false

N-2

0000786035

0000786035

2023-01-01

2023-12-31

0000786035

ASG:InvestmentAndMarketRiskMember

2023-01-01

2023-12-31

0000786035

ASG:MarketDiscountRiskMember

2023-01-01

2023-12-31

0000786035

ASG:CommonStockRiskMember

2023-01-01

2023-12-31

0000786035

ASG:ManagementRiskMember

2023-01-01

2023-12-31

0000786035

ASG:GrowthStockRiskMember

2023-01-01

2023-12-31

0000786035

ASG:SmallAndMidCapStockRiskMember

2023-01-01

2023-12-31

0000786035

ASG:ForeignSecuritiesRiskMember

2023-01-01

2023-12-31

0000786035

ASG:TaxRiskMember

2023-01-01

2023-12-31

0000786035

ASG:InflationRiskMember

2023-01-01

2023-12-31

0000786035

ASG:DeflationRiskMember

2023-01-01

2023-12-31

0000786035

ASG:MarketDisruptionAndGeopoliticalRiskMember

2023-01-01

2023-12-31

0000786035

ASG:LegislationAndRegulatoryRiskMember

2023-01-01

2023-12-31

iso4217:USD

xbrli:shares

iso4217:USD

xbrli:shares

xbrli:pure

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number: 811-04537

Liberty All-Star Growth Fund, Inc.

(Exact name of registrant as specified in charter)

1290 Broadway, Suite 1000, Denver, Colorado

80203

(Address of principal executive offices) (Zip code)

Sareena Khwaja-Dixon, Esq.

ALPS Fund Services, Inc.

1290 Broadway, Suite 1000

Denver, Colorado 80203

(Name and address of agent for service)

Registrant’s telephone number, including

area code: 303-623-2577

Date of fiscal year end: December 31

Date of reporting period: January 1, 2023 -

December 31, 2023

Item 1. Report to Stockholders.

(a)

Contents

| |

1 |

|

President’s Letter |

| |

6 |

|

Unique Fund Attributes |

| |

8 |

|

Table of Distributions, Rights Offerings and Distribution Policy |

| |

9 |

|

Investment Growth |

| |

10 |

|

Stock Changes in the Quarter |

| |

11 |

|

Top 20 Holdings and Economic Sectors |

| |

12 |

|

Investment Managers/Portfolio Characteristics |

| |

13 |

|

Manager Roundtable |

| |

18 |

|

Schedule of Investments |

| |

24 |

|

Statement of Assets and Liabilities |

| |

25 |

|

Statement of Operations |

| |

26 |

|

Statements of Changes in Net Assets |

| |

28 |

|

Financial Highlights |

| |

30 |

|

Notes to Financial Statements |

| |

40 |

|

Report of Independent Registered Public Accounting Firm |

| |

41 |

|

Automatic Dividend Reinvestment and Direct Purchase Plan |

| |

43 |

|

Additional Information |

| |

44 |

|

Directors and Officers |

| |

48 |

|

Board Consideration of the Renewal of the Fund Management & Portfolio Management Agreements |

| |

53 |

|

Summary of Updated Information Regarding the Fund |

| |

58 |

|

Privacy Policy |

| |

60 |

|

Description of Lipper Benchmark and Market Indices |

| Inside Back Cover: Fund Information |

A SINGLE INVESTMENT...

A DIVERSIFIED GROWTH PORTFOLIO

A single fund that offers:

| · | A diversified, multi-managed portfolio of small-, mid- and large-cap growth stocks |

| · | Exposure to many of the industries that make the U.S. economy one of the world’s most dynamic |

| · | Access to institutional quality investment managers |

| · | Objective and ongoing manager evaluation |

| · | Active portfolio rebalancing |

| · | A quarterly fixed distribution policy |

| · | Actively managed, exchange-traded, closed-end fund listed on the New York Stock Exchange (ticker symbol: ASG) |

LIBERTY ALL-STAR® GROWTH FUND, INC.

| Liberty All-Star®

Growth Fund |

President’s Letter |

(Unaudited)

| Fellow Shareholders: |

February 2024 |

Steady economic data, moderating inflation, improved

corporate earnings and the prospect of lower interest rates in 2024 propelled equity markets higher in 2023, overcoming hurdles that ranged

from regional bank failures domestically to armed conflicts abroad. At year’s end, respective annual returns for the S&P 500®

Index, the Dow Jones Industrial Average (DJIA) and the NASDAQ Composite Index were 26.29 percent, 16.18 percent and 44.64 percent, respectively.

The year’s solid results were a welcome turnaround from 2022, when all three indices tumbled into negative territory.

Throughout the year investors’ primary focus

was on the Federal Reserve and its tightrope walk of combatting inflation without tipping the economy into recession. In this effort the

Fed raised the benchmark federal funds rate seven times in 2022 and four more times in 2023. The last increase, in July, brought the rate

to a range of 5.25 to 5.50 percent—the highest in 22 years. Despite the rising rate regime, U.S. stocks showed resilience, the S&P

500® returning 16.89 percent for the first six months of the year.

The strong six-month return captured the year’s

recurring theme: resilience. While January got the year off to a good start, the Fed raised rates in February while March was upended

by the collapse of Silicon Valley Bank, the second-biggest bank failure in U.S. history. Although another failure, Signature Bank, would

follow, forceful action by regulators staunched a systemic banking crisis. The ensuing late March through July period was highly positive

for stocks, which were buoyed by “The Magnificent Seven1,” investor euphoria over artificial intelligence (AI),

earnings that exceeded expectations and data indicating that inflation was easing.

As August began, that period came to an abrupt

end: U.S. sovereign debt was downgraded, political infighting roiled the Nation’s Capital and consumer prices crept back up, breaking

a string of monthly declines. In announcing the July rate increase Fed Chair Jerome Powell made it clear that the Fed would continue to

monitor data and act to raise rates further if warranted. His remarks— along with surging Treasury bond yields, strong job creation

and low unemployment, soft retail sales, and the Israeli-Hamas war—raised the specter of a “hard landing” for the economy

in 2024— if not an outright recession. The result for stocks: three straight months of decline culminating in the poorest October

since 2020.

Once again, however, stocks reversed course and

surged over the last two months of the year. A key catalyst was Treasury yields: Rising during the third quarter they siphoned money out

of stocks but falling over the last two months they made stocks more attractive. In addition, consumer and producer prices eased, consumer

confidence ticked higher, and the picture for labor—both employment levels and wages—appeared sustainable. More importantly

for stocks, these factors allowed the Fed to assume a more accommodative interest rate posture. For the fourth quarter, the S&P 500®

returned 11.69 percent, the DJIA gained 13.09 percent and the NASDAQ Composite advanced 13.79 percent.

| 1 | Those stocks are Alphabet, Amazon, Apple, Meta Platforms, Microsoft,

NVIDIA and Tesla. |

| Annual Report | December 31, 2023 |

1 |

| Liberty All-Star® Growth Fund |

President’s Letter |

(Unaudited)

Among the 11 S&P 500® sectors,

information technology led the way with an annual return of 60.79 percent, followed by communication services and consumer discretionary,

returning 56.37 percent and 43.19 percent, respectively. These three sectors accounted for the majority of the S&P 500®

return (87 percent) while returns for each of the remaining eight sectors were all less than the index return, including two sectors that

were negative: utilities (-7.09 percent) and energy (-1.30 percent).

Among the capitalization ranges represented in

the Fund, large-cap growth produced higher annual returns than did mid- and small-cap growth. The large-cap Russell 1000®

Growth Index returned 42.68 percent; the Russell Midcap® Growth Index returned 25.87 percent; and the small-cap Russell

2000® Growth Index trailed with a return of 18.66 percent.

Liberty All-Star® Growth Fund

Although returns for the fourth quarter were in

line with most benchmarks, for the full year Liberty All-Star® Growth Fund returns generally lagged. For the year,

the Fund returned 19.37 percent when shares are valued at net asset value (NAV) with dividends reinvested and 16.28 percent when shares

are valued at market price with dividends reinvested. (Fund returns are net of expenses.) Both measures of the Fund’s annual return

trailed the 32.92 percent gain of its primary benchmark, the Lipper Multi-Cap Growth Mutual Fund Average. Fund returns topped that of

the DJIA, but otherwise trailed widely followed equity market benchmarks.

The Fund’s fourth quarter NAV return was

12.28 percent with dividends reinvested while the market price return with dividends reinvested was 8.94 percent. The NAV return topped

the S&P 500® return of 11.69 percent but trailed other benchmarks.

Over the year, the Fund shared an uphill climb

with many growth equity investment vehicles. This challenge can be illustrated by the Russell Growth Average. This gauge of performance

returned 30.38 percent for the year; yet the median stock in the average realized a return of just 6.32 percent and a full 71 percent

were below the return of the average. The better performance of benchmarks such as this can be attributed largely to their higher weighting

of information technology stocks, especially those companies seen as leaders in the emerging AI field. Moreover, rising interest rates—a

drag on returns in general—had a greater effect on small- and mid-cap stocks that comprise roughly two-thirds of Fund assets; as

interest rates eased somewhat in the fourth quarter the market broadened and the Fund was able to make up ground.

