Merger”

“SPECIAL FACTORS - Purpose and Reasons of ARC for the Merger;

Recommendations of the ARC Board and the Special Committee; Fairness of the Merger”

“SPECIAL FACTORS - Opinion of the Special Committee’s Financial

Advisor”

“SPECIAL FACTORS - Position of the Purchaser Filing Parties as to

the Fairness of the Merger”

“SPECIAL FACTORS - Purpose and Reasons of the Purchaser Filing

Parties for the Merger”

“SPECIAL FACTORS - Interests of Executive Officers and Directors of

ARC in the Merger”

“THE MERGER AGREEMENT”

Annex B - Opinion of William Blair & Company, L.L.C.

(c) Approval of Security Holders. The information set forth in the

Proxy Statement under the following captions is incorporated herein by reference:

“SUMMARY TERM SHEET”

“QUESTIONS AND ANSWERS ABOUT THE PROPOSALS AND THE SPECIAL MEETING”

“THE MERGER AGREEMENT - Conditions to the Closing of the Merger”

“THE SPECIAL MEETING - Record Date and Quorum”

“THE SPECIAL MEETING - Vote Required”

“THE SPECIAL MEETING - Voting”

“THE SPECIAL MEETING - Abstentions”

“THE SPECIAL MEETING - How to Vote”

“THE SPECIAL MEETING - Proxies and Revocation”

Annex A – Merger Agreement

(d) Unaffiliated Representative. The information set forth in the

Proxy Statement under the following captions is incorporated herein by reference:

“SUMMARY TERM SHEET”

“SPECIAL FACTORS - Background of the Merger”

“SPECIAL FACTORS - Purpose and Reasons of ARC for the Merger;

Recommendations of the ARC Board and the Special Committee; Fairness of the Merger”

“SPECIAL FACTORS - Opinion of the Special Committee’s Financial

Advisor”

“SPECIAL FACTORS - Position of the Purchaser Filing Parties as to

the Fairness of the Merger”

“SPECIAL FACTORS - Purpose and Reasons of the Purchaser Filing

Parties for the Merger”

(e) Approval of Directors. The information set forth in the Proxy

Statement under the following captions is incorporated herein by reference:

“SUMMARY TERM SHEET”

“QUESTIONS AND ANSWERS ABOUT THE PROPOSALS AND THE SPECIAL MEETING”

“SPECIAL FACTORS - Background of the Merger”

“SPECIAL FACTORS - Purpose and Reasons of ARC for the Merger;

Recommendations of the ARC Board and the Special Committee; Fairness of the Merger”

“SPECIAL FACTORS - Position of the Purchaser Filing Parties as to

the Fairness of the Merger”

(f) Other Offers. The information set forth in the Proxy Statement

under the following captions is incorporated herein by reference:

“SPECIAL FACTORS - Background of the Merger”

“SPECIAL FACTORS - Purpose and Reasons of ARC for the Merger;

Recommendations of the ARC Board and the Special Committee; Fairness of the Merger”

“SPECIAL FACTORS - Position of the Purchaser Filing Parties as to

the Fairness of the Merger”

“SPECIAL FACTORS - Purpose and Reasons of the Purchaser Filing

Parties for the Merger”

“THE MERGER AGREEMENT - Solicitation of Other Offers”

“THE MERGER AGREEMENT – Change of Recommendation”

Annex A – Merger Agreement

| Item 9. |

Reports, Opinions, Appraisals and Negotiations |

(a), (b) Report, Opinion or Appraisal; Preparer and Summary of the

Report, Opinion or Appraisal. The information set forth in the Proxy Statement under the following captions is incorporated herein by reference:

“SUMMARY TERM SHEET”

“QUESTIONS AND ANSWERS ABOUT THE PROPOSALS AND THE SPECIAL MEETING”

“SPECIAL FACTORS - Background of the Merger”

“SPECIAL FACTORS - Purpose and Reasons of ARC for the Merger;

Recommendations of the ARC Board and the Special Committee; Fairness of the Merger”

“SPECIAL FACTORS - Opinion of the Special Committee’s Financial

Advisor”

“SPECIAL FACTORS - Position of the Purchaser Filing Parties as to

the Fairness of the Merger”

“SPECIAL FACTORS - Purpose and Reasons of the Purchaser Filing

Parties for the Merger”

“WHERE YOU CAN FIND MORE INFORMATION”

Annex B - Opinion of William Blair & Company, L.L.C.

(c) Availability of Documents. The reports, opinions or appraisals

referenced in this Item 9 will be made available for inspection and copying at the principal executive offices of ARC during its regular business hours by any interested equity holder of ARC Common Stock or by a representative who has been so

designated in writing.

| Item 10. |

Source and Amount of Funds or Other Consideration |

(a), (b) Source of Funds; Conditions. The information set forth in

the Proxy Statement under the following captions is incorporated herein by reference:

“SUMMARY TERM SHEET”

“SPECIAL FACTORS - Financing of the Merger”

“SPECIAL FACTORS - Limited Guarantee”

“SPECIAL FACTORS - Interests of Executive Officers and Directors of

ARC in the Merger”

“SPECIAL FACTORS - Exchange and Payment Procedures”

“THE MERGER AGREEMENT - Effect of the Merger”

“THE MERGER AGREEMENT - Closing and Effective Time”

“THE MERGER AGREEMENT - Conduct of Business Pending the Merger”

“THE MERGER AGREEMENT - Conditions to the Closing of the Merger”

Annex A – Merger Agreement

(c) Expenses. The information set forth in the Proxy Statement under

the following captions is incorporated herein by reference:

“SPECIAL FACTORS - Fees and Expenses”

“THE MERGER AGREEMENT - Termination of the Merger Agreement”

“THE MERGER AGREEMENT - Termination Fees”

“THE MERGER AGREEMENT - Fees and Expenses”

“THE SPECIAL MEETING - Solicitation of Proxies; Payment of

Solicitation Expenses”

Annex A – Merger Agreement

(d) Borrowed Funds.

“SPECIAL FACTORS - Financing of the Merger”

| Item 11. |

Interest in Securities of the Subject Company |

(a) Securities Ownership. The information set forth in the Proxy

Statement under the following captions is incorporated herein by reference:

“SUMMARY TERM SHEET”

“SPECIAL FACTORS - Interests of Executive Officers and Directors of

ARC in the Merger”

“SPECIAL FACTORS – Voting Agreement”

“THE SPECIAL MEETING - Record Date and Quorum”

“OTHER IMPORTANT INFORMATION REGARDING ARC - Security Ownership of

Certain Beneficial Owners and Management”

Annex C – Rollover Agreement

Annex E –Voting Agreement

(b) Securities Transactions. The information set forth in the Proxy

Statement under the following captions is incorporated herein by reference:

“SPECIAL FACTORS - Background of the Merger”

“SPECIAL FACTORS - Interests of Executive Officers and Directors of

ARC in the Merger”

“SPECIAL FACTORS – Voting Agreement”

“THE MERGER AGREEMENT”

“OTHER IMPORTANT INFORMATION REGARDING ARC - Stock Repurchases”

“OTHER IMPORTANT INFORMATION REGARDING ARC - Certain Transactions in

the Shares of ARC

Common Stock”

Annex A – Merger Agreement

Annex C – Rollover Agreement

Annex E –Voting Agreement

| Item 12. |

The Solicitation or Recommendation |

(d) Intent to Tender or Vote in a Going-Private Transaction. The

information set forth in the Proxy Statement under the following captions is incorporated herein by reference:

“SUMMARY TERM SHEET”

“QUESTIONS AND ANSWERS ABOUT THE PROPOSALS AND THE SPECIAL MEETING”

“SPECIAL FACTORS - Background of the Merger”

“SPECIAL FACTORS - Purpose and Reasons of ARC for the Merger;

Recommendations of the ARC Board and the Special Committee; Fairness of the Merger”

“SPECIAL FACTORS - Interests of Executive Officers and Directors of

ARC in the Merger”

“SPECIAL FACTORS - Intent of the Directors and Executive Officers to

Vote in Favor of the Merger”

“SPECIAL FACTORS - Intent of the Purchaser Filing Parties to Vote in

Favor of the Merger”

“SPECIAL FACTORS - Voting Agreement”

“THE SPECIAL MEETING - Record Date and Quorum”

“THE SPECIAL MEETING - Voting Intentions of ARC’s Directors and

Executive Officers”

“OTHER IMPORTANT INFORMATION REGARDING ARC - Directors and Executive

Officers of ARC”

“OTHER IMPORTANT INFORMATION REGARDING ARC - Security Ownership of

Certain Beneficial Owners and Management”

Annex C - Rollover Agreement

Annex F – Voting Agreement

(e) Recommendation of Others. The information set forth in the Proxy

Statement under the following captions is incorporated herein by reference:

“SUMMARY TERM SHEET”

“QUESTIONS AND ANSWERS ABOUT THE PROPOSALS AND THE SPECIAL MEETING”

“SPECIAL FACTORS - Background of the Merger”

“SPECIAL FACTORS - Notice Regarding Ratification Under Section 204

of the Delaware General Corporation Law”

“SPECIAL FACTORS - Purpose and Reasons of ARC for the Merger;

Recommendations of the ARC Board and the Special Committee; Fairness of the Merger”

“SPECIAL FACTORS - Position of the Purchaser Filing Parties as to

the Fairness of the Merger”

“SPECIAL FACTORS - Purpose and Reasons of the Purchaser Filing

Parties for the Merger”

| Item 13. |

Financial Statements |

(a) Financial Information. The audited consolidated financial

statements of the Company for the fiscal years ended December 31, 2023 and 2022 are incorporated herein by reference to the Company’s Annual Report on Form 10-K for the fiscal year ended December 31, 2023, filed on February 29, 2024 (see “Item 8.

Financial Statements and Supplementary Data” beginning on page 35). The unaudited financial statements of the Company for the six months ended June 30, 2024 are incorporated herein by reference to the Company’s Quarterly Report on Form 10-Q for the

fiscal quarter ended June 30, 2024, filed on August 8, 2024 (see “Item 1. Condensed Consolidated Financial Statements” beginning on page 6).

