UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

|

|

|

| Investment Company Act file number |

|

811-05120 |

Nuveen Municipal Value Fund, Inc.

(Exact name of registrant as

specified in charter)

Nuveen Investments

333 West Wacker Drive

Chicago, IL

60606

(Address of principal

executive offices) (Zip code)

Mark L. Winget

Nuveen Investments

333 West Wacker

Drive

Chicago, IL 60606

(Name and address of agent for service)

|

|

|

| Registrant’s telephone number, including area code: |

|

(312) 917-7700 |

|

|

|

| Date of fiscal year end: |

|

October 31 |

|

|

|

| Date of reporting period: |

|

October 31, 2023 |

Form N-CSR is to be used by management investment companies to file reports with the

Commission not later than 10 days after the transmission to stockholders of any report that is required to be transmitted to stockholders under Rule 30e-1 under the Investment Company Act of 1940 (17 CFR 270.30e-1). The Commission may use the information provided on Form N-CSR in its regulatory, disclosure review, inspection, and policymaking roles.

A registrant is required to disclose the information specified by Form N-CSR, and the Commission will make this

information public. A registrant is not required to respond to the collection of information contained in Form N-CSR unless the Form displays a currently valid Office of Management and Budget (“OMB”)

control number. Please direct comments concerning the accuracy of the information collection burden estimate and any suggestions for reducing the burden to Secretary, Securities and Exchange Commission, 450 Fifth Street, NW, Washington, DC

20549-0609. The OMB has reviewed this collection of information under the clearance requirements of 44 U.S.C. ss. 3507.

| ITEM 1. |

REPORTS TO STOCKHOLDERS. |

|

|

|

|

|

|

|

|

|

|

|

|

|

Closed-End Funds |

|

|

|

October 31,

2023 |

Nuveen Municipal Closed-End Funds

|

|

|

| |

|

| Nuveen Municipal Value Fund, Inc. |

|

NUV |

| |

|

| Nuveen AMT-Free Municipal Value Fund |

|

NUW |

| |

|

| Nuveen Municipal Income Fund, Inc. |

|

NMI |

Annual

Report

Table

of Contents

2

Chair’s Letter

to Shareholders

|

|

|

|

|

Dear Shareholders,

Financial markets spent the past year focused on the direction of inflation and whether policy makers would be able to deliver a soft landing in their economies. After

more than a year and a half of interest rate increases by the U.S. Federal Reserve (Fed) and other central banks, financial conditions have tightened and inflation rates have cooled considerably. The Fed increased the target fed funds rate from near

zero in March 2022 to a range of 5.25% to 5.50% as of November 2023, with pauses in June 2023, September 2023 and November 2023. But current inflation rates remain above central banks’ targets, and the trajectory from here is difficult to

predict given that monetary policy acts on the economy with long and variable lags.

Surprisingly, economies were relatively resilient for much of 2023. By year-end, the “most predicted recession” had yet

to materialize in the U.S., while U.K. and European economic growth was just beginning to show signs of stagnation or decline. U.S. gross domestic product rose 5.2% in the third quarter of 2023, 2.1% in the second quarter of 2023 and 2.0% in the

first quarter of 2023, after growing 2.1% in 2022 overall compared to 2021. Much of the growth was driven by a relatively strong jobs market, which kept consumer sentiment and spending elevated despite long-term interest rates nearing multi-year

highs, a series of U.S. regional bank failures and shocks from flaring geopolitical tensions.

While central banks are likely nearing the end of this interest rate hiking cycle, there are still upside risks to inflation and downside risks to the economy. Some

labor market and consumer indicators are softening. Government funding and deficits remain a concern, especially as the U.S. election year gets underway. The markets will continue to try to anticipate monetary policy shifts as the Fed evaluates

incoming data and adjusts its rate setting activity on a meeting-by-meeting basis. Geopolitical risks – from relations with China, to wars in Europe and the Middle

East – also expand the range of outcomes from economies and markets around the world. All these uncertainties, and others, will remain sources of short-term market volatility. In this environment, Nuveen remains committed to filtering the

market noise for investable opportunities that ultimately serve long-term investment objectives. Maintaining a long-term perspective is also important for investors, and we encourage you to review your time horizon, risk tolerance and investment

goals with your financial professional. On behalf of the other members of the Nuveen Fund

Board, we look forward to continuing to earn your trust in the months and years ahead.

Terence J. Toth

Chair of the Board

December 22, 2023 |

3

Important Notices

Investment Policy Updates for NMI

Effective September 29, 2023, the

Fund’s Board of Directors approved certain investment policy changes for the Fund. The policy changes grant the Fund more flexibility to invest in lower rated municipal securities. For a description of the investment policy changes please see

the Shareholder Update section within this report. In addition, the Fund’s performance benchmark was changed from the S&P Municipal Bond Index to a linked benchmark comprised of the return streams from 100% of the S&P Municipal Bond

Index through September 29, 2023 and thereafter 100% of the S&P Municipal Yield Index. The Fund’s investment objective to provide a high level of current income exempt from federal income tax remains unchanged.

For more information regarding these changes, please visit Nuveen’s CEF homepage

www.nuveen.com/closed-end-funds.

Portfolio Manager Updates

Effective October 13, 2023, Kristen DeJong, CFA, and Scott Romans, Ph.D. were added as a portfolio manager of NMI. Effective October 13, 2023, Kristen DeJong,

CFA, was also added as a portfolio manager of NUV and NUW. Christopher Drahn will also continue to serve as a portfolio manager of NMI until his retirement on April 1, 2024. There were no other changes to the portfolio management of the Funds

during the reporting period.

4

Portfolio Managers’

Comments

Nuveen Municipal Value

Fund, Inc. (NUV)

Nuveen AMT-Free Municipal Value Fund (NUW)

Nuveen Municipal Income Fund, Inc. (NMI)

These Funds feature portfolio

management by Nuveen Asset Management, LLC (NAM), an affiliate of Nuveen Fund Advisors, LLC, the Funds’ investment adviser. Portfolio manager Daniel Close, CFA, and Kristen DeJong, CFA, manage the Nuveen Municipal Value Fund, Inc. (NUV) and

Nuveen AMT-Free Municipal Value Fund (NUW). Christopher Drahn, CFA, Kristen DeJong, CFA, and Scott Romans, PhD. serve as portfolio managers for the Nuveen Municipal Income Fund, Inc. (NMI).

Effective October 13, 2023, Kristen DeJong was added as portfolio manager of the Nuveen Municipal Value Fund, Inc. (NUV) and Nuveen AMT-Free Municipal Value Fund (NUW). Kristen DeJong and Scott Romans were added as portfolio managers of the Nuveen Municipal Income Fund, Inc. (NMI). Christopher Drahn will be retiring as a portfolio manager of NMI

on April 1, 2024.

Effective September 29, 2023, the benchmark for the Nuveen Municipal Income Fund, Inc. (NMI) changed to a linked benchmark

comprised of the return streams from 100% of the S&P Municipal Bond Index through September 29, 2023, and thereafter 100% of the S&P Municipal Yield Index.

Here the portfolio management teams discuss U.S. economic and municipal market conditions, key investment strategies and the Funds’ performance for the

twelve-month reporting period ended October 31, 2023. For more information on the Funds’ investment objectives and policies, please refer to the Shareholder Update section at the end of the report.

What factors affected the U.S. economy and market conditions during the twelve-month annual reporting period ended October 31, 2023?

The U.S. economy performed better than expected despite persistent inflationary pressure and rising interest rates during the twelve-month period ended October 31,

2023. Gross domestic product accelerated sharply in the third quarter of 2023 to an annualized rate of 5.2%, according to the U.S. Bureau of Economic Analysis second estimate, up from 2.1% in the second quarter of 2023. By comparison, GDP grew 2.1%

in 2022 overall. Early in the reporting period, inflation had risen sharply because of supply chain disruptions and high food and energy prices, the Russia-Ukraine war and China’s zero-COVID restrictions

(lifted in December 2022). Since then, price pressures have eased given normalization in supply chains, falling energy prices and aggressive measures by the U.S. Federal Reserve (Fed) and other global central banks to tighten financial conditions

and slow demand in their economies. Nevertheless, during the reporting period inflation levels remained much higher than central banks’ target levels.