Relative to their underlying NAV, Fund shares

traded at a discount over the course of the year. For the year, the discount ranged from -2.8 percent to -8.4 percent. In the fourth quarter,

the range was a tighter -4.9 percent to -8.4 percent.

In accordance with the Fund’s distribution

policy, the Fund paid a distribution of $0.10 to shareholders during the fourth quarter, bringing the total distributed to shareholders

since 1997, when the distribution policy commenced, to $16.93 per share. The Fund’s distribution policy is a major component of

the Fund’s total return, and we continue to emphasize that shareholders should include these distributions when determining the

total return on their investment in the Fund.

| Liberty All-Star® Growth Fund |

President’s Letter |

(Unaudited)

Once again in this Annual Report, we present a

Q&A session with the Fund’s three growth style investment managers, seeking to provide shareholders with greater insights into

their philosophy, style and strategy. This year we asked about areas of opportunity, managing through uncertainty and the risk/reward

characteristics of growth stocks in their capitalization range. We hope you find this feature, beginning on page 13, to be informative

and useful.

Despite double-digit returns for the year, it

was a challenging environment for the Fund’s diversified multi-cap growth strategy. You have doubtless heard various investment

authorities extol the virtues of diversification; at the moment we are in a period when the opposite—concentration— has produced

exceptional results. The Fund is focused on the long term, and I am encouraged by its track record over longer periods. Thus, we remain

committed to our structure as a diversified, multi-managed growth equity investment for long-term investors. We thank you for your confidence

in the Fund and pledge our best efforts on your behalf going forward.

Sincerely,

Mark T. Haley, CFA

President

Liberty All-Star® Growth Fund, Inc.

The views expressed in the President’s Letter,

Unique Fund Attributes and Manager Roundtable reflect the current views of the respective parties and may not reflect their views on the

date this report is first published or anytime thereafter. These views are not guarantees of future performance and involve certain risks,

uncertainties and assumptions that are difficult to predict, so actual outcomes and results may differ significantly from the views expressed.

These views are subject to change at any time based upon economic, market or other conditions, and the respective parties disclaim any

responsibility to update such views. These views may not be relied on as investment advice and, because investment decisions for the Fund

are based on numerous factors, may not be relied on as an indication of trading intent. References to specific company securities should

not be construed as a recommendation or investment advice.

| Annual Report | December 31, 2023 |

3 |

| Liberty All-Star® Growth Fund |

President’s Letter |

(Unaudited)

FUND STATISTICS AND SHORT-TERM PERFORMANCE

PERIODS ENDED DECEMBER 31, 2023

FUND STATISTICS:

| Net Asset Value (NAV) |

$5.75 |

| Market Price |

$5.28 |

| Discount |

-8.2% |

| |

Quarter |

2023 |

| Distributions* |

$0.10 |

$0.43 |

| Market Price Trading Range |

$4.47 to $5.40 |

$4.47 to $5.71 |

| Discount Range |

-4.9% to -8.4% |

-2.8% to -8.4% |

PERFORMANCE:

| Shares Valued at NAV with Dividends Reinvested |

12.28% |

19.37% |

| Shares Valued at Market Price with Dividends Reinvested |

8.94% |

16.28% |

| Dow Jones Industrial Average |

13.09% |

16.18% |

| Lipper Multi-Cap Growth Mutual Fund Average |

13.91% |

32.92% |

| NASDAQ Composite Index |

13.79% |

44.64% |

| Russell Growth Average |

13.80% |

30.38% |

| S&P 500® Index |

11.69% |

26.29% |

| * | All 2023

distributions consist of return of capital. A breakdown of each 2023 distribution for federal income tax purposes can be found in the

table on page 43. |

| Liberty All-Star® Growth Fund |

President’s Letter |

(Unaudited)

LONG-TERM PERFORMANCE SUMMARY

AND DISTRIBUTIONS PERIODS ENDED DECEMBER 31, 2023 |

ANNUALIZED RATES OF RETURN |

| 3 YEARS |

5 YEARS |

10 YEARS |

| |

|

|

|

| LIBERTY ALL-STAR® GROWTH FUND, INC. |

|

|

|

| |

|

|

|

| Distributions |

$1.95 |

$3.04 |

$5.38 |

| Shares Valued at NAV with Dividends Reinvested |

-0.91% |

13.47% |

10.32% |

| Shares Valued at Market Price with Dividends Reinvested |

-4.56% |

14.22% |

9.94% |

| Dow Jones Industrial Average |

9.38% |

12.47% |

11.08% |

| Lipper Multi-Cap Growth Mutual Fund Average |

-0.16% |

14.01% |

10.82% |

| NASDAQ Composite Index |

6.04% |

18.75% |

14.80% |

| Russell Growth Average |

2.80% |

14.61% |

11.26% |

| S&P 500® Index |

10.00% |

15.69% |

12.03% |

Performance returns for the Fund are calculated

assuming all distributions are reinvested at actual reinvestment prices and all primary rights in the Fund’s rights offerings were exercised.

Returns are net of management fees and other Fund expenses.

The returns shown for the Lipper Multi-Cap Growth

Mutual Fund Average are based on open-end mutual funds’ total returns, which include dividends, and are net of fund expenses. Returns

for the unmanaged Dow Jones Industrial Average, NASDAQ Composite Index, the Russell Growth Average and the S&P 500®

Index are total returns, including dividends. A description of the Lipper benchmark and the market indices can be found on page 60.

Past performance cannot predict future results.

Performance will fluctuate with market conditions. Current performance may be lower or higher than the performance data shown. Performance

information does not reflect the deduction of taxes that shareholders would pay on Fund distributions or the sale of Fund shares. An investment

in the Fund involves risk, including loss of principal.

Closed-end funds raise money in an initial public

offering and shares are listed and traded on an exchange. Open-end mutual funds continuously issue and redeem shares at net asset value.

Shares of closed-end funds frequently trade at a discount to net asset value. The price of the Fund’s shares is determined by a

number of factors, several of which are beyond the control of the Fund. Therefore, the Fund cannot predict whether its shares will trade

at, below or above net asset value.

| Annual Report | December 31, 2023 |

5 |

| Liberty All-Star® Growth Fund |

Unique Fund Attributes |

(Unaudited)

UNIQUE ATTRIBUTES OF Liberty All-Star®

Growth Fund

Several attributes help to make the Fund a core equity holding for

investors seeking a diversified growth portfolio, income and the potential for long-term appreciation.

|

MULTI-MANAGEMENT FOR INDIVIDUAL INVESTORS |

| |

Large institutional investors have traditionally employed multiple investment managers. With three investment managers investing across the full capitalization range of growth stocks, the Fund brings multi-management to individual investors. |

| |

|

|

REAL-TIME TRADING AND LIQUIDITY |

| |

The Fund has a fixed number of shares that trade on the New York Stock Exchange and other exchanges. Share pricing is continuous—not just end-of-day, as it is with open-end mutual funds. Fund shares offer immediate liquidity, there are no annual sales fees and can often be traded commission free. |

| Liberty All-Star® Growth Fund |

Unique Fund Attributes |

(Unaudited)

|

ACCESS TO INSTITUTIONAL MANAGERS |

| |

The Fund’s investment managers invest primarily for pension funds, endowments, foundations and other institutions. Because institutional managers are closely monitored by their clients, they tend to be more disciplined and consistent in their investment process. |

| |

|

|

MONITORING AND REBALANCING |

| |

ALPS Advisors continuously monitors these investment managers to ensure that they are performing as expected and adhering to their style and strategy, and will replace the managers when warranted. Periodic rebalancing maintains the Fund’s structural integrity and is a well-recognized investment discipline. |

| |

|

|

ALIGNMENT AND OBJECTIVITY |

| |

Alignment with shareholders’ best interests and objective decision-making help to ensure that the Fund is managed openly and equitably. In addition, the Fund is governed by a Board of Directors that is elected by and responsible to shareholders. |

| |

|

|

DISTRIBUTION POLICY |

| |

Since 1997, the Fund has followed a policy of paying annual distributions on its shares at a rate that approximates historical equity market returns. The current annual distribution rate is 8 percent of the Fund’s net asset value (paid quarterly at 2 percent per quarter), providing a systematic mechanism for distributing funds to shareholders. |

| Annual Report | December 31, 2023 |

7 |

| Liberty All-Star® Growth Fund |

Table of Distributions,

Rights Offerings and Distribution Policy |

(Unaudited)