The information set forth in the Proxy Statement under the following

captions is incorporated herein by reference:

“SUMMARY TERM SHEET”

“OTHER IMPORTANT INFORMATION REGARDING ARC - Book

Value per Share”

“OTHER IMPORTANT INFORMATION REGARDING ARC - Selected Historical

Consolidated Financial Data”

“WHERE YOU CAN FIND MORE INFORMATION”

(b) Pro Forma Information. Not Applicable.

| Item 14. |

Persons/Assets, Retained, Employed, Compensated or Used |

(a) Solicitations or Recommendations. The information set forth in

the Proxy Statement under the following captions is incorporated herein by reference:

“SUMMARY TERM SHEET”

“QUESTIONS AND ANSWERS ABOUT THE PROPOSALS AND THE SPECIAL MEETING”

“SPECIAL FACTORS - Background of the Merger”

“SPECIAL FACTORS - Purpose and Reasons of ARC for the Merger;

Recommendations of the ARC Board and the Special Committee; Fairness of the Merger”

“SPECIAL FACTORS - Fees and Expenses”

“THE SPECIAL MEETING - Solicitation of Proxies; Payment of

Solicitation Expenses”

(b) Employees and Corporate Assets. The information set forth in the

Proxy Statement under the following captions is incorporated herein by reference:

“SUMMARY TERM SHEET”

“QUESTIONS AND ANSWERS ABOUT THE PROPOSALS AND THE SPECIAL MEETING”

“SPECIAL FACTORS - Background of the Merger”

“SPECIAL FACTORS - Interests of Executive Officers and Directors of

ARC in the Merger”

“THE SPECIAL MEETING”

“THE SPECIAL MEETING - Solicitation of Proxies; Payment of

Solicitation Expenses”

| Item 15. |

Additional Information |

(b) Golden Parachute Compensation. The information set forth in the

Proxy Statement under the following captions is incorporated herein by reference:

“SUMMARY TERM SHEET”

“SPECIAL FACTORS - Interests of Executive Officers and Directors of

ARC in the Merger”

“Merger-Related Compensation Proposal (The Merger-Related

Compensation Proposal—Proposal 3)”

(c) Other Material Information. The entirety of the Proxy Statement,

including all annexes and appendices thereto, is incorporated herein by reference.

The following exhibits are filed herewith:

| Exhibit No. |

|

Description |

| (a)(2)(i) |

|

Preliminary Proxy Statement of ARC Document Solutions, Inc.

(included in the Schedule 14A filed on September 1 1 , 2024, and incorporated herein by reference) (the “Preliminary Proxy Statement”). |

| (a)(2)(ii) |

|

Form of Proxy Card (included in the Preliminary Proxy

Statement and incorporated herein by reference). |

| (a)(2)(iii) |

|

Letter to Stockholders (included in the Preliminary Proxy

Statement and incorporated herein by reference). |

| (a)(2)(iv) |

|

Notice of Special Meeting of Stockholders (included in the

Preliminary Proxy Statement and incorporated herein by reference). |

| (a)(2)(v) |

|

Current Report on Form 8-K, filed August 28, 2024 (included

in the Preliminary Proxy Statement and incorporated herein by reference). |

(a)(2)(vi)

|

|

Current Report on Form 8-K filed September 11 (included in the Preliminary Proxy Statement and incorporated herein by reference)

|

| (a)(5)(i) |

|

Press Release, dated August 28, 2024 (incorporated by

reference to Exhibit 99.1 of the Company’s Form 8-K (filed August 28, 2024) (File No. 001-32407)). |

| (c)(i) |

|

Opinion of William Blair & Company, L.L.C., dated August

27, 2024 (included as Annex B to the Preliminary Proxy Statement, and incorporated herein by reference). |

| (c)(ii) |

|

Discussion Materials of William Blair & Company, L.L.C.

for the Special Committee, dated June 20, 2024. |

| (c)(iii) |

|

Discussion Materials of William Blair & Company, L.L.C.

for the Special Committee, dated August 27, 2024. |

| (c)(iv) |

|

Discussion Materials of AlixPartners, LLC for the Special

Committee, dated June 20, 2024. |

| (d)(i) |

|

Agreement and Plan of Merger, dated August 27, 2024 by and among

ARC Document Solutions, Inc.

TechPrint Holdings, LLC, TechPrint Merger Sub, Inc. (included as

Annex A to the Preliminary Proxy Statement, and incorporated herein by reference).

|

| (d)(ii) |

|

First Amendment, dated as of September 10, to the Agreement

and Plan of Merger by and among ARC Document Solutions, Inc. TechPrint Holdings, LLC, TechPrint Merger Sub, Inc. (contained within Annex A to the Preliminary Proxy Statement, and incorporated herein by reference). |

| (d)(iii) |

|

Rollover Agreement, dated as of August 27, 2024, by and

among TechPrint Holdings, LLC, Kumarakulasingam Suriyakumar, Dilantha Wijesuriya, Jorge Avalos, Rahul Roy, Sujeewa Sean Pathiratne, Suriyakumar Family Trust, Shiyulli Suriyakumar 2013 Irrevocable Trust, and Seiyonne Suriyakumar 2013 Irrevocable

Trust (included as Annex C to the Preliminary Proxy Statement, and incorporated herein by reference). |

| (d)(iv) |

|

First Amendment to the Rollover Agreement, dated as of

September 10, by and among TechPrint Holdings, LLC, Kumarakulasingam Suriyakumar, Dilantha Wijesuriya, Jorge Avalos, Rahul Roy, Sujeewa Sean Pathiratne, Suriyakumar Family Trust, Shiyulli Suriyakumar 2013 Irrevocable Trust, and Seiyonne

Suriyakumar 2013 Irrevocable Trust (contained within Annex C to the Preliminary Proxy Statement, and incorporated herein by reference). |

| (d)(v) |

|

Equity Commitment Letter, dated August 27, 2024, dated

August 27, 2024, by and among TechPrint Holdings, LLC, Kumarakulasingam Suriyakumar and Sujeewa Sean Pathiratne (included as Annex D to the Preliminary Proxy Statement, and incorporated herein by reference). |

| (d)(vi) |

|

Voting Agreement, dated as of August 27, 2024, by and among

TechPrint Holdings, LLC, Kumarakulasingam Suriyakumar, Dilantha Wijesuriya, Jorge Avalos, Rahul Roy, Sujeewa Sean Pathiratne, Suriyakumar Family Trust, Shiyulli Suriyakumar 2013 Irrevocable Trust, and Seiyonne Suriyakumar 2013 Irrevocable Trust

(included as Annex E to the Preliminary Proxy Statement, and incorporated herein by reference). |

| (d)(vii) |

|

First Amendment to the Voting Agreement, dated as of September 10, by and among

TechPrint Holdings, LLC, Kumarakulasingam Suriyakumar, Dilantha Wijesuriya, Jorge Avalos, Rahul Roy, Sujeewa Sean Pathiratne, Suriyakumar Family Trust, Shiyulli Suriyakumar 2013 Irrevocable Trust, and Seiyonne Suriyakumar 2013 Irrevocable Trust

(contained within Annex E to the Preliminary Proxy Statement, and incorporated herein by reference). |

| (d)(viii) |

|

Limited Guarantee, dated as of August 27, 2024, by and

between ARC Document Solutions, Inc. and Kumarakulasingam Suriyakumar (included as Annex F to the Preliminary Proxy Statement, and incorporated herein by reference). |

| (f) |

|

Section 262 of the DGCL (included as Annex G to the

Definitive Proxy Statement, and incorporated herein by reference). |

| (g) |

|

Not Applicable. |

| 107 |

|

Filing Fee Table. |

* Previously Filed.

SIGNATURES

After due inquiry and to the best of my knowledge and belief, I certify

that the information set forth in this statement is true, complete and correct.

Date: September 1 1 , 2024

| |

ARC DOCUMENT SOLUTIONS, INC. |

| |

|

|

|

| |

By: |

/s/ Tracey Luttrell |

| |

|

Name: |

Tracey Luttrell |

| |

|

Title: |

Corporate Counsel & Corporate Secretary |

After due inquiry and to the best of my knowledge and belief, I certify

that the information set forth in this statement is true, complete and correct.

Date: September 1 1 , 2024

| |

TECHPRINT HOLDINGS, LLC |

| |

|

|

|

| |

By: |

/s/ Kumarakulasingam Suriyakumar |

| |

|

Name: |

Kumarakulasingam Suriyakumar |

| |

|

Title: |

Manager |

| |

|

|

|

| |

TECHPRINT MERGER SUB, INC. |

| |

|

|

|

| |

By: |

/s/ Kumarakulasingam Suriyakumar |

| |

|

Name: |

Kumarakulasingam Suriyakumar |

| |

|

Title: |

President |

After due inquiry and to the best of my knowledge and belief, I certify

that the information set forth in this statement is true, complete and correct.

Date: September 1 1 , 2024

| |

By: |

/s/ Kumarakulasingam Suriyakumar |

| |

|

Name: |

Kumarakulasingam Suriyakumar |

| |

|

|

|

After due inquiry and to the best of my knowledge and belief, I certify

that the information set forth in this statement is true, complete and correct.

Date: September 1 1 , 2024

| |

By: |

/s/ Dilantha Wijesuriya |

| |

|

Name: |

Dilantha Wijesuriya |

| |

|

|

|

After due inquiry and to the best of my knowledge and belief, I certify

that the information set forth in this statement is true, complete and correct.

Date: September 1 1 , 2024

| |

By: |

/s/ Jorge Avalos |

| |

|

Name: |

Jorge Avalos |

After due inquiry and to the best of my knowledge and belief, I certify

that the information set forth in this statement is true, complete and correct.

Date: September 1 1 , 2024

| |

By: |

/s/ Rahul Roy |

| |

|

Name: |

Rahul Roy |

After due inquiry and to the best of my knowledge and belief, I certify

that the information set forth in this statement is true, complete and correct.

Date: September 1 1 , 2024

| |

By: |

/s/ Sujeewa Sean Pathiratne |

| |

|

Name: |

Sujeewa Sean Pathiratne |

After due inquiry and to the best of my knowledge and belief, I certify

that the information set forth in this statement is true, complete and correct.

Date: September 1 1 , 2024

| |

SURIYAKUMAR FAMILY TRUST |

| |

|

|

|

| |

By: |

/s/ Kumarakulasingam Suriyakumar |

| |

|

Name: |

Kumarakulasingam Suriyakumar |

| |

|

Title: |

Trustee |

After due inquiry and to the best of my knowledge and belief, I certify

that the information set forth in this statement is true, complete and correct.

Date: September 1 1 , 2024

| |

SHIYULLI SURIYAKUMAR 2013 IRREVOCABLE TRUST |

| |

|

|

|

| |

By: |

/s/ Shiyulli Suriyakumar |

| |

|

Name: |

Shiyulli Suriyakumar |

| |

|

Title: |

Trustee |

After due inquiry and to the best of my knowledge and belief, I certify

that the information set forth in this statement is true, complete and correct.

Date: September 1 1 , 2024

| |

SEIYONNE SURIYAKUMAR 2013 IRREVOCABLE TRUST |

| |

|

|

|

| |

By: |

/s/ Seiyonne Suriyakumar |

| |

|

Name: |

Seiyonne Suriyakumar |

| |

|

Title: |

Trustee |

Exhibit

(c)(ii)

CONFIDENTIAL

Discussion

Materials for the Special

Committee

of the Board of Directors

Project

ARIAL

June

20, 2024

William

Blair

CONFIDENTIAL

This

presentation (together with any accompanying oral presentation and any supplementary documents provided therewith, the “Presentation”)

has been prepared by

William

Blair & Company, L.L.C. (“William Blair”) exclusively for the benefit and internal use of the Special Committee

of the Board of Directors of ARIAL (the “Company” or

“ARIAL”).