The Fed

raised its target fed funds rate six times during the reporting period, bringing it to a range of 5.25% to 5.50% as of July 2023 and voting to hold it at that level at its next two meetings held near the end of the reporting period. For much of the

reporting period, the Fed’s activity led to significant volatility in bond and stock markets, given the uncertainty of how rising interest rates would affect the economy. One of the most highly visible impacts occurred in the U.S. regional

banking sector in March 2023, when Silicon Valley Bank, Signature Bank, First Republic Bank and Silvergate Bank failed. In the same month, Swiss bank UBS agreed to buy Credit Suisse, which was considered vulnerable in the current environment. The

Fed’s monetary tightening policy also contributed to an increase in the U.S. dollar’s value relative to major world currencies, which acts as a headwind to the profits of international companies and U.S. domestic companies with overseas

earnings.

During the reporting period, elevated inflation and higher borrowing costs weighed on some segments of the economy, including the real estate market.

Consumer spending, however, has remained more resilient than expected, in part because of a still-strong labor market, another key gauge of the economy’s health. As of October 2023, the unemployment rate was 3.9%, rising from its pre-pandemic low, with monthly job growth continuing to moderate. The strong labor market and wage gains helped the U.S. economy during the reporting period, even as the Fed sought to soften job growth to help curb

inflation pressures.

During the reporting period, investors also continued to monitor government funding and deficits. The U.S. government avoided a default

scenario after approving an increase to the debt ceiling limit in June 2023. At the same time, the potential for a government shutdown loomed but was ultimately avoided with funding resolutions passed in September 2023 and, subsequent to the close

of the reporting period, November 2023. Notably, in August 2023, ratings agency Fitch downgraded U.S. debt from AAA to AA+ based on concerns about the U.S.’s growing fiscal debt and reduced confidence in fiscal management.

The broad municipal bond market was impacted by interest rate volatility and economic uncertainty during the reporting period. Municipal yields rose across the maturity

spectrum, but the move was uneven. The greatest increase in yields was at the shorter end

5

Portfolio Managers’ Comments (continued)

of the curve as markets priced in a more aggressive pace of monetary tightening to combat

persistently high inflation. Although municipal bonds continued to exhibit relatively strong credit fundamentals, there were periods of spread widening during the reporting period as the market sell-off

continued.

Nuveen Municipal Value Fund, Inc. (NUV)

What key

strategies were used to manage the Fund during the twelve-month reporting period ended October 31, 2023?

NUV’s investment objective is to provide

current income exempt from regular federal income tax, investing primarily in a portfolio of municipal obligations issued by state and local government authorities or certain U.S. territories.

During the reporting period, the Fund’s trading activity remained focused on pursuing the Fund’s investment objective. The rising yield environment during this

reporting period was favorable for the Fund to reset embedded yields higher in its portfolio, primarily by executing on tax-loss swap opportunities. This strategy involves selling depreciated bonds with lower

embedded yields to reinvest in similarly structured, higher income-producing bonds to support the Fund’s income earnings and capture tax efficiencies.

During

the reporting period, buying was focused on longer dated, 4% and 5% coupon structures in the BBB to A rated credit quality range. Purchases were funded from the proceeds of called and maturing bonds, as well as from tax loss swapping.

As of October 31, 2023, NUV continued to use inverse floating rate securities. The Fund employs inverse floating rate securities, which are the residual interest in

a tender option bond (TOB) trust, and are sometimes referred to as “inverse floaters,” for a variety of reasons, including duration management, income enhancement and total return enhancement.

How did the Fund perform during the twelve-month reporting period ended October 31, 2023?

For the twelve-month reporting period ended October 31, 2023, NUV outperformed the S&P Municipal Bond Index. For the purposes of this Performance Commentary,

references to relative performance are in comparison to the S&P Municipal Bond Index.

The primary contributor to NUV’s relative performance was its

overweights to A and BBB rated credit quality bonds and corresponding underweights to AAA and AA rated bonds. Security selection also contributed to the Fund’s relative performance, particularly in zero coupon bonds held over the full reporting

period and a position in the Florida high speed rail, Brightline, which was still held at the end of the reporting period. Brightline’s Orlando station completed construction and opened to the public during the period while ridership growth has

continued to gain momentum. In addition, the Fund benefited from an overweight allocation to the outperforming dedicated tax sector and an underweight to the life care sector, which mitigated the fund’s exposure to the sector’s downturn.

Partially offsetting the Fund’s outperformance was an underweight to the industrial development revenue (IDR) sector, which outperformed during the reporting

period. Additionally, relative performance was negatively impacted by the Fund’s exposure to bonds purchased earlier in the reporting period when interest rates were lower. These bonds generally underperformed as rates rose over the remainder

of the reporting period.

Nuveen AMT-Free Municipal Value Fund (NUW)

What key strategies were used to manage the Fund during the twelve-month reporting period ended October 31, 2023?

NUW’s investment objective is to provide current income exempt from regular federal income tax, investing primarily in a portfolio of municipal obligations issued

by state and local government authorities or certain U.S. territories.

During the reporting period, the Fund’s trading activity remained focused on pursuing

the Fund’s investment objectives. The rising yield environment during this reporting period was favorable for the Fund to reset embedded yields higher in its portfolio, primarily by executing on tax-loss

swap opportunities. This strategy involves selling depreciated bonds with lower embedded yields to reinvest in similarly structured, higher income-producing bonds to support the Fund’s income earnings and capture tax efficiencies.

During the reporting period, buying was focused on longer dated, 4% and 5% coupon structures in the BBB to A rated credit quality range. Purchases were funded from the

proceeds of called and maturing bonds, as well as from tax loss swapping.

6

As of October 31, 2023, NUW continued to use inverse floating rate securities. The Fund

employs inverse floating rate securities, which are the residual interest in a tender option bond (TOB) trust, and are sometimes referred to as “inverse floaters,” for a variety of reasons, including duration management, income enhancement

and total return enhancement.

How did the Fund perform during the twelve-month reporting period ended October 31, 2023?

For the twelve-month reporting period ended October 31, 2023, NUW outperformed the S&P Municipal Bond Index. For the purposes of this Performance Commentary,

references to relative performance are in comparison to the S&P Municipal Bond Index.

The primary contributor to NUW’s relative performance was security

selection, particularly in zero coupon bonds, which recovered from lows during the period. NUW’s overall duration positioning was also favorable. The Fund’s underweight to the shortest (zero to four year) duration bonds contributed

positively to relative performance earlier in the reporting period while an overweight to the longest (10 years and longer) duration bonds added value later in the period. NUW’s duration shortening hedge through interest rate futures also

positively impacted relative performance over the reporting period. NUW’s credit quality positioning was advantageous, as credit spreads narrowed occasionally throughout the period. Overweight allocations to A and BBB rated bonds added to

relative performance as lower rated categories outperformed the highest grade (AAA and AA rated) categories.

NUW’s outperformance was partially offset by an

underweight to the “other transportation” sector, and especially New York MTA (Metropolitan Transportation Authority) bonds, both of which outperformed. Additionally, relative performance was negatively impacted by the Fund’s exposure

to bonds purchased earlier in the reporting period when interest rates were lower. These bonds generally underperformed as rates rose over the remainder of the reporting period.

Nuveen Municipal Income Fund, Inc. (NMI)

What key strategies were used to

manage the Fund during the twelve-month reporting period ended October 31, 2023?

NMI’s investment objective is to provide current income exempt from

regular federal income tax, investing primarily in a portfolio of municipal obligations issued by state and local government authorities or certain U.S. territories.

During the reporting period, the Fund’s trading activity remained focused on pursuing the Fund’s investment objective. The rising yield environment during this

reporting period was favorable for the Fund to reset embedded yields higher in its portfolio, primarily by executing on tax-loss swap opportunities. This strategy involves selling depreciated bonds with lower

embedded yields to reinvest in similarly structured, higher income-producing bonds to support the Fund’s income earnings and capture tax efficiencies.