| |

|

RIGHTS OFFERINGS |

| YEAR |

PER SHARE DISTRIBUTIONS |

MONTH COMPLETED |

SHARES NEEDED TO PURCHASE ONE ADDITIONAL SHARE |

SUBSCRIPTION PRICE |

| 1997 |

$1.24 |

|

|

|

| 1998 |

1.35 |

July |

10 |

$12.41 |

| 1999 |

1.23 |

|

|

|

| 2000 |

1.34 |

|

|

|

| 2001 |

0.92 |

September |

8 |

6.64 |

| 2002 |

0.67 |

|

|

|

| 2003 |

0.58 |

September |

81 |

5.72 |

| 2004 |

0.63 |

|

|

|

| 2005 |

0.58 |

|

|

|

| 2006 |

0.59 |

|

|

|

| 2007 |

0.61 |

|

|

|

| 2008 |

0.47 |

|

|

|

| 20092 |

0.24 |

|

|

|

| 2010 |

0.25 |

|

|

|

| 2011 |

0.27 |

|

|

|

| 2012 |

0.27 |

|

|

|

| 2013 |

0.31 |

|

|

|

| 2014 |

0.33 |

|

|

|

| 20153 |

0.77 |

|

|

|

| 2016 |

0.36 |

|

|

|

| 2017 |

0.42 |

|

|

|

| 2018 |

0.46 |

November |

3 |

4.81 |

| 2019 |

0.46 |

|

|

|

| 2020 |

0.63 |

March |

5 |

4.34 |

| 2021 |

1.02 |

June |

51 |

8.21 |

| 2022 |

0.50 |

|

|

|

| 2023 |

0.43 |

|

|

|

| Total |

$16.93 |

|

|

|

| 1 | The number of shares offered was increased by an additional 25 percent

to cover a portion of the over-subscription requests. |

| 2 | Effective with the second quarter distribution, the annual distribution

rate was changed from 10 percent to 6 percent. |

| 3 | Effective with the second quarter distribution, the annual distribution

rate was changed from 6 percent to 8 percent. |

DISTRIBUTION POLICY

The current policy is to pay distributions on

its shares totaling approximately 8 percent of its net asset value per year, payable in four quarterly installments of 2 percent of the

Fund’s net asset value at the close of the New York Stock Exchange on the Friday prior to each quarterly declaration date. Sources

of distributions to shareholders may include ordinary dividends, long-term capital gains and return of capital. The actual amounts and

sources of the amounts for tax reporting purposes will depend upon the Fund’s investment experience during its fiscal year and may

be subject to changes based on tax regulations. If a distribution includes anything other than net investment income, the Fund provides

a Section 19(a) notice of the best estimate of its distribution sources at that time. These estimates may not match the final tax characterization

(for the full year’s distributions) contained in shareholder 1099-DIV forms after the end of the year. If the Fund’s ordinary

dividends and long-term capital gains for any year exceed the amount distributed under the distribution policy, the Fund may, in its discretion,

retain and not distribute capital gains and pay income tax thereon to the extent of such excess.

| Liberty All-Star® Growth Fund |

Investment Growth |

(Unaudited)

GROWTH OF A HYPOTHETICAL $10,000 INVESTMENT

The graph below illustrates the growth of a hypothetical

$10,000 investment assuming the pur-chase of shares of common stock at the closing market price (NYSE: ASG) of $9.25 on December 31, 1996,

and tracking its progress through December 31, 2023. For certain information, it also assumes that a shareholder exercised all primary

rights in the Fund’s rights offerings (see below). This graph covers the period since the Fund commenced its distribution policy

in 1997.

|

The growth of the investment assuming all distributions were received in cash and not reinvested back into the Fund. The value of the investment under this scenario grew to $24,011 (including the December 31, 2023 value of the original investment of $5,708, plus distributions during the period of $18,303). |

| |

|

|

The additional value realized through reinvestment of all distributions. The value of the investment under this scenario grew to $75,558. |

| |

|

|

The additional value realized by exercising all primary rights in the Fund’s rights offerings. The value of the investment under this scenario grew to $120,511 excluding the cost to exercise all primary rights in the rights offerings which was $82,340. |

Past performance cannot predict future results.

Performance will fluctuate with changes in market conditions. Current performance may be lower or higher than the performance data shown.

Performance information does not reflect the deduction of taxes that shareholders would pay on Fund distributions or the sale of Fund

shares. An investment in the Fund involves risk, including loss of principal.

| Annual Report | December 31, 2023 |

9 |

| Liberty All-Star® Growth Fund |

Stock Changes in the Quarter |

December 31, 2023 (Unaudited)

The following are the largest ($2 million or more) stock changes -

both purchases and sales - that were made in the Fund’s portfolio during the fourth quarter of 2023.

| |

SHARES |

| SECURITY NAME |

PURCHASE (SALES) |

HELD AS OF 12/31/23 |

| PURCHASES |

|

|

| Brown & Brown, Inc. |

29,000 |

29,000 |

| Fabrinet |

13,000 |

13,000 |

| Novo Nordisk A/S |

34,182 |

34,182 |

| Valvoline, Inc. |

65,000 |

65,000 |

| Watts Water Technologies, Inc., Class A |

15,000 |

15,000 |

| SALES |

|

|

| Asbury Automotive Group, Inc. |

(13,000) |

0 |

| Choice Hotels International, Inc. |

(22,500) |

0 |

| Ciena Corp. |

(50,000) |

0 |

| Deckers Outdoor Corp. |

(3,500) |

5,000 |

| Flywire Corp. |

(95,919) |

72,527 |

| IDEX Corp. |

(14,000) |

0 |

| Regeneron Pharmaceuticals, Inc. |

(3,737) |

0 |

| Liberty All-Star® Growth Fund |

Top 20 Holdings and Economic Sectors |

December 31, 2023 (Unaudited)

| TOP 20 HOLDINGS* |

PERCENT OF NET ASSETS |

| SPS Commerce, Inc. |

2.74% |

| Microsoft Corp. |

2.07 |

| Amazon.com, Inc. |

1.97 |

| Progyny, Inc. |

1.85 |

| FirstService Corp. |

1.77 |

| Glaukos Corp. |

1.71 |

| ACADIA Pharmaceuticals, Inc. |

1.70 |

| Visa, Inc. |

1.66 |

| Vertex, Inc. |

1.62 |

| UnitedHealth Group, Inc. |

1.56 |

| Casella Waste Systems, Inc. |

1.52 |

| SiteOne Landscape Supply, Inc. |

1.47 |

| Danaher Corp. |

1.40 |

| S&P Global, Inc. |

1.37 |

| Transcat, Inc. |

1.32 |

| Hamilton Lane, Inc. |

1.28 |

| Canadian Pacific Kansas City, Ltd. |

1.27 |

| Inspire Medical Systems, Inc. |

1.26 |

| StepStone Group, Inc. |

1.25 |

| Crane Co. |

1.21 |

| |

32.00% |

| ECONOMIC SECTORS* |

PERCENT OF NET ASSETS |

| Health Care |

23.08% |

| Information Technology |

22.41 |

| Industrials |

16.52 |

| Financials |

12.68 |

| Consumer Discretionary |

10.52 |

| Materials |

3.69 |

| Real Estate |

3.66 |

| Communication Services |

3.03 |

| Consumer Staples |

1.58 |

| Energy |

1.41 |

| Other Net Assets |

1.42 |

| |

100.00% |

| * | Because

the Fund is actively managed, there can be no guarantee that the Fund will continue to hold securities of the indicated issuers and sectors

in the future. |

| Annual Report | December 31, 2023 |

11 |

| Liberty All-Star® Growth Fund |

Investment Managers/

Portfolio Characteristics |

(Unaudited)

THE FUND’S THREE GROWTH INVESTMENT MANAGERS

AND THE MARKET CAPITALIZATION ON WHICH EACH

FOCUSES:

ALPS Advisors, Inc., the investment advisor to

the Fund, has the ultimate authority (subject to oversight by the Board of Directors) to oversee the investment managers and recommend

their hiring, termination and replacement.

MANAGERS’ DIFFERING INVESTMENT STRATEGIES

ARE

REFLECTED IN PORTFOLIO CHARACTERISTICS

The portfolio characteristics table below is a

regular feature of the Fund’s shareholder reports. It serves as a useful tool for understanding the value of the Fund’s multi-managed

portfolio. The characteristics are different for each of the Fund’s three investment managers. These differences are a reflection

of the fact that each has a different capitalization focus and investment strategy. The shaded column highlights the characteristics of

the Fund as a whole, while the first three columns show portfolio characteristics for the Russell Smallcap, Midcap and Largecap Growth

indices. See page 60 for a description of these indices.

| |

|

|

MARKET CAPITALIZATION SPECTRUM |

|

| PORTFOLIO CHARACTERISTICS |

|

|

SMALL |

|

LARGE |

|

| AS OF DECEMBER 31, 2023 |

|

|

|

|

| |

RUSSELL GROWTH: |

|

|

|

|

| |

Smallcap Index |

Midcap Index |

Largecap Index |

Weatherbie |

Congress |

Sustainable |

Total Fund |

| Number of Holdings |

1,074 |

333 |

443 |

48 |

40 |

28 |

115* |

| Percent of Holdings in Top 10 |

7% |

14% |

51% |

50% |

31% |

45% |

19% |

| Weighted Average Market Capitalization (billions) |

$3.8 |

$28.4 |

$1,114.8 |

$4.3 |

$16.4 |

$502.8 |

$174.5 |

| Average Five-Year Earnings Per Share Growth |

18% |

17% |

21% |

15% |

21% |

15% |

18% |

| Average Five-Year Sales Per Share Growth |

11% |

15% |

16% |

11% |

12% |

13% |

12% |

| Price/Sales Ratio |

2.0x |

3.5x |

4.7x |

3.4x |

2.9x |

4.8x |

3.6x |

| Price/Book Value Ratio |

4.4x |

10.0x |

8.9x |

5.2x |

5.4x |

6.6x |

5.7x |

| * | Certain holdings are held by more than one manager. |

| Liberty All-Star® Growth Fund |

Manager Roundtable |

(Unaudited)

MANAGER ROUNDTABLE

Guiding portfolios toward the objective of

long-term returns requires a deft touch tactically while operating within the larger framework of each manager’s style, strategy

and process.