The accompanying material was compiled or prepared on a confidential basis solely for use by the Special Committee of the Board

of Directors and not with a view

toward

public disclosure, and may not be disclosed, summarized, reproduced, disseminated or quoted, or otherwise referred to in whole

or in part, without the prior written

consent

of William Blair & Company, L.L.C. (“William Blair” or “Blair”). No party may rely on this Presentation

without William Blair’s prior written consent. William Blair

and

its affiliates, partners, directors, employees and agents do not accept responsibility or liability for this Presentation or its

contents (except to the extent that such liability

cannot

be excluded by law).

This

Presentation is for discussion purposes only and speaks only as of the date it is given, and the views expressed are subject to

change based on a number of factors,

including

market conditions and the Recipient’s business and prospects. The information utilized in preparing this presentation was

obtained from the Company, the Speical

Committee

of the Board of Directors, its advisors and public sources. William Blair assumes no responsibility for independent investigation

or verification of any such

information

and has relied on such information being complete and accurate in all respects. Any estimates and projections regarding the Company

contained herein have

been

prepared by senior management of ARIAL and approved for our use by the Special Committee of the Board of Directors, or are publicly

available or based upon such

estimates

and projections and involve numerous and significant subjective determinations, which may or may not prove to be correct, and

William Blair expresses no opinion

with

respect to such estimates, projections and determinations. In addition, any analyses relating to the value of assets, businesses

or securities do not purport to be

appraisals

or to reflect prices at which they may be sold. In furnishing this Presentation, William Blair undertakes no obligation to provide

additional information or to

correct

or update any of the Information.

William

Blair, together with its affiliates and partners, is a financial services institution engaged in a wide range of investment banking

and other activities (including, but

not

limited to, investment management, corporate finance, private wealth management, securities trading, research and brokerage activities).

It is understood and agreed

that

William Blair may, from time to time, make a market in, have a long or short position, buy and sell or otherwise effect transactions

for customer accounts and for their

own

accounts in the securities of, or may perform or be solicited to perform investment banking, corporate finance or other services

for, the Recipient and other third-party

entities

which are or may be the subject of the transactions contemplated by this Presentation. William Blair has adopted policies and

procedures designed to ensure the

independence

of its research analysts, whose views may differ from those of William Blair’s investment banking department and who may

produce research reports and

other

materials the timing or content of which conflict with the views of the investment banking department or the Recipient’s

interests, in connection with the transactions

contemplated

by this Presentation or otherwise.

Nothing

in the Presentation is, or shall be relied upon as, investment advice or any recommendation by William Blair. This Presentation

does not purport to contain all of the

information

that may be necessary or appropriate to evaluate the proposed transaction, and the Recipient should conduct its own independent

assessment and such

investigations

as it deems necessary. Recipient should rely on its own counsel, accountants and other similar expert advisors for legal, regulatory,

accounting, tax and other

similar

advice. Nothing in the Presentation or any related discussions is intended to create, or shall be construed as creating, a principal-agent,

advisor-client or fiduciary

relationship

between William Blair and the Recipient.

Disclosure

1

William

Blair

CONFIDENTIAL

Table

of Contents

Executive

Summary

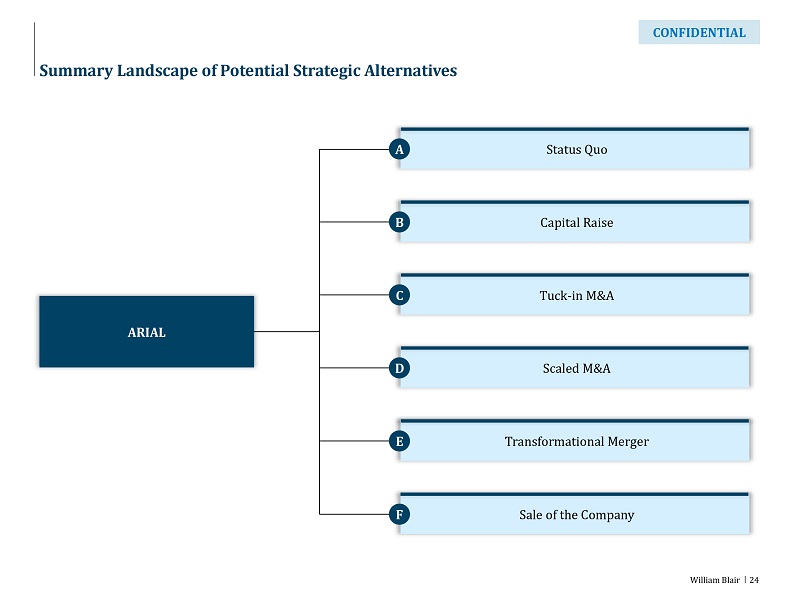

ARIAL

Situation Update

Selected

Valuation Perspectives

Potential

Strategic Alternatives

Appendix

1

2

3

4

5

William

Blair

CONFIDENTIAL

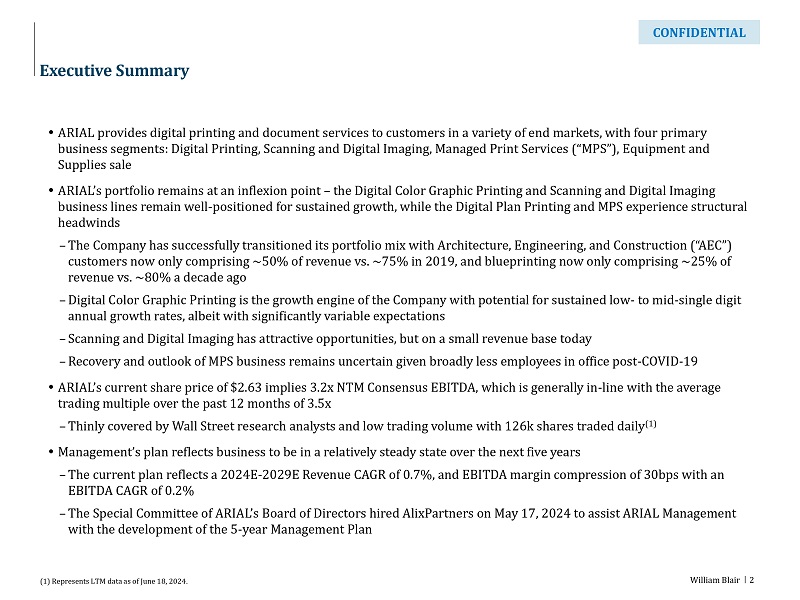

Executive

Summary

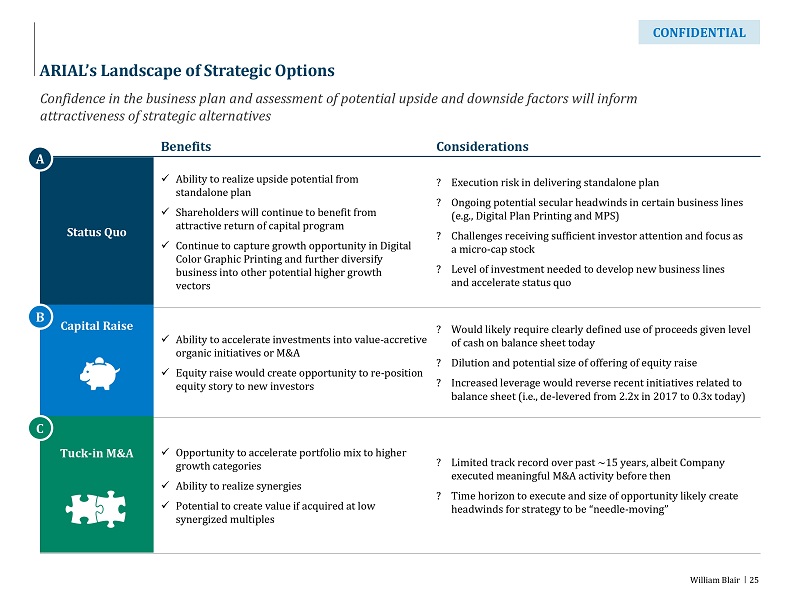

●

ARIAL provides digital printing and document services to customers in a variety of end markets, with four primary

business

segments: Digital Printing, Scanning and Digital Imaging, Managed Print Services (“MPS”), Equipment and

Supplies

sale

●

ARIAL’s portfolio remains at an inflexion point – the Digital Color Graphic Printing and Scanning and Digital Imaging

business

lines remain well-positioned for sustained growth, while the Digital Plan Printing and MPS experience structural

headwinds

–

The Company has successfully transitioned its portfolio mix with Architecture, Engineering, and Construction (“AEC”)

customers

now only comprising ~50% of revenue vs. ~75% in 2019, and blueprinting now only comprising ~25% of

revenue

vs. ~80% a decade ago

–

Digital Color Graphic Printing is the growth engine of the Company with potential for sustained low- to mid-single digit

annual

growth rates, albeit with significantly variable expectations

–

Scanning and Digital Imaging has attractive opportunities, but on a small revenue base today

–

Recovery and outlook of MPS business remains uncertain given broadly less employees in office post-COVID-19

●

ARIAL’s current share price of $2.63 implies 3.2x NTM Consensus EBITDA, which is generally in-line with the average

trading

multiple over the past 12 months of 3.5x

–

Thinly covered by Wall Street research analysts and low trading volume with 126k shares traded daily(1)

●

Management’s plan reflects business to be in a relatively steady state over the next five years

–

The current plan reflects a 2024E-2029E Revenue CAGR of 0.7%, and EBITDA margin compression of 30bps with an

EBITDA

CAGR of 0.2%

–

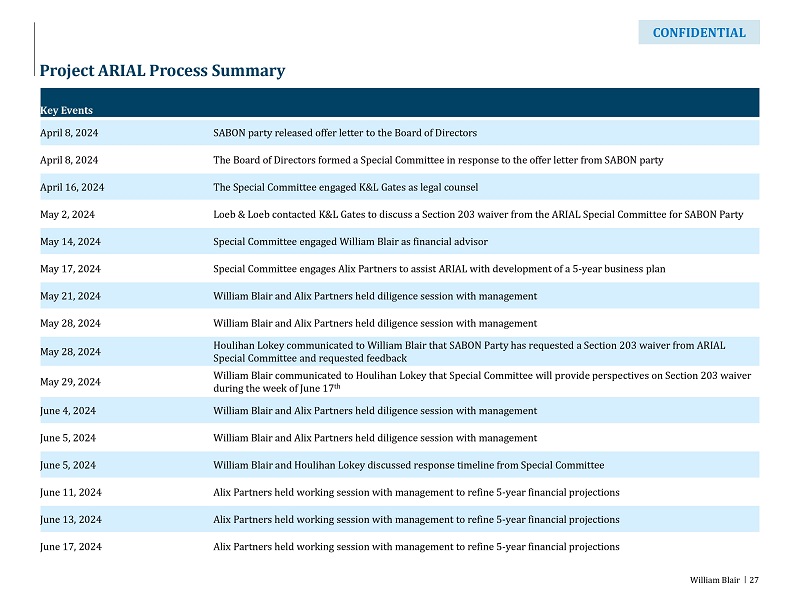

The Special Committee of ARIAL’s Board of Directors hired AlixPartners on May 17, 2024 to assist ARIAL Management

with

the development of the 5-year Management Plan

(1)

Represents LTM data as of June 18, 2024. 2

William

Blair

CONFIDENTIAL

Executive

Summary (cont’d)

●

On April 8, 2024, Kumarakulasingam Suriyakumar (“Suri”) submitted a proposal to ARIAL’s Board of Directors for

$3.25

per

share in cash

–

Included in the proposal was a highly confident letter from U.S. Bank as the lead left arranger or sole bookrunner for the

financing

–

Purchase price implies a 23.6% premium to ARIAL’s current share price and a transaction multiple of 4.1x LTM

EBITDA(1)

and 4.3x 2024E EBITDA(2)

●

A Special Committee to evaluate Suri’s proposal was formed on April 8, 2024, and William Blair was retained as financial

advisor

to the Special Committee on May 14, 2024

–

The Special Committee has asked William Blair to provide its perspectives on ARIAL in the context of the current

strategic,

trading, and transaction environment

–

William Blair has considered a variety of potential strategic alternatives for ARIAL, ranging from status quo to more

transformational

options including a sale of the Company

(1)

LTM as of March 31, 2024.