The

Fund’s weighting in the pre-refunded sector declined over the reporting period, driven by bond calls and maturities. The portfolio management team reinvested the proceeds across a diverse group of

sectors. Notably, NMI increased its weighting in A rated bonds and the airport sector during the reporting period. In October 2023, as a result of investment policy and other related changes, the portfolio management team increased NMI’s

exposure to sub investment grade and non-rated bonds and lengthened the Fund’s duration to align it with the S&P Municipal Yield Index.

How did the Fund perform during the twelve-month reporting period ended October 31, 2023?

For the twelve-month reporting period ended October 31, 2023, NMI outperformed the NMI Linked Benchmark. For the purposes of this reporting period, references to

relative performance are in comparison to the NMI Linked Benchmark, which represents the linked returns between the S&P Municipal Bond Index (through September 29, 2023) and the S&P Municipal Yield Index (subsequent to

September 29, 2023).

During the first 11 months of the reporting period, the primary contributor to NMI’s relative performance versus the S&P

Municipal Bond Index was its overweight to longer-duration bonds. Additional contributors during the first 11 months of the reporting period included overweights to A, BBB and BB rated bonds. The Fund also benefited from overweights to airports and

toll roads, which saw traffic and travel volumes rebound to pre-pandemic levels, and underweights to state and local general obligation bonds, which helped offset the sector’s relative underperformance.

In the one-month period ended October 31, 2023, NMI’s outperformance relative to the S&P Municipal Yield Index was driven by its overweight to higher rated bonds.

7

Portfolio Managers’ Comments (continued)

During the reporting period, there were no material detractors from relative performance.

This material is not intended to be a recommendation or investment advice, does not constitute a solicitation to buy, sell or hold a security or an investment

strategy, and is not provided in a fiduciary capacity. The information provided does not take into account the specific objectives or circumstances of any particular investor, or suggest any specific course of action. Investment decisions should be

made based on an investor’s objectives and circumstances and in consultation with his or her advisors.

Certain statements in this report are

forward-looking statements. Discussions of specific investments are for illustration only and are not intended as recommendations of individual investments. The forward-looking statements and other views expressed herein are those of the portfolio

managers as of the date of this report. Actual future results or occurrences may differ significantly from those anticipated in any forward-looking statements, and the views expressed herein are subject to change at any time, due to numerous market

and other factors. The Funds disclaim any obligation to update publicly or revise any forward-looking statements or views expressed herein.

For financial

reporting purposes, the ratings disclosed are the highest rating given by one of the following national rating agencies: Standard & Poor’s Group (S&P), Moody’s Investors Service, Inc. (Moody’s) or Fitch, Inc. (Fitch).

This treatment of split-rated securities may differ from that used for other purposes, such as for Fund investment policies. Credit ratings are subject to change. AAA, AA, A and BBB are investment grade ratings, while BB, B, CCC, CC, C and D are

below investment grade ratings. Holdings designated N/R are not rated by these national rating agencies.

Bond insurance guarantees only the payment of

principal and interest on the bond when due, and not the value of the bonds themselves, which will fluctuate with the bond market and the financial success of the issuer and the insurer. Insurance relates specifically to the bonds in the portfolio

and not to the share prices of a Fund. No representation is made as to the insurers’ ability to meet their commitments.

Refer to the Glossary of Terms

Used in this Report for further definition of the terms used within this section.

8

Common Share Information

COMMON SHARE DISTRIBUTION INFORMATION

The following information

regarding the Funds’ distributions is current as of October 31, 2023. Each Fund’s distribution levels may vary over time based on each Fund’s investment activity and portfolio investment value changes.

During the current reporting period, each Fund’s distributions to common shareholders were as shown in the accompanying table.

|

|

|

|

|

|

|

| |

|

Per Common Share Amounts |

| Monthly Distributions (Ex-Dividend Date) |

|

NUV |

|

NUW |

|

NMI |

|

|

|

|

| November |

|

$0.0280 |

|

$0.0390 |

|

$0.0300 |

| December |

|

0.0280 |

|

0.0390 |

|

0.0300 |

| January |

|

0.0280 |

|

0.0390 |

|

0.0300 |

| February |

|

0.0280 |

|

0.0390 |

|

0.0300 |

| March |

|

0.0280 |

|

0.0390 |

|

0.0300 |

| April |

|

0.0280 |

|

0.0405 |

|

0.0300 |

| May |

|

0.0280 |

|

0.0405 |

|

0.0300 |

| June |

|

0.0280 |

|

0.0405 |

|

0.0300 |

| July |

|

0.0280 |

|

0.0405 |

|

0.0315 |

| August |

|

0.0280 |

|

0.0405 |

|

0.0315 |

| September |

|

0.0280 |

|

0.0405 |

|

0.0315 |

| October |

|

0.0290 |

|

0.0425 |

|

0.0315 |

| Total Distributions from Net

Investment Income |

|

$0.3370 |

|

$0.4805 |

|

$0.3660 |

|

|

|

|

| Yields |

|

NUV |

|

NUW |

|

NMI |

| Market Yield1 |

|

4.36% |

|

4.05% |

|

4.53% |

| Taxable-Equivalent

Yield1 |

|

7.34% |

|

6.84% |

|

7.65% |

| 1 |

Market Yield is based on the Fund’s current annualized monthly dividend divided by the Fund’s current market

price as of the end of the reporting period. Taxable-Equivalent Yield represents the yield that must be earned on a fully taxable investment in order to equal the yield of the Fund on an after-tax basis. It is

based on a federal income tax rate of 40.8%. Your actual federal income tax rate may differ from the assumed rate. The Taxable-Equivalent Yield also takes into account the percentage of the Fund’s income generated and paid by the Fund (based on

payments made during the previous calendar year) that was not exempt from federal income tax. Separately, if the comparison were instead to investments that generate qualified dividend income, which is taxable at a rate lower than an

individual’s ordinary graduated tax rate, the fund’s Taxable-Equivalent Yield would be lower. |

Each Fund seeks to pay regular monthly

dividends out of its net investment income at a rate that reflects its past and projected net income performance. To permit each Fund to maintain a more stable monthly dividend, the Fund may pay dividends at a rate that may be more or less than the

amount of net income actually earned by the Fund during the period. Distributions to common shareholders are determined on a tax basis, which may differ from amounts recorded in the accounting records. In instances where the monthly dividend exceeds

the earned net investment income, the Fund would report a negative undistributed net ordinary income. Refer to the Notes to Financial Statements for additional information regarding the amounts of undistributed net ordinary income and

undistributed net long-term capital gains and the character of the actual distributions paid by the Fund during the period.

All monthly dividends paid by each Fund

during the current reporting period were paid from net investment income. If a portion of the Fund’s monthly distributions is sourced or comprised of elements other than net investment income, including capital gains and/ or a return of

capital, shareholders will be notified of those sources. For financial reporting purposes, the per share amounts of each Fund’s distributions for the reporting period are presented in this report’s Financial Highlights. For income tax

purposes, distribution information for each Fund as of its most recent tax year end is presented in the Notes to Financial Statements of this report.

Updated Distribution Policy

On October 23, 2023, the Funds’ Board

of Trustees (the “Board”) updated each Fund’s distribution policy. Effective for distributions payable on December 1, 2023, each Fund’s distribution policy, which may be changed by the Board, is to make regular monthly cash

distributions to holders of its common shares (stated in terms of a fixed cents per common share dividend distribution rate which may be set from time to time). The Fund intends to distribute all or substantially all of its net investment income

through its regular monthly distribution and to distribute realized capital gains at least annually. In addition, in any monthly period, to maintain its declared per common share distribution amount, the Fund may distribute more or less than its net

investment income during the period. In the event the Fund distributes more than its net investment income during any yearly period, such distributions may also include realized gains and/or a return of capital. To the extent that a distribution

includes a return of capital the NAV per share may erode. If the Fund’s distribution includes anything other than net investment income, the Fund will provide a notice to shareholders

9

Common Share Information (continued)

of its best estimate of the distribution sources at that the time of the distribution. These

estimates may not match the final tax characterization (for the full year’s distributions) contained in shareholders’ 1099-DIV forms after the end of the year.