Higher inflation and rising interest rates pummeled

stocks in 2022. Entering 2023 expectations were modest. But stocks delivered a surprisingly strong year—even with the formidable

wall of worry in place—as investors looked ahead to a more hospitable environment. With change being the only constant, this was

an opportune time to query the Fund’s managers about how they are navigating through short-term uncertainty. The interview concludes

by returning to a principle of Liberty All-Star Growth Fund that is a constant regardless of market conditions: A dedication to growth

style investing across the capitalization spectrum. In this instance, the managers go inside the risk and return characteristics of their

particular approach to large-, mid- and small-cap investing. The Fund’s Investment Advisor, ALPS Advisors, serves as moderator of

the roundtable. Participating investment management firms, the portfolio manager for each and their respective capitalization focus are:

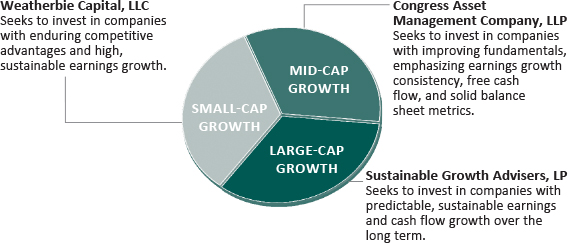

CONGRESS ASSET MANAGEMENT COMPANY, LLP

Portfolio Manager/Todd Solomon, CFA

Senior Vice President, Portfolio Manager

Capitalization Focus: Mid-Cap Growth—Congress

Asset Management’s mid-cap growth strategy focuses on established, high-quality companies that are growing earnings and generating

attractive levels of free cash flow. The firm also strives to construct portfolios with relatively low levels of volatility.

SUSTAINABLE GROWTH ADVISERS, LP

Portfolio Manager/Kishore D. Rao

Principal, Portfolio Manager

Capitalization Focus: Large-Cap Growth—Sustainable

focuses on companies that have unique characteristics that lead to a high degree of predictability, strong profitability and above-average

earnings and cash flow growth over the long term.

WEATHERBIE CAPITAL, LLC

Portfolio Manager/H. George Dai, Ph.D.

Chief Investment Officer, Senior Portfolio Manager

Capitalization Focus: Small-Cap Growth—Weatherbie

practices a small capitalization growth investment style focusing on high quality companies that demonstrate superior earnings growth

prospects yet are reasonably priced relative to their intrinsic value. The firm seeks to provide superior returns relative to small capitalization

growth indices over a full market cycle.

Artificial intelligence (AI) dominated the

investment headlines in 2023, but there are other emerging scientific, medical and technological innovations that hold promise for growth-oriented

investors. What themes run through your portfolio that may rise to the forefront of investors’ minds over the next 12 to 18 months?

Kishore, we’ll turn to you first.

| Annual Report | December 31, 2023 |

13 |

| Liberty All-Star® Growth Fund |

Manager Roundtable |

(Unaudited)

Rao (Sustainable – Large-Cap Growth):

While we are not thematic investors, there are several themes present in the portfolio due to our bottom-up stock selection. We have exposure

to generative artificial intelligence (AI) infrastructure providers such as NVIDIA (NVDA), which will benefit from the need for incredibly

accelerated computing capabilities, as well as Microsoft (MSFT), Alphabet (GOOG) and Amazon (AMZN), which will respond to demand for increased

cloud computing infrastructure. We also have exposure to companies that possess massive amounts of data and will use that data to better

train their Gen AI models to produce more helpful insights and processes. These include Salesforce (CRM), ServiceNow (NOW), Workday (WDAY)

and Intuit (INTU). In health care, we own Novo Nordisk (NVO), which is focused on addressing the diabetes and obesity epidemic, as well

as companies that enable biopharma research, development and manufacturing, including Danaher (DHR), Thermo Fisher Scientific (TMO) and

IQVIA Holdings (IQV).

Todd, what themes does Congress find attractive?

Solomon (Congress – Mid-Cap Growth):

AI effects could be felt beyond chip stocks in 2024. This transformative technology could aid drug discovery by cost-effectively screening

the efficacy and safety of more molecules and combinations than currently possible. This would provide a boost to research and equipment

companies. AI will also help bad actors strengthen attempts to penetrate networks and thus focus more IT budgets on security software,

which would benefit Qualys (QLYS), a portfolio holding since 2018.

Although it was passed in August 2022, the CHIPS

and Science Act’s first funding announcement of the $52 billion allotment for semiconductor manufacturing was made in December 2023.

Several large projects announced in 2022 that will be helped by the act have expected completion dates in 2024 or 2025, spreading the

increased construction benefit over several years. Entegris (ENTG), a portfolio holding since 2020, highlighted the act in its 2023 10-K.

They mentioned adding a facility in Colorado Springs to enable the company to service new fabs expected to be built in the U.S. Greater

semiconductor manufactoring should increase demand for Entegris’ advanced materials and process solutions.

George, “next big things” often

emerge from small-cap companies. What are you keeping your eye on?

Dai (Weatherbie – Small-Cap Growth):

AI headlines certainly overshadowed other themes that promise growth and innovation. Here are some others we see, with a specific example

of each:

In medical innovation Glaukos Corp. (GKOS) is

a device company that has been a pioneer in micro-invasive glaucoma surgery or “MIGS.” Glaukos is the market leader and enjoys

multiple tailwinds, the most important of which is the recent FDA approval of iDose—a drug/device combination that slowly releases

medicine into a glaucoma patient’s eyes.

In the theme of technological innovation Impinj

(PI) is an example. Impinj engages in the development and sale of radio frequency identification (RFID) solutions. Impinj’s RFID

technology—often viewed as a potential replacement for barcodes—connects everyday items to the digital world in industries

such as retail, supply chain and logistics, airlines, autos, and healthcare.

| Liberty All-Star® Growth Fund |

Manager Roundtable |

(Unaudited)

Another is the scientific innovation theme and

Kratos Defense & Security Solutions (KTOS) is a good example. Kratos designs and manufactures high performance, tactical and target

drones for the U.S. military. Around the world, the conflicts of recent years have seen traditional military engagements transformed by

drone technology. A leader in unmanned tactical aerospace technology, Kratos will see greater demand, in our view.

There are uncertainties ahead—there always

are—but 2024 may outdo the typical year: a presidential election, a divided Congress, “sticky” inflation, the business

environment, and realized and unrealized geopolitical threats … and each with its own ramifications not to mention the cross-dynamics

among them. Do these factors tend to tilt you toward a risk-off posture or mean you give more weight to macro factors than you ordinarily

would? Or are you taking an entirely bottom-up perspective and assessing each stock on its fundamentals? George, take us inside Weatherbie’s

thinking.

Dai (Weatherbie – Small-Cap Growth):

We adhere to a bottom-up investment process by which each of our holdings is selected on fundamentals, as opposed to “risk-on/off”

positioning. With that said, we do pay close attention to macro factors and how they impact each investment. Many smaller-cap growth stocks

are valued on future market share gains and may have low, or no, earnings at present. Across 2023 many of these “longer duration”

growth stocks fell as their discounted present values were impacted by higher interest rates. As a result, we currently see many quality

small-cap growth companies with the lowest valuations in years. Our research shows that the S&P Small Cap 600® Growth

Index is trading at an average price to earnings ratio of about 15. Across the last 25 years of monthly returns this P/E level has produced

a 10-year annualized return of about 13 percent.

Todd and Kishore, continue for Congress and Sustainable, please.

Solomon (Congress – Mid-Cap Growth):

Congress strives to maintain a low portfolio risk profile regardless of the market environment and the expected macroeconomic conditions.

Uncertainties always abound in capital markets, but our process is focused on considering an investment’s growth profile, margin

stability and valuation. While macro factors certainly do impact the favorability of these measures, we don’t vary the level of

scrutiny based on outlook.

We are more concerned with any potential unforeseen

market challenges as these may have a greater impact than those already identified and assumed by investors. Forecasts are often inaccurate,

and we feel real-time review of any new information and its effects is the best way to protect capital.