(2)

Reflects ARIAL management projections as of June 19, 2024. 3

ARIAL

Situation Update

William

Blair

CONFIDENTIAL

Summary

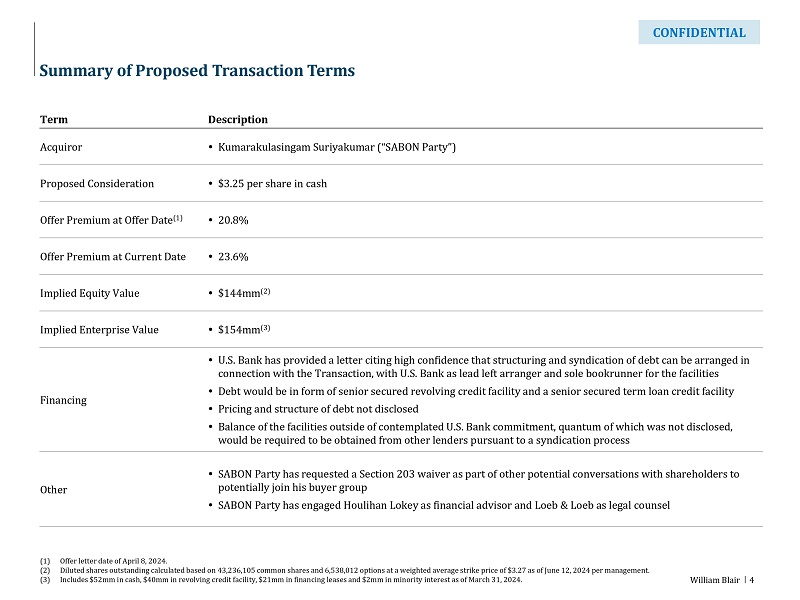

of Proposed Transaction Terms

Term

Description

Acquiror

● Kumarakulasingam Suriyakumar (“SABON Party”)

Proposed

Consideration ● $3.25 per share in cash

Offer

Premium at Offer Date(1) ● 20.8%

Offer

Premium at Current Date ● 23.6%

Implied

Equity Value ● $144mm(2)

Implied

Enterprise Value ● $154mm(3)

Financing

●

U.S. Bank has provided a letter citing high confidence that structuring and syndication of debt can be arranged in

connection

with the Transaction, with U.S. Bank as lead left arranger and sole bookrunner for the facilities

●

Debt would be in form of senior secured revolving credit facility and a senior secured term loan credit facility

●

Pricing and structure of debt not disclosed

●

Balance of the facilities outside of contemplated U.S. Bank commitment, quantum of which was not disclosed,

would

be required to be obtained from other lenders pursuant to a syndication process

Other

●

SABON Party has requested a Section 203 waiver as part of other potential conversations with shareholders to

potentially

join his buyer group

●

SABON Party has engaged Houlihan Lokey as financial advisor and Loeb & Loeb as legal counsel

(1)

Offer letter date of April 8, 2024.

(2)

Diluted shares outstanding calculated based on 43,236,105 common shares and 6,538,012 options at a weighted average strike price

of $3.27 as of June 12, 2024 per management.

(3)

Includes $52mm in cash, $40mm in revolving credit facility, $21mm in financing leases and $2mm in minority interest as of March

31, 2024. 4

William

Blair

CONFIDENTIAL

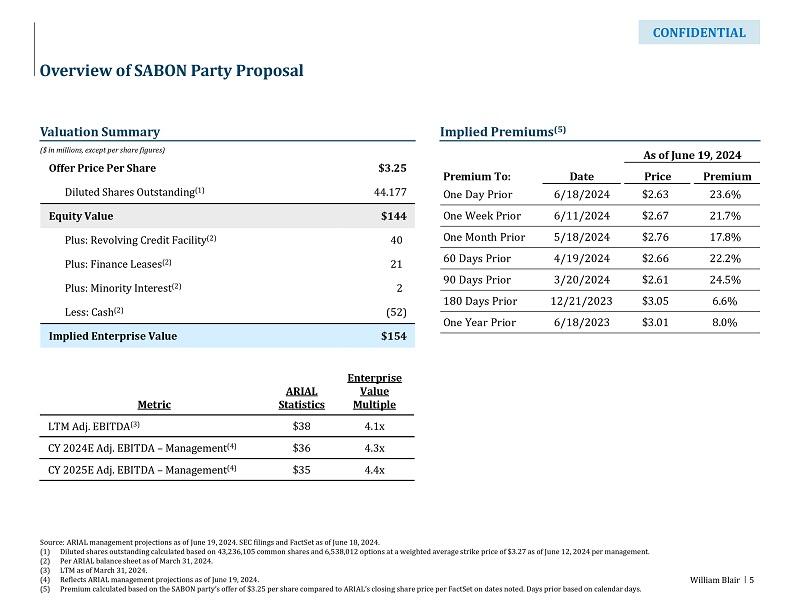

Overview

of SABON Party Proposal

Valuation

Summary

($

in millions, except per share figures)

Implied

Premiums(5)

Offer

Price Per Share $3.25

Diluted

Shares Outstanding(1) 44.177

Equity

Value $144

Plus:

Revolving Credit Facility(2) (40)

Plus:

Finance Leases(2) (21)

Plus:

Minority Interest(2) 2)

Less:

Cash(2) (52)

Implied

Enterprise Value $154

Metric

ARIAL

Statistics

Enterprise

Value

Multiple

LTM

Adj. EBITDA(3) $38 4.1x

CY

2024E Adj. EBITDA – Management(4) $36 4.3x

CY

2025E Adj. EBITDA – Management(4) $35 4.4x

As

of June 19, 2024

Premium

To: Date Price Premium

One

Day Prior 6/18/2024 $2.63 23.6%

One

Week Prior 6/11/2024 $2.67 21.7%

One

Month Prior 5/18/2024 $2.76 17.8%

60

Days Prior 4/19/2024 $2.66 22.2%

90

Days Prior 3/20/2024 $2.61 24.5%

180

Days Prior 12/21/2023 $3.05 6.6%

One

Year Prior 6/18/2023 $3.01 8.0%

Source:

ARIAL management projections as of June 19, 2024. SEC filings and FactSet as of June 18, 2024.

(1)

Diluted shares outstanding calculated based on 43,236,105 common shares and 6,538,012 options at a weighted average strike price

of $3.27 as of June 12, 2024 per management.

(2)

Per ARIAL balance sheet as of March 31, 2024.

(3)

LTM as of March 31, 2024.

(4)

Reflects ARIAL management projections as of June 19, 2024.

(5)

Premium calculated based on the SABON party’s offer of $3.25 per share compared to ARIAL’s closing share price per

FactSet on dates noted. Days prior based on calendar days.

5

William

Blair

CONFIDENTIAL

Sources:

Capital IQ, FactSet and SEC filings as of June 18, 2024.

(1)

Represents the SABON party’s April 8, 2024 inbound offer.

(2)

Diluted shares outstanding calculated based on 43,236,105 common shares and 6,538,012 options at a weighted average strike price

of $3.27 as of June 12, 2024 per management.

(3)

Net debt includes $40M of revolver, $21M of finance leases, $2M of minority interest, and $52M of cash and cash equivalents as

of March 31, 2024.

(4)

Trading information based on calendar days.

(5)

LTM as of March 31, 2024.

(6)

Reflects ARIAL management projections as of June 19, 2024.

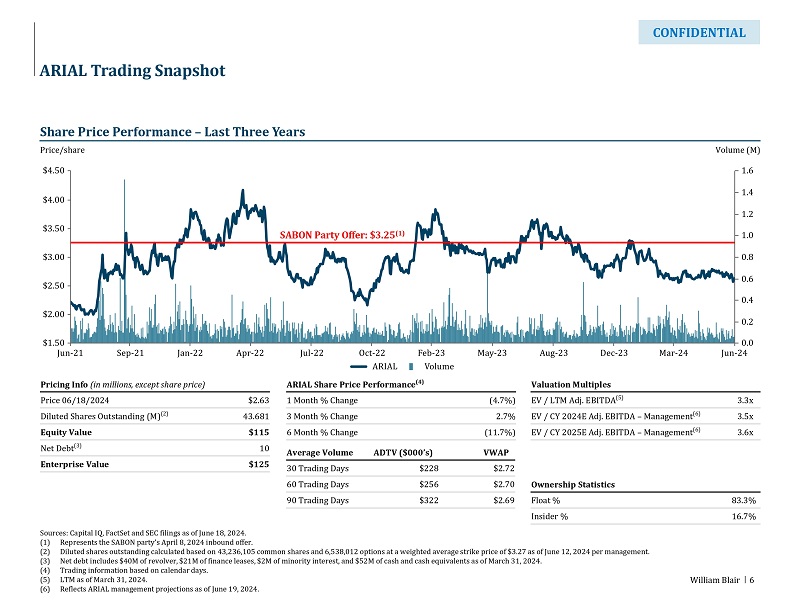

ARIAL

Trading Snapshot

Share

Price Performance – Last Three Years

Price/share

Volume (M)

Pricing

Info (in millions, except share price)

Price

06/18/2024 $2.63

Diluted

Shares Outstanding (M)(2) 43.681

Equity

Value $115

Net

Debt(3) 10

Enterprise

Value $125

ARIAL

Share Price Performance(4)

1

Month % Change (4.7%)

3

Month % Change 2.7%

6

Month % Change (11.7%)