NUVEEN CLOSED-END FUND DISTRIBUTION AMOUNTS

The Nuveen Closed-End Funds’ monthly and quarterly periodic distributions to shareholders are posted on www.nuveen.com and

can be found on Nuveen’s enhanced closed-end fund resource page, which is at https://www.nuveen.com/resource-center-closedend funds, along with other Nuveen

closed-end fund product updates. To ensure timely access to the latest information, shareholders may use a subscribe function, which can be activated at this web page (https://www.nuveen.com/subscriptions).

COMMON SHARE EQUITY SHELF PROGRAM

During the current reporting

period, NMI was authorized by the Securities and Exchange Commission to issue additional common shares through an equity shelf program (Shelf Offering). Under these programs, NMI, subject to market conditions, may raise additional capital

from time to time in varying amounts and offering methods at a net price at or above the Fund’s NAV per common share. The maximum aggregate offering under these Shelf Offerings are as shown in the accompanying table.

|

|

|

| |

|

NMI |

| Additional authorized common shares |

|

2,000,000 |

During the current reporting period, the Fund sold common shares through their Shelf Offerings at a weighted average premium to their NAV

per common share as shown in the accompanying table.

|

|

|

| |

|

NMI |

| Common shares sold through shelf offering |

|

4,954 |

| Weighted average premium to NAV per common share sold |

|

1.11% |

Refer to the Notes to Financial Statements for further details on Shelf Offerings and the Fund’s transactions.

COMMON SHARE REPURCHASES

The Funds’ Board of Directors/Trustees

reauthorized an open-market share repurchase program, allowing each Fund to repurchase and retire an aggregate of up to approximately 10% of its outstanding common shares.

During the current reporting period, the Funds did not repurchase any of their outstanding common shares. As of October 31, 2023, (and since the inception of the

Funds’ repurchase programs), each Fund has cumulatively repurchased and retired its outstanding common shares as shown in the accompanying table.

|

|

|

|

|

|

|

| |

|

NUV |

|

NUW |

|

NMI |

| Common shares cumulatively repurchased and retired |

|

0 |

|

0 |

|

0 |

| Common shares authorized for repurchase |

|

20,750,000 |

|

1,795,000 |

|

1,005,000 |

OTHER COMMON SHARE INFORMATION

As of

October 31, 2023, the Funds’ common share prices were trading at a premium/(discount) to their common share NAVs and trading at an average premium/(discount) to NAV during the current reporting period, as follows:

|

|

|

|

|

|

|

| |

|

NUV |

|

NUW |

|

NMI |

| Common share NAV |

|

$ 8.69 |

|

$ 14.20 |

|

$ 9.16 |

| Common share price |

|

$ 7.99 |

|

$ 12.60 |

|

$ 8.35 |

| Premium/(Discount) to NAV |

|

(8.06)% |

|

(11.27)% |

|

(8.84)% |

| Average premium/(discount) to NAV |

|

(6.03)% |

|

(8.73)% |

|

(4.55)% |

10

About the Funds’ Benchmarks

S&P Municipal Bond Index: An index designed to measure the performance of the tax-exempt U.S. municipal bond market. Index returns assume reinvestment of distributions, but do not reflect any

applicable sales charges or management fees.

S&P Municipal Yield Index: An index that is structured so that 70% of the index consists of bonds that are either not rated or are rated below investment grade, 20% are rated BBB/Baa, and 10% are rated single A. Index returns assume

reinvestment of distributions, but do not reflect any applicable sales charges or management fees.

NMI

Linked Benchmark: Represents the linked returns between the S&P Municipal Bond Index (defined herein) through September 29, 2023 and the S&P Municipal Yield Index (defined

herein) subsequent to September 29, 2023.

11

|

|

|

| NUV |

|

Nuveen Municipal Value Fund,

Inc. Performance Overview and Holding Summaries as of

October 31, 2023 |

Refer to the Glossary of Terms Used in this Report for further definition of the terms used within this section.

Fund Performance*

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |

|

|

|

|

Total Returns as of

October 31, 2023

|

|

| |

|

|

|

|

Average Annual |

|

| |

|

Inception

Date |

|

|

1-Year |

|

|

5-Year |

|

|

10-Year |

|

| |

|

| NUV at Common Share NAV |

|

|

6/17/87 |

|

|

|

2.79% |

|

|

|

1.04% |

|

|

|

2.77% |

|

| |

|

| NUV at Common Share Price |

|

|

6/17/87 |

|

|

|

(0.52)% |

|

|

|

0.84% |

|

|

|

2.64% |

|

| |

|

| S&P Municipal Bond Index |

|

|

– |

|

|

|

2.36% |

|

|

|

1.04% |

|

|

|

2.18% |

|

| |

|

*For purposes of Fund performance, relative results are measured against the S&P Municipal Bond Index.

Performance data shown represents past performance and does not predict or guarantee future results. Current performance may be higher or lower than the data shown.

Returns do not reflect the deduction of taxes that shareholders may have to pay on Fund distributions or upon the sale of Fund shares. Returns at NAV are net of Fund expenses, and assume reinvestment of distributions. Comparative index return

information is provided for the Fund’s shares at NAV only. Indexes are not available for direct investment.

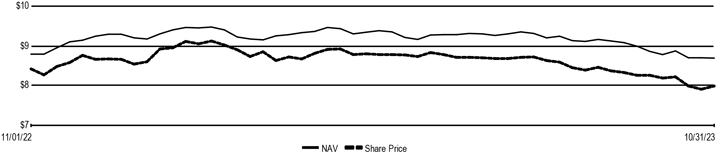

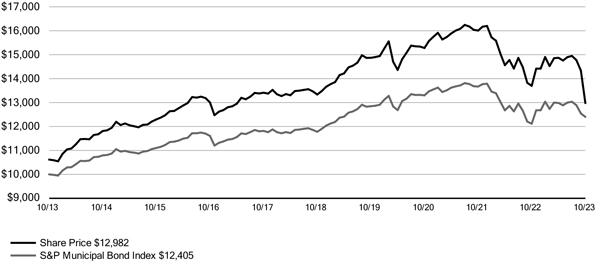

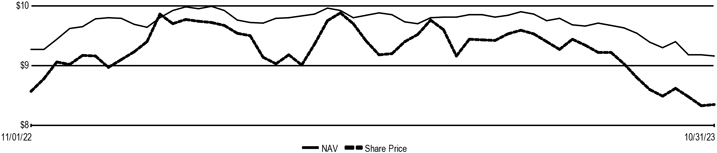

Daily Common Share NAV and Share Price

Growth of an Assumed $10,000 Investment as of October 31, 2023 - Common Share

Price

12

Holdings Summaries as of October 31, 2023

This data relates to the securities held in the Fund’s portfolio of investments as of the end of the reporting period. It should not be construed as a measure of

performance for the Fund itself. Holdings are subject to change.