Rao (Sustainable – Large-Cap Growth):

While we are very aware of macroeconomic and geopolitical issues and consider them at a higher level, we do not position our portfolios

based on top-down market outlooks. We look at each company based on its merits, focusing on key business quality and growth factors, including

strong pricing power, recurring revenue streams and strong cash flow generation. This leads us to more predictable and sustainable growth

companies that often sell consumables or have subscription-based or toll-taker type business models that are less impacted by macroeconomic

volatility. As a result, our companies tend to have higher gross margins, better cash flow generation, less leverage and less earnings

variability than the index. Most importantly, they are generally less susceptible to macro-induced earnings variability and well positioned

for more uncertain environments with better downside protection than the index over time. Our focus on more predictable growth companies

affects our relative returns: The portfolio generally outperforms in gradually appreciating markets when multiples are relatively stable

but may underperform in periods favoring economically cyclical companies or expensive stocks with pronounced upward price momentum.

| Annual Report | December 31, 2023 |

15 |

| Liberty All-Star® Growth Fund |

Manager Roundtable |

(Unaudited)

True to its name, Liberty All-Star Growth Fund

concentrates on growth stocks. At the same time shareholders benefit from exposure to a well-diversified portfolio of stocks across the

capitalization range. From the perspective of a diversified growth portfolio, please discuss the risk and return characteristics that

are distinctive to your capitalization focus for the Fund. Todd, take us inside the characteristics of your mid-cap portfolio.

Solomon (Congress – Mid-Cap Growth):

We feel that mid- cap companies are often in the optimal phase of their life cycle—beyond the inherent volatility of the start-up

phase, possessing a proven business plan and able to grow faster than larger companies. Mid-caps have historically provided an attractive

mix of risk and return relative to larger and smaller peers over time. In addition, mid-cap companies derive less foreign revenues as

a percentage of total revenue than larger companies but more than small companies. This could be an opportunity to gain measured international

exposure without facing excessive currency volatility or political risk. Congress’ approach also considers diversification within

our mid-cap portfolio. We avoid oversized individual positions and industry allocations to further mute volatility.

“Mid-cap companies are often in the optimal

phase of their life cycle—beyond the inherent volatility of the start-up phase, possessing a proven business plan and able to grow

faster than larger companies.”

—Todd Solomon

(Congress – Mid-Cap Growth)

Kishore and George, do the same, please, for your respective large-cap

and small-cap growth portfolios.

Rao (Sustainable – Large-Cap

Growth): Sustainable invests in more predictable larger capitalization growth businesses with strong pricing power, recurring

revenue streams and attractive cash flow generation over the next three- to five-year period. Portfolio companies have expected

earnings growth rates ranging from the mid-single digits to high 20s with a portfolio average of about 16 percent. We also invest in

some select earlier lifecycle businesses, which offer similar characteristics as well as longer durations of growth. Portfolios are

built purely on investment opportunity and not index membership. In recent years as the index has become highly concentrated in

“The Magnificent Seven,” this approach has led our portfolios to be better diversified than those of many peers that

have embraced the index regardless of the added risk that entails. While our portfolio construction is opportunity focused, we do

set broad guidelines in terms of security, industry and sector weights to ensure proper diversification and risk control.

“Sustainable invests in more predictable

larger capitalization growth businesses with strong pricing power, recurring revenue streams and attractive cash flow generation over

the next three- to five-year period.”

—Kishore Rao

(Sustainable – Large-Cap Growth)

| Liberty All-Star® Growth Fund |

Manager Roundtable |

(Unaudited)

Dai (Weatherbie – Small-Cap Growth):

A key tenet of our investment process is finding dynamic, high quality smaller-cap growth stocks in otherwise mundane industries. These

“hidden gems” are often times shorter duration growth stocks with strong earnings and free cash flow in the near term. Beginning

in 2021—and through the Fed’s rate hike-driven market of 2022/2023—we increased the weighting in several of these positions

and are likely to maintain this incremental focus on quality into the new year.

Weatherbie growth stocks have differentiated business

models and strong competitive positions. In our view, these companies control their own destiny to a greater extent than their peers.

Looking to the year ahead, the market is currently anticipating inflation coming down, interest rates falling and fairly full valuation

in the S&P 500 and large-cap stocks in general. As mentioned, smaller-cap growth companies are trading at a discount relative to broader

indices versus historical levels. In our opinion, the highest quality, smaller-cap growth companies that actually warrant premium valuations

are poised to deliver strong results.

“Weatherbie growth stocks have differentiated business models

and strong competitive positions … these companies control their own destiny to a greater extent than their peers.”

—George Dai

(Weatherbie – Small-Cap Growth)

A great wrap-up and a great discussion, thanks

to all of you. No one can predict market movements, but you can be prepared for them. Well thought-out strategies are timeless and almost

always prove their value.

| Annual Report | December 31, 2023 |

17 |

| Liberty All-Star® Growth Fund |

Schedule of Investments |

December 31, 2023

| | |

SHARES | | |

VALUE | |

| COMMON STOCKS (98.58%) | |

| | | |

| | |

| COMMUNICATION SERVICES (3.03%) | |

| | | |

| | |

| Entertainment (1.83%) | |

| | | |

| | |

| Netflix, Inc.(a) | |

| 6,963 | | |

$ | 3,390,145 | |

| Take-Two Interactive Software, Inc.(a) | |

| 17,500 | | |

| 2,816,625 | |

| | |

| | | |

| 6,206,770 | |

| Interactive Media & Services (1.20%) | |

| | | |

| | |

| Alphabet, Inc., Class C(a) | |

| 28,879 | | |

| 4,069,918 | |

| | |

| | | |

| | |

| CONSUMER DISCRETIONARY (10.52%) | |

| | | |

| | |

| Broadline Retail (3.11%) | |

| | | |

| | |

| Amazon.com, Inc.(a) | |

| 44,169 | | |

| 6,711,038 | |

| Ollie’s Bargain Outlet Holdings, Inc.(a) | |

| 44,855 | | |

| 3,404,046 | |

| Savers Value Village, Inc.(a) | |

| 26,961 | | |

| 468,582 | |

| | |

| | | |

| 10,583,666 | |

| Distributors (0.82%) | |

| | | |

| | |

| Pool Corp. | |

| 7,000 | | |

| 2,790,970 | |

| | |

| | | |

| | |

| Hotels, Restaurants & Leisure (3.82%) | |

| | | |

| | |

| Darden Restaurants, Inc. | |

| 19,500 | | |

| 3,203,850 | |

| Planet Fitness, Inc., Class A(a) | |

| 21,168 | | |

| 1,545,264 | |

| Starbucks Corp. | |

| 30,147 | | |

| 2,894,413 | |

| Wingstop, Inc. | |

| 6,022 | | |

| 1,545,125 | |

| Yum! Brands, Inc. | |

| 29,206 | | |

| 3,816,056 | |

| | |

| | | |

| 13,004,708 | |

| Leisure Products (0.06%) | |

| | | |

| | |

| Latham Group, Inc.(a) | |

| 78,888 | | |

| 207,476 | |

| | |

| | | |

| | |

| Specialty Retail (1.73%) | |

| | | |

| | |

| Ulta Beauty, Inc.(a) | |

| 7,000 | | |

| 3,429,930 | |

| Valvoline, Inc.(a) | |

| 65,000 | | |

| 2,442,700 | |

| | |

| | | |

| 5,872,630 | |

| Textiles, Apparel & Luxury Goods (0.98%) | |

| | | |

| | |

| Deckers Outdoor Corp.(a) | |

| 5,000 | | |

| 3,342,150 | |

| | |

| | | |

| | |

| CONSUMER STAPLES (1.58%) | |

| | | |

| | |

| Consumer Staples Distribution & Retail (0.64%) | |

| | | |

| | |

| BJ’s Wholesale Club Holdings, Inc.(a) | |

| 32,500 | | |

| 2,166,450 | |

| | |

| | | |

| | |

| Household Products (0.83%) | |

| | | |

| | |

| Church & Dwight Co., Inc. | |

| 30,000 | | |

| 2,836,800 | |

See Notes to Financial Statements.