Valuation

Multiples

EV

/ LTM Adj. EBITDA(5) 3.3x

EV

/ CY 2024E Adj. EBITDA – Management(6) 3.5x

EV

/ CY 2025E Adj. EBITDA – Management(6) 3.6x

Ownership

Statistics

Float

% 83.3%

Insider

% 16.7%

Average

Volume ADTV ($000’s) VWAP

30

Trading Days $228 $2.72

60

Trading Days $256 $2.70

90

Trading Days $322 $2.69

SABON

Party Offer: $3.25(1)

6

William

Blair

CONFIDENTIAL

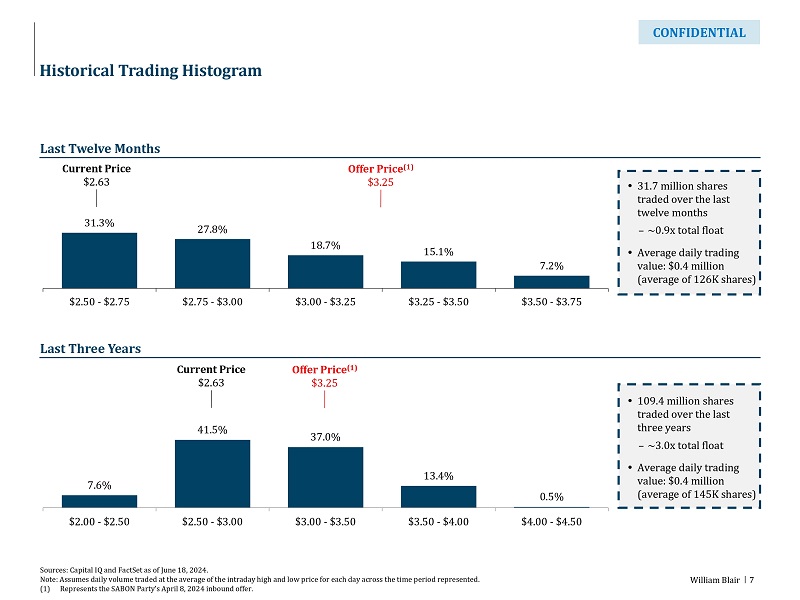

Historical

Trading Histogram

Last

Twelve Months

Last

Three Years

●

31.7 million shares

traded

over the last

twelve

months

–

~0.9x total float

●

Average daily trading

value:

$0.4 million

(average

of 126K shares)

●

109.4 million shares

traded

over the last

three

years

–

~3.0x total float

●

Average daily trading

value:

$0.4 million

(average

of 145K shares)

Current

Price

$2.63

Sources:

Capital IQ and FactSet as of June 18, 2024.

Note:

Assumes daily volume traded at the average of the intraday high and low price for each day across the time period represented.

(1)

Represents the SABON Party’s April 8, 2024 inbound offer.

Offer

Price(1)

$3.25

Offer

Price(1)

$3.25

Current

Price

$2.63

31.3%

27.8%

18.7%

15.1%

7.2%

$2.50

- $2.75 $2.75 - $3.00 $3.00 - $3.25 $3.25 - $3.50 $3.50 - $3.75

7.6%

41.5%

37.0%

13.4%

0.5%

$2.00

- $2.50 $2.50 - $3.00 $3.00 - $3.50 $3.50 - $4.00 $4.00 - $4.50

7

William

Blair

CONFIDENTIAL

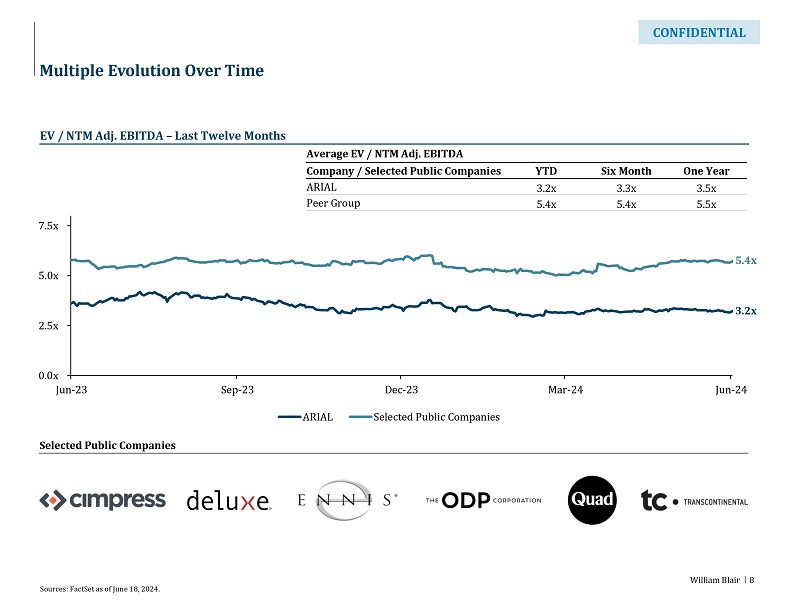

Average

EV / NTM Adj. EBITDA

Company

/ Selected Public Companies YTD Six Month One Year

ARIAL

3.2x 3.3x 3.5x

Peer

Group 5.4x 5.4x 5.5x

Sources:

FactSet as of June 18, 2024.

Multiple

Evolution Over Time

Selected

Public Companies

EV

/ NTM Adj. EBITDA – Last Twelve Months

5.4x

3.2x

0.0x

2.5x

5.0x

7.5x

Jun-23

Sep-23 Dec-23 Mar-24 Jun-24

ARIAL

Selected Public Companies

8

William

Blair

CONFIDENTIAL

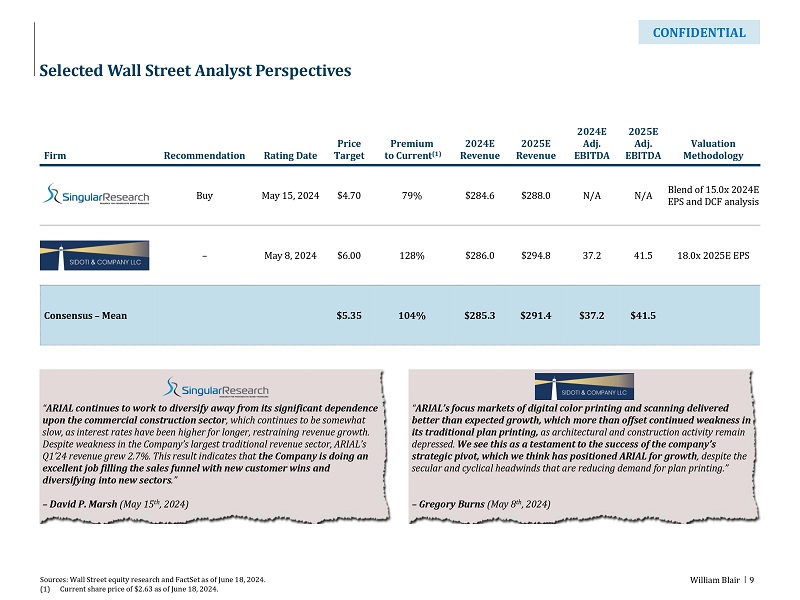

Firm

Recommendation Rating Date

Price

Target

Premium

to

Current(1)

2024E

Revenue

2025E

Revenue

2024E

Adj.

EBITDA

2025E

Adj.

EBITDA

Valuation

Methodology

Buy

May 15, 2024 $4.70 79% $284.6 $288.0 N/A N/A

Blend

of 15.0x 2024E

EPS

and DCF analysis

–

May 8, 2024 $6.00 128% $286.0 $294.8 37.2 41.5 18.0x 2025E EPS

Consensus

– Mean $5.35 104% $285.3 $291.4 $37.2 $41.5

Selected

Wall Street Analyst Perspectives

Sources:

Wall Street equity research and FactSet as of June 18, 2024.

(1)

Current share price of $2.63 as of June 18, 2024.

“ARIAL’s

focus markets of digital color printing and scanning delivered

better

than expected growth, which more than offset continued weakness in

its

traditional plan printing, as architectural and construction activity remain

depressed.

We see this as a testament to the success of the company’s

strategic

pivot, which we think has positioned ARIAL for growth, despite the

secular

and cyclical headwinds that are reducing demand for plan printing.”

–

Gregory Burns (May 8th, 2024)

“ARIAL

continues to work to diversify away from its significant dependence

upon

the commercial construction sector, which continues to be somewhat

slow,

as interest rates have been higher for longer, restraining revenue growth.

Despite

weakness in the Company’s largest traditional revenue sector, ARIAL’s

Q1’24

revenue grew 2.7%. This result indicates that the Company is doing an

excellent

job filling the sales funnel with new customer wins and

diversifying

into new sectors.”

–

David P. Marsh (May 15th, 2024)

9

William

Blair

CONFIDENTIAL

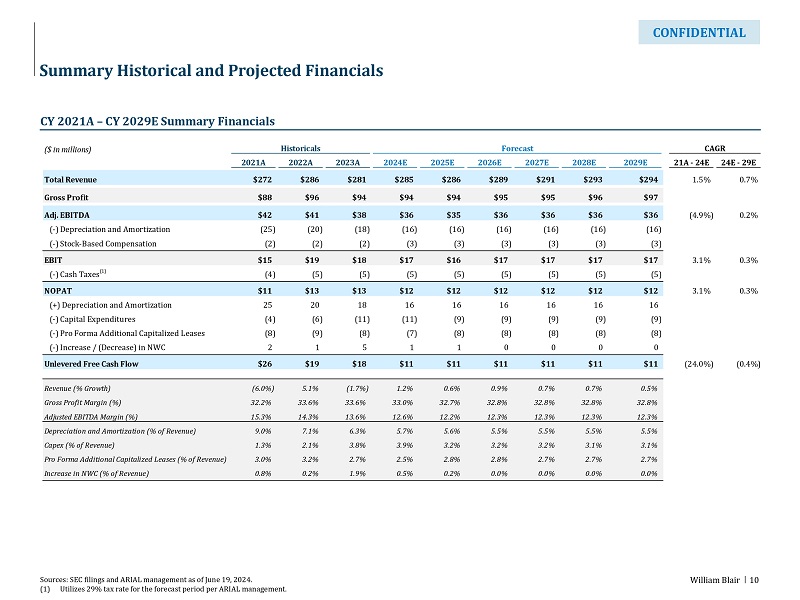

Summary

Historical and Projected Financials

CY

2021A – CY 2029E Summary Financials

Sources:

SEC filings and ARIAL management as of June 19, 2024.

(1)

Utilizes 29% tax rate for the forecast period per ARIAL management.

($

in millions) Historicals Forecast CAGR

2021A

2022A 2023A 2024E 2025E 2026E 2027E 2028E 2029E 21A - 24E 24E - 29E

Total

Revenue $272 $286 $281 $285 $286 $289 $291 $293 $294 1.5% 0.7%

Gross

Profit $88 $96 $94 $94 $94 $95 $95 $96 $97

Adj.