For financial reporting purposes, the ratings disclosed are the highest rating given by one of

the following national rating agencies: Standard & Poor’s Group, Moody’s Investors Service, Inc. or Fitch, Inc. This treatment of split-rated securities may differ from that used for other purposes, such as for Fund investment

policies. Credit ratings are subject to change. AAA, AA, A and BBB are investment grade ratings; BB, B, CCC, CC, C and D are below-investment grade ratings. Holdings designated N/R are not rated by these national rating agencies.

|

|

|

|

|

| Fund Allocation |

|

|

|

| (% of net assets) |

|

|

|

| |

|

| Municipal Bonds |

|

|

99.5% |

|

| |

|

| Other Assets & Liabilities, Net |

|

|

1.7% |

|

| |

|

| Floating Rate Obligations |

|

|

(1.2)% |

|

| |

|

| Net Assets |

|

|

100% |

|

| |

|

|

|

| Bond Credit Quality |

|

|

|

| (% of total investment exposure) |

|

|

|

| |

|

| U.S. Guaranteed |

|

|

4.2% |

|

| |

|

| AAA |

|

|

7.6% |

|

| |

|

| AA |

|

|

40.4% |

|

| |

|

| A |

|

|

28.4% |

|

| |

|

| BBB |

|

|

11.2% |

|

| |

|

| BB or Lower |

|

|

2.3% |

|

| |

|

| N/R (not rated) |

|

|

5.9% |

|

| |

|

| Total |

|

|

100% |

|

| |

|

|

|

|

|

|

| Portfolio Composition |

|

|

|

| (% of total investments) |

|

|

|

| |

|

| Tax Obligation/Limited |

|

|

28.4% |

|

| |

|

| Transportation |

|

|

20.6% |

|

| |

|

| Tax Obligation/General |

|

|

14.4% |

|

| |

|

| Utilities |

|

|

14.2% |

|

| |

|

| Health Care |

|

|

7.6% |

|

| |

|

| Education and Civic Organizations |

|

|

4.8% |

|

| |

|

| U.S. Guaranteed |

|

|

4.7% |

|

| |

|

| Other |

|

|

5.3% |

|

| |

|

| Total |

|

|

100% |

|

| |

|

|

|

|

|

|

| States and Territories1 |

|

|

|

| (% of total municipal bonds) |

|

|

|

| |

|

| Texas |

|

|

13.1% |

|

| |

|

| Illinois |

|

|

11.0% |

|

| |

|

| New York |

|

|

7.6% |

|

| |

|

| California |

|

|

6.5% |

|

| |

|

| Colorado |

|

|

6.4% |

|

| |

|

| Florida |

|

|

5.7% |

|

| |

|

| New Jersey |

|

|

4.5% |

|

| |

|

| Ohio |

|

|

4.0% |

|

| |

|

| Washington |

|

|

4.0% |

|

| |

|

| Georgia |

|

|

4.0% |

|

| |

|

| Michigan |

|

|

3.0% |

|

| |

|

| Nevada |

|

|

2.7% |

|

| |

|

| South Carolina |

|

|

2.4% |

|

| |

|

| Pennsylvania |

|

|

2.1% |

|

| |

|

| Kentucky |

|

|

1.8% |

|

| |

|

| Puerto Rico |

|

|

1.8% |

|

| |

|

| District of Columbia |

|

|

1.7% |

|

| |

|

| Tennessee |

|

|

1.5% |

|

| |

|

| Oklahoma |

|

|

1.4% |

|

| |

|

| Utah |

|

|

1.4% |

|

| |

|

| Other |

|

|

13.4% |

|

| |

|

| Total |

|

|

100% |

|

| |

|

| 1 |

See the Portfolio of Investments for the remaining states comprising “Other” and not listed in the table above.

|

13

|

|

|

| NUW |

|

Nuveen AMT-Free Municipal

Value Fund Performance Overview and Holding Summaries as of

October 31, 2023 |

Refer to the Glossary of Terms Used in this Report for further definition of the terms used within this section.

Fund Performance*

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |

|

|

|

|

Total Returns as of

October 31, 2023 |

|

| |

|

|

|

|

Average Annual |

|

| |

|

Inception

Date |

|

|

1-Year |

|

|

5-Year |

|

|

10-Year |

|

| |

|

| NUW at Common Share NAV |

|

|

2/25/09 |

|

|

|

3.27% |

|

|

|

1.24% |

|

|

|

2.79% |

|

| |

|

| NUW at Common Share Price |

|

|

2/25/09 |

|

|

|

(1.08)% |

|

|

|

1.04% |

|

|

|

2.42% |

|

| |

|

| S&P Municipal Bond Index |

|

|

– |

|

|

|

2.36% |

|

|

|

1.04% |

|

|

|

2.18% |

|

| |

|

*For purposes of Fund performance, relative results are measured against the S&P Municipal Bond Index.

Performance data shown represents past performance and does not predict or guarantee future results. Current performance may be higher or lower than the data shown.

Returns do not reflect the deduction of taxes that shareholders may have to pay on Fund distributions or upon the sale of Fund shares. Returns at NAV are net of Fund expenses, and assume reinvestment of distributions. Comparative index return

information is provided for the Fund’s shares at NAV only. Indexes are not available for direct investment.

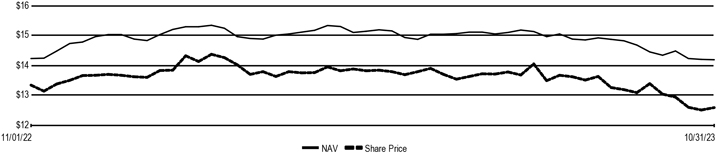

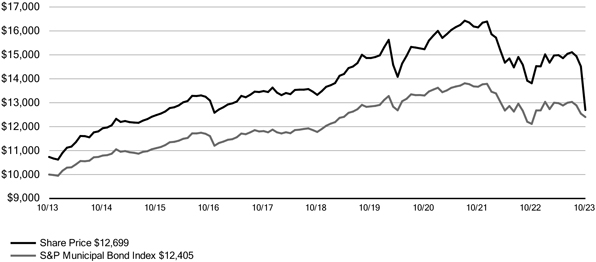

Daily Common Share NAV and Share Price

Growth of an Assumed $10,000 Investment as of October 31, 2023 - Common Share

Price

14

Holdings Summaries as of October 31, 2023

This data relates to the securities held in the Fund’s portfolio of investments as of the end of the reporting period. It should not be construed as a measure of

performance for the Fund itself. Holdings are subject to change.

For financial reporting purposes, the ratings disclosed are the highest rating given by one of

the following national rating agencies: Standard & Poor’s Group, Moody’s Investors Service, Inc. or Fitch, Inc. This treatment of split-rated securities may differ from that used for other purposes, such as for Fund investment

policies. Credit ratings are subject to change. AAA, AA, A and BBB are investment grade ratings; BB, B, CCC, CC, C and D are below-investment grade ratings. Holdings designated N/R are not rated by these national rating agencies.