| Liberty All-Star® Growth Fund |

Schedule of Investments |

December 31, 2023

| | |

SHARES | | |

VALUE | |

| COMMON STOCKS (continued) | |

| | | |

| | |

| Personal Care Products (0.11%) | |

| | | |

| | |

| Oddity Tech, Ltd.(a) | |

| 8,254 | | |

$ | 384,059 | |

| | |

| | | |

| | |

| ENERGY (1.41%) | |

| | | |

| | |

| Energy Equipment & Services (1.41%) | |

| | | |

| | |

| ChampionX Corp. | |

| 100,000 | | |

| 2,921,000 | |

| Core Laboratories, Inc. | |

| 53,342 | | |

| 942,020 | |

| Dril-Quip, Inc.(a) | |

| 41,045 | | |

| 955,117 | |

| | |

| | | |

| 4,818,137 | |

| FINANCIALS (12.68%) | |

| | | |

| | |

| Capital Markets (6.81%) | |

| | | |

| | |

| FactSet Research Systems, Inc. | |

| 7,000 | | |

| 3,339,350 | |

| Hamilton Lane, Inc., Class A | |

| 38,449 | | |

| 4,361,655 | |

| MSCI, Inc. | |

| 7,178 | | |

| 4,060,236 | |

| Raymond James Financial, Inc. | |

| 22,500 | | |

| 2,508,750 | |

| S&P Global, Inc. | |

| 10,556 | | |

| 4,650,129 | |

| StepStone Group, Inc., Class A | |

| 133,697 | | |

| 4,255,575 | |

| | |

| | | |

| 23,175,695 | |

| Consumer Finance (1.12%) | |

| | | |

| | |

| American Express Co. | |

| 17,090 | | |

| 3,201,640 | |

| Upstart Holdings, Inc.(a)(b) | |

| 15,244 | | |

| 622,870 | |

| | |

| | | |

| 3,824,510 | |

| Financial Services (3.04%) | |

| | | |

| | |

| FleetCor Technologies, Inc.(a) | |

| 10,712 | | |

| 3,027,318 | |

| Flywire Corp.(a) | |

| 72,527 | | |

| 1,679,000 | |

| Visa, Inc., Class A | |

| 21,717 | | |

| 5,654,021 | |

| | |

| | | |

| 10,360,339 | |

| Insurance (1.71%) | |

| | | |

| | |

| Aon PLC, Class A | |

| 12,845 | | |

| 3,738,152 | |

| Brown & Brown, Inc. | |

| 29,000 | | |

| 2,062,190 | |

| | |

| | | |

| 5,800,342 | |

| HEALTH CARE (23.08%) | |

| | | |

| | |

| Biotechnology (3.02%) | |

| | | |

| | |

| ACADIA Pharmaceuticals, Inc.(a) | |

| 184,666 | | |

| 5,781,893 | |

| Natera, Inc.(a) | |

| 44,521 | | |

| 2,788,795 | |

| Ultragenyx Pharmaceutical, Inc.(a) | |

| 35,660 | | |

| 1,705,261 | |

| | |

| | | |

| 10,275,949 | |

| Health Care Equipment & Supplies (7.60%) | |

| | | |

| | |

| Cooper Cos., Inc. | |

| 7,500 | | |

| 2,838,300 | |

| Glaukos Corp.(a) | |

| 73,446 | | |

| 5,838,222 | |

| Hologic, Inc.(a) | |

| 32,500 | | |

| 2,322,125 | |

See Notes to Financial Statements.

| Annual Report | December 31, 2023 |

19 |

| Liberty All-Star® Growth Fund |

Schedule of Investments |

December 31, 2023

| | |

SHARES | | |

VALUE | |

| COMMON STOCKS (continued) | |

| | | |

| | |

| Health Care Equipment & Supplies (continued) | |

| | | |

| | |

| Inmode, Ltd.(a) | |

| 17,733 | | |

$ | 394,382 | |

| Inogen, Inc.(a) | |

| 41,696 | | |

| 228,911 | |

| Inspire Medical Systems, Inc.(a) | |

| 21,139 | | |

| 4,300,307 | |

| iRhythm Technologies, Inc.(a) | |

| 13,756 | | |

| 1,472,442 | |

| Nevro Corp.(a) | |

| 124,271 | | |

| 2,674,312 | |

| ResMed, Inc. | |

| 14,000 | | |

| 2,408,280 | |

| STERIS PLC | |

| 14,000 | | |

| 3,077,900 | |

| Tandem Diabetes Care, Inc.(a) | |

| 11,291 | | |

| 333,988 | |

| | |

| | | |

| 25,889,169 | |

| Health Care Providers & Services (4.49%) | |

| | | |

| | |

| Agiliti, Inc.(a) | |

| 112,178 | | |

| 888,450 | |

| NeoGenomics, Inc.(a) | |

| 102,552 | | |

| 1,659,291 | |

| Progyny, Inc.(a) | |

| 169,553 | | |

| 6,303,980 | |

| UnitedHealth Group, Inc. | |

| 10,065 | | |

| 5,298,921 | |

| US Physical Therapy, Inc. | |

| 12,148 | | |

| 1,131,465 | |

| | |

| | | |

| 15,282,107 | |

| Health Care Technology (0.46%) | |

| | | |

| | |

| Definitive Healthcare Corp.(a) | |

| 156,155 | | |

| 1,552,181 | |

| | |

| | | |

| | |

| Life Sciences Tools & Services (6.47%) | |

| | | |

| | |

| Bruker Corp. | |

| 35,000 | | |

| 2,571,800 | |

| Charles River Laboratories International, Inc.(a) | |

| 10,500 | | |

| 2,482,200 | |

| Danaher Corp. | |

| 20,633 | | |

| 4,773,238 | |

| IQVIA Holdings, Inc.(a) | |

| 13,863 | | |

| 3,207,621 | |

| Mettler-Toledo International, Inc.(a) | |

| 2,250 | | |

| 2,729,160 | |

| Thermo Fisher Scientific, Inc. | |

| 6,847 | | |

| 3,634,319 | |

| West Pharmaceutical Services, Inc. | |

| 7,500 | | |

| 2,640,900 | |

| | |

| | | |

| 22,039,238 | |

| Pharmaceuticals (1.04%) | |

| | | |

| | |

| Novo Nordisk A/S(c) | |

| 34,182 | | |

| 3,536,128 | |

| | |

| | | |

| | |

| INDUSTRIALS (16.52%) | |

| | | |

| | |

| Aerospace & Defense (0.99%) | |

| | | |

| | |

| AAR Corp.(a) | |

| 19,368 | | |

| 1,208,563 | |

| Cadre Holdings, Inc. | |

| 15,599 | | |

| 513,051 | |

| Kratos Defense & Security Solutions, Inc.(a) | |

| 80,770 | | |

| 1,638,824 | |

| | |

| | | |

| 3,360,438 | |

| Commercial Services & Supplies (2.96%) | |

| | | |

| | |

| Casella Waste Systems, Inc., Class A(a) | |

| 60,651 | | |

| 5,183,234 | |

| Copart, Inc. | |

| 65,000 | | |

| 3,185,000 | |

See Notes to Financial Statements.

| Liberty All-Star® Growth Fund |

Schedule of Investments |

December 31, 2023

| | |

SHARES | | |

VALUE | |

| COMMON STOCKS (continued) | |

| | | |

| | |

| Commercial Services & Supplies (continued) | |

| | | |

| | |

| Montrose Environmental Group, Inc.(a) | |

| 53,206 | | |

$ | 1,709,509 | |

| | |

| | | |

| 10,077,743 | |

| Construction & Engineering (1.70%) | |

| | | |

| | |

| EMCOR Group, Inc. | |

| 15,500 | | |

| 3,339,165 | |

| WillScot Mobile Mini Holdings Corp.(a) | |

| 55,000 | | |

| 2,447,500 | |

| | |

| | | |

| 5,786,665 | |

| Electrical Equipment (0.95%) | |

| | | |

| | |

| nVent Electric PLC | |

| 55,000 | | |

| 3,249,950 | |

| | |

| | | |

| | |

| Ground Transportation (2.96%) | |

| | | |

| | |

| Canadian Pacific Kansas City, Ltd. | |

| 54,534 | | |

| 4,311,458 | |

| RXO, Inc.(a) | |

| 78,624 | | |

| 1,828,794 | |

| Saia, Inc.(a) | |

| 9,000 | | |

| 3,943,980 | |

| | |

| | | |

| 10,084,232 | |

| Machinery (2.13%) | |

| | | |

| | |

| Crane Co. | |

| 35,000 | | |

| 4,134,900 | |

| Watts Water Technologies, Inc., Class A | |

| 15,000 | | |

| 3,125,100 | |

| | |

| | | |

| 7,260,000 | |

| Professional Services (1.77%) | |

| | | |

| | |

| Booz Allen Hamilton Holding Corp. | |

| 25,000 | | |

| 3,197,750 | |

| NV5 Global, Inc.(a) | |

| 2,121 | | |

| 235,686 | |

| Paycom Software, Inc. | |

| 12,500 | | |

| 2,584,000 | |

| | |

| | | |

| 6,017,436 | |

| Trading Companies & Distributors (3.06%) | |

| | | |

| | |

| SiteOne Landscape Supply, Inc.(a) | |

| 30,758 | | |

| 4,998,175 | |

| Transcat, Inc.(a) | |

| 41,229 | | |

| 4,507,567 | |

| Xometry, Inc., Class A(a) | |

| 25,083 | | |

| 900,730 | |

| | |

| | | |

| 10,406,472 | |

| INFORMATION TECHNOLOGY (22.41%) | |

| | | |

| | |

| Electronic Equipment, Instruments & Components (2.66%) | |

| | | |

| | |

| Fabrinet | |

| 13,000 | | |

| 2,474,290 | |

| Keysight Technologies, Inc.(a) | |

| 15,000 | | |

| 2,386,350 | |

| Novanta, Inc.(a) | |

| 7,624 | | |

| 1,283,958 | |

| Teledyne Technologies, Inc.(a) | |

| 6,500 | | |

| 2,900,885 | |

| | |

| | | |

| 9,045,483 | |

| IT Services (0.96%) | |

| | | |

| | |

| Globant SA(a) | |

| 3,673 | | |

| 874,101 | |

| Perficient, Inc.(a) | |

| 36,649 | | |

| 2,412,237 | |

| | |

| | | |

| 3,286,338 | |

See Notes to Financial Statements.