EBITDA $42 $41 $38 $36 $35 $36 $36 $36 $36 (4.9%) 0.2%

(-)

Depreciation and Amortization (25) (20) (18) (16) (16) (16) (16) (16) (16)

(-)

Stock-Based Compensation (2) (2) (2) (3) (3) (3) (3) (3) (3)

EBIT

$15 $19 $18 $17 $16 $17 $17 $17 $17 3.1% 0.3%

(-)

Cash Taxes(1) (4) (5) (5) (5) (5) (5) (5) (5) (5)

NOPAT

$11 $13 $13 $12 $12 $12 $12 $12 $12 3.1% 0.3%

(+)

Depreciation and Amortization 25 20 18 16 16 16 16 16 16

(-)

Capital Expenditures (4) (6) (11) (11) (9) (9) (9) (9) (9)

(-)

Pro Forma Additional Capitalized Leases (8) (9) (8) (7) (8) (8) (8) (8) (8)

(-)

Increase / (Decrease) in NWC 2 1 5 1 1 0 0 0 0

Unlevered

Free Cash Flow $26 $19 $18 $11 $11 $11 $11 $11 $11 (24.0%) (0.4%)

Revenue

(% Growth) (6.0%) 5.1% (1.7%) 1.2% 0.6% 0.9% 0.7% 0.7% 0.5%

Gross

Profit Margin (%) 32.2% 33.6% 33.6% 33.0% 32.7% 32.8% 32.8% 32.8% 32.8%

Adjusted

EBITDA Margin (%) 15.3% 14.3% 13.6% 12.6% 12.2% 12.3% 12.3% 12.3% 12.3%

Depreciation

and Amortization (% of Revenue) 9.0% 7.1% 6.3% 5.7% 5.6% 5.5% 5.5% 5.5% 5.5%

Capex

(% of Revenue) 1.3% 2.1% 3.8% 3.9% 3.2% 3.2% 3.2% 3.1% 3.1%

Pro

Forma Additional Capitalized Leases (% of Revenue) 3.0% 3.2% 2.7% 2.5% 2.8% 2.8% 2.7% 2.7% 2.7%

Increase

in NWC (% of Revenue) 0.8% 0.2% 1.9% 0.5% 0.2% 0.0% 0.0% 0.0% 0.0%

10

William

Blair

CONFIDENTIAL

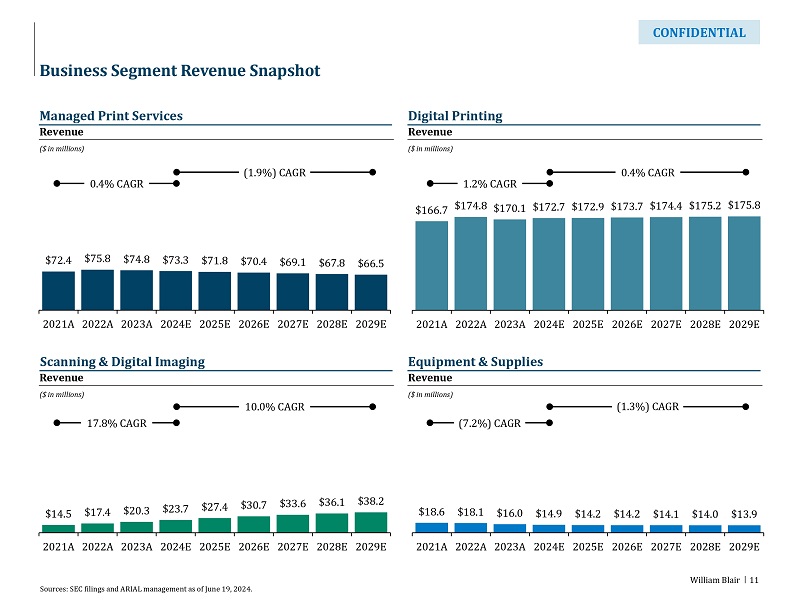

Digital

Printing

Revenue

($

in millions)

Business

Segment Revenue Snapshot

Managed

Print Services

Scanning

& Digital Imaging Equipment & Supplies

Revenue

($

in millions)

Revenue

($

in millions)

Revenue

($

in millions)

17.8%

CAGR

10.0%

CAGR

0.4%

CAGR

(1.9%)

CAGR

1.2%

CAGR

0.4%

CAGR

(7.2%)

CAGR

(1.3%)

CAGR

Sources:

SEC filings and ARIAL management as of June 19, 2024.

$72.4

$75.8 $74.8 $73.3 $71.8 $70.4 $69.1 $67.8 $66.5

2021A

2022A 2023A 2024E 2025E 2026E 2027E 2028E 2029E

$14.5

$17.4 $20.3 $23.7 $27.4 $30.7 $33.6 $36.1 $38.2

2021A

2022A 2023A 2024E 2025E 2026E 2027E 2028E 2029E

$18.6

$18.1 $16.0 $14.9 $14.2 $14.2 $14.1 $14.0 $13.9

2021A

2022A 2023A 2024E 2025E 2026E 2027E 2028E 2029E

$166.7

$174.8 $170.1 $172.7 $172.9 $173.7 $174.4 $175.2 $175.8

2021A

2022A 2023A 2024E 2025E 2026E 2027E 2028E 2029E

11

Selected

Valuation Perspectives

William

Blair

CONFIDENTIAL

Summary

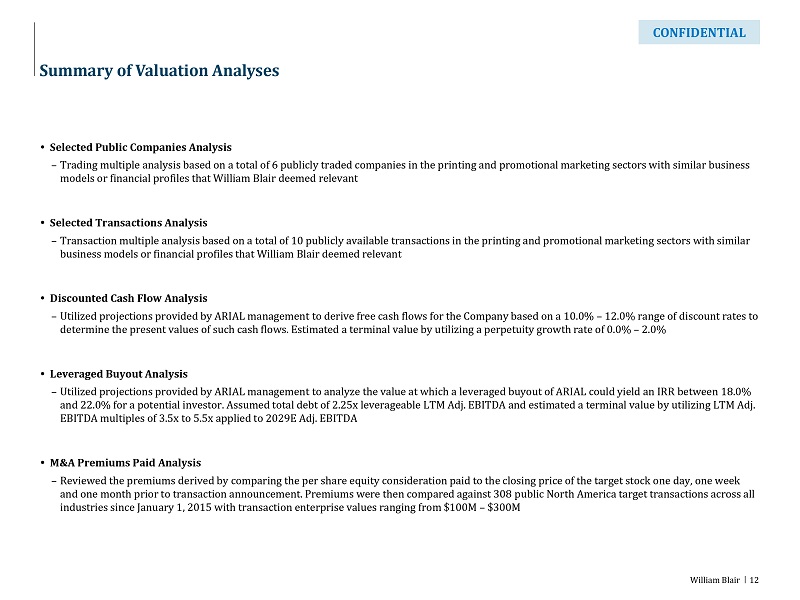

of Valuation Analyses

●

Selected Public Companies Analysis

–

Trading multiple analysis based on a total of 6 publicly traded companies in the printing and promotional marketing sectors with

similar business

models

or financial profiles that William Blair deemed relevant

●

Selected Transactions Analysis

–

Transaction multiple analysis based on a total of 10 publicly available transactions in the printing and promotional marketing

sectors with similar

business

models or financial profiles that William Blair deemed relevant

●

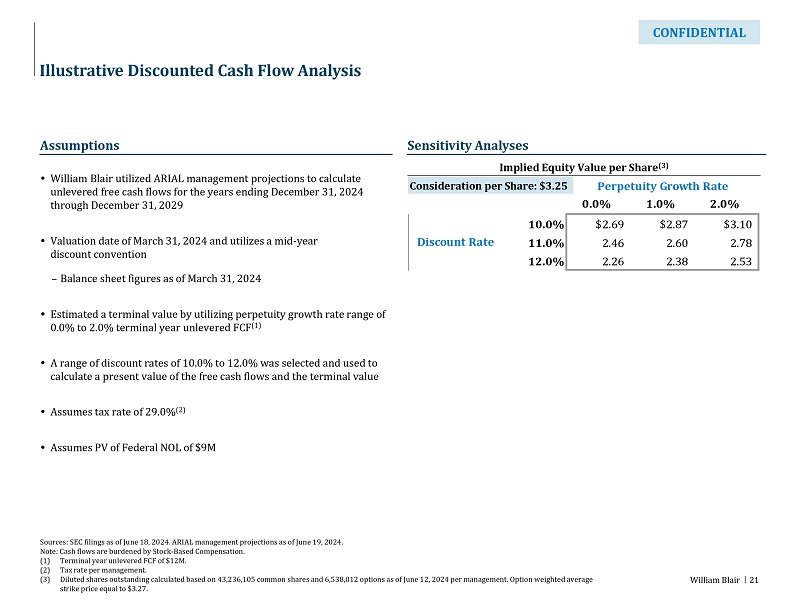

Discounted Cash Flow Analysis

–

Utilized projections provided by ARIAL management to derive free cash flows for the Company based on a 10.0% – 12.0% range

of discount rates to

determine

the present values of such cash flows. Estimated a terminal value by utilizing a perpetuity growth rate of 0.0% – 2.0%

●

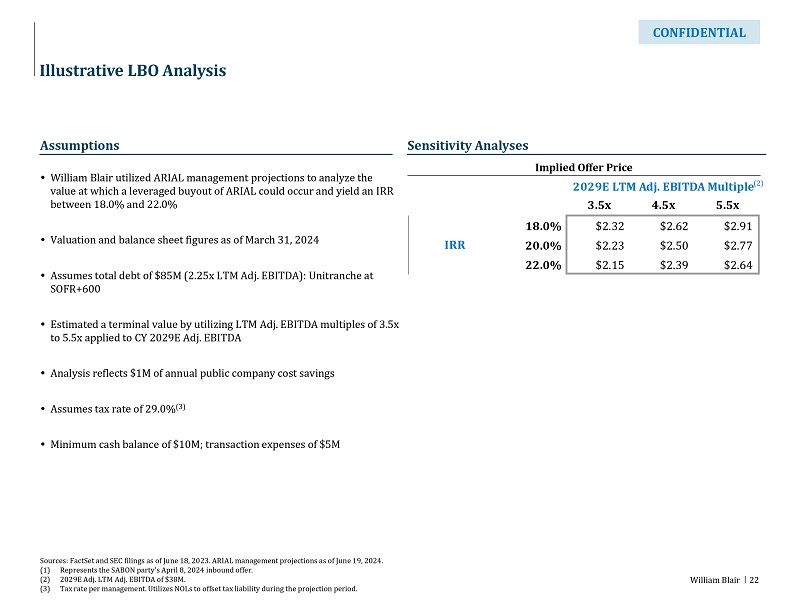

Leveraged Buyout Analysis

–

Utilized projections provided by ARIAL management to analyze the value at which a leveraged buyout of ARIAL could yield an IRR

between 18.0%

and

22.0% for a potential investor. Assumed total debt of 2.25x leverageable LTM Adj. EBITDA and estimated a terminal value by utilizing

LTM Adj.