|

|

|

|

|

| Fund Allocation |

|

|

|

| (% of net assets) |

|

|

|

| |

|

| Municipal Bonds |

|

|

98.5% |

|

| |

|

| Common Stocks |

|

|

0.5% |

|

| |

|

| Other Assets & Liabilities, Net |

|

|

1.8% |

|

| |

|

| Floating Rate Obligations |

|

|

(0.8)% |

|

| |

|

| Net Assets |

|

|

100% |

|

| |

|

|

|

| Bond Credit Quality |

|

|

|

| (% of total investment exposure) |

|

|

|

| |

|

| U.S. Guaranteed |

|

|

1.6% |

|

| |

|

| AAA |

|

|

7.7% |

|

| |

|

| AA |

|

|

40.8% |

|

| |

|

| A |

|

|

29.6% |

|

| |

|

| BBB |

|

|

11.7% |

|

| |

|

| BB or Lower |

|

|

2.0% |

|

| |

|

| N/R (not rated) |

|

|

6.1% |

|

| |

|

| N/A (not applicable) |

|

|

0.5% |

|

| |

|

| Total |

|

|

100% |

|

| |

|

|

|

|

|

|

| Portfolio Composition |

|

|

|

| (% of total investments) |

|

|

|

| |

|

| Tax Obligation/Limited |

|

|

24.2% |

|

| |

|

| Utilities |

|

|

20.2% |

|

| |

|

| Tax Obligation/General |

|

|

16.9% |

|

| |

|

| Transportation |

|

|

10.5% |

|

| |

|

| Health Care |

|

|

9.5% |

|

| |

|

| Education and Civic Organizations |

|

|

7.2% |

|

| |

|

| Consumer Staples |

|

|

4.4% |

|

| |

|

| Other |

|

|

6.6% |

|

| |

|

| Common Stocks |

|

|

0.5% |

|

| |

|

| Total |

|

|

100% |

|

| |

|

|

|

|

|

|

| States and Territories1 |

|

|

|

| (% of total municipal bonds) |

|

|

|

| |

|

| California |

|

|

11.5% |

|

| |

|

| Illinois |

|

|

10.4% |

|

| |

|

| Texas |

|

|

9.6% |

|

| |

|

| New York |

|

|

6.9% |

|

| |

|

| New Jersey |

|

|

6.9% |

|

| |

|

| Nevada |

|

|

5.6% |

|

| |

|

| Pennsylvania |

|

|

4.4% |

|

| |

|

| Ohio |

|

|

4.2% |

|

| |

|

| Colorado |

|

|

4.1% |

|

| |

|

| Florida |

|

|

3.8% |

|

| |

|

| Tennessee |

|

|

3.8% |

|

| |

|

| Washington |

|

|

3.5% |

|

| |

|

| Kentucky |

|

|

3.4% |

|

| |

|

| Maryland |

|

|

3.2% |

|

| |

|

| Puerto Rico |

|

|

3.0% |

|

| |

|

| Georgia |

|

|

2.6% |

|

| |

|

| South Carolina |

|

|

1.7% |

|

| |

|

| West Virginia |

|

|

1.5% |

|

| |

|

| Arizona |

|

|

1.3% |

|

| |

|

| Minnesota |

|

|

1.2% |

|

| |

|

| Other |

|

|

7.4% |

|

| |

|

| Total |

|

|

100% |

|

| |

|

| 1 |

See the Portfolio of Investments for the remaining states comprising “Other” and not listed in the table above.

|

15

|

|

|

| NMI |

|

Nuveen Municipal Income Fund, Inc. |

| |

Performance Overview and Holding Summaries as of October 31, 2023 |

Refer to the Glossary of Terms Used in this Report for further definition of the terms used within this section.

Fund Performance*

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |

|

|

|

|

Total Returns as of

October 31, 2023 |

|

| |

|

|

|

|

Average Annual |

|

| |

|

Inception

Date |

|

|

1-Year |

|

|

5-Year |

|

|

10-Year |

|

| |

|

| NMI at Common Share NAV |

|

|

4/20/88 |

|

|

|

2.94% |

|

|

|

0.24% |

|

|

|

2.47% |

|

| |

|

| NMI at Common Share Price |

|

|

4/20/88 |

|

|

|

1.80% |

|

|

|

0.05% |

|

|

|

2.26% |

|

| |

|

| S&P Municipal Bond Index |

|

|

– |

|

|

|

2.36% |

|

|

|

1.04% |

|

|

|

2.18% |

|

| |

|

| S&P Municipal Yield Index |

|

|

– |

|

|

|

3.80% |

|

|

|

1.55% |

|

|

|

3.70% |

|

| |

|

| NMI Linked Benchmark |

|

|

– |

|

|

|

1.23% |

|

|

|

0.81% |

|

|

|

2.06% |

|

| |

|

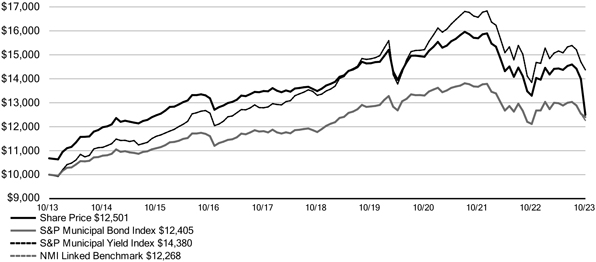

*For purposes of Fund performance, relative results are measured against the linked returns between the S&P Municipal Bond Index

(through September 29, 2023) and the S&P Municipal Yield Index (subsequent to September 29, 2023).

Performance data shown represents past performance

and does not predict or guarantee future results. Current performance may be higher or lower than the data shown. Returns do not reflect the deduction of taxes that shareholders may have to pay on Fund distributions or upon the sale of Fund shares.

Returns at NAV are net of Fund expenses, and assume reinvestment of distributions. Comparative index return information is provided for the Fund’s shares at NAV only. Indexes are not available for direct investment.

Daily Common Share NAV and Share Price

Growth of an Assumed $10,000 Investment as of October 31, 2023 - Common Share

Price

16

Holdings Summaries as of October 31, 2023

This data relates to the securities held in the Fund’s portfolio of investments as of the end of the reporting period. It should not be construed as a measure of

performance for the Fund itself. Holdings are subject to change.

For financial reporting purposes, the ratings disclosed are the highest rating given by one of

the following national rating agencies: Standard & Poor’s Group, Moody’s Investors Service, Inc. or Fitch, Inc. This treatment of split-rated securities may differ from that used for other purposes, such as for Fund investment

policies. Credit ratings are subject to change. AAA, AA, A and BBB are investment grade ratings; BB, B, CCC, CC, C and D are below-investment grade ratings. Holdings designated N/R are not rated by these national rating agencies.

|

|

|

|

|

| Fund Allocation (% of net assets) |

|

|

|

| |

|

| Municipal Bonds |

|

|

96.6% |

|

| |

|

| Short-Term Municipal Bonds |

|

|

2.9% |

|

| |

|

| Other Assets & Liabilities, Net |

|

|

0.5% |

|

| |

|

| Net Assets |

|

|

100% |

|

| |

|

|

|

| Bond Credit Quality

(% of total investment exposure) |

|

|

|

|

| |

|

| U.S. Guaranteed |

|

|

3.7% |

|

| |

|

| AAA |

|

|

2.1% |

|

| |

|

| AA |

|

|

29.0 |

|

| |

|

| A |

|

|

30.3% |

|

| |

|

| BBB |

|

|

11.0% |

|

| |

|

| BB or Lower |

|

|

6.1% |

|

| |

|

| N/R (not rated) |

|

|

17.8% |

|

| |

|

| Total |

|

|

100% |

|

| |

|

|

|

|

|

|

| Portfolio Composition (% of total

investments) |

|

|

|

| |

|

| Transportation |

|

|

21.2% |

|

| |

|

| Health Care |

|

|

21.0% |

|

| |

|

| Tax Obligation/Limited |

|

|

18.0% |

|

| |

|

| Education and Civic Organizations |

|

|

10.5% |

|

| |

|

| Utilities |

|

|

8.7% |

|

| |

|

| Tax Obligation/General |

|

|

7.4% |

|

| |

|

| Long-Term Care |

|

|

3.8% |

|

| |

|

| Other |

|

|

9.4% |

|

| |

|

| Total |

|

|

100% |

|

| |

|

|

|

|

|

|

| States and Territories1

(% of total municipal bonds) |

|

|

|

| |

|

| Colorado |

|

|

15.0% |

|

| |

|

| Illinois |

|

|

12.6% |

|

| |

|

| Texas |

|

|

10.2% |

|

| |

|

| Florida |

|

|

5.6% |

|

| |

|

| Arizona |

|

|

4.9% |

|

| |

|

| Missouri |

|

|

4.2% |

|

| |

|

| New York |

|

|

3.8% |

|

| |

|

| Wisconsin |

|

|

3.8% |

|

| |

|

| Indiana |

|

|

2.8% |

|

| |

|

| North Carolina |

|

|

2.8% |

|

| |

|

| California |

|

|

2.7% |

|

| |

|

| New Jersey |

|

|

2.6% |

|

| |

|

| Louisiana |

|

|

2.3% |

|

| |

|

| Pennsylvania |

|

|

2.3% |

|

| |

|

| Alabama |

|

|

2.3% |

|

| |

|

| Georgia |

|

|

2.2% |

|

| |

|

| Virginia |

|

|

2.0% |

|

| |

|

| Hawaii |

|

|

1.8% |

|

| |

|

| Minnesota |

|

|

1.8% |

|

| |

|

| Ohio |

|

|

1.8% |

|

| |

|

| Other |

|

|

12.5% |

|

| |

|

| Total |

|

|

100% |

|

| |

|

| 1 |

See the Portfolio of Investments for the remaining states comprising “Other” and not listed in the table above.