| Annual Report | December 31, 2023 |

21 |

| Liberty All-Star® Growth Fund |

Schedule of Investments |

December 31, 2023

| | |

SHARES | | |

VALUE | |

| COMMON STOCKS (continued) | |

| | | |

| | |

| Semiconductors & Semiconductor Equipment (4.37%) | |

| | | |

| | |

| Diodes, Inc.(a) | |

| 30,000 | | |

$ | 2,415,600 | |

| Entegris, Inc. | |

| 20,000 | | |

| 2,396,400 | |

| Impinj, Inc.(a) | |

| 31,340 | | |

| 2,821,540 | |

| Monolithic Power Systems, Inc. | |

| 5,500 | | |

| 3,469,290 | |

| NVIDIA Corp. | |

| 5,403 | | |

| 2,675,674 | |

| SiTime Corp.(a) | |

| 8,873 | | |

| 1,083,216 | |

| | |

| | | |

| 14,861,720 | |

| Software (14.42%) | |

| | | |

| | |

| Autodesk, Inc.(a) | |

| 16,094 | | |

| 3,918,567 | |

| Intapp, Inc.(a) | |

| 29,864 | | |

| 1,135,429 | |

| Intuit, Inc. | |

| 6,463 | | |

| 4,039,569 | |

| Microsoft Corp. | |

| 18,710 | | |

| 7,035,709 | |

| nCino, Inc.(a) | |

| 38,364 | | |

| 1,290,181 | |

| Qualys, Inc.(a) | |

| 19,000 | | |

| 3,729,320 | |

| Rapid7, Inc.(a) | |

| 6,163 | | |

| 351,907 | |

| Salesforce, Inc.(a) | |

| 13,050 | | |

| 3,433,977 | |

| ServiceNow, Inc.(a) | |

| 4,855 | | |

| 3,430,009 | |

| Sprout Social, Inc.(a) | |

| 32,211 | | |

| 1,979,044 | |

| SPS Commerce, Inc.(a) | |

| 48,054 | | |

| 9,314,787 | |

| Vertex, Inc., Class A(a) | |

| 205,162 | | |

| 5,527,064 | |

| Workday, Inc., Class A(a) | |

| 14,216 | | |

| 3,924,469 | |

| | |

| | | |

| 49,110,032 | |

| MATERIALS (3.69%) | |

| | | |

| | |

| Chemicals (2.10%) | |

| | | |

| | |

| Ecolab, Inc. | |

| 20,326 | | |

| 4,031,662 | |

| Sherwin-Williams Co. | |

| 9,997 | | |

| 3,118,064 | |

| | |

| | | |

| 7,149,726 | |

| Containers & Packaging (1.59%) | |

| | | |

| | |

| Avery Dennison Corp. | |

| 15,000 | | |

| 3,032,400 | |

| Ball Corp. | |

| 41,432 | | |

| 2,383,169 | |

| | |

| | | |

| 5,415,569 | |

| REAL ESTATE (3.66%) | |

| | | |

| | |

| Real Estate Management & Development (1.77%) | |

| | | |

| | |

| FirstService Corp. | |

| 37,156 | | |

| 6,022,616 | |

| | |

| | | |

| | |

| Residential REITs (0.76%) | |

| | | |

| | |

| Sun Communities, Inc. | |

| 19,500 | | |

| 2,606,175 | |

See Notes to Financial Statements.

| Liberty All-Star® Growth Fund |

Schedule of Investments |

December 31, 2023

| | |

SHARES | | |

VALUE | |

| COMMON STOCKS (continued) | |

| | | |

| | |

| Specialized REITs (1.13%) | |

| | | |

| | |

| Equinix, Inc. | |

| 4,770 | | |

$ | 3,841,710 | |

| | |

| | | |

| | |

| TOTAL COMMON STOCKS | |

| | | |

| | |

| (COST OF $234,467,614) | |

| | | |

| 335,601,697 | |

| | |

| | | |

| | |

| SHORT TERM INVESTMENTS (2.74%) | |

| | | |

| | |

| MONEY MARKET FUND (2.54%) | |

| | | |

| | |

| State Street Institutional US Government Money Market Fund, Premier Class, 5.31%(d) | |

| | | |

| | |

| (COST OF $8,642,562) | |

| 8,642,562 | | |

| 8,642,562 | |

| | |

| | | |

| | |

| INVESTMENTS PURCHASED WITH COLLATERAL FROM SECURITIES LOANED (0.20%) | |

| | | |

| | |

| State Street Navigator Securities Lending Government Money Market Portfolio, 5.36% | |

| | | |

| | |

| (COST OF $689,791) | |

| 689,791 | | |

| 689,791 | |

| | |

| | | |

| | |

| TOTAL SHORT TERM INVESTMENTS | |

| | | |

| | |

| (COST OF $9,332,353) | |

| | | |

| 9,332,353 | |

| | |

| | | |

| | |

| TOTAL INVESTMENTS (101.32%) | |

| | | |

| | |

| (COST OF $243,799,967) | |

| | | |

| 344,934,050 | |

| | |

| | | |

| | |

| LIABILITIES IN EXCESS OF OTHER ASSETS (-1.32%) | |

| | | |

| (4,484,046 | ) |

| | |

| | | |

| | |

| NET ASSETS (100.00%) | |

| | | |

$ | 340,450,004 | |

| | |

| | | |

| | |

| NET ASSET VALUE PER SHARE | |

| | | |

| | |

| (59,218,601 SHARES OUTSTANDING) | |

| | | |

$ | 5.75 | |

| (a) | Non-income producing security. |

| (b) | Security, or a portion of the security position, is currently on loan. The total market value of securities on loan is $622,870. |

| (c) | American Depositary Receipt. |

| (d) | Rate reflects seven-day effective yield on December 31, 2023. |

See Notes to Financial Statements.

| Annual Report | December 31, 2023 |

23 |

| Liberty All-Star® Growth Fund |

Statement of Assets and Liabilities |

December 31, 2023

| ASSETS: | |

| | |

| Investments at value (Cost $243,799,967)(a) | |

$ | 344,934,050 | |

| Dividends and interest receivable | |

| 120,416 | |

| Tax reclaim receivable | |

| 2,552 | |

| Prepaid and other assets | |

| 65,241 | |

| TOTAL ASSETS | |

| 345,122,259 | |

| | |

| | |

| LIABILITIES: | |

| | |

| Distributions payable to shareholders | |

| 3,531,311 | |

| Investment advisory fee payable | |

| 221,599 | |

| Payable for administration, pricing and bookkeeping fees | |

| 58,024 | |

| Payable for collateral upon return of securities loaned | |

| 689,791 | |

| Accrued Directors’ fees payable | |

| 6,849 | |

| Accrued expenses | |

| 164,681 | |

| TOTAL LIABILITIES | |

| 4,672,255 | |

| NET ASSETS | |

$ | 340,450,004 | |

| | |

| | |

| NET ASSETS REPRESENTED BY: | |

| | |

| Paid-in capital | |

$ | 275,812,951 | |

| Total distributable earnings | |

| 64,637,053 | |

| NET ASSETS | |

$ | 340,450,004 | |

| | |

| | |

Shares of common stock outstanding

(authorized 200,000,000 shares at $0.10 Par) | |

| 59,218,601 | |

| NET ASSET VALUE PER SHARE | |

$ | 5.75 | |

| (a) | Includes securities on loan of $622,870. |

See Notes to Financial Statements.

| Liberty All-Star® Growth Fund |

Statement of Operations |

For the Year Ended December 31, 2023

| INVESTMENT INCOME: | |

| | |

| Dividends (Net of foreign taxes withheld at source which amounted to $8,964) | |

$ | 1,996,315 | |

| Securities lending income | |

| 26,842 | |

| TOTAL INVESTMENT INCOME | |

| 2,023,157 | |

| | |

| | |

| EXPENSES: | |

| | |

| Investment advisory fee | |

| 2,505,758 | |

| Administration, pricing and bookkeeping fees | |

| 629,454 | |

| Audit fee | |

| 19,432 | |

| Custodian fee | |

| 37,941 | |

| Directors’ fees and expenses | |

| 122,183 | |

| Insurance expense | |

| 10,454 | |

| Legal fees | |

| 39,380 | |

| NYSE fee | |

| 64,794 | |

| Proxy fees | |

| 30,893 | |

| Shareholder communication expenses | |

| 23,973 | |

| Transfer agent fees | |

| 81,923 | |

| Miscellaneous expenses | |

| 5,130 | |

| TOTAL EXPENSES | |

| 3,571,315 | |

| NET INVESTMENT LOSS | |

| (1,548,158 | ) |

| | |

| | |

| REALIZED AND UNREALIZED GAIN/(LOSS) ON INVESTMENTS: | |

| | |

| Net realized loss on investments | |

| (8,850,739 | ) |

| Net realized loss on foreign currency transactions | |

| (107 | ) |

| Net change in unrealized appreciation on investments | |

| 66,429,117 | |

| Net change in unrealized depreciation on foreign currency transactions | |

| (11 | ) |

| NET REALIZED AND UNREALIZED GAIN/(LOSS) ON INVESTMENTS | |

| 57,578,260 | |

| NET INCREASE IN NET ASSETS RESULTING FROM OPERATIONS | |

$ | 56,030,102 | |

See Notes to Financial Statements.