EBITDA

multiples of 3.5x to 5.5x applied to 2029E Adj. EBITDA

●

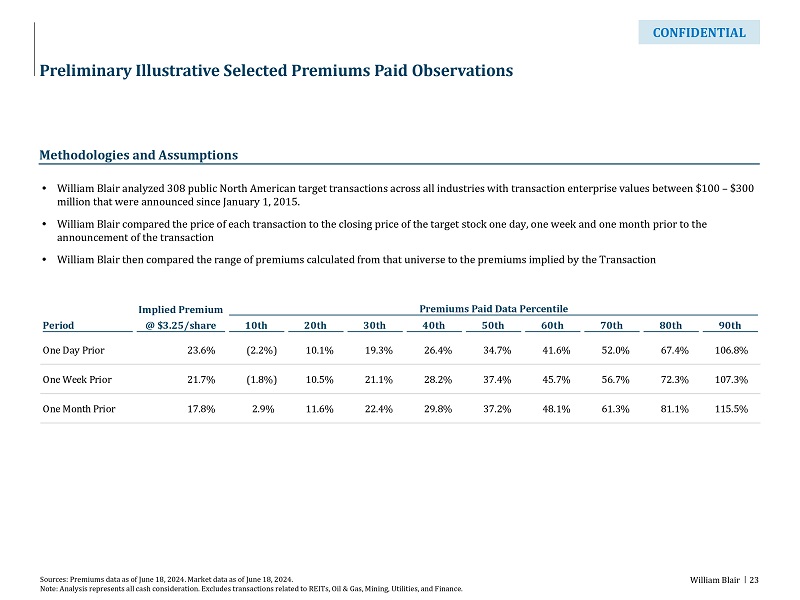

M&A Premiums Paid Analysis

–

Reviewed the premiums derived by comparing the per share equity consideration paid to the closing price of the target stock one

day, one week

and

one month prior to transaction announcement. Premiums were then compared against 308 public North America target transactions

across all

industries

since January 1, 2015 with transaction enterprise values ranging from $100M – $300M

12

William

Blair

CONFIDENTIAL

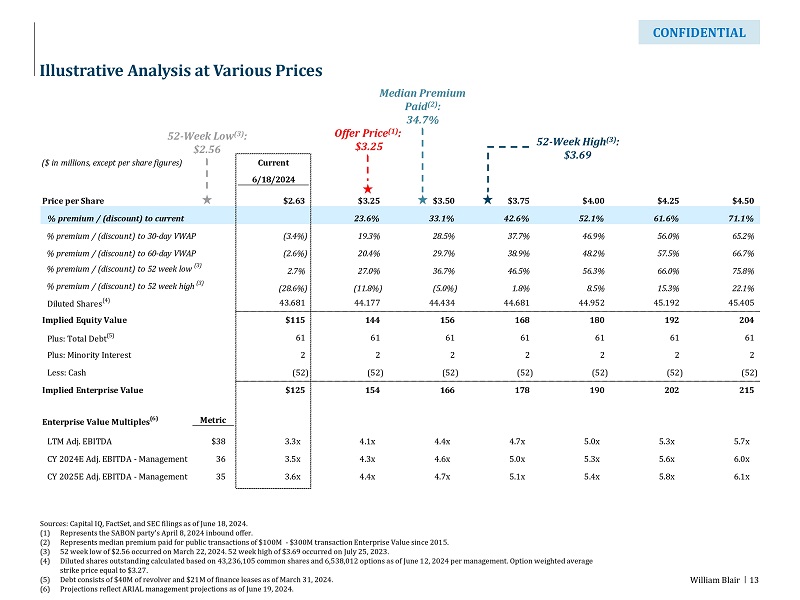

Sources:

Capital IQ, FactSet, and SEC filings as of June 18, 2024.

(1)

Represents the SABON party’s April 8, 2024 inbound offer.

(2)

Represents median premium paid for public transactions of $100M - $300M transaction Enterprise Value since 2015.

(3)

52 week low of $2.56 occurred on March 22, 2024. 52 week high of $3.69 occurred on July 25, 2023.

(4)

Diluted shares outstanding calculated based on 43,236,105 common shares and 6,538,012 options as of June 12, 2024 per management.

Option weighted average

strike

price equal to $3.27.

(5)

Debt consists of $40M of revolver and $21M of finance leases as of March 31, 2024.

(6)

Projections reflect ARIAL management projections as of June 19, 2024.

Illustrative

Analysis at Various Prices

52-Week

Low(3):

$2.56

52-Week

High(3):

$3.69

Offer

Price(1):

$3.25

Median

Premium

Paid(2):

34.7%

($

in millions, except per share figures) Current

6/18/2024

Price

per Share $2.63 $3.25 $3.50 $3.75 $4.00 $4.25 $4.50

%

premium / (discount) to current 23.6% 33.1% 42.6% 52.1% 61.6% 71.1%

%

premium / (discount) to 30-day VWAP (3.4%) 19.3% 28.5% 37.7% 46.9% 56.0% 65.2%

%

premium / (discount) to 60-day VWAP (2.6%) 20.4% 29.7% 38.9% 48.2% 57.5% 66.7%

%

premium / (discount) to 52 week low (3)

2.7%

27.0% 36.7% 46.5% 56.3% 66.0% 75.8%

%

premium / (discount) to 52 week high (3)

(28.6%)

(11.8%) (5.0%) 1.8% 8.5% 15.3% 22.1%

Diluted

Shares(4) 43.681 44.177 44.434 44.681 44.952 45.192 45.405

Implied

Equity Value $115 144 156 168 180 192 204

Plus:

Total Debt(5) 61 61 61 61 61 61 61

Plus:

Minority Interest 2 2 2 2 2 2 2

Less:

Cash (52) (52) (52) (52) (52) (52) (52)

Implied

Enterprise Value $125 154 166 178 190 202 215

Enterprise

Value Multiples(6) Metric

LTM

Adj. EBITDA $38 3.3x 4.1x 4.4x 4.7x 5.0x 5.3x 5.7x

CY

2024E Adj. EBITDA - Management 36 3.5x 4.3x 4.6x 5.0x 5.3x 5.6x 6.0x

CY

2025E Adj. EBITDA - Management 35 3.6x 4.4x 4.7x 5.1x 5.4x 5.8x 6.1x

13

William

Blair

CONFIDENTIAL

Methodologies

and Assumptions

●

Identified five publicly traded companies in the

printing

and promotional marketing sectors

with

similar business models or financial

profiles

that William Blair deemed relevant

●

Calculated relevant operating and financial

metrics

and the following relevant multiples

and

compared them to the similar multiples for

ARIAL

at the current enterprise value and

implied

transaction value:

–

Enterprise Value / CY 2024E Adj. EBITDA

–

Enterprise Value / CY 2025E Adj. EBITDA

Selected

Public Companies

($

in millions)

Enterprise

Value /

Company

Equity Value

Enterprise

Value

CY

2024E Adj.

EBITDA

CY

2025E Adj.

EBITDA

$2,251

$3,769 7.8x 7.3x

981

2,528 6.2x 6.0x

950

1,623 4.8x 4.8x

1,468

1,311 2.8x 2.4x

258

802 3.4x 3.3x

577

453 5.7x N/A

Maximum

$2,251 $3,769 7.8x 7.3x

Median

965 1,467 5.3x 4.8x

Mean

1,081 1,748 5.1x 4.8x

Minimum

258 453 2.8x 2.4x

Selected

Public Companies Analysis

Sources:

FactSet, SEC filings and Wall Street consensus estimates as of June 18, 2024.

14

William

Blair

CONFIDENTIAL

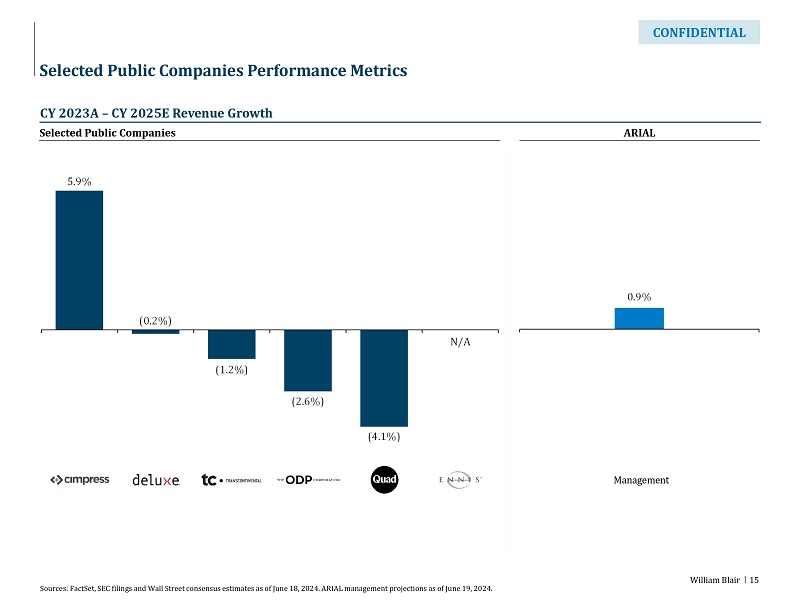

CY

2023A – CY 2025E Revenue Growth

Selected

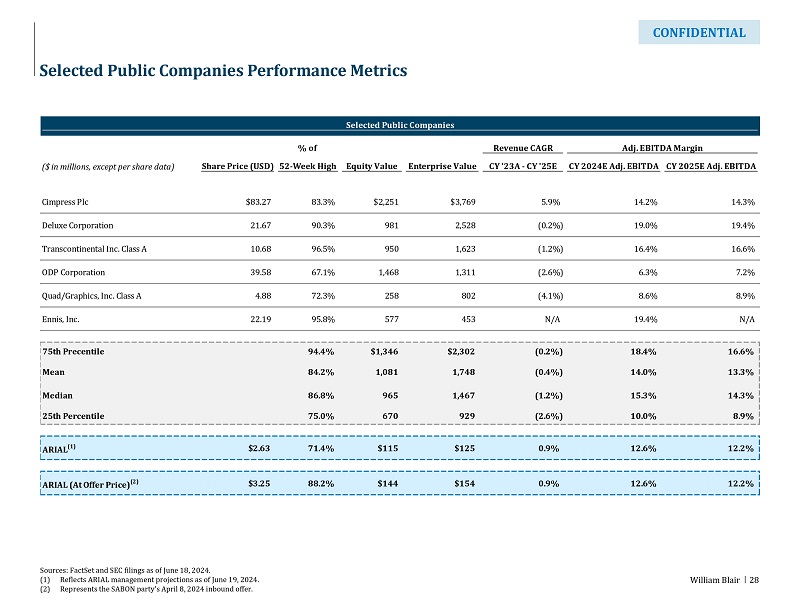

Public Companies Performance Metrics

ARIAL

Sources:

FactSet, SEC filings and Wall Street consensus estimates as of June 18, 2024. ARIAL management projections as of June 19, 2024.