|

17

Shareholder Meeting Report

The annual meeting of shareholders was held on August 9, 2023, for NUV, NUW, and NMI; at this meeting the shareholders were asked to elect Board members.

|

|

|

|

|

|

|

|

|

|

|

|

|

| |

|

NUV |

|

|

NUW |

|

|

NMI |

|

| |

|

| |

|

Common

Shares |

|

|

Common

Shares |

|

|

Common

Shares |

|

| |

|

| Approval of the Board Members was reached as follows: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Amy B.R. Lancellotta |

|

|

|

|

|

|

|

|

|

|

|

|

| For |

|

|

167,611,770 |

|

|

|

14,293,466 |

|

|

|

7,951,418 |

|

| Withhold |

|

|

4,342,613 |

|

|

|

1,752,981 |

|

|

|

364,554 |

|

| |

|

| Total |

|

|

171,954,383 |

|

|

|

16,046,447 |

|

|

|

8,315,972 |

|

| |

|

|

|

|

|

| John K. Nelson |

|

|

|

|

|

|

|

|

|

|

|

|

| For |

|

|

167,524,604 |

|

|

|

14,153,422 |

|

|

|

7,922,811 |

|

| Withhold |

|

|

4,429,779 |

|

|

|

1,893,025 |

|

|

|

393,161 |

|

| |

|

| Total |

|

|

171,954,383 |

|

|

|

16,046,447 |

|

|

|

8,315,972 |

|

| |

|

|

|

|

|

| Terence J. Toth |

|

|

|

|

|

|

|

|

|

|

|

|

| For |

|

|

167,333,902 |

|

|

|

14,162,033 |

|

|

|

7,896,658 |

|

| Withhold |

|

|

4,620,481 |

|

|

|

1,884,414 |

|

|

|

419,314 |

|

| |

|

| Total |

|

|

171,954,383 |

|

|

|

16,046,447 |

|

|

|

8,315,972 |

|

| |

|

|

|

|

|

| Robert L. Young |

|

|

|

|

|

|

|

|

|

|

|

|

| For |

|

|

167,700,960 |

|

|

|

14,153,629 |

|

|

|

7,966,792 |

|

| Withhold |

|

|

4,253,423 |

|

|

|

1,892,818 |

|

|

|

349,180 |

|

| |

|

| Total |

|

|

171,954,383 |

|

|

|

16,046,447 |

|

|

|

8,315,972 |

|

| |

|

18

Report of Independent Registered

Public Accounting Firm

To the

Shareholders and Board of Directors/Trustees

Nuveen Municipal Value Fund, Inc., Nuveen AMT-Free Municipal Value Fund,

and Nuveen Municipal Income Fund, Inc.:

Opinion on the Financial Statements

We have audited the accompanying statements of assets and liabilities of Nuveen Municipal Value Fund, Inc., Nuveen AMT-Free

Municipal Value Fund, and Nuveen Municipal Income Fund, Inc. (the Funds), including the portfolios of investments, as of October 31, 2023, the related statements of operations for the year then ended, the statements of changes in net assets for

each of the years in the two-year period then ended, and the related notes (collectively, the financial statements) and the financial highlights for each of the years in the

five-year period then ended. In our opinion, the financial statements and financial highlights present fairly, in all material respects, the financial position of the Funds as of October 31, 2023, the

results of their operations for the year then ended, the changes in their net assets for each of the years in the two-year period then ended, and the financial highlights for each of the years in the five-year period then ended, in conformity with U.S. generally accepted accounting principles.

Basis for Opinion

These financial statements and financial highlights are the responsibility of the Funds’ management. Our responsibility is to express an opinion on these financial

statements and financial highlights based on our audits. We are a public accounting firm registered with the Public Company Accounting Oversight Board (United States) (PCAOB) and are required to be independent with respect to the Funds in accordance

with the U.S. federal securities laws and the applicable rules and regulations of the Securities and Exchange Commission and the PCAOB.

We conducted our audits in

accordance with the standards of the PCAOB. Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements and financial highlights are free of material misstatement, whether due to

error or fraud. Our audits included performing procedures to assess the risks of material misstatement of the financial statements and financial highlights, whether due to error or fraud, and performing procedures that respond to those risks. Such

procedures included examining, on a test basis, evidence regarding the amounts and disclosures in the financial statements and financial highlights. Such procedures also included confirmation of securities owned as of October 31, 2023, by

correspondence with custodians and brokers; when replies were not received from brokers, we performed other auditing procedures. Our audits also included evaluating the accounting principles used and significant estimates made by management, as well

as evaluating the overall presentation of the financial statements and financial highlights. We believe that our audits provide a reasonable basis for our opinion.

/s/ KPMG LLP

We have served as the auditor of one or more Nuveen

investment companies since 2014.

Chicago, Illinois

December 28, 2023

19

|

|

|

| NUV |

|

Nuveen Municipal Value Fund, Inc. |

| |

Portfolio of Investments October 31, 2023 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Principal

Amount (000) |

|

|

|

|

Description (a) |

|

|

Optional Call

Provisions (b) |

|

|

|

Value |

|

|

|

|

|

|

|

LONG-TERM INVESTMENTS - 99.5% |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

MUNICIPAL BONDS - 99.5% |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Alabama - 0.2% |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Birmingham Airport Authority, Alabama, Airport Revenue Bonds, Series 2020: |

|

|

|

|

|

|

|

|

| $ |

255 |

|

|

|

|

4.000%, 7/01/39 - BAM Insured |

|

|

7/30 at 100.00 |

|

|

$ |

232,507 |

|

| |

225 |

|

|

|

|

4.000%, 7/01/40 - BAM Insured |

|

|

7/30 at 100.00 |

|

|

|

203,945 |

|

|

|

|

|

|

| |

3,805 |

|

|

(c) |

|

Homewood, Alabama, General Obligation Warrants, Series 2016, 5.000%, 9/01/36, (Pre-refunded 9/01/26) |

|

|

9/26 at 100.00 |

|

|

|

3,938,059 |

|

|

|

|

|

|

|

Total Alabama |

|

|

|

|

|

|

4,374,511 |

|

|

|

|

|

|

|

|

|

|

|

|

Alaska - 0.4% |

|

|

|

|

|

|

|

|

|

|

|

|

|

| |

9,750 |

|

|

|

|

Anchorage, Alaska, Solid Waste Services Revenue Bonds, Refunding Series 2022A, 4.000%, 11/01/52 |

|

|

11/32 at 100.00 |

|

|

|

8,021,167 |

|

|

|

|

|

|

| |

110 |

|

|

|

|

Northern Tobacco Securitization Corporation, Alaska, Tobacco Settlement Asset-Backed

Bonds, Senior Series 2021A Class 1, 4.000%, 6/01/50 |

|

|

6/31 at 100.00 |

|

|

|

88,132 |

|

|

|

|

|

|

|

Total Alaska |

|

|

|

|

|

|

8,109,299 |

|

|

|

|

|

|

|

|

|

|

|

|

Arizona - 1.0% |

|

|

|

|

|

|

|

|

|

|

|

|

|

| |

1,915 |

|

|

|

|

Chandler Industrial Development Authority, Arizona, Industrial Development Revenue Bonds, Intel Corporation Project, Series 2019,

5.000%, 6/01/49, (AMT), (Mandatory Put 6/03/24) |

|

|

6/24 at 100.00 |

|

|

|

1,914,386 |

|

|

|

|

|

|

| |

2,935 |

|

|

|

|

Phoenix Civic Improvement Corporation, Arizona, Airport Revenue Bonds, Senior Lien Series 2017A, 5.000%, 7/01/35 |

|

|

7/27 at 100.00 |

|

|

|

3,010,385 |

|

|

|

|

|

|

| |

780 |

|

|

|

|

Phoenix Civic Improvement Corporation, Arizona, Excise Tax Revenue Bonds, Subordinate Lien Series 2020A, 4.000%, 7/01/45 |

|

|

7/30 at 100.00 |

|

|

|

669,283 |

|

|

|

|

|

|

| |

2,590 |

|

|

|

|

Phoenix Civic Improvement Corporation, Arizona, Water System Revenue Bonds, Junior Lien Series 2021A, 5.000%, 7/01/45 |

|

|

7/31 at 100.00 |

|

|

|

2,645,395 |

|

|

|

|

|

|

| |

2,175 |

|

|

|

|

Pima County Industrial Development Authority, Arizona, Revenue Bonds, Tucson Medical Center, Series 2021A, 4.000%,