| Annual Report | December 31, 2023 |

25 |

| Liberty All-Star® Growth Fund |

Statements of Changes in Net Assets |

| | |

For the

Year Ended

December 31, 2023 | | |

For the

Year Ended

December 31, 2022 | |

| FROM OPERATIONS: | |

| | | |

| | |

| Net investment loss | |

$ | (1,548,156 | ) | |

$ | (2,001,172 | ) |

| Net realized loss on investments | |

| (8,850,848 | ) | |

| (19,749,593 | ) |

| Net change in unrealized appreciation/(depreciation) on investments | |

| 66,429,106 | | |

| (118,492,798 | ) |

| Net Increase/(Decrease) in Net Assets From Operations | |

| 56,030,102 | | |

| (140,243,563 | ) |

| | |

| | | |

| | |

| DISTRIBUTIONS TO SHAREHOLDERS: | |

| | | |

| | |

| From distributable earnings | |

| (1,404,630 | ) | |

| (27,962,642 | ) |

| Return of capital | |

| (23,519,102 | ) | |

| – | |

| Total Distributions | |

| (24,923,732 | ) | |

| (27,962,642 | ) |

| | |

| | | |

| | |

| CAPITAL SHARE TRANSACTIONS: | |

| | | |

| | |

| Dividend reinvestments | |

| 10,391,899 | | |

| 11,196,747 | |

| Net increase resulting from Capital Share Transactions | |

| 10,391,899 | | |

| 11,196,747 | |

| Total Increase/(Decrease) in Net Assets | |

| 41,498,269 | | |

| (157,009,458 | ) |

| | |

| | | |

| | |

| NET ASSETS: | |

| | | |

| | |

| Beginning of year | |

| 298,951,735 | | |

| 455,961,193 | |

| End of year | |

$ | 340,450,004 | | |

$ | 298,951,735 | |

See Notes to Financial Statements.

Intentionally Left Blank

Liberty All-Star®

Growth Fund

Financial Highlights

| PER SHARE OPERATING PERFORMANCE: |

| Net asset value at beginning of year |

| INCOME FROM INVESTMENT OPERATIONS: |

| Net investment loss(a) |

| Net realized and unrealized gain/(loss) on investments |

| Total from Investment Operations |

| |

| LESS DISTRIBUTIONS TO SHAREHOLDERS: |

| Net investment income |

| Net realized gain on investments |

| Return of capital |

| Total Distributions |

| Change due to rights offering(b) |

| Net asset value at end of year |

| Market price at end of year |

| |

| TOTAL INVESTMENT RETURN FOR SHAREHOLDERS:(c) |

| Based on net asset value |

| Based on market price |

| |

| RATIOS AND SUPPLEMENTAL DATA: |

| Net assets at end of period (millions) |

| Ratio of expenses to average net assets |

| Ratio of net investment loss to average net assets |

| Portfolio turnover rate |

| (a) | Calculated using average shares outstanding during the period. |

| (b) | Effect of Fund’s rights offering for shares at a price below net asset value, net of costs. |

| (c) | Calculated assuming all distributions are reinvested at actual reinvestment prices and all primary rights in the Fund’s rights offering

were exercised. The net asset value and market price returns will differ depending upon the level of any discount from or premium to net

asset value at which the Fund’s shares traded during the period. Past performance is not a guarantee of future results. |

See Notes to Financial Statements.

Financial Highlights

| For the Year Ended December 31, | |

| 2023 | | |

2022 | | |

2021 | | |

2020 | | |

2019 | |

| | | |

| | |

| | |

| | |

| |

| $ | 5.23 | | |

$ | 8.25 | | |

$ | 7.98 | | |

$ | 6.19 | | |

$ | 4.94 | |

| | | | |

| | | |

| | | |

| | | |

| | |

| | (0.03 | ) | |

| (0.04 | ) | |

| (0.06 | ) | |

| (0.05 | ) | |

| (0.03 | ) |

| | 0.98 | | |

| (2.48 | ) | |

| 1.46 | | |

| 2.51 | | |

| 1.74 | |

| | 0.95 | | |

| (2.52 | ) | |

| 1.40 | | |

| 2.46 | | |

| 1.71 | |

| | | | |

| | | |

| | | |

| | | |

| | |

| | (0.02 | ) | |

| – | | |

| – | | |

| – | | |

| – | |

| | – | | |

| (0.50 | ) | |

| (1.02 | ) | |

| (0.63 | ) | |

| (0.46 | ) |

| | (0.41 | ) | |

| – | | |

| – | | |

| – | | |

| – | |

| | (0.43 | ) | |

| (0.50 | ) | |

| (1.02 | ) | |

| (0.63 | ) | |

| (0.46 | ) |

| | – | | |

| – | | |

| (0.11 | ) | |

| (0.04 | ) | |

| – | |

| $ | 5.75 | | |

$ | 5.23 | | |

$ | 8.25 | | |

$ | 7.98 | | |

$ | 6.19 | |

| $ | 5.28 | | |

$ | 4.93 | | |

$ | 9.00 | | |

$ | 8.20 | | |

$ | 6.50 | |

| | | | |

| | | |

| | | |

| | | |

| | |

| | 19.4 | % | |

| (31.0 | %) | |

| 18.1 | % | |

| 42.4 | % | |

| 35.8 | % |

| | 16.3 | % | |

| (40.4 | %) | |

| 25.4 | % | |

| 39.4 | % | |

| 60.5 | % |

| | | | |

| | | |

| | | |

| | | |

| | |

| $ | 340 | | |

$ | 299 | | |

$ | 456 | | |

$ | 338 | | |

$ | 235 | |

| | 1.13 | % | |

| 1.14 | % | |

| 1.12 | % | |

| 1.20 | % | |

| 1.22 | % |

| | (0.49 | %) | |

| (0.60 | %) | |

| (0.66 | %) | |

| (0.69 | %) | |

| (0.57 | %) |

| | 39 | % | |

| 31 | % | |

| 42 | % | |

| 55 | % | |

| 34 | % |

| Annual Report | December 31, 2023 |

29 |

| Liberty All-Star® Growth Fund |

Notes to Financial Statements |

December 31, 2023

NOTE 1. ORGANIZATION

Liberty All-Star® Growth Fund,

Inc. (the “Fund”) is a Maryland corporation registered under the Investment Company Act of 1940 (the “1940 Act”),

as amended, as a diversified, closed-end management investment company.

Investment Goal

The Fund seeks long-term capital appreciation.

Fund Shares

The Fund may issue 200,000,000 shares of common stock at $0.10 par.

NOTE 2. SIGNIFICANT ACCOUNTING POLICIES

The following is a summary of significant accounting

policies consistently followed by the Fund in the preparation of its financial statements. The Fund is considered an investment company

under U.S. generally accepted accounting principles (“GAAP”) and follows the accounting and reporting guidance applicable

to investment companies in the Financial Accounting Standards Board Accounting Standards Codification Topic 946 Financial Services

- Investment Companies.

Use of Estimates

The preparation of financial statements in conformity

with GAAP requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities and disclosures

of contingent assets and liabilities at the date of the financial statements and the reported amounts of increases and decreases in net

assets from operations during the reporting period. Actual results could differ from these estimates.

Security Valuation

Equity securities are valued at the last sale

price at the close of the principal exchange on which they trade, except for securities listed on the NASDAQ Stock Market LLC (“NASDAQ”),

which are valued at the NASDAQ official closing price. Unlisted securities or listed securities for which there were no sales during the

day are valued at the closing bid price on such exchanges or over-the-counter markets.

Cash collateral from securities lending activity

is reinvested in the State Street Navigator Securities Lending Government Money Market Portfolio (“State Street Navigator”),

a registered investment company under the 1940 Act, which operates as a money market fund in compliance with Rule 2a-7 under the 1940

Act. Shares of registered investment companies are valued daily at that investment company’s net asset value (“NAV”) per

share.

The Fund’s investments are valued at market

value or, in the absence of market value with respect to any portfolio securities, at fair value according to procedures adopted by the

Fund’s Board of Directors (the “Board”). The Board has designated ALPS Advisors, Inc. (the “Advisor”) as the Fund’s

Valuation Designee (as defined in Rule 2a-5 under the 1940 Act). The Valuation Designee is responsible for determining fair value in good

faith for all Fund investments, subject to oversight by the Board. When market quotations are not readily available, or in management’s

judgment they do not accurately reflect fair value of a security, or an event occurs after the market close but before the Fund is priced

that materially affects the value of a security, the security will be valued by the Advisor’s Valuation Committee, using fair valuation

procedures established by the Valuation Designee. Examples of potentially significant events that could materially impact a Fund’s

net asset value include, but are not limited to: single issuer events such as corporate actions, reorganizations, mergers, spin-offs,

liquidations, acquisitions and buyouts; corporate announcements on earnings or product offerings; regulatory news; and litigation and

multiple issuer events such as governmental actions; natural disasters or armed conflicts that affect a country or a region; or significant