Selected

Public Companies

Management

15

William

Blair

CONFIDENTIAL

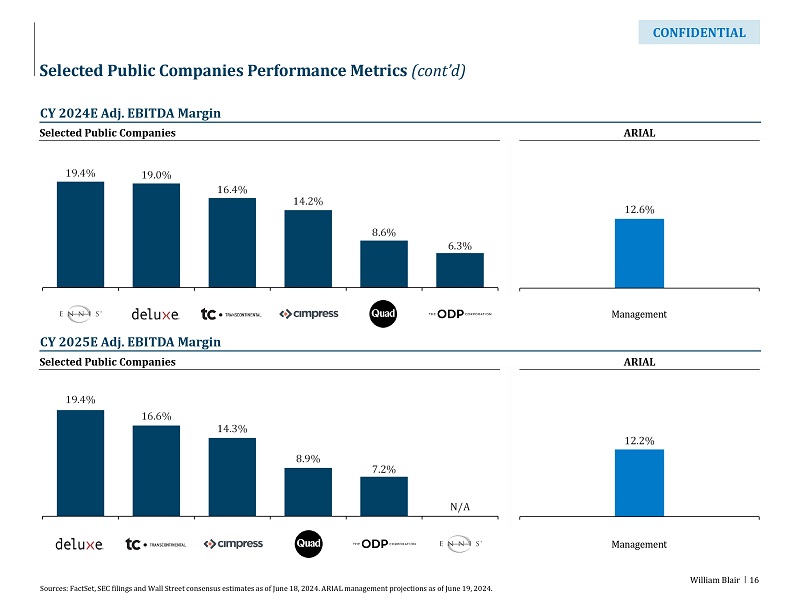

CY

2024E Adj. EBITDA Margin

Selected

Public Companies Performance Metrics (cont’d)

Selected

Public Companies

CY

2025E Adj. EBITDA Margin

ARIAL

Sources:

FactSet, SEC filings and Wall Street consensus estimates as of June 18, 2024. ARIAL management projections as of June 19, 2024.

Management

Management

Selected

Public Companies ARIAL

16

William

Blair

CONFIDENTIAL

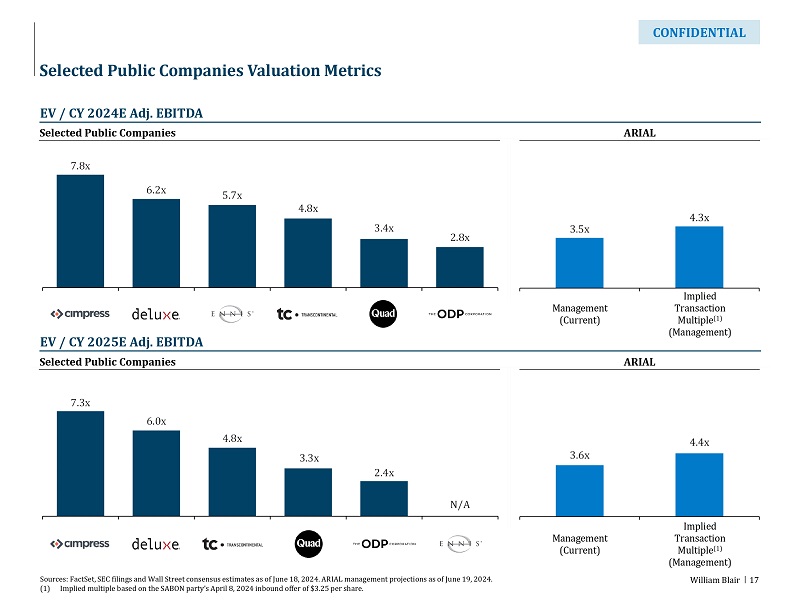

EV

/ CY 2024E Adj. EBITDA

Selected

Public Companies Valuation Metrics

Selected

Public Companies

EV

/ CY 2025E Adj. EBITDA

ARIAL

Sources:

FactSet, SEC filings and Wall Street consensus estimates as of June 18, 2024. ARIAL management projections as of June 19, 2024.

(1)

Implied multiple based on the SABON party’s April 8, 2024 inbound offer of $3.25 per share.

Management

(Current)

Implied

Transaction

Multiple(1)

(Management)

Management

(Current)

Implied

Transaction

Multiple(1)

(Management)

Selected

Public Companies ARIAL

17

William

Blair

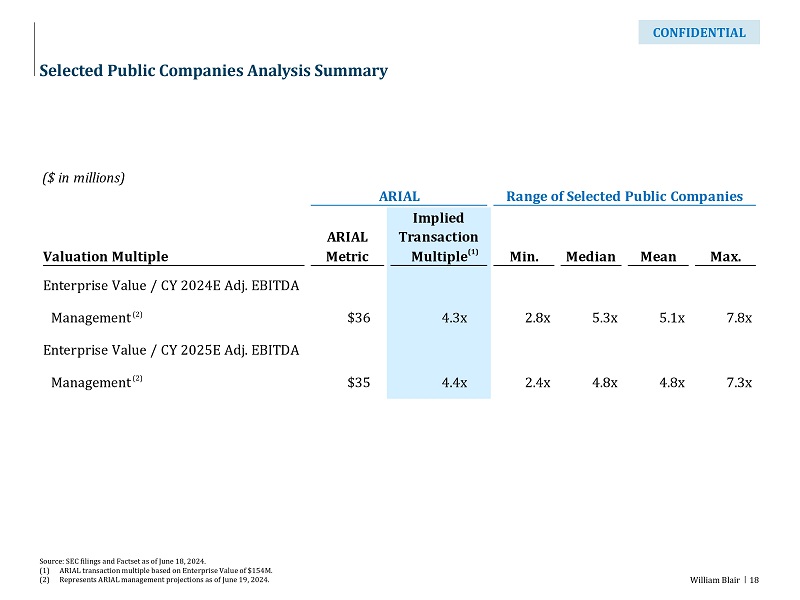

CONFIDENTIAL

($

in millions)

ARIAL

Range of Selected Public Companies

Implied

ARIAL

Transaction

Valuation

Multiple Metric Multiple Min. Median Mean Max.

Enterprise

Value / CY 2024E Adj. EBITDA

Management

$36 4.3x 2.8x 5.3x 5.1x 7.8x

Enterprise

Value / CY 2025E Adj. EBITDA

Management

$35 4.4x 2.4x 4.8x 4.8x 7.3x

Selected

Public Companies Analysis Summary

Source:

SEC filings and Factset as of June 18, 2024.

(1)

ARIAL transaction multiple based on Enterprise Value of $154M.

(2)

Represents ARIAL management projections as of June 19, 2024.

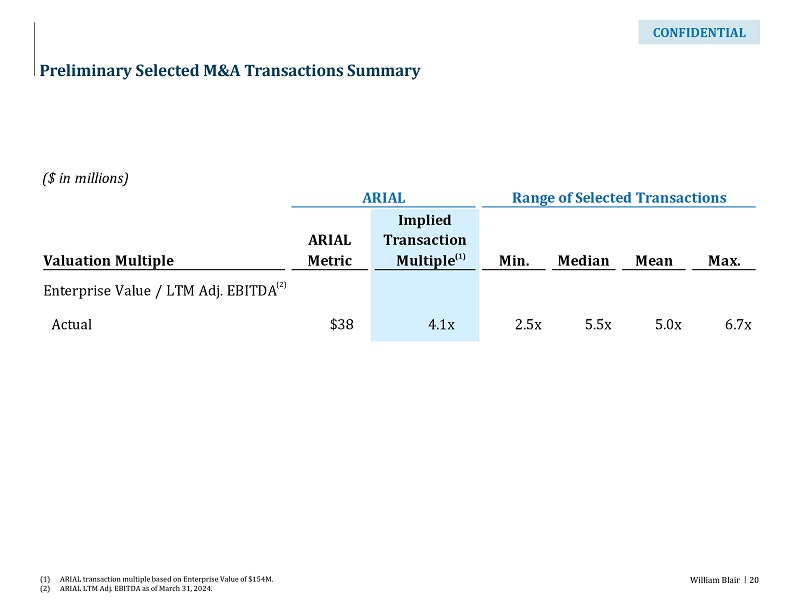

(1)

(2)

18

(2)

William

Blair

CONFIDENTIAL

($

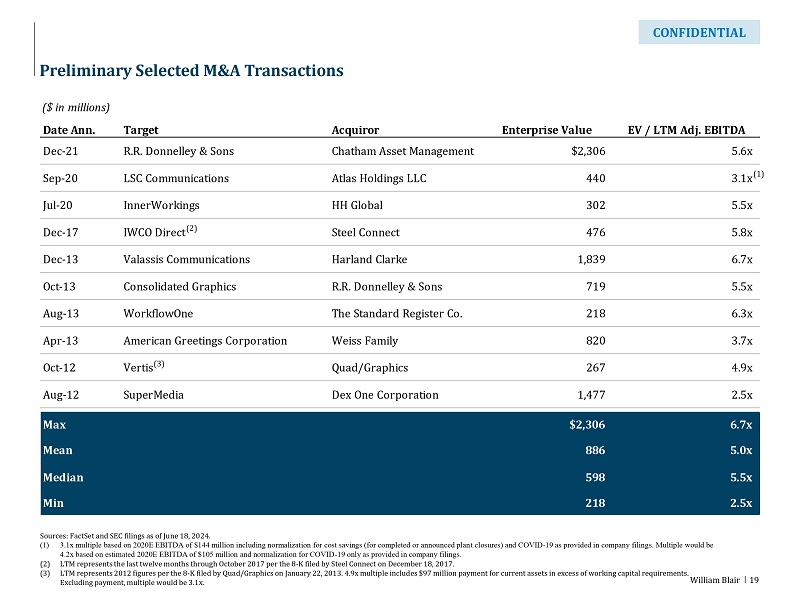

in millions)

Date

Ann. Target Acquiror Enterprise Value EV / LTM Adj. EBITDA

Dec-21

R.R. Donnelley & Sons Chatham Asset Management $2,306 5.6x

Sep-20

LSC Communications Atlas Holdings LLC 440 3.1x

Jul-20

InnerWorkings HH Global 302 5.5x

Dec-17

IWCO Direct Steel Connect 476 5.8x

Dec-13

Valassis Communications Harland Clarke 1,839 6.7x

Oct-13

Consolidated Graphics R.R. Donnelley & Sons 719 5.5x

Aug-13

WorkflowOne The Standard Register Co. 218 6.3x

Apr-13

American Greetings Corporation Weiss Family 820 3.7x

Oct-12

Vertis Quad/Graphics 267 4.9x

Aug-12

SuperMedia Dex One Corporation 1,477 2.5x

Max

$2,306 6.7x

Mean

886 5.0x

Median

598 5.5x

Min