4/01/46 |

|

|

4/31 at 100.00 |

|

|

|

1,728,821 |

|

|

|

|

|

|

| |

5,600 |

|

|

|

|

Salt Verde Financial Corporation, Arizona, Senior Gas Revenue Bonds, Citigroup Energy Inc Prepay Contract Obligations, Series

2007, 5.000%, 12/01/37 |

|

|

No Opt. Call |

|

|

|

5,436,116 |

|

|

|

|

|

|

|

|

|

|

|

|

Tucson, Arizona, Water System Revenue Bonds, Refunding Series 2017: |

|

|

|

|

|

|

|

|

| |

1,000 |

|

|

|

|

5.000%, 7/01/34 |

|

|

7/27 at 100.00 |

|

|

|

1,034,891 |

|

| |

750 |

|

|

|

|

5.000%, 7/01/35 |

|

|

7/27 at 100.00 |

|

|

|

774,102 |

|

|

|

|

|

|

|

Total Arizona |

|

|

|

|

|

|

17,213,379 |

|

|

|

|

|

|

|

|

|

|

|

|

California - 6.5% |

|

|

|

|

|

|

|

|

|

|

|

|

|

| |

405 |

|

|

|

|

California County Tobacco Securitization Agency, Tobacco Settlement Asset-Backed Bonds, Los Angeles County Securitization

Corporation, Series 2020A, 4.000%, 6/01/49 |

|

|

6/30 at 100.00 |

|

|

|

329,753 |

|

|

|

|

|

|

| |

1,250 |

|

|

|

|

California County Tobacco Securitization Agency, Tobacco Settlement Asset-Backed Bonds, Sonoma County Tobacco Securitization

Corporation, Series 2020A, 4.000%, 6/01/49 |

|

|

12/30 at 100.00 |

|

|

|

1,017,757 |

|

|

|

|

|

|

| |

4,080 |

|

|

(c) |

|

California Health Facilities Financing Authority, California, Revenue Bonds, Sutter Health, Refunding Series 2016B, 5.000%,

11/15/46, (Pre-refunded 11/15/26) |

|

|

11/26 at 100.00 |

|

|

|

4,250,951 |

|

|

|

|

|

|

| |

5,920 |

|

|

|

|

California Health Facilities Financing Authority, California, Revenue Bonds, Sutter Health, Series 2018A, 5.000%,

11/15/48 |

|

|

11/27 at 100.00 |

|

|

|

5,836,000 |

|

20

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Principal

Amount (000) |

|

|

|

|

Description (a) |

|

|

Optional Call

Provisions (b) |

|

|

|

Value |

|

|

|

|

|

|

|

|

|

|

|

|

California (continued) |

|

|

|

|

|

|

|

|

|

|

|

|

|

| $ |

1,650 |

|

|

|

|

California Health Facilities Financing Authority, Revenue Bonds, Children’s Hospital Los Angeles, Series 2017A, 5.000%,

8/15/35 |

|

|

8/27 at 100.00 |

|

|

$ |

1,660,904 |

|

|

|

|

|

|

|

|

|

|

|

|

California Municipal Finance Authority, Revenue Bonds, Linxs APM Project, Senior Lien Series 2018A: |

|

|

|

|

|

|

|

|

| |

1,635 |

|

|

|

|

5.000%, 12/31/43, (AMT) |

|

|

6/28 at 100.00 |

|

|

|

1,547,046 |

|

| |

3,495 |

|

|

|

|

5.000%, 12/31/47, (AMT) |

|

|

6/28 at 100.00 |

|

|

|

3,273,156 |

|

|

|

|

|

|

| |

1,000 |

|

|

|

|

California Municipal Finance Authority, Revenue Bonds, Linxs APM Project, Senior Lien Series 2018B, 5.000%, 6/01/48,

(AMT) |

|

|

6/28 at 100.00 |

|

|

|

933,003 |

|

|

|

|

|

|

| |

2,290 |

|

|

|

|

California Pollution Control Financing Authority, Water Furnishing Revenue Bonds, San Diego County Water Authoriity Desalination

Project Pipeline, Refunding Series 2019, 5.000%, 7/01/39, 144A |

|

|

1/29 at 100.00 |

|

|

|

2,260,481 |

|

|

|

|

|

|

| |

1,625 |

|

|

(c) |

|

California State Public Works Board, Lease Revenue Bonds, Various Capital Projects, Series 2013I, 5.000%, 11/01/38, (Pre-refunded 1/02/24) |

|

|

1/24 at 100.00 |

|

|

|

1,628,422 |

|

|

|

|

|

|

| |

3,500 |

|

|

|

|

California Statewide Communities Development Authority, California, Revenue Bonds, Loma Linda University Medical Center, Series

2016A, 5.000%, 12/01/46, 144A |

|

|

6/26 at 100.00 |

|

|

|

3,092,843 |

|

|

|

|

|

|

| |

4,505 |

|

|

|

|

Covina-Valley Unified School District, Los Angeles County, California, General Obligation Bonds, Series 2003B, 0.000%, 6/01/28 -

FGIC Insured |

|

|

No Opt. Call |

|

|

|

3,683,488 |

|

|

|

|

|

|

| |

5,700 |

|

|

|

|

East Bay Municipal Utility District, Alameda and Contra Costa Counties, California, Water System Revenue Bonds, Green Series

2017A, 5.000%, 6/01/45 |

|

|

6/27 at 100.00 |

|

|

|

5,806,107 |

|

|

|

|

|

|

| |

2,180 |

|

|

(d) |

|

Foothill/Eastern Transportation Corridor Agency, California, Toll Road Revenue Bonds, Refunding Series 2013A, 0.000%,

1/15/42 |

|

|

1/31 at 100.00 |

|

|

|

2,456,142 |

|

|

|

|

|

|

|

|

|

|

|

|

Fresno, California, Airport Revenue Bonds, Series 2023A: |

|

|

|

|

|

|

|

|

| |

1,000 |

|

|

|

|

5.000%, 7/01/48 - BAM Insured, (AMT) |

|

|

7/33 at 100.00 |

|

|

|

960,234 |

|

| |

1,000 |

|

|

|

|

5.000%, 7/01/53 - BAM Insured, (AMT) |

|

|

7/33 at 100.00 |

|

|

|

947,968 |

|

|

|

|

|

|

| |

49,020 |

|

|

|

|

Golden State Tobacco Securitization Corporation, California, Tobacco Settlement Asset-Backed Bonds, Capital Appreciation Series 2021B-2, 0.000%, 6/01/66 |

|

|

12/31 at 27.75 |

|

|

|

4,020,733 |

|

|

|

|

|

|

| |

345 |

|

|

|

|

Golden State Tobacco Securitization Corporation, California, Tobacco Settlement Asset-Backed Revenue Bonds, Series 2022A-1, 5.000%, 6/01/51 |

|

|

12/31 at

100.00 |

|

|

|

344,986 |

|

|

|

|

|

|

| |

2,780 |

|

|

|

|

Los Angeles Department of Airports, California, Revenue Bonds, Los Angeles International Airport, Refunding Subordinate Series

2022I, 5.000%, 5/15/48 |

|

|

11/31 at

100.00 |

|

|

|

2,835,235 |

|

|

|

|

|

|

| |

2,725 |

|

|

|

|

Los Angeles Department of Water and Power, California, Water System Revenue Bonds, Series 2023A, 5.250%, 7/01/53 |

|

|

7/33 at 100.00 |

|

|

|

2,870,152 |

|

|

|

|

|

|

| |

2,555 |

|

|

|